Education

Business

Finance

Profitability

Valuation

Growth & Capex

Industry Trends

Position Sizing

Risks & Anti Thesis

My name is XPRO & i am not a packaging film maker.

A new 7% position for me. A company promoted by Birlas.

Do retweet if you find it useful. 🙏

🧵

A new 7% position for me. A company promoted by Birlas.

Do retweet if you find it useful. 🙏

🧵

Disclaimer

I am not a sebi registered advisor. The reason i share about my learnings is to motivate everyone to do the same & build a sharing ecosystem. I firmly believe that knowledge multiplies by sharing

Nothing i share should be construed as a buy or sell reco

I am not a sebi registered advisor. The reason i share about my learnings is to motivate everyone to do the same & build a sharing ecosystem. I firmly believe that knowledge multiplies by sharing

Nothing i share should be construed as a buy or sell reco

Outline

1. Business

2. Growth & Capex

3. Profitability

4. Industry Trends

5. Moats & Competitive positioning

6. Valuation

7. Position sizing

8. Risks & Anti thesis

1. Business

2. Growth & Capex

3. Profitability

4. Industry Trends

5. Moats & Competitive positioning

6. Valuation

7. Position sizing

8. Risks & Anti thesis

1. Business

XPRO creates polymer (Poly propylene) based films & is a leading manufacturer in India of Coextruded Plastic Films (70% market share), & specialty films (including dielectric films (33% market share) which are the heart of capacitors Film Capacitors)

XPRO creates polymer (Poly propylene) based films & is a leading manufacturer in India of Coextruded Plastic Films (70% market share), & specialty films (including dielectric films (33% market share) which are the heart of capacitors Film Capacitors)

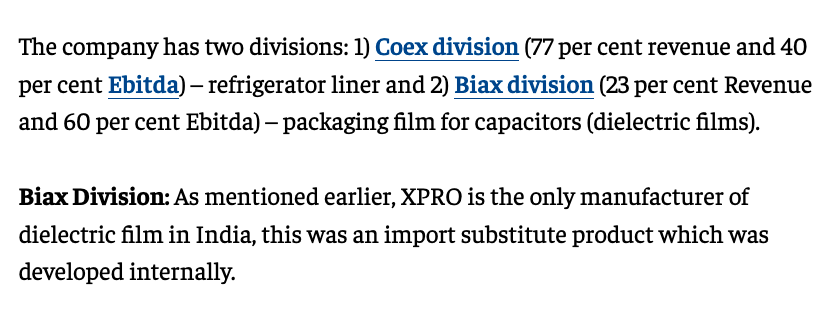

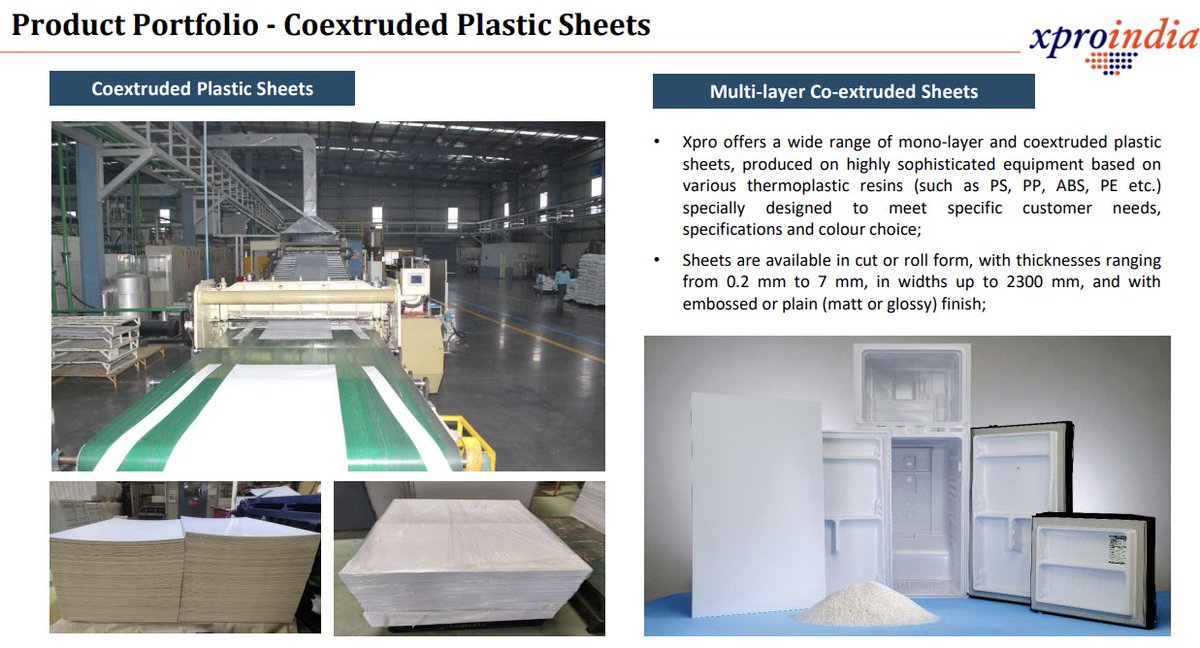

Co has 2 main business divisions, Coex (Coextruded Plastic Sheets film) division, & Biax (Biaxial film) division. The biax division had 23% of revenue in FY21 but 60% of EBITDA.

Pic src: economictimes.indiatimes.com

Pic src: economictimes.indiatimes.com

This works out to 28% EBITDA for