Samvardhana Motherson International Limited Analysis! 🇮🇳

A Detailed Thread🧵⬇️

#investing #StocksToBuy

A Detailed Thread🧵⬇️

#investing #StocksToBuy

(1/17)

About:

SAMIL was incorporated as MSSL, the flagship company of the Motherson group, as a JV between SAMIL and Japan-based Sumitomo Wiring Systems.

It is a globally diversified manufacturer & a full system solutions provider to

customers in automotive & other industries.

About:

SAMIL was incorporated as MSSL, the flagship company of the Motherson group, as a JV between SAMIL and Japan-based Sumitomo Wiring Systems.

It is a globally diversified manufacturer & a full system solutions provider to

customers in automotive & other industries.

(2/17)

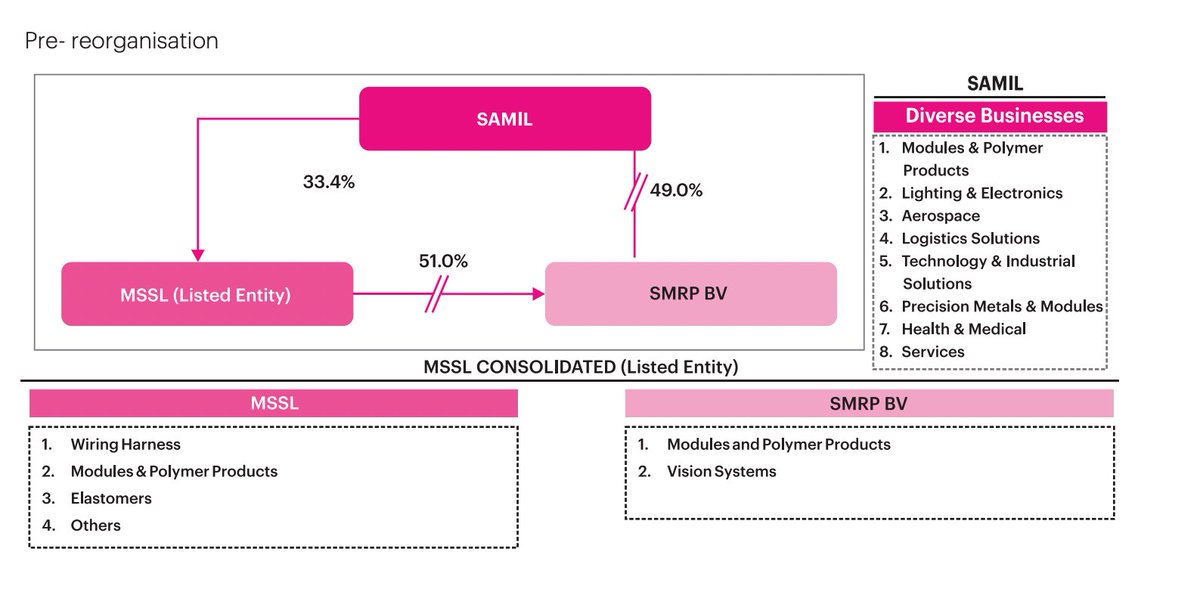

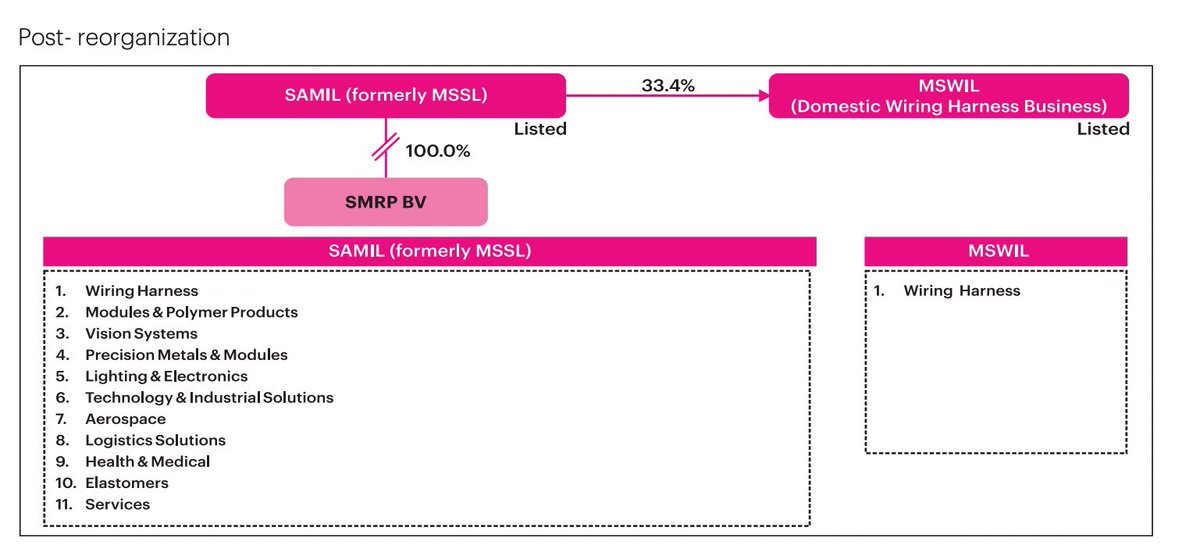

Understanding The Structure

Understanding The Structure

(3/17)

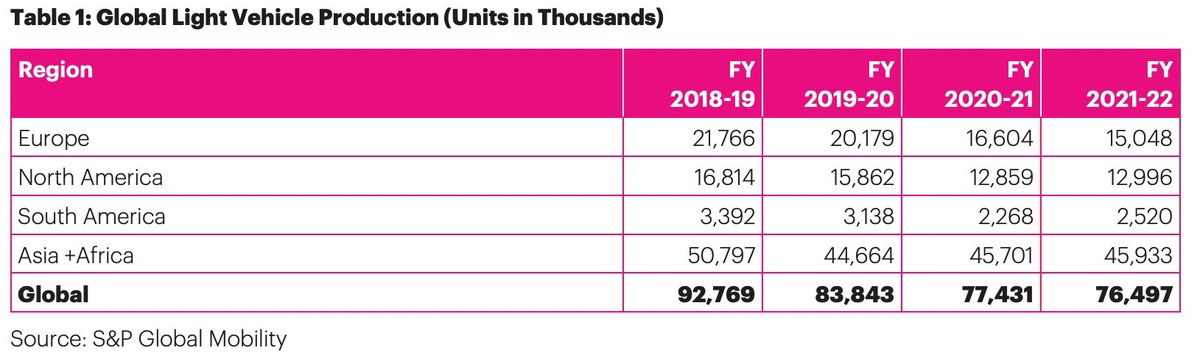

Global Automotive Industry:

The Global LV Production has seen a drop from 92 Mn Units in FY19 to 76 Mn Units in FY22 due to headwinds such as chip shortages, COVID-19, & geo-political disruptions resulting in irregular production & line stoppages by OEMs globally.

Global Automotive Industry:

The Global LV Production has seen a drop from 92 Mn Units in FY19 to 76 Mn Units in FY22 due to headwinds such as chip shortages, COVID-19, & geo-political disruptions resulting in irregular production & line stoppages by OEMs globally.

(4/17)

Outlook:

Various agencies are forecasting global light vehicle production volumes to rebound to approx. 94 Mn units by FY25- 26.

The volume growth is

premised on continuous demand, normalization of supply chain challenges and recovery of the global economy.

Outlook:

Various agencies are forecasting global light vehicle production volumes to rebound to approx. 94 Mn units by FY25- 26.

The volume growth is

premised on continuous demand, normalization of supply chain challenges and recovery of the global economy.

