Key highlights from Chemcon Specialty Chemicals Q2FY23 concall🧪🧪

CMP - ₹298

Like and retweet for maximum reach!!

CMP - ₹298

Like and retweet for maximum reach!!

The business performance has been slow in this quarter in the domestic market due to lower volume demand from the pharma clients of the company. The downturn in the domestic market was offset by strong demand in the export market. The pharma clients of the company are facing

adverse price issues on the formulation side which has led to softening of the demand

Inorganic bromides have also been affected due to the irregular sourcing of the key raw material bromine

Inorganic bromides have also been affected due to the irregular sourcing of the key raw material bromine

The company has acquired a new land parcel at Gothada near Vadodara at a cost of Rs 21 crore. This land parcel will be used for capacity expansions which will be the future growth leg of the company

The company has also invested in a 2.1MW solar power plant at Dabhoi which is

The company has also invested in a 2.1MW solar power plant at Dabhoi which is

about 30 km away from Vadodara to reduce dependence on non-renewable energy sources. This power plant is estimated to save power costs for the company in the range of Rs 50 to 60 lakhs every quarter

The company procures methyl chloroformate from Paushak which is the raw material for CMIC manufacturing. The company is getting regular supplies of this raw material and the majority of this raw material is procured domestically. The company procures only 10-15 % of this raw

material from China to maintain a parallel supply. The company supplies CMIC to 4 major users in China of which 2 are the company’s customers and the company is in discussion with the other 2 users for customer acquisition

For HMDS, the company procures it only from the international markets with 70% coming from China and the remaining amount coming from other countries

The company also makes high-purity HMDS however it has been facing issues in selling it to the semiconductor industry. The company right now has got approval for supplies in Europe and Japan and is selling to these markets in silicon rubber applications.

The margins here are at par with the semiconductor industry

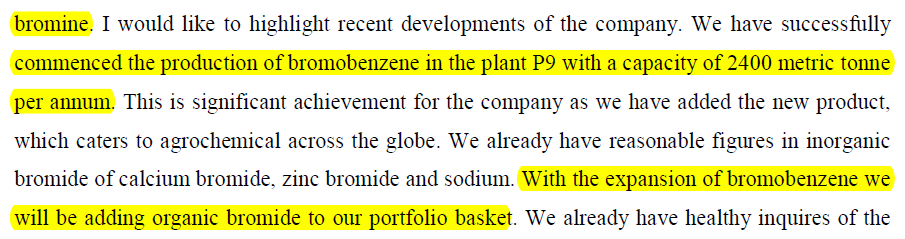

The company successfully commissioned its bromobenzene capacity of 2400 MTPA which will be made in its P9 plant. This product is a key intermediate for agrochemical industry across the globe. The company was present only in inorganic bromides like calcium bromide, zinc bromide

and sodium bromide. The addition of bromobenzene will help the company to get into organic bromides

