Detailed analysis on Divi’s Laboratories - A Mega Cap Compounding Machine

CMP - ₹3498

Like and retweet for maximum reach!!

CMP - ₹3498

Like and retweet for maximum reach!!

1. Company Overview

-Divi’s Labs is one of the largest suppliers of APIs and intermediates globally.

-They have a dominant share in several generic APIs like Naproxen, Dextromethorphan, Levetiracetam and Gabapentin. They have achieved market leadership in these products through

-Divi’s Labs is one of the largest suppliers of APIs and intermediates globally.

-They have a dominant share in several generic APIs like Naproxen, Dextromethorphan, Levetiracetam and Gabapentin. They have achieved market leadership in these products through

their focus on green chemistry, backward integration and scale.

-Apart from generic APIs, Divi’s also provides custom synthesis services to innovative pharma companies.

-They are also present in the Nutraceuticals business where they supply the ingredients which are used in the

-Apart from generic APIs, Divi’s also provides custom synthesis services to innovative pharma companies.

-They are also present in the Nutraceuticals business where they supply the ingredients which are used in the

food, beverages, health supplements and animal feed industries

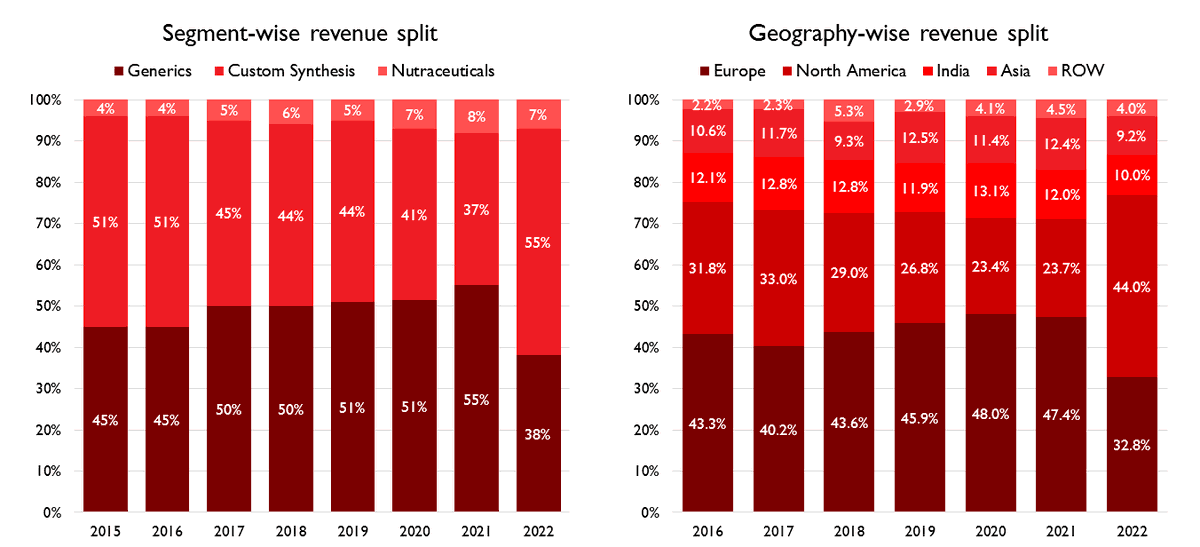

2. Revenue Split

-In FY22, they got 38% of their revenues from their Generic API business, 55% from the Custom Synthesis business and 7% from the Nutraceuticals business

2. Revenue Split

-In FY22, they got 38% of their revenues from their Generic API business, 55% from the Custom Synthesis business and 7% from the Nutraceuticals business

-The company usually tries to keep the contribution from Generic API and Custom Synthesis equal. But in FY22, they manufactured and supplied Molnupiravir which was a Covid drug under their customer synthesis division. This increased the contribution from the Custom Synthesis

division during the year

-The company’s products are primarily exported to regulated markets. Europe and North America are their largest markets which make up 70-75% of their revenues. This is followed by India. Asia and the rest of the world

-The company’s products are primarily exported to regulated markets. Europe and North America are their largest markets which make up 70-75% of their revenues. This is followed by India. Asia and the rest of the world