(5/17)

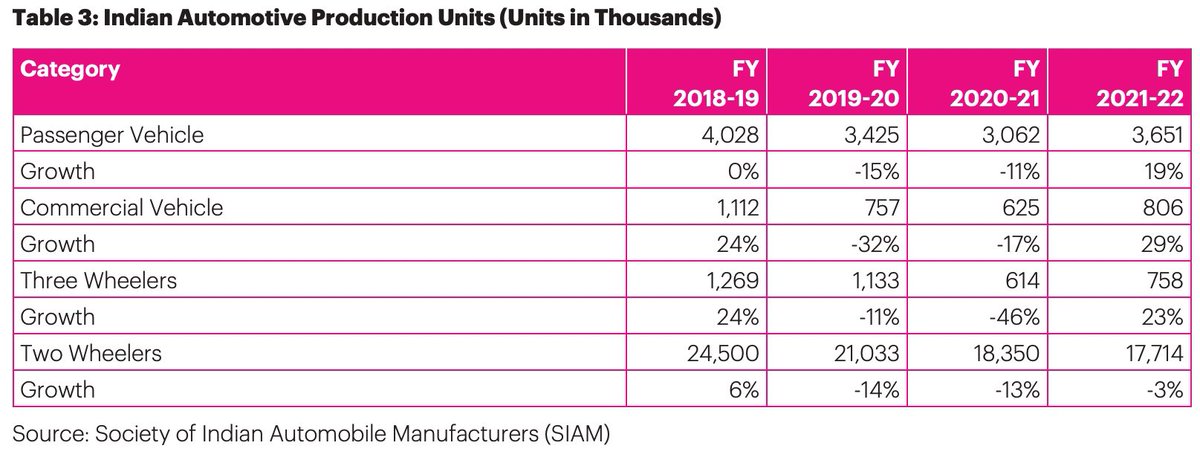

• India Outlook:

The Indian Automative Industry has shown signs of recovery from supply chain induced challenges.

It has been incentivized by the GOI with the Automotive PLI scheme which are expected to result in further investments in the country in the future.

• India Outlook:

The Indian Automative Industry has shown signs of recovery from supply chain induced challenges.

It has been incentivized by the GOI with the Automotive PLI scheme which are expected to result in further investments in the country in the future.

(6/17)

Company’s Vision 2025:

• $36 bn revenues in FY25 with 40% RoCE

• 3CX10: No Country, Customer or Component should contribute more than 10% to the revenue

• 75% of revenues from the automotive industry, 25%

from new divisions

• Up to 40% of profit as dividend

Company’s Vision 2025:

• $36 bn revenues in FY25 with 40% RoCE

• 3CX10: No Country, Customer or Component should contribute more than 10% to the revenue

• 75% of revenues from the automotive industry, 25%

from new divisions

• Up to 40% of profit as dividend

(7/17)

Key Clients: (High to low Revenue Share)

• Mercedes Benz

• Audi

• Volkswagen

• Suzuki

• BMW

• Porsche

• Daimler trucks

• Hyundai

• Renault

• Paccar

• PSA Group

• Ford

• Scania

• John Deere

• Volvo Trucks

Key Clients: (High to low Revenue Share)

• Mercedes Benz

• Audi

• Volkswagen

• Suzuki

• BMW

• Porsche

• Daimler trucks

• Hyundai

• Renault

• Paccar

• PSA Group

• Ford

• Scania

• John Deere

• Volvo Trucks

(8/17)

