Bajaj Finance was given 46% CAGR over the last 10 years!

Even after a strong Q3 update yesterday, the stock tanked!

A thread on the business for Bajaj Finance and the opportunities ahead

Lets go👇

(1/16)

Even after a strong Q3 update yesterday, the stock tanked!

A thread on the business for Bajaj Finance and the opportunities ahead

Lets go👇

(1/16)

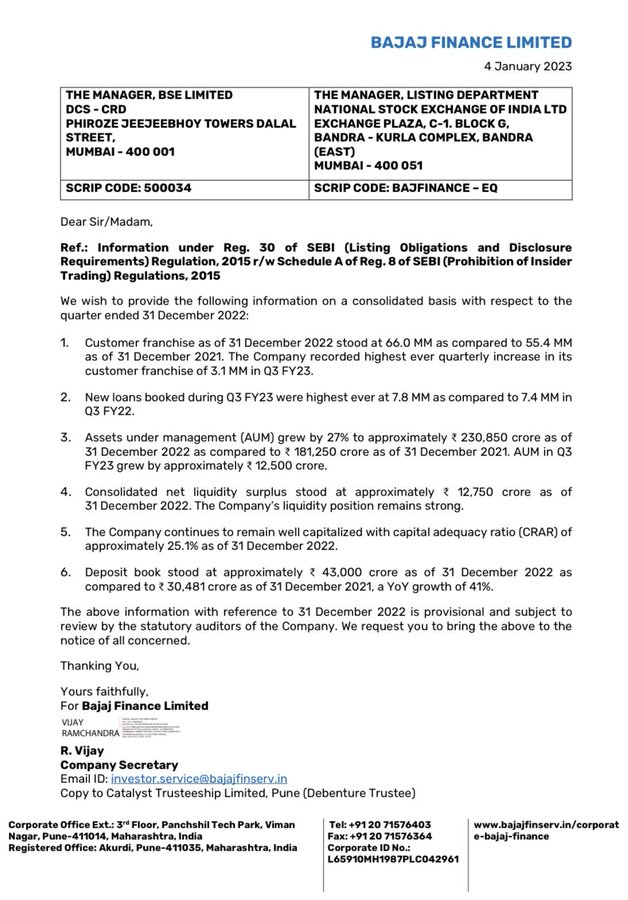

What has happened?

Bajaj Finance reported its Q3 update:-

🏦AUM growth at 27%

🏦Deposit growth at 41%

The stock tanked up to 9% after this.

Lets find out how the business is doing:-

(2/16)

Bajaj Finance reported its Q3 update:-

🏦AUM growth at 27%

🏦Deposit growth at 41%

The stock tanked up to 9% after this.

Lets find out how the business is doing:-

(2/16)

Q3 Update:-

🏦Customer growth has remained strong;

🏦AUM growth moderates, but remains strong

🏦New loans is at all time high of 78 lakhs, up 5.4%YOY & 14.7%QOQ

🏦Customer base at 6.6cr, up 19.13%YOY & 4.93%QOQ

(3/16)

🏦Customer growth has remained strong;

🏦AUM growth moderates, but remains strong

🏦New loans is at all time high of 78 lakhs, up 5.4%YOY & 14.7%QOQ

🏦Customer base at 6.6cr, up 19.13%YOY & 4.93%QOQ

(3/16)

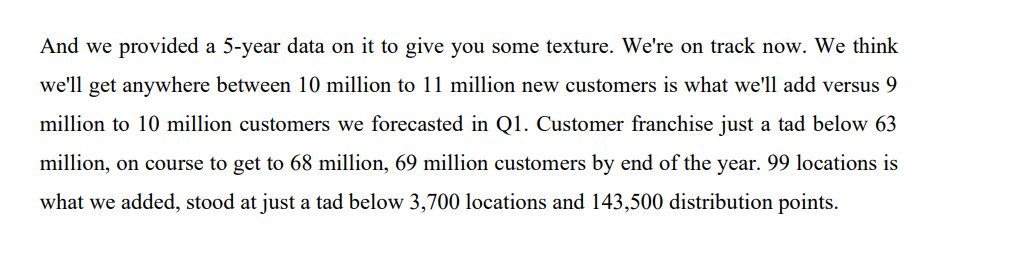

Customer Franchise is growing ever so stronger:-

Bajaj finance is on track to add 10-11 Million customers this year

Customer franchise is ramping up to 69 Million customers

(4/16)

