Interest rates. Inflation. Recession.

Moats matter more now than ever.

If you invest, you MUST know how to identify them.

Here are 9 financial “rules of thumb” that Warren Buffett uses to tell if a company has one:⤵️

Moats matter more now than ever.

If you invest, you MUST know how to identify them.

Here are 9 financial “rules of thumb” that Warren Buffett uses to tell if a company has one:⤵️

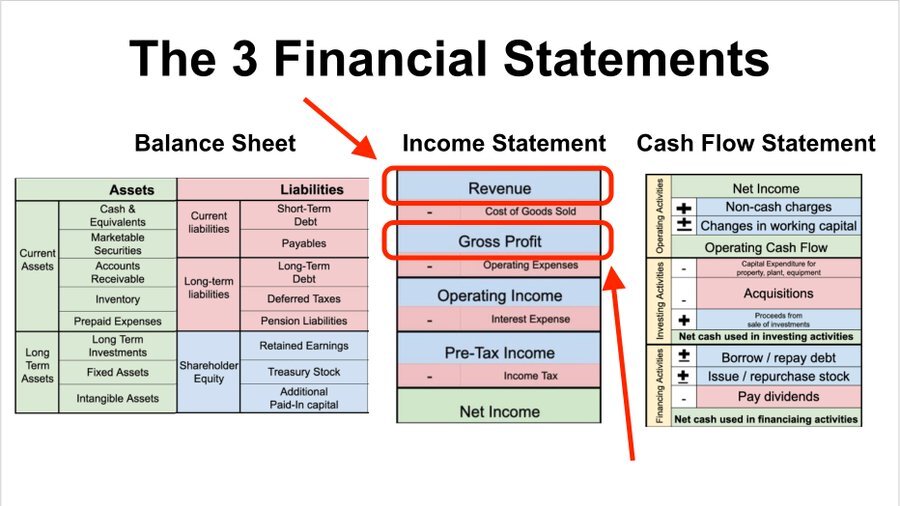

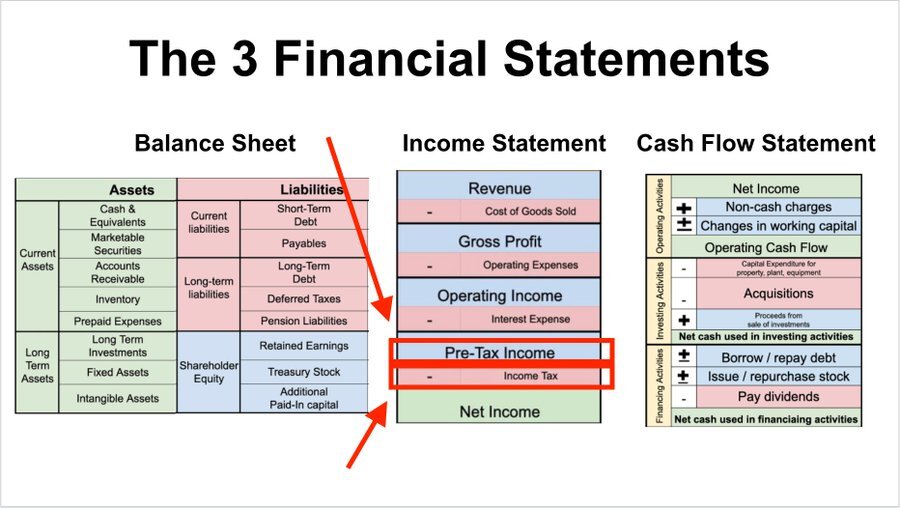

1: Gross Margin

Formula: Gross Profit / Revenue

Where: Income Statement

Moat: Consistently above 40%

No Moat: Under 40% & volatile

Formula: Gross Profit / Revenue

Where: Income Statement

Moat: Consistently above 40%

No Moat: Under 40% & volatile

Buffett’s logic:

A consistently high gross margin signals that the company isn’t competing exclusively on price.

A high gross margin also provides ample gross profit to pay all expenses and still leaves money for shareholders.

A consistently high gross margin signals that the company isn’t competing exclusively on price.

A high gross margin also provides ample gross profit to pay all expenses and still leaves money for shareholders.

