Gamma and Delta are two of the most important option greeks.

Here's how they work:

Here's how they work:

1. By the end of this thread, you'll have mastered:

· Delta

· Gamma

· Dealer Exposure

Let's dive in!

· Delta

· Gamma

· Dealer Exposure

Let's dive in!

2. What is Delta?

The formal definition of delta is that it is the change in option price per change in the price of the stock.

Calls have positive delta.

Puts have negative delta.

The formal definition of delta is that it is the change in option price per change in the price of the stock.

Calls have positive delta.

Puts have negative delta.

3. Delta is not a constant number — it varies as the difference between the price of the stock and the strike being considered in the option - their difference.

4. Delta is about 50 per contract when the strike price of the option and the spot price are the same.

For example, if the current spot price is $100, then the delta of a 100-strike contract will be about 50.

For example, if the current spot price is $100, then the delta of a 100-strike contract will be about 50.

5. This is also called a “50-delta”, as it represents 100 shares/contract * 0.50 delta/share= 50 delta/contract.

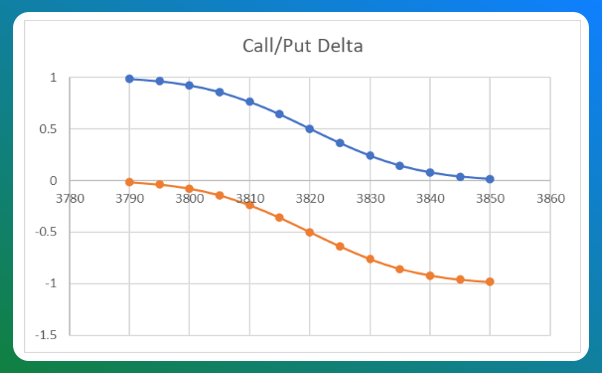

6. Here's an example:

The strike price is 3820, & you can see that for the calls (blue), the delta is 0.5 per contract or 0.5 / contract * 100 shares / contract = 50 shares.

You can also see that for puts the value is negative at -0.50 but the shapes are equivalent as shown.

The strike price is 3820, & you can see that for the calls (blue), the delta is 0.5 per contract or 0.5 / contract * 100 shares / contract = 50 shares.

You can also see that for puts the value is negative at -0.50 but the shapes are equivalent as shown.

7. Now, what is Gamma?

8. Gamma is the change in delta as the price of the stock changes.

Long option contracts (puts and calls) have positive gamma.

Short option contracts have negative gamma. This will become important later.

Long option contracts (puts and calls) have positive gamma.

Short option contracts have negative gamma. This will become important later.

9. Gamma is a measure of change — you’ll often hear the word convexity — and it is at a peak value near the at-the-money (ATM) strike.

10. Gamma is influenced by many things, the primary influences being the current spot price and the other being the days-to-expiration (DTE) of the contract.

11. The further away from a strike the current price is the lower the gamma, and the further out in time the DTE of the contract, the lower the amount of gamma.

As DTE approaches zero, gamma grows larger, which is why we pay attention to 0DTE, 1DTE, etc. trading plays.

As DTE approaches zero, gamma grows larger, which is why we pay attention to 0DTE, 1DTE, etc. trading plays.

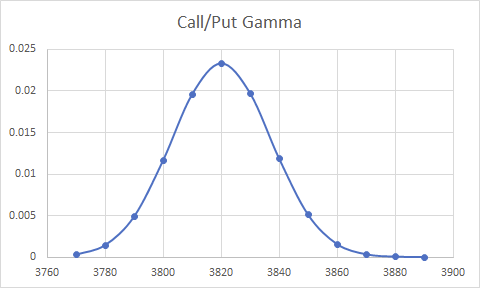

12. Here is that same option, but now in context of gamma;

13. Note how the gamma function peaks at 3820 and falls off on either side. This is why people buy out-of-the-money (OTM) options -- as they approach a strike from above or below, the impact of gamma can have a large impact on the change in their delta.

14. But how is this knowledge useful?

Every action you take falls on a dealer, who also has delta and gamma exposure.

The changes in their exposure play a key role in how large, liquid stocks perform!

What is dealer exposure? 👇

Every action you take falls on a dealer, who also has delta and gamma exposure.

The changes in their exposure play a key role in how large, liquid stocks perform!

What is dealer exposure? 👇

15. When you open a long call with your broker/dealer, there is an associated delta with that long call that you now own. Let’s presume that it is a 50-delta contract (completely arbitrary).

16. There is a dealer on the other side of your transaction, and their business model is to sell you that long call. In the process of doing this, they become short that call, and their “shortness” is -50-delta (negative because they are short).

17. At this point, their exposure to the market is the same as having 50 short shares of the stock or stock asset, which means that if the stock goes up in price, they lose money.

18. Directionality is bad for business (think JPM, Goldman, Citidel, etc.), so they seek to reduce this directionality.

19. Hence, to hedge this short (negative) delta exposure the broker/dealer/market maker (MM) will buy 50 shares (long) of the stock or correlated asset (often futures), effectively neutralizing their exposure.

20. This is because when you are long stock you are long delta, and buying 50 shares is +50-delta, combined with the -50-delta, is a net zero delta.

21. What is important here is that YOU bought a 50-delta long call, and the dealer response is to 1) sell you that call (now they are short 50 delta) AND 2) they must buy 50 shares of the stock to hedge their position. What happens when they buy?

22. Remember -- they care about delta, not price. Hence, they buy buy buy.... and the price goes up.

23. The converse of this is true too if you open a long put. The reaction to hedge flat is that the dealer must sell.

24. Now, multiply this by large orders, all buying calls, or all buying puts. Now you can see where the dealer response is important. Depending on the market, the dealers respond, and if we track this, we can get a good feel for what the next few moves could be...

I hope you've found this thread helpful.

Follow us @GammaEdges for more content on the stock market.

Like/Retweet the first tweet below:

Follow us @GammaEdges for more content on the stock market.

Like/Retweet the first tweet below:

Loading suggestions...