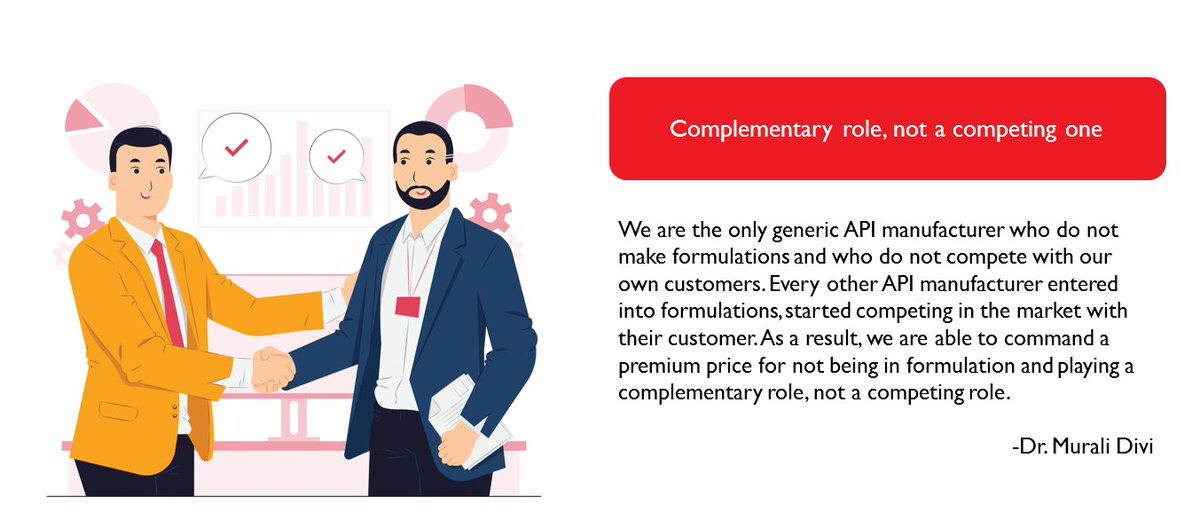

3. Not competing with the customer

-Divi’s does not want to compete with their customers but they want to be a partner to all the formulation companies

-Divi’s does not want to compete with their customers but they want to be a partner to all the formulation companies

-Divi’s started their business at a time when large pharma companies used to manufacture their own APIs for backward integration. They would sell their surplus supply to each other. But this created a conflict as they were also competing with their customers

-So Divi’s was able to gain significant market share by not entering into formulations and supplying APIs to all the formulation players.

-Even today, we see players like Laurus Labs, who started by gaining significant market share in the API and then forward integrating into

-Even today, we see players like Laurus Labs, who started by gaining significant market share in the API and then forward integrating into

formulations. While it does give them better margins, it creates a conflict where they are competing with their customers for the same products.

-Divi’s has said they will never enter into formulations. They want to play a complementary role and not a competing one.

-Divi’s has said they will never enter into formulations. They want to play a complementary role and not a competing one.

4. Green chemistry

-Divi’s biggest strength is their mastery of green chemistry. The company tries to follow the principles of green chemistry

-For example, the company used enzymes instead of chemical catalysts for manufacturing Naproxen. This enabled them to have much higher

-Divi’s biggest strength is their mastery of green chemistry. The company tries to follow the principles of green chemistry

-For example, the company used enzymes instead of chemical catalysts for manufacturing Naproxen. This enabled them to have much higher

yields and less waste.

-We see other examples where the company follows the 12 principles of green chemistry like Atom Economy - where they try to maximize the use of every atom that is used as an input. So the waste generated is reduced.

-They have also designed their rectors

-We see other examples where the company follows the 12 principles of green chemistry like Atom Economy - where they try to maximize the use of every atom that is used as an input. So the waste generated is reduced.

-They have also designed their rectors

to be very energy efficient, which reduces their input costs.

5. Key Products

-The key products of the company are Naproxen, Dextromethorphan, Levetiracetam and Gabapentin. Divi’s has between 50-70% market share in these products.

5. Key Products

-The key products of the company are Naproxen, Dextromethorphan, Levetiracetam and Gabapentin. Divi’s has between 50-70% market share in these products.

-These were the products that they first entered into with the most efficient process and they now have a dominant market share in these products.

-Their strategy is to become the lowest cost producer of a product by having the most efficient process through green chemistry and

-Their strategy is to become the lowest cost producer of a product by having the most efficient process through green chemistry and

technology. Then they backward integrate up to the starting materials so that they can maintain their leadership position and ensure security of supply.

-Other key products that the company is present in are Pregabalin, Mesalamine, Levodopa and Valsartan.

Divi’s has about 20-30%

-Other key products that the company is present in are Pregabalin, Mesalamine, Levodopa and Valsartan.

Divi’s has about 20-30%

market share in these products. These are products where they have entered more recently

-An interesting thing to note about these products is that they are for chronic diseases. The demand for drugs like Naproxen, Gabapentin, Pregabalin, Valsartan and Mesalamine is not going

-An interesting thing to note about these products is that they are for chronic diseases. The demand for drugs like Naproxen, Gabapentin, Pregabalin, Valsartan and Mesalamine is not going

away anytime soon.

-They are high volume products with very stable demand. So this is a very secure business for the company