Bajaj finance is on track to add 10-11 Million customers this year

Customer franchise is ramping up to 69 Million customers

(4/16)

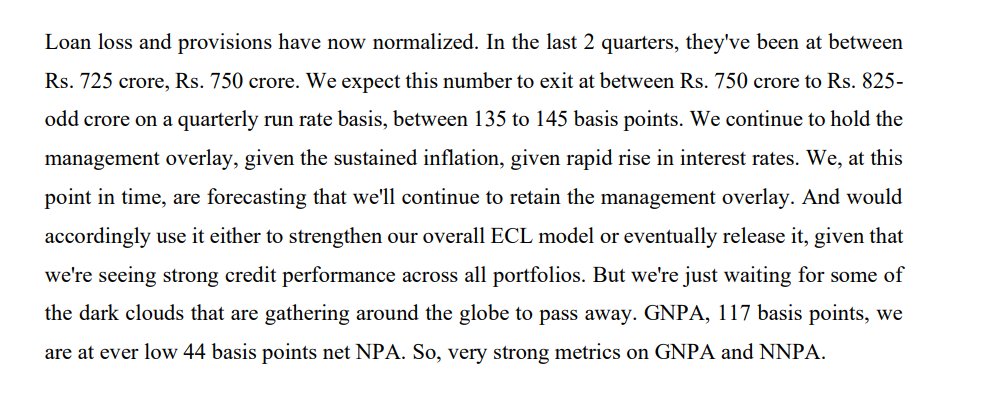

NPAs have started to stabilize:-

Covid was indeed bad for Bajaj's finance.

But now the management expects credit cost to be 135 bps-145bps

Provisions are normalising and the slippages are coming back to acceptable levels

(5/16)

Covid was indeed bad for Bajaj's finance.

But now the management expects credit cost to be 135 bps-145bps

Provisions are normalising and the slippages are coming back to acceptable levels

(5/16)