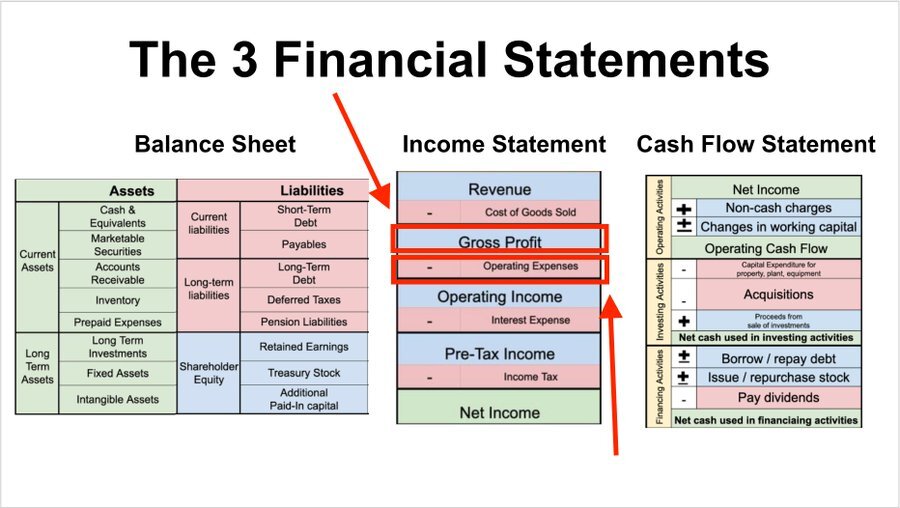

2: Sales, General, and Administrative Expenses

Formula: SG&A / Gross Profit

Where: Income Statement

Moat: Consistently under 30%

No Moat: Over 80% & volatile

Formula: SG&A / Gross Profit

Where: Income Statement

Moat: Consistently under 30%

No Moat: Over 80% & volatile

Buffett’s logic:

Wide moat companies don’t need to spend big on overhead to operate. Businesses without moats do.

Buffett looks for companies that consistently spend under 30% of their gross profit on SG&A.

Wide moat companies don’t need to spend big on overhead to operate. Businesses without moats do.

Buffett looks for companies that consistently spend under 30% of their gross profit on SG&A.