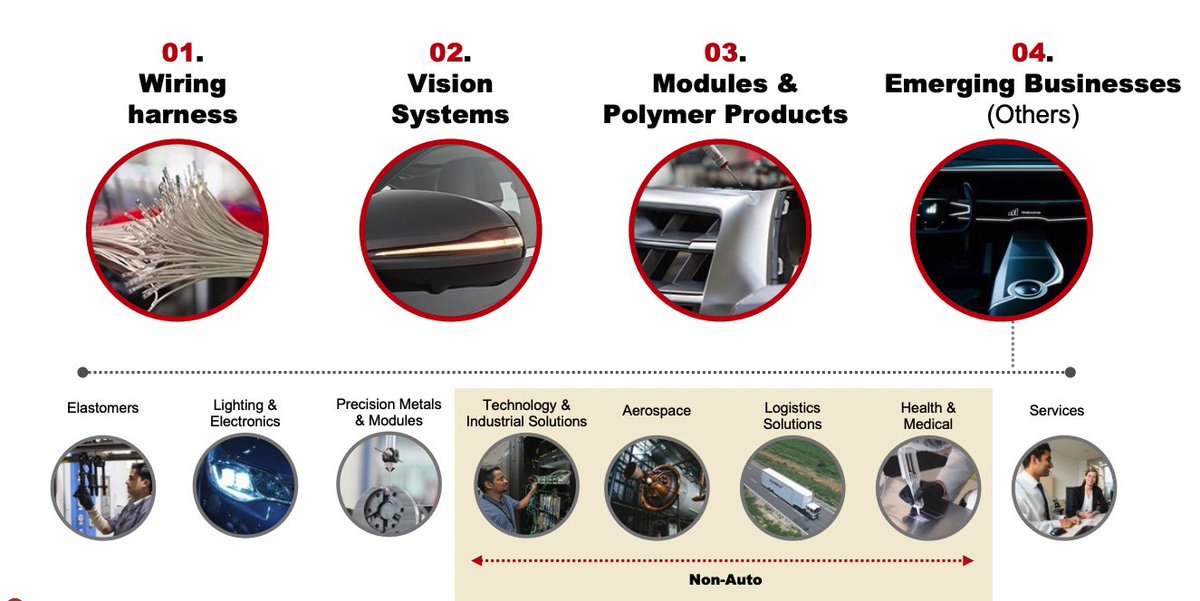

• Products it deals in:

• Wiring Harness

• Bumpers

• Vision Systems

• Door Panels

• Instrument Panel

• Engineering

• Other Polymer Products

• Non-Automative

• Others

• Products it deals in:

• Wiring Harness

• Bumpers

• Vision Systems

• Door Panels

• Instrument Panel

• Engineering

• Other Polymer Products

• Non-Automative

• Others

(9/17)

Wiring Harness Division:

• Revenue Share - 30% (Largest)

• Company is Working on launches of new large programs in Europe and India

• Company believes that Passenger vehicle market in India will remain robust.

• Also Commodity price cooling off provide tailwind

Wiring Harness Division:

• Revenue Share - 30% (Largest)

• Company is Working on launches of new large programs in Europe and India

• Company believes that Passenger vehicle market in India will remain robust.

• Also Commodity price cooling off provide tailwind

(10/17)

• Key Strengths:

Diversified Business Profile:

SAMIL has a diversified revenue base with regard to its customers, geographies and products, and a global manufacturing footprint, mitigating the risks arising from cyclicality, regulatory and technological aspects.

• Key Strengths:

Diversified Business Profile:

SAMIL has a diversified revenue base with regard to its customers, geographies and products, and a global manufacturing footprint, mitigating the risks arising from cyclicality, regulatory and technological aspects.

(11/17)

• Leadership

1. SMR is a global leader in the external rear-view mirror segment.

2. SMP is a leading player in polymer modules in the PV premium segment in Europe.

3. PKC is a leading player in the CV wiring harness markets in North America & Europe.

• Leadership

1. SMR is a global leader in the external rear-view mirror segment.

2. SMP is a leading player in polymer modules in the PV premium segment in Europe.

3. PKC is a leading player in the CV wiring harness markets in North America & Europe.

(12/17)

• Long-standing Relationship:

SAMIL has longstanding relationships with key OEMs globally, including the VW group, Daimler, Renault-Nissan & Hyundai.

The strong business relationships enable the group to mitigate competitive & profitability pressure.

• Long-standing Relationship:

SAMIL has longstanding relationships with key OEMs globally, including the VW group, Daimler, Renault-Nissan & Hyundai.

The strong business relationships enable the group to mitigate competitive & profitability pressure.

(13/17)

Weakness:

Cooling of Profitability:

The company is witnessing a downward trend in its profit margin owing to the various headwinds that the automative sector is facing like significant increase in the RM prices, supply chain disruptions, & higher energy costs.

Weakness:

Cooling of Profitability:

The company is witnessing a downward trend in its profit margin owing to the various headwinds that the automative sector is facing like significant increase in the RM prices, supply chain disruptions, & higher energy costs.