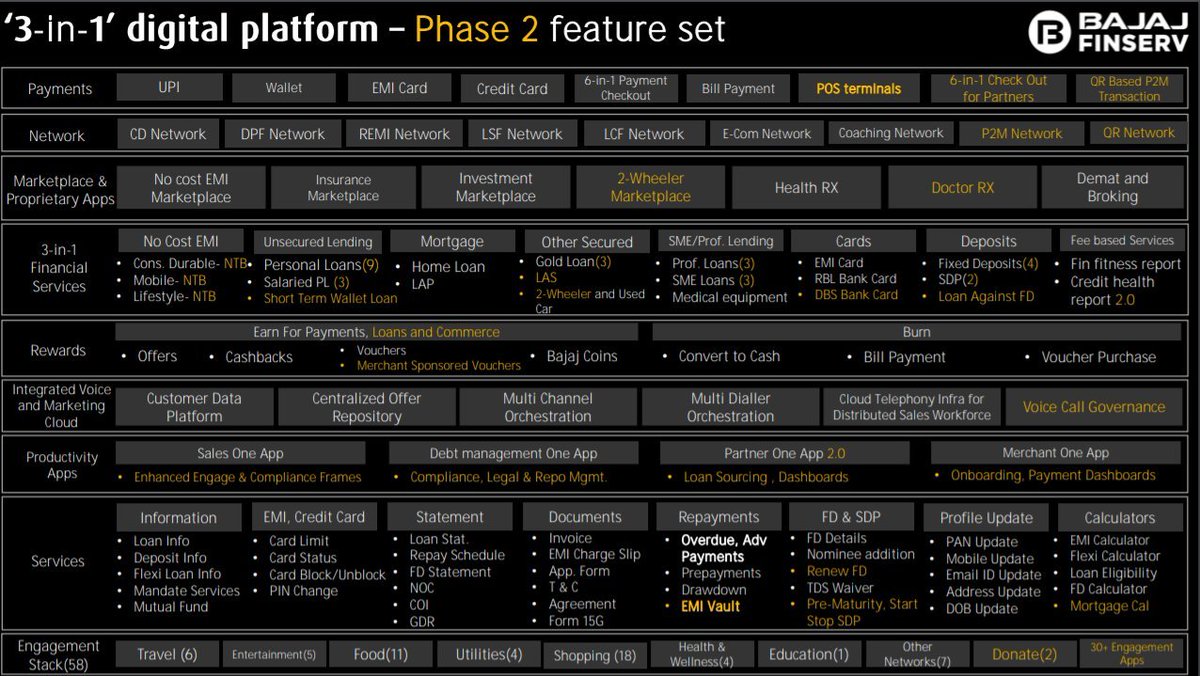

The aggressive entry of Bajaj finance in the Payments space means they can do exactly what Paytm is doing

Bajaj Finance's payment stack will be fully integrated on the app by next year

This means they do everything a Paytm does but being a lender themselves.

(6/16)

Bajaj Finance's payment stack will be fully integrated on the app by next year

This means they do everything a Paytm does but being a lender themselves.

(6/16)

Rapid Ramp up of the deposit franchise:-

Bajaj Finance is rapidly ramping up its deposit growth.

The growth is as high as 40%

This is when the systemic growth is at just 10%

(7/16)

Bajaj Finance is rapidly ramping up its deposit growth.

The growth is as high as 40%

This is when the systemic growth is at just 10%

(7/16)

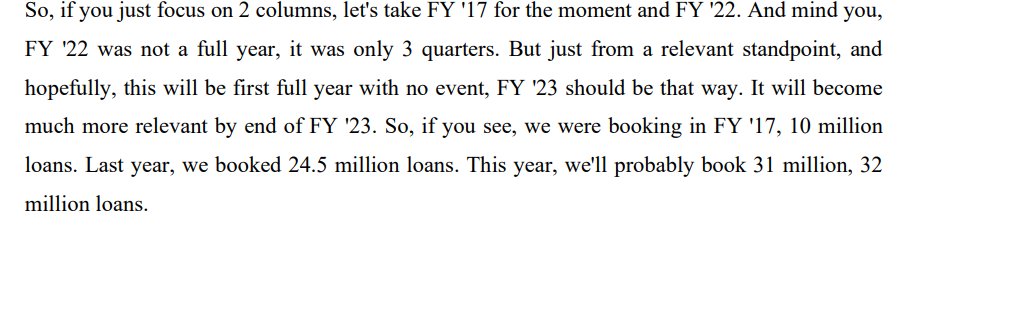

Payments app will help bajaj scale up very quickly:-

In FY17 Bajaj booked 10 Million loans

As the company becomes more digital

The company will book nearly 31 Million loans this year

A 3x scale up in 5 years!

(8/16)

In FY17 Bajaj booked 10 Million loans

As the company becomes more digital

The company will book nearly 31 Million loans this year

A 3x scale up in 5 years!

(8/16)

Rajiv Jain from Bajaj Finance!

His deep understanding of the lending business is brilliant.

Insights on the call are brilliant!

Rajiv Jain,Uday Kotak, Aditya Puri are some top bankers in this country

(9/16)

His deep understanding of the lending business is brilliant.

Insights on the call are brilliant!

Rajiv Jain,Uday Kotak, Aditya Puri are some top bankers in this country

(9/16)

Will Bajaj Finance face problems from fintechs?

Bajaj Finance on Buy Now Pay Later(BNPL) fintech:-

The credit costs are so big in the BNPL business that most businesses won't survive!

Credit costs are upwards of 20-25%.

There is no comparison b/w Bajaj and fintechs

(10/16)

Bajaj Finance on Buy Now Pay Later(BNPL) fintech:-

The credit costs are so big in the BNPL business that most businesses won't survive!

Credit costs are upwards of 20-25%.

There is no comparison b/w Bajaj and fintechs

(10/16)

So what lies ahead for Bajaj Finance?

The launch of the app will significantly ramp up customer acquisitions for Bajaj.

COVID was significantly bad for Bajaj.

The company has now recovered from the problems

(11/16)

The launch of the app will significantly ramp up customer acquisitions for Bajaj.