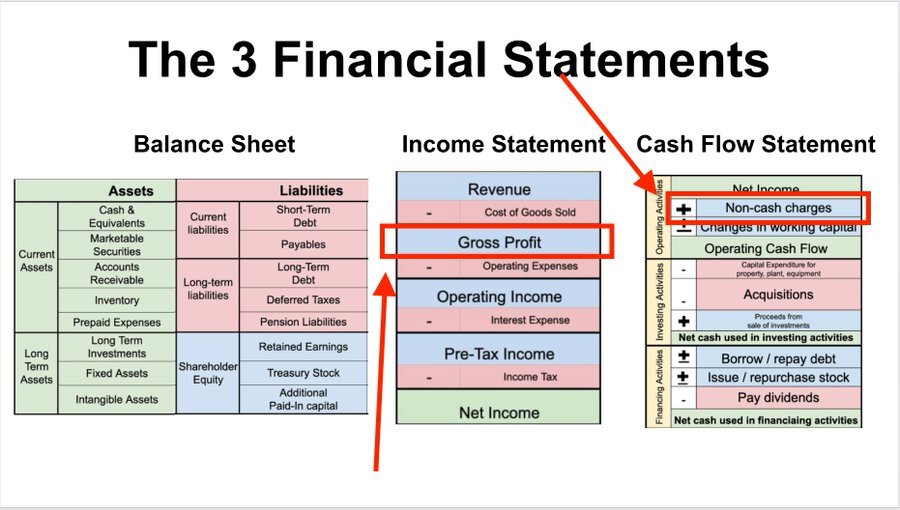

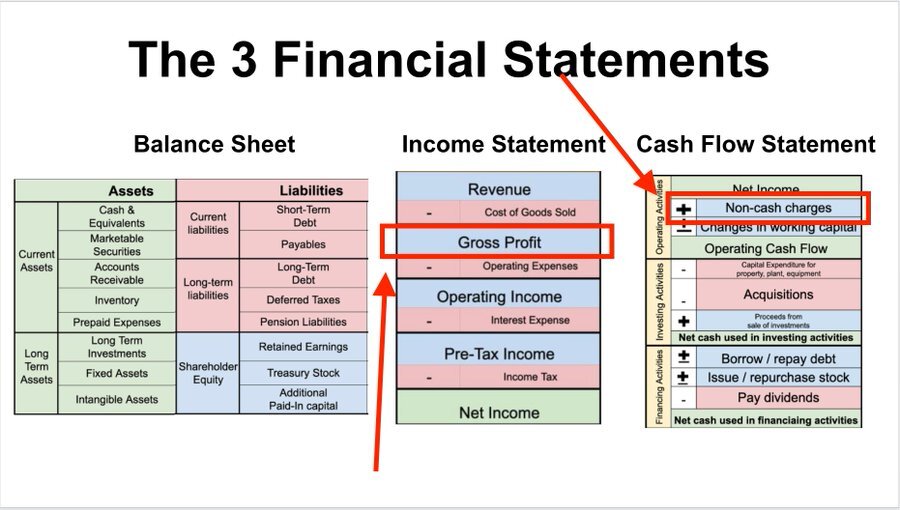

3: Depreciation Expense

Formula: Depreciation / Gross Profit

Where: Income Statement & Cash Flow Statement

Moat: Consistently under 10%

No Moat: Volatility & high

Formula: Depreciation / Gross Profit

Where: Income Statement & Cash Flow Statement

Moat: Consistently under 10%

No Moat: Volatility & high

Buffett’s logic:

Low depreciation expense signals that the business doesn’t need to spend big on capital expenditures to maintain its competitive advantage and has a moat.

Low depreciation expense signals that the business doesn’t need to spend big on capital expenditures to maintain its competitive advantage and has a moat.

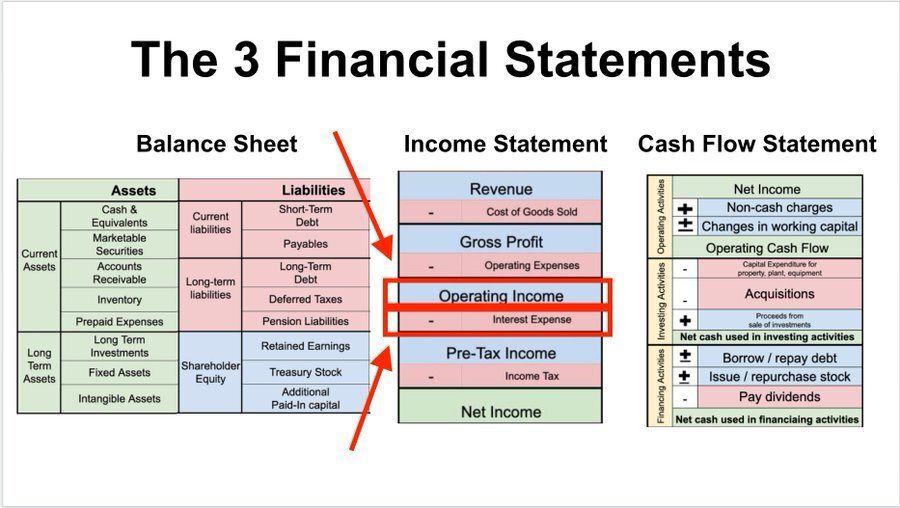

4: Interest Expense

Formula: Interest Expense / Operating Income

Where: Income Statement

Moat: Consistently under 15%

No Moat: Over 50% & volatile

Formula: Interest Expense / Operating Income

Where: Income Statement

Moat: Consistently under 15%

No Moat: Over 50% & volatile

Buffett’s logic:

Great businesses have such wonderful economics that they don’t need debt.

While this number varies greatly from industry to industry, it’s a great sign if a company consistently spends less than 15% of its operating income on interest.

Great businesses have such wonderful economics that they don’t need debt.

While this number varies greatly from industry to industry, it’s a great sign if a company consistently spends less than 15% of its operating income on interest.

5: Income Tax Expenses

Formula: Income Tax Paid / Pre-tax Income (EBT)

Where: Income Statement

Moat: Consistently pays the full amount (~21% in U.S.)