(14/17)

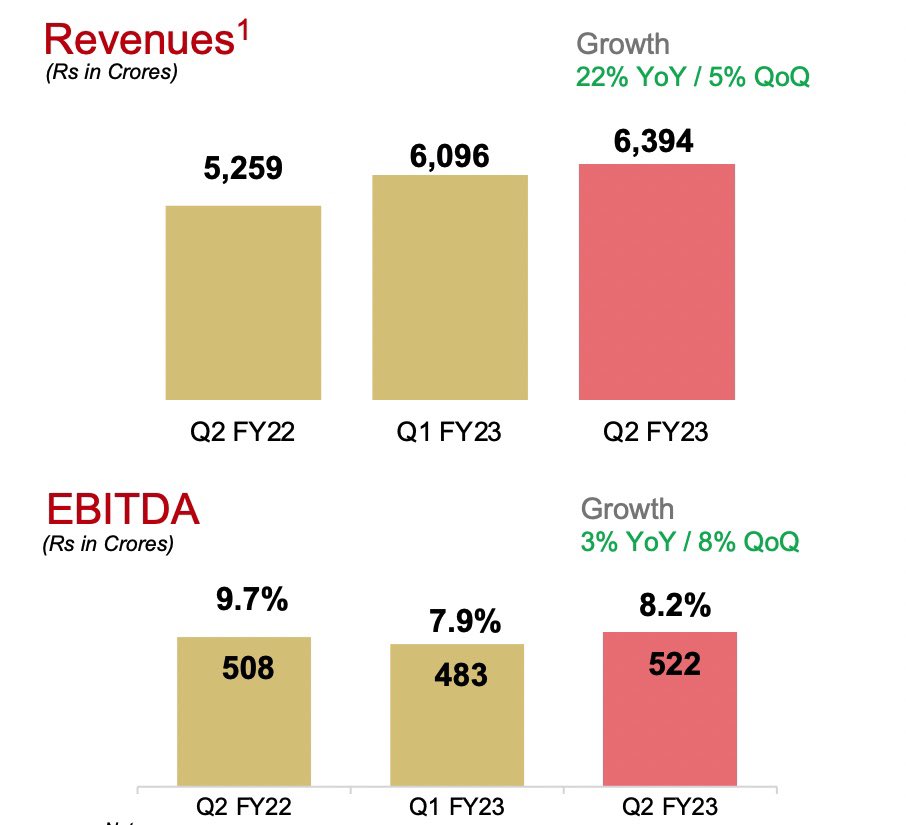

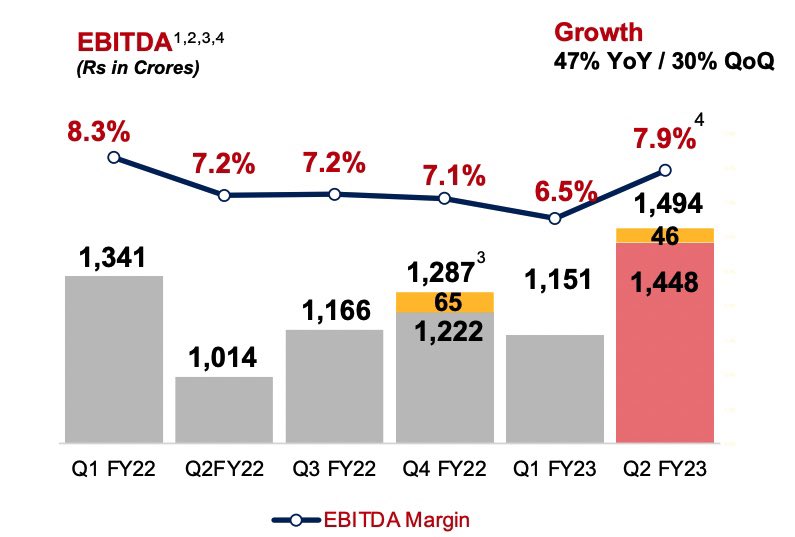

The company saw an improvement in its EBITDA Margins in Q2FY23 which is a positive for the company.

The company saw an improvement in its EBITDA Margins in Q2FY23 which is a positive for the company.