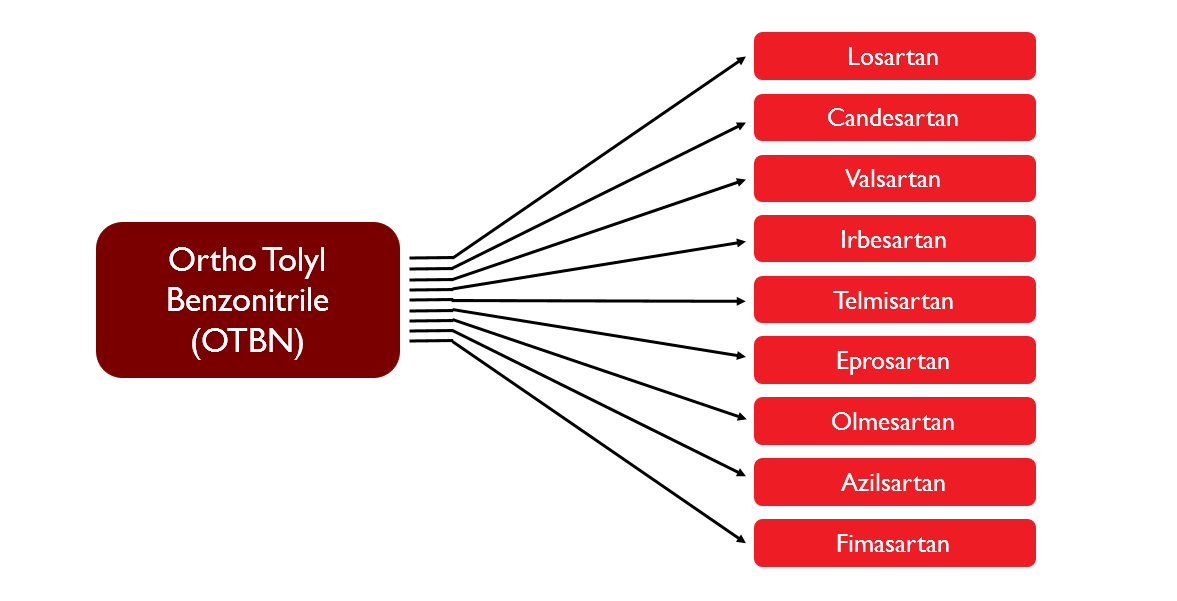

6. Sartans

-Sartans are also known as Angiotensin 2 receptor blockers. They are a class of drugs that are primarily used to treat hypertension, which is

-They are high volume products with very stable demand. So this is a very secure business for the company

6. Sartans

-Sartans are also known as Angiotensin 2 receptor blockers. They are a class of drugs that are primarily used to treat hypertension, which is

high blood pressure.

-Divi’s manufactures a range of sartans including Losartan, Valsartan, Olmesartan, Telmisartan and Irbesartan. Similar to their strategy, they have a more efficient manufacturing process for producing sartans.

-So just like their key products, these are also

-Divi’s manufactures a range of sartans including Losartan, Valsartan, Olmesartan, Telmisartan and Irbesartan. Similar to their strategy, they have a more efficient manufacturing process for producing sartans.

-So just like their key products, these are also

drugs used to treat a chronic disease. So they are high volume products. So Divi’s can benefit from their massive scale to produce these drugs economically.

-An interesting thing that happened with Sartans in 2019 was that the US FDA found NDMA impurities in a lot of drugs

-An interesting thing that happened with Sartans in 2019 was that the US FDA found NDMA impurities in a lot of drugs

including the Sartan drugs.

-NDMA is a compound that falls under a group of compounds known as N-Nitrosamines. They are incredibly toxic compounds which can cause liver damage and even cancer.

-So the US FDA recalled many of the sartan products where these NDMA impurities were

-NDMA is a compound that falls under a group of compounds known as N-Nitrosamines. They are incredibly toxic compounds which can cause liver damage and even cancer.

-So the US FDA recalled many of the sartan products where these NDMA impurities were

detected. Divi’s was the only manufacturer where the NDMA impurity was not detected in their Sartan products.

-This is because their manufacturing process was different than the other API manufacturers and NDMA was not formed in the drug through their manufacturing process.

-This is because their manufacturing process was different than the other API manufacturers and NDMA was not formed in the drug through their manufacturing process.

-They are also backward integrated in Sartan products where they manufacture the starting material known as Ortho Tolyl Benzonitrile or OTBN.

-And the starting material of all sartans is the same which is OTBN. So Divi’s is entering the whole sartan range of products as they are

-And the starting material of all sartans is the same which is OTBN. So Divi’s is entering the whole sartan range of products as they are

fully backward integrated and have the best manufacturing process

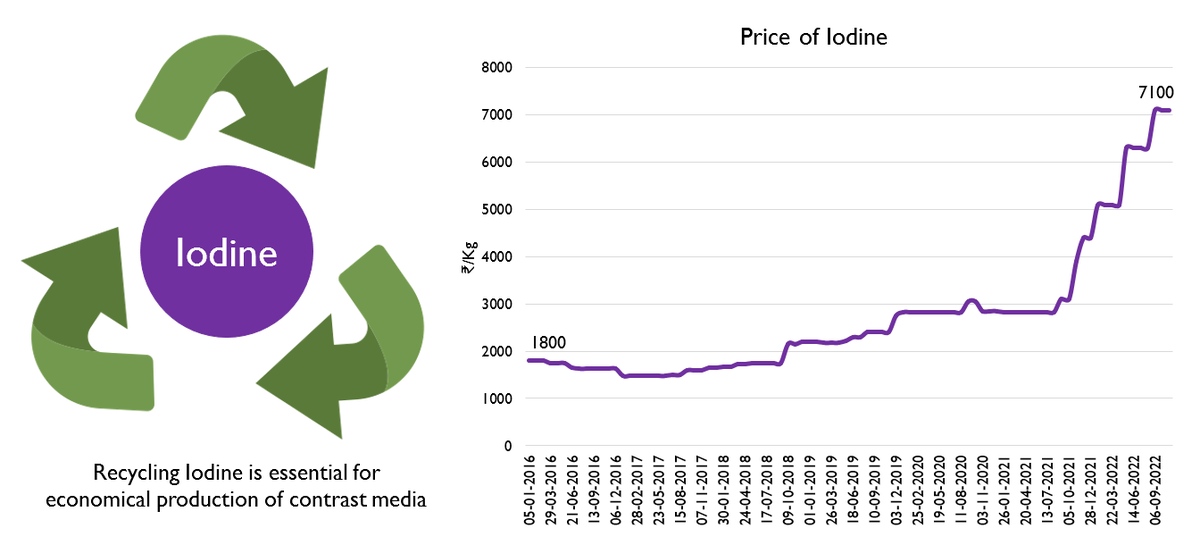

7. Contrast Media

-Contrast media are substances that make certain body parts look different when they are subjected to imaging tools like X-Rays.