No Moat: Negative, erratic

Formula: Income Tax Paid / Pre-tax Income (EBT)

Where: Income Statement

Moat: Consistently pays the full amount (~21% in U.S.)

No Moat: Negative, erratic

Buffett’s logic:

Wide moat businesses make so much money that they consistently pay their full share of taxes.

Companies with negative/erratic income tax expenses aren't as likely to have a durable moat.

Wide moat businesses make so much money that they consistently pay their full share of taxes.

Companies with negative/erratic income tax expenses aren't as likely to have a durable moat.

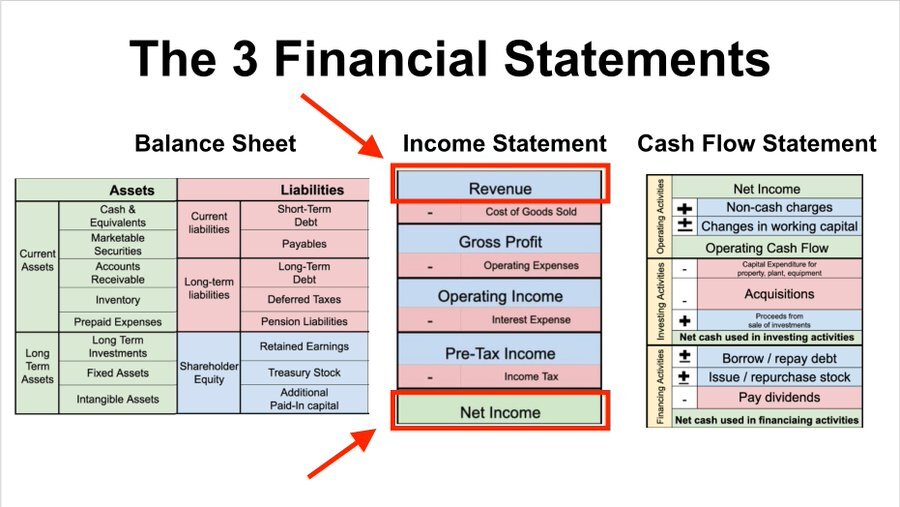

6: Profit Margin (Net Margin)

Formula: Net Income / Revenue

Where: Income Statement

Moat: Consistently above 20%

No Moat: Below 10%, negative, and volatile

Formula: Net Income / Revenue

Where: Income Statement

Moat: Consistently above 20%

No Moat: Below 10%, negative, and volatile

Buffett’s logic:

Companies that consistently convert 20% of their revenue into net income likely have a moat.

If this number is under 10%, negative, or volatile, the competition is likely fierce.

(There’s tons of nuance between 10% and 20%)

Companies that consistently convert 20% of their revenue into net income likely have a moat.

If this number is under 10%, negative, or volatile, the competition is likely fierce.

(There’s tons of nuance between 10% and 20%)

7: Capital Expenditures

Formula: Capital Expenditures / Net Income

Where: Income Statement & Cash Flow Statement

Moat: Consistently under 25%

No Moat: Consistently above 75%

Formula: Capital Expenditures / Net Income

Where: Income Statement & Cash Flow Statement

Moat: Consistently under 25%

No Moat: Consistently above 75%

Buffett’s logic:

Capital expenditures eat into profits.

Companies that don’t have to spend big on CAPEX have more money to reward shareholders.

Important: Capital Expenditures can vary greatly from year to year, so averaging over 10+ years is best.

Capital expenditures eat into profits.

Companies that don’t have to spend big on CAPEX have more money to reward shareholders.

Important: Capital Expenditures can vary greatly from year to year, so averaging over 10+ years is best.