(15/17)

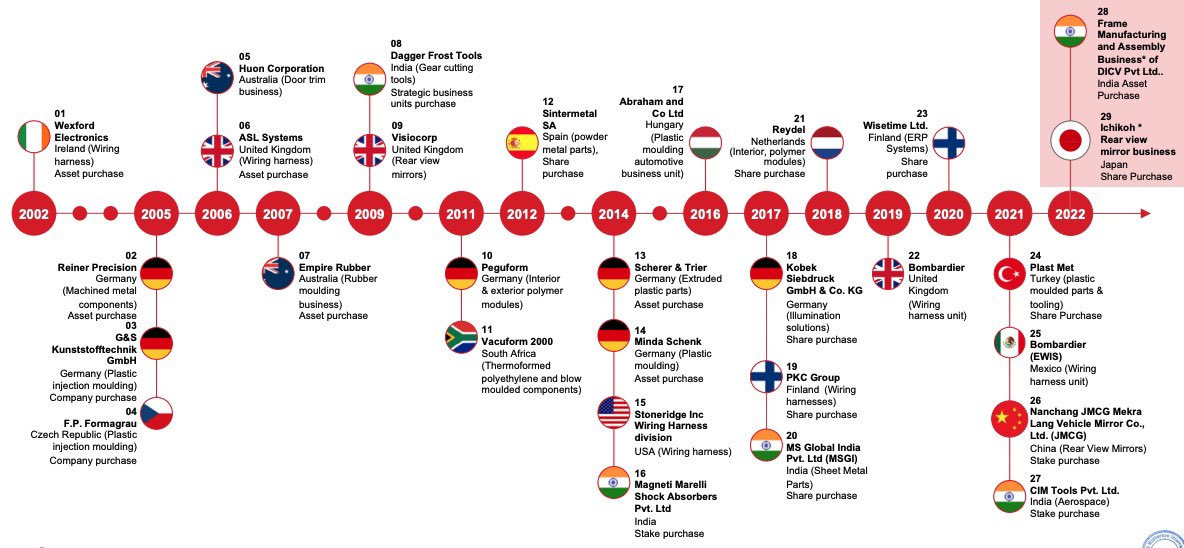

Other points:

• Inventory on the rise, in order to mitigate supply crunch.

• Company focusing on both organic through greenfield expansion and inorganic growth through M&As (picture below)

• 37% of the current order book comes from EVs up from 27% as on 31.03.22

Other points:

• Inventory on the rise, in order to mitigate supply crunch.

• Company focusing on both organic through greenfield expansion and inorganic growth through M&As (picture below)

• 37% of the current order book comes from EVs up from 27% as on 31.03.22

(16/17)

Key Ratios & Numbers:

• Market Cap: ₹ 47,570 Cr

• Stock P/E: 58.6 vs Ind P/E: 23.71

• RoE: 5.4%

• RoCE: 8.09%

• Sales 3 year CAGR: 0.01%

• Price to Sales: 0.69

• NPM Last year: 1.92%

• OPM Q2FY23: 8%

• D/E: 0.68

• Dividend Yield: 0.61%

Key Ratios & Numbers:

• Market Cap: ₹ 47,570 Cr

• Stock P/E: 58.6 vs Ind P/E: 23.71

• RoE: 5.4%

• RoCE: 8.09%

• Sales 3 year CAGR: 0.01%

• Price to Sales: 0.69

• NPM Last year: 1.92%

• OPM Q2FY23: 8%

• D/E: 0.68

• Dividend Yield: 0.61%

(17/17)

Shareholding Pattern:

• Promoters: 68.16%

• FIIs: 8.76%

• DIIs: 10.48%

• Public: 12.53%

Watch out for its profit margins in the coming quarters as RM prices cool off.

@caniravkaria @kuttrapali26 @chartmojo

Shareholding Pattern:

• Promoters: 68.16%

• FIIs: 8.76%

• DIIs: 10.48%

• Public: 12.53%

Watch out for its profit margins in the coming quarters as RM prices cool off.

@caniravkaria @kuttrapali26 @chartmojo

Loading suggestions...