-The major ingredient in contrast media is Iodine which blocks x-rays. Bones block x-rays and that is why they can be seen clearly on

-Contrast media are substances that make certain body parts look different when they are subjected to imaging tools like X-Rays.

-The major ingredient in contrast media is Iodine which blocks x-rays. Bones block x-rays and that is why they can be seen clearly on

a X-ray scan. But soft tissue like the stomach and the intestine do not block x-rays which makes them less visible on a scan

-So when contrast media is injected, it helps block the x-rays which makes those body parts visible on the x-ray

-Iodine based contrast media are used for X-rays and CT scans whereas Gadolinium based contrast media are used for MRIs

-Divi’s is developing a range of iodine based

-Iodine based contrast media are used for X-rays and CT scans whereas Gadolinium based contrast media are used for MRIs

-Divi’s is developing a range of iodine based

contrast media and a few gadolinium based contrast media.

-They already are manufacturing a few iodine based products in their generic segment and they also have a product in their custom synthesis segment as well

-Management has said that contrast media as an industry is growing

-They already are manufacturing a few iodine based products in their generic segment and they also have a product in their custom synthesis segment as well

-Management has said that contrast media as an industry is growing

at 15-20% CAGR as doctors are increasingly relying on MRIs and CT scans to treat patients.

-Recycling of iodine is very important in manufacturing contrast media as iodine makes up a majority of the cost of manufacturing these products.

-Iodine is a very scarce substance and the

-Recycling of iodine is very important in manufacturing contrast media as iodine makes up a majority of the cost of manufacturing these products.

-Iodine is a very scarce substance and the

price of iodine has gone up from ₹1800 per kg in 2016 to ₹7100 in 2022.

Divi’s has designed a process where they can recover all of the iodine that they use in the manufacturing process. So they can produce contrast media for much cheaper than their competitors

8. CSM Business

-In this segment Divi’s manufactures APIs and intermediates for clinical

8. CSM Business

-In this segment Divi’s manufactures APIs and intermediates for clinical

trials and commercial products of global innovator companies

-This is a very high gross margin business for the company.

-Divi’s has an R&D team of more than 500 scientists who design the innovative processes to manufacture novel drugs of innovator companies.

-12 of the top 20

-This is a very high gross margin business for the company.

-Divi’s has an R&D team of more than 500 scientists who design the innovative processes to manufacture novel drugs of innovator companies.

-12 of the top 20

big pharma companies across US, Europe and Japan have been their clients for more than 10 years

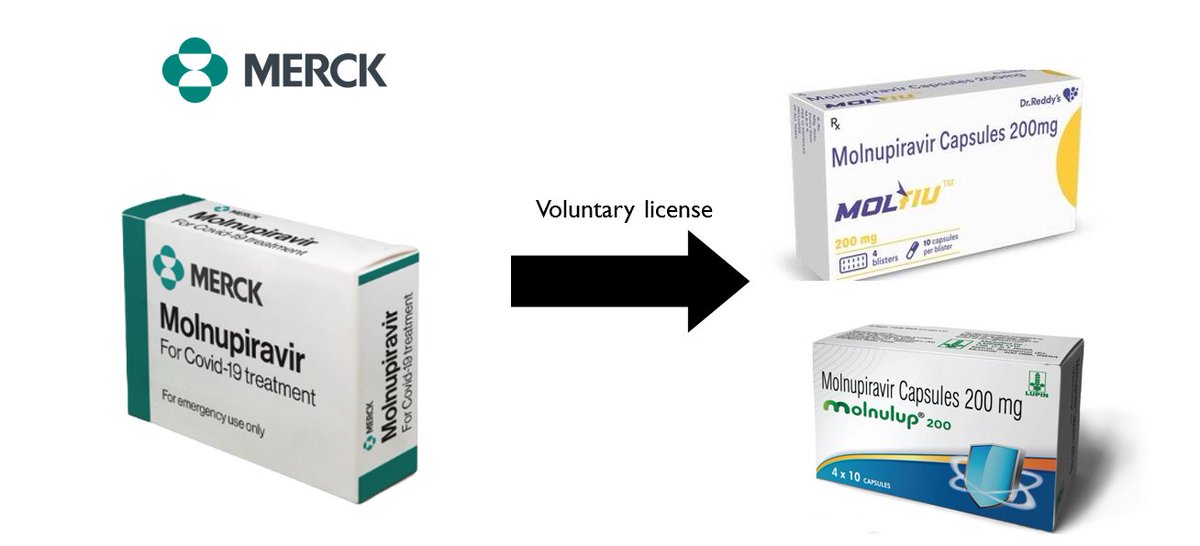

-An interesting thing about their CSM business was that in FY22, they were the largest manufacturers of Molnupiravir API.