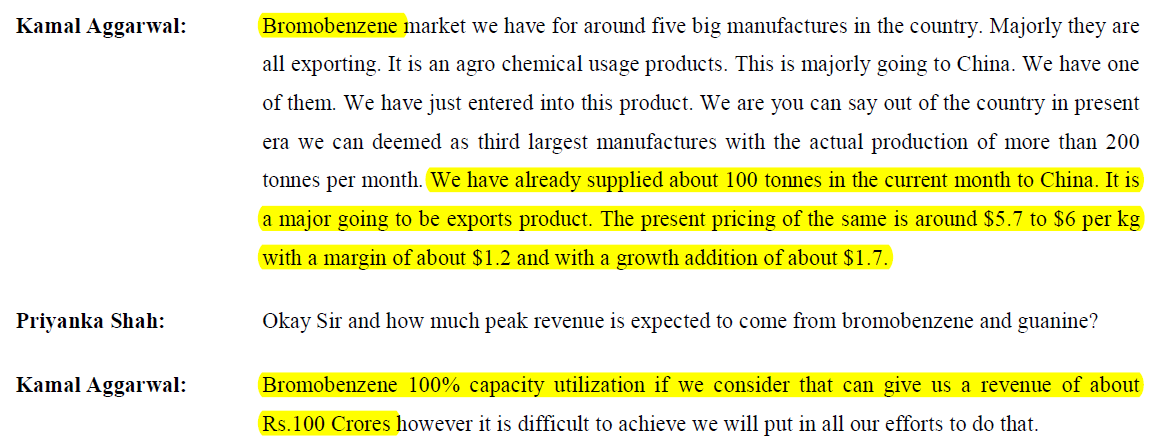

The company has already supplied 100 tons of bromobenzene in the current month to China. The pricing of this product is around $5.7 to $6/kg with a margin of $1.2.Bromobenzene at peak capacity utilization is expected to give a revenue of about Rs 100 crores

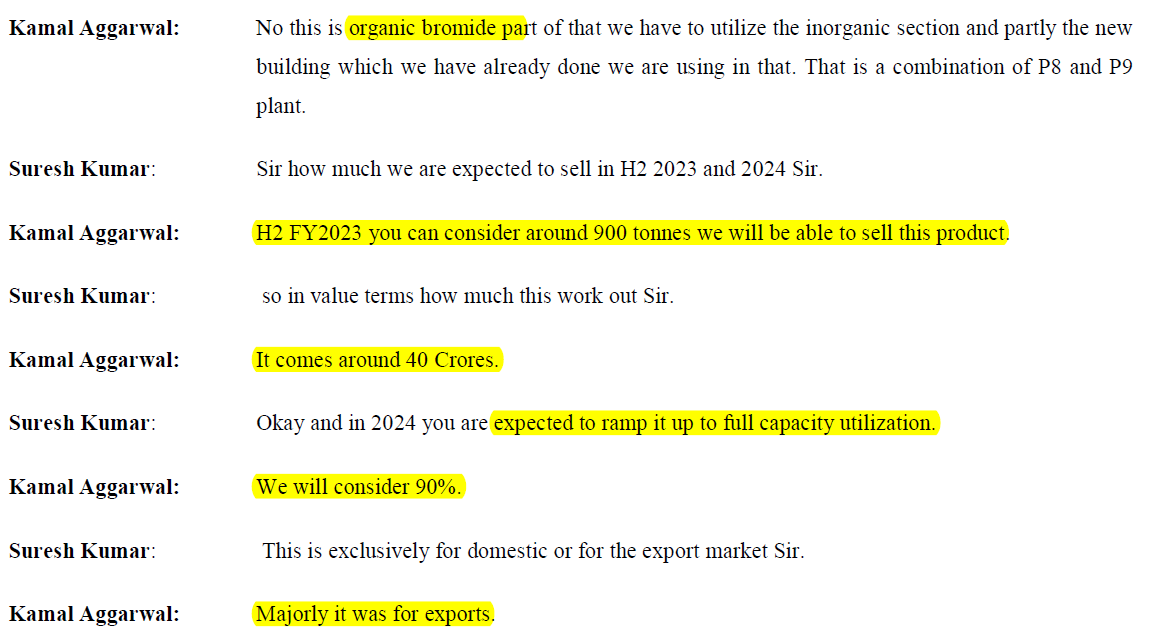

The company plans to sell Rs 40 crore or 900 tons of organic bromides in H2FY23.The company will ramp up the capacity to 90% by 2024 and this organic bromides will cater to the export market

The P10 facility will be used for the manufacturing of intermediate guanine which is used in pharma and agro industries and is currently being imported in India. The P10 facility is expected to come online in Q1FY24 with a capacity of 600 TPA

The company has nearly achieved import substitution for HMDS and CMIC and plans to do the same with guanine once its facility comes online

The company is planning to discontinue the DHT and CBC products as they were not able to penetrate into the supply chain

The company is planning to discontinue the DHT and CBC products as they were not able to penetrate into the supply chain

Loading suggestions...