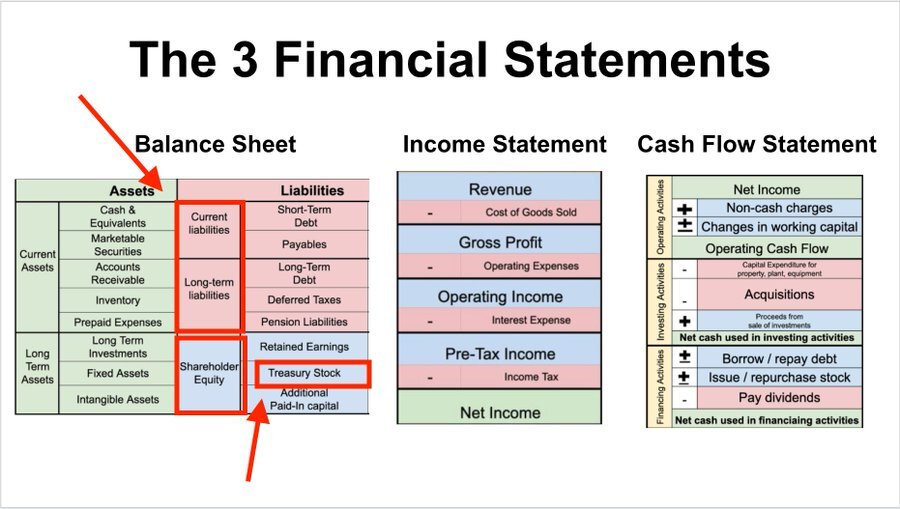

8: Total Liabilities to Adjusted Shareholder Equity

Formula: Total Liabilities / Shareholder Equity

Where: Balance Sheet

Moat: Below 0.80

No Moat: Over 2.00

Formula: Total Liabilities / Shareholder Equity

Where: Balance Sheet

Moat: Below 0.80

No Moat: Over 2.00

Buffett’s logic:

Wide moat businesses finance themselves with profits, not debt.

However, stock buybacks can throw off this equation. Adjust for this by adding back any treasury stock to the shareholder equity number.

Wide moat businesses finance themselves with profits, not debt.

However, stock buybacks can throw off this equation. Adjust for this by adding back any treasury stock to the shareholder equity number.

9: Return on Shareholders’ Equity

Formula: Net Income / Shareholder Equity

Where: Balance Sheet & Income Statement

Moat: Consistently above 15%

No Moat: Below 10%, negative, or volatile

Formula: Net Income / Shareholder Equity

Where: Balance Sheet & Income Statement

Moat: Consistently above 15%

No Moat: Below 10%, negative, or volatile

Buffett’s logic:

Return on equity shows how effectively management is reinvesting its profits. A number consistently over 15% indicates that the business has a moat.

Under 10%, negative, or volatile indicates that the business is struggling with the competition.

Return on equity shows how effectively management is reinvesting its profits. A number consistently over 15% indicates that the business has a moat.

Under 10%, negative, or volatile indicates that the business is struggling with the competition.

Three Important Caveats:

1) These “rules of thumb” are only useful when a company is fully optimized for profits (phase 4).

Many of them don’t work at all when a company is in phases 1, 2, 3, or 5

1) These “rules of thumb” are only useful when a company is fully optimized for profits (phase 4).

Many of them don’t work at all when a company is in phases 1, 2, 3, or 5

2) CONSISTENCY is key. These must be tested over multiple years & various economic conditions.

3) There are PLENTY of exceptions. Many of Buffett’s largest holdings do not pass every test. Investing (+ accounting) has tons of nuance.

Still, rules of thumb are useful.

3) There are PLENTY of exceptions. Many of Buffett’s largest holdings do not pass every test. Investing (+ accounting) has tons of nuance.

Still, rules of thumb are useful.

Learning to read financial statements is an INCREDIBLY important skill for investors, managers, and business owners to master

Want help? @BrianFeroldi and I teach a live course that gets rookies up to speed, FAST

Interested? DM me for a coupon code

maven.com

Want help? @BrianFeroldi and I teach a live course that gets rookies up to speed, FAST

Interested? DM me for a coupon code

maven.com

Summary:

1. GM >40%

2. SG&A < 30%

3. Depreciation <8%

4. Interest Expense <15%

5. Income tax ~21%

6. Profit Margin >20%

7. CapEx <10%

8. Debt to adjusted Equity < 0.80

9. Return on equity >15%

1. GM >40%

2. SG&A < 30%

3. Depreciation <8%

4. Interest Expense <15%

5. Income tax ~21%

6. Profit Margin >20%

7. CapEx <10%

8. Debt to adjusted Equity < 0.80

9. Return on equity >15%

Loading suggestions...