-Merck developed this drug called Molnupiravir which was an

-An interesting thing about their CSM business was that in FY22, they were the largest manufacturers of Molnupiravir API.

-Merck developed this drug called Molnupiravir which was an

oral pill which was used in the treatment of Covid. Divi’s was the CDMO partner to manufacture and supply this drug.

-Under normal circumstances, This drug would only be sold by Merck as they had the patent for it. But because Covid was an extraordinary situation, Merck had

-Under normal circumstances, This drug would only be sold by Merck as they had the patent for it. But because Covid was an extraordinary situation, Merck had

given voluntary licenses to any pharma company that wanted to manufacture this drug.

-So many pharma companies like Dr Reddy’s and Lupin took voluntary licenses to sell Molnupiravir. Divi’s was the biggest global supplier of this drug, not only in India but also other emerging

-So many pharma companies like Dr Reddy’s and Lupin took voluntary licenses to sell Molnupiravir. Divi’s was the biggest global supplier of this drug, not only in India but also other emerging

countries where companies had taken voluntary licenses

-They were able to deliver this project in record time where they put in capex of 400 crores and commercialized it within 6 months to manufacture this product.

-This caused the revenues from their CSM business to be much

-They were able to deliver this project in record time where they put in capex of 400 crores and commercialized it within 6 months to manufacture this product.

-This caused the revenues from their CSM business to be much

higher in FY22 than in other years.

-This was a one-off and the Molnupiravir business is not expected to be of the same size going forward. The company intends to go back to similar contribution from Generic API and CSM business in the future

-This was a one-off and the Molnupiravir business is not expected to be of the same size going forward. The company intends to go back to similar contribution from Generic API and CSM business in the future

9. Nutraceuticals

-Under this segment, the company manufactures Beta-Carotene, Apocarotenal, Canthaxanthin, Astaxanthin, Lycopene, Lutein & Vitamin A, D and E.

-These products are primarily used in Health supplements, Food, Beverages, Pet food and Animal feed.

-Under this segment, the company manufactures Beta-Carotene, Apocarotenal, Canthaxanthin, Astaxanthin, Lycopene, Lutein & Vitamin A, D and E.

-These products are primarily used in Health supplements, Food, Beverages, Pet food and Animal feed.

-Divi’s is one of the largest manufacturers of Beta Carotenes globally. Beta Carotene is a pigment that is found in plants. It is responsible for the bright red, orange, yellow color of various fruits and vegetables like carrots, papaya and tomatoes

-Beta carotene is a precursor

-Beta carotene is a precursor

to Vitamin A which is good for eyesight. It also acts as an antioxidant. But most importantly, they are used as pigments to give color to various foods and drinks.

-The nutraceutical business is currently small for the company, but they expect it to grow very fast as the use of

-The nutraceutical business is currently small for the company, but they expect it to grow very fast as the use of

nutraceuticals in everyday life is increasing. People are relying more on fortified foods and supplements to maintain their health.

-This industry is currently very consolidated with 3 big players - DSM, BASF and Divi’s.

-This industry is currently very consolidated with 3 big players - DSM, BASF and Divi’s.

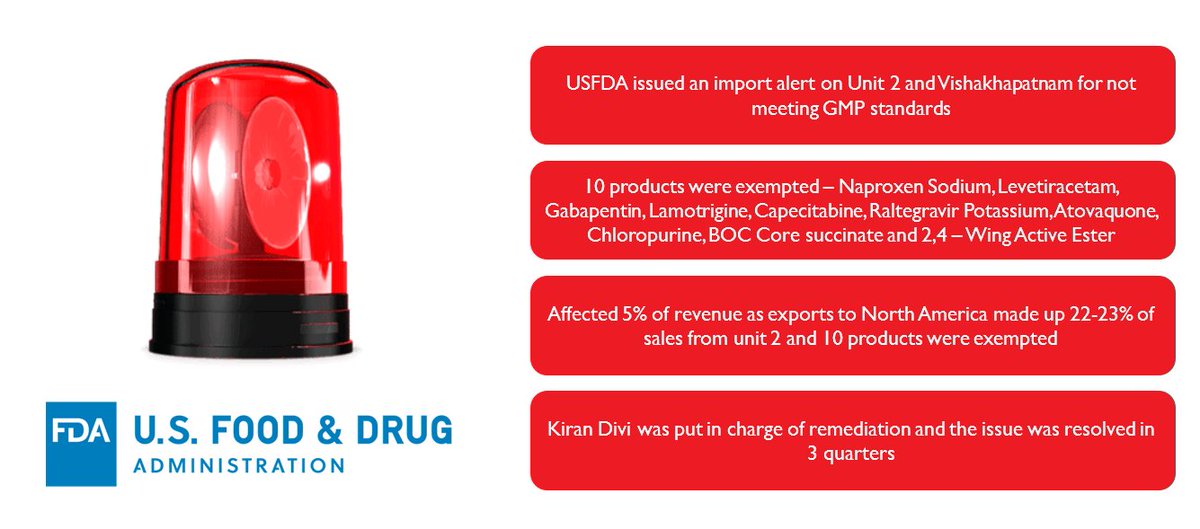

10. Import Alert

11. Kakinada Capex

-The one big investment that they have been trying to make for a long time is that they are trying to set up a new unit at Kakinada.