COVID was significantly bad for Bajaj.

The company has now recovered from the problems

(11/16)

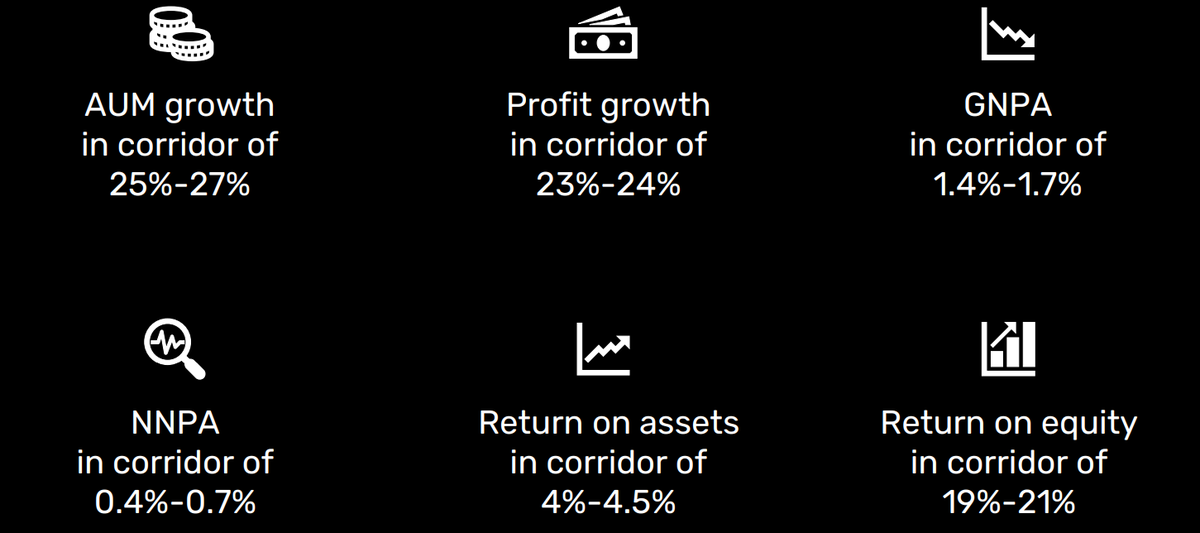

The company has now guided for the growth of

🏦25-27% in AUM

🏦Gross NPAs of 1.4-17%

🏦Profit growth of 23-24%

(12/16)

🏦25-27% in AUM

🏦Gross NPAs of 1.4-17%

🏦Profit growth of 23-24%

(12/16)

The hangover of conversion to a bank:-

It is no secret that RBI wants big NBFCs to convert to Banks.

HDFC ltd merging with HDFC Bank was the first step

The regulatory arbitrage b/w Bank and NBFCs is starting to wane off.

(13/16)

It is no secret that RBI wants big NBFCs to convert to Banks.

HDFC ltd merging with HDFC Bank was the first step

The regulatory arbitrage b/w Bank and NBFCs is starting to wane off.

(13/16)

Bajaj has always operated on a lean model.

While the management does not want to convert to a bank...the next 2-3 years remain crucial for the conversion to a bank.

(14/16)

While the management does not want to convert to a bank...the next 2-3 years remain crucial for the conversion to a bank.

(14/16)

Valuation:-

Bajaj Finance has always traded at very rich valuations.

The company still trades at nearly 10x P/B which is super expensive.

(15/16)

Bajaj Finance has always traded at very rich valuations.

The company still trades at nearly 10x P/B which is super expensive.

(15/16)

Conclusion-

Bajaj finance is a class company

🏦Covid problems are now behind the company

🏦The new app should help ramp up the customer franchise

🏦Slippages should remain in check

Valuations are extremely expensive..however the stock should always be on investor radar

(16/16)

Bajaj finance is a class company

🏦Covid problems are now behind the company

🏦The new app should help ramp up the customer franchise

🏦Slippages should remain in check

Valuations are extremely expensive..however the stock should always be on investor radar

(16/16)

Disclaimer:-

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

This is my own study

Not an investment recommendation

Please consult your own financial advisor before making any investment decisions

Loading suggestions...