Every company in my portfolio has some underlying cycle to it.

Instead of searching for secular stories, I've embraced this cyclicity, and work to identify and play these underlying cycles to outperform the index.

A thread on a few ideas that could possibly see recovery in 2023

Instead of searching for secular stories, I've embraced this cyclicity, and work to identify and play these underlying cycles to outperform the index.

A thread on a few ideas that could possibly see recovery in 2023

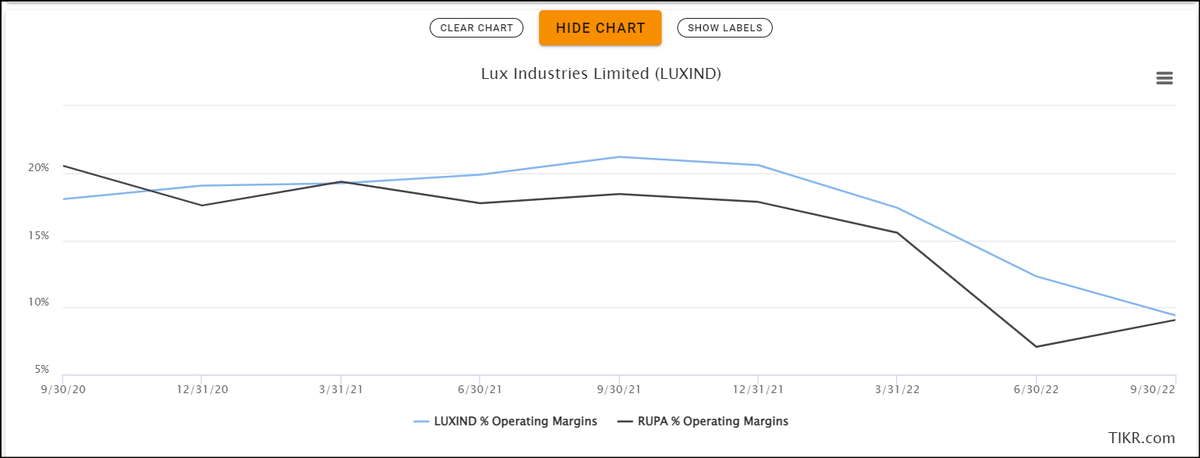

1. Chaddi companies

Both Lux and Rupa have seen large corrections this year. What's interesting to note is the drawdowns happened at different times:

Lux in Jan following a SEBI inquiry, and Rupa in June, following news of cotton prices.

2/

Both Lux and Rupa have seen large corrections this year. What's interesting to note is the drawdowns happened at different times:

Lux in Jan following a SEBI inquiry, and Rupa in June, following news of cotton prices.

2/

Prices of (Shankar-6) Cotton were around Rs. 35-40,000 per candy before the pandemic, and rose to almost Rs. 100,000 in June/July 2022.

The high raw material cost hurt margins for both of these companies. Margins fell from 15-20% to 6-10% for both companies.

3/

The high raw material cost hurt margins for both of these companies. Margins fell from 15-20% to 6-10% for both companies.

3/

Currently, prices have corrected to Rs. 60,000 per candy. This is still high, but as they cool, margins will overall improve.

Both Lux and Rupa have a lot of inventory, so could take a few quarters of inventory adjustment.

On valuations, both are near cyclical lows:

4/

Both Lux and Rupa have a lot of inventory, so could take a few quarters of inventory adjustment.

On valuations, both are near cyclical lows:

4/

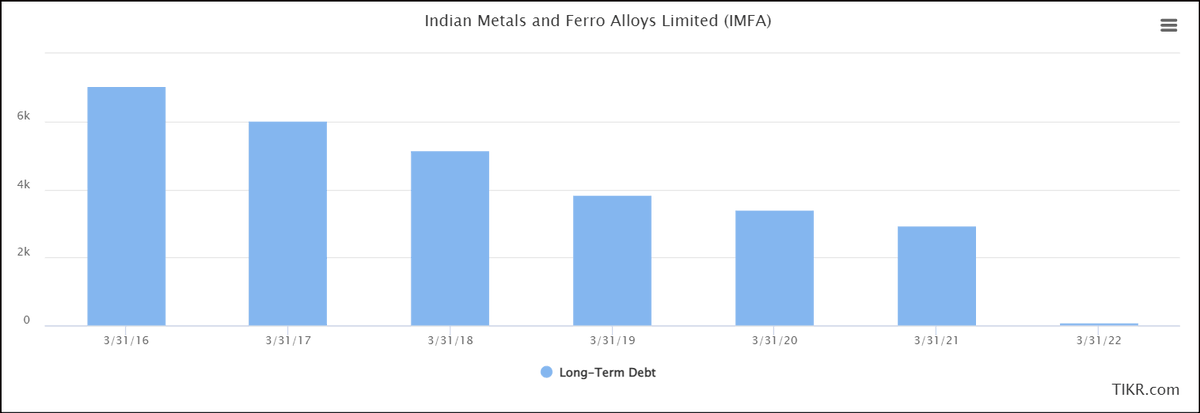

2. Ferro Alloys

IMFA and Maithan Alloys have had a poor showing in 2022. While both are trading at cyclical lows, the former is more interesting to evaluate.

Margins have fallen on account of increased coal and freight costs. Recovery should happen from Q3 onwards.

5/

IMFA and Maithan Alloys have had a poor showing in 2022. While both are trading at cyclical lows, the former is more interesting to evaluate.

Margins have fallen on account of increased coal and freight costs. Recovery should happen from Q3 onwards.

5/

In the past, IMFA's cyclical low valuations have come at 0.3-0.5 times book, but the company has since repaid all of its long term debt.

Commodity companies with clean balance sheets usually trade above book.

6/

Commodity companies with clean balance sheets usually trade above book.

6/

A nice bonus optionality comes from a potential re-opening of China (one of their largest markets), and them receiving dues from the government.

For Maithan, valuations are rock bottom, and any positive news could take it to 1.3-1.5x book.

[H/T: @WayneDMello]

7/

For Maithan, valuations are rock bottom, and any positive news could take it to 1.3-1.5x book.

[H/T: @WayneDMello]

7/

3. Sharda Cropchem

Sharda is a high quality business in the agrochem space, showcased in both their margins over time, and RoCE profile over a decade:

8/

Sharda is a high quality business in the agrochem space, showcased in both their margins over time, and RoCE profile over a decade:

8/

They're having a horrible time at the moment due to forex losses, when the Euro depreciated strongly against the USD in Q1 and Q2.

One should already expect recovery in Q3 as this has since reversed...

9/

One should already expect recovery in Q3 as this has since reversed...

9/

...while valuations are near all-time lows:

Q2's concall is a really nice read on the dynamics of realisations, and how supply changes over time.

For Sharda, it looks like a longer term story.

[H/T: @theHarshFolio who's the go to person on anything agrochem!]

10/10

Q2's concall is a really nice read on the dynamics of realisations, and how supply changes over time.

For Sharda, it looks like a longer term story.

[H/T: @theHarshFolio who's the go to person on anything agrochem!]

10/10

Disclosure: IMFA, Maithan and Sharda form nearly 10% of my portfolio. Currently evaluating Rupa.

These are not recommendations; thought it would be nice to discsuss a few cyclicals. There are so many more sectors and ideas that are at attractive valuations.

These are not recommendations; thought it would be nice to discsuss a few cyclicals. There are so many more sectors and ideas that are at attractive valuations.

Loading suggestions...