-They have acquired 425 crores in APIIC Kakinada. But due to local farmer protests, the development of the third unit has been

-The one big investment that they have been trying to make for a long time is that they are trying to set up a new unit at Kakinada.

-They have acquired 425 crores in APIIC Kakinada. But due to local farmer protests, the development of the third unit has been

delayed.

-The high court has dismissed the farmer’s case and management is expecting the land to be handed over to them within the next year. However, the handover of this land has been delayed many times before as well.

-But it should not affect the operations of the company as

-The high court has dismissed the farmer’s case and management is expecting the land to be handed over to them within the next year. However, the handover of this land has been delayed many times before as well.

-But it should not affect the operations of the company as

they still have 200 acres of land at Unit 1 and 150 in Unit 2 for further expansion.

-They will be starting with an investment of ₹1000 crores at Kakinada and will increase capacity when needed.

-They will be starting with an investment of ₹1000 crores at Kakinada and will increase capacity when needed.

12. Financials

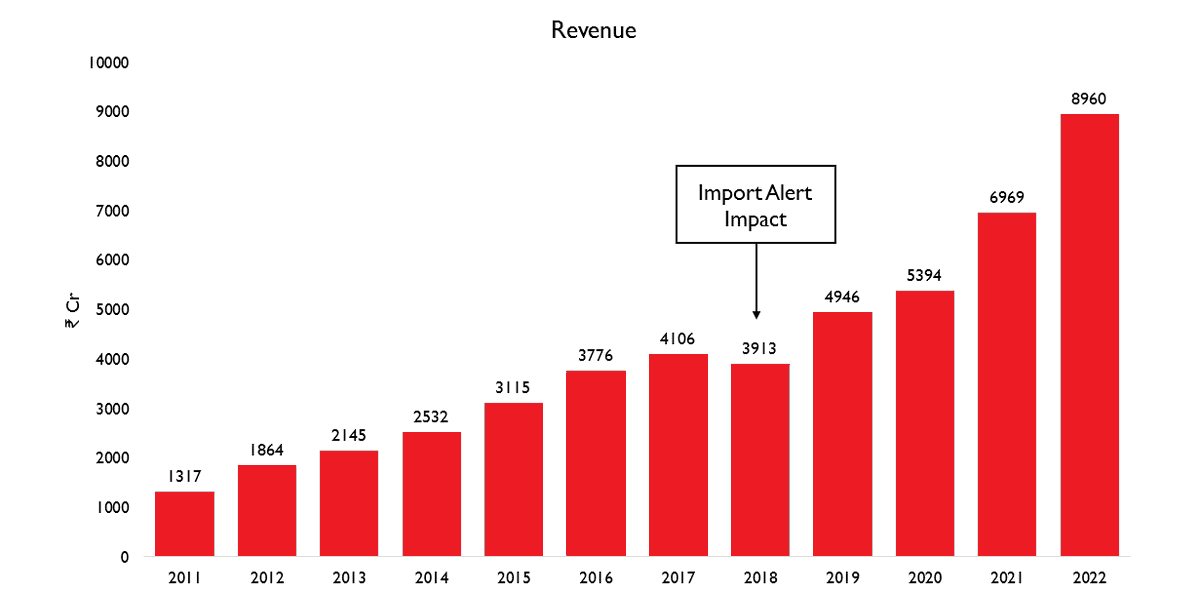

-Divi’s has always had a very stable and increasing revenues. They have been able to grow their revenues at over 19% CAGR for the past 11 years.

-In FY18, we can see the impact of the import alert on the company’s revenues. The issue happened at the end of Q4 FY17

-Divi’s has always had a very stable and increasing revenues. They have been able to grow their revenues at over 19% CAGR for the past 11 years.

-In FY18, we can see the impact of the import alert on the company’s revenues. The issue happened at the end of Q4 FY17

and was resolved by Q3 of FY18. It was the only year the company had a degrowth in revenues

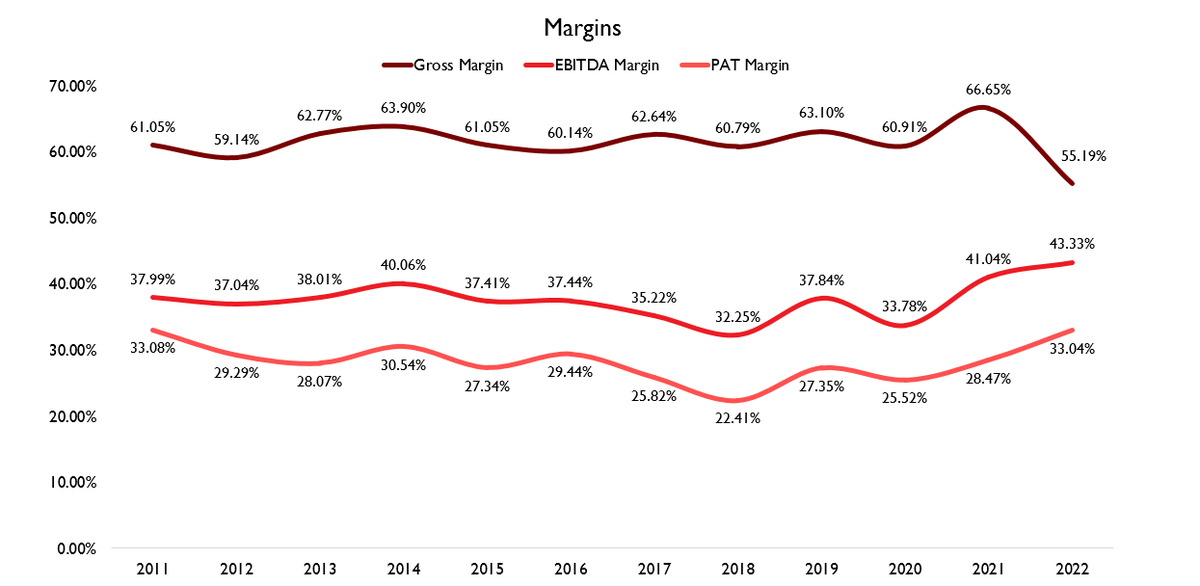

-Divi’s also has the best in class margins of any generic API manufacturer. Their gross margins are over 60% and the company has EBITDA margins in the range of 35-40% . Their PAT margins

-Divi’s also has the best in class margins of any generic API manufacturer. Their gross margins are over 60% and the company has EBITDA margins in the range of 35-40% . Their PAT margins

are also in the range of 25-30%

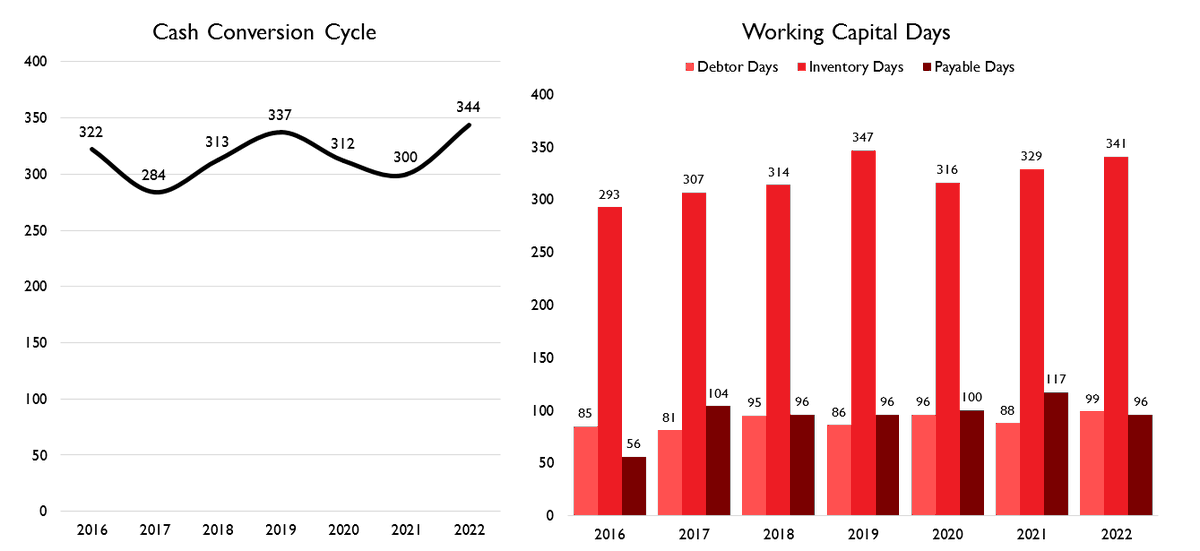

-One negative about the company’s financials is that they have a very long cash conversion cycle of over 300 days.

-This is because the company stores a lot of inventory to always have stock available for their key products and ample supply of raw

-One negative about the company’s financials is that they have a very long cash conversion cycle of over 300 days.

-This is because the company stores a lot of inventory to always have stock available for their key products and ample supply of raw

materials. So the working capital cycle is very long for the company.

-The company has a very healthy ROCE of over 30% on average and the company is completely debt free.

-In fact, they have never raised any outside money in the form of either debt or equity. Everything the

-The company has a very healthy ROCE of over 30% on average and the company is completely debt free.

-In fact, they have never raised any outside money in the form of either debt or equity. Everything the

company has built, it has built through internal accruals

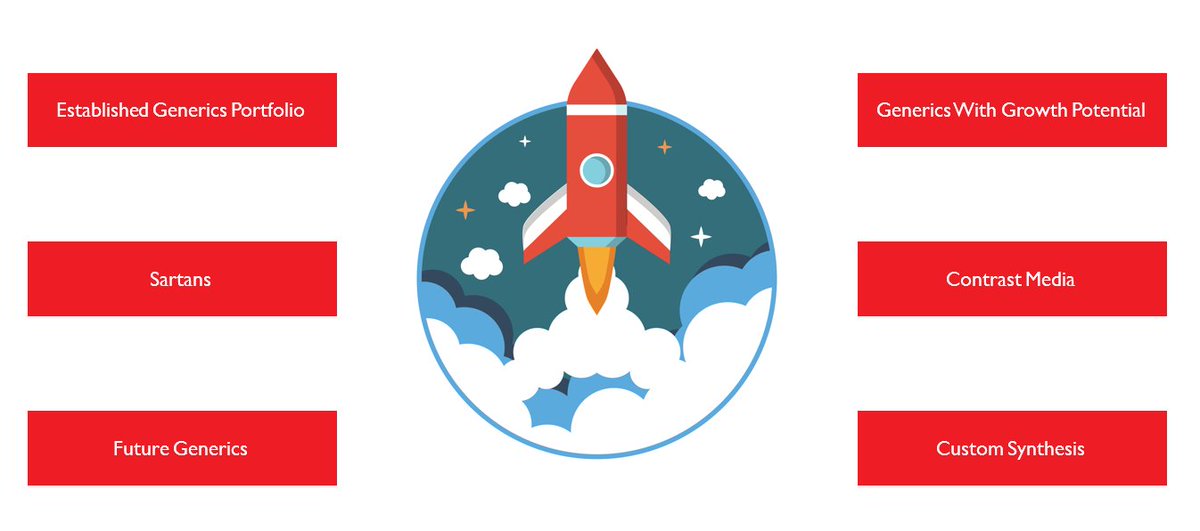

13. 6 Growth Engines

-The management recently talked about how they plan to grow their business through 6 growth engines

13. 6 Growth Engines

-The management recently talked about how they plan to grow their business through 6 growth engines

-The first engine is their established generic portfolio. These are the products where they have 50-70% market share and are the largest player. Management believes that they will continue growing at 10%.

-These are chronic products and the demand for them is expected to go up.

-These are chronic products and the demand for them is expected to go up.

The capacities need to go up with the demand. So they plan to maintain their leadership position in these molecules

-The second growth engine is their generics with growth potential. These are the molecules where they have 20-30% market share, Management believes that similar to

-The second growth engine is their generics with growth potential. These are the molecules where they have 20-30% market share, Management believes that similar to

their older products, they can reach 60-70% market share in these products as well.

-The third growth engine is the sartan products where they are developing the whole basket of products and expect to be market leaders in those products as well.

-The fourth growth engine is their

-The third growth engine is the sartan products where they are developing the whole basket of products and expect to be market leaders in those products as well.

-The fourth growth engine is their

contrast media business which the company expects will grow very rapidly.

-Their fifth growth engine will be generics which will be going off patent from 2023 to 2025. They have identified several products with several billion in opportunity size and developed the technology to

-Their fifth growth engine will be generics which will be going off patent from 2023 to 2025. They have identified several products with several billion in opportunity size and developed the technology to

manufacture them.

-Their sixth growth engine will be their custom synthesis business where they expect to commercialize several products over the next few years.

-Their sixth growth engine will be their custom synthesis business where they expect to commercialize several products over the next few years.

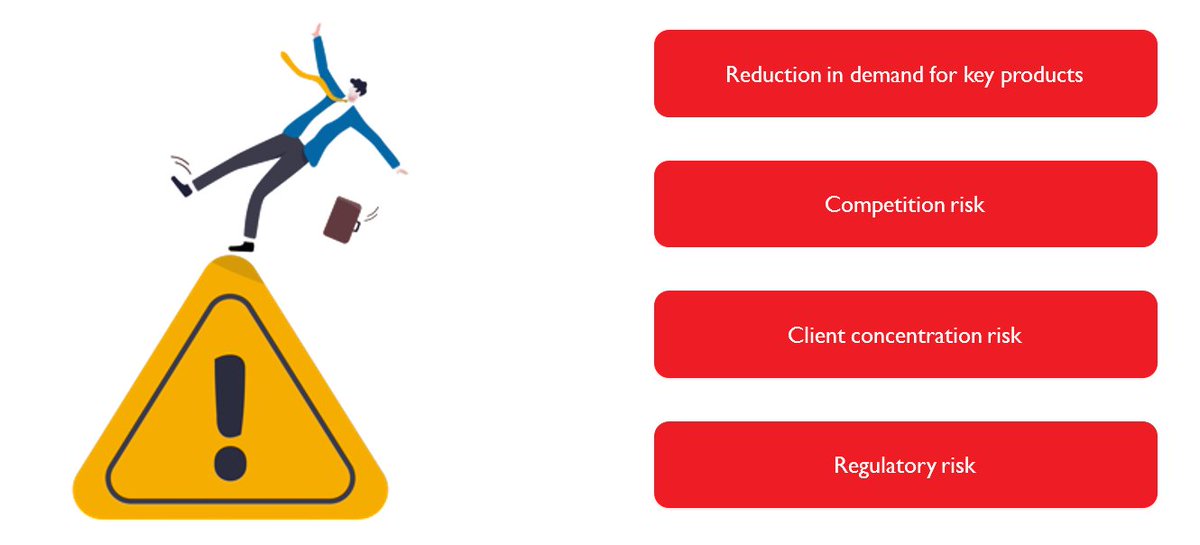

14. Risks

Watch the detailed analysis:

youtu.be

youtu.be

Loading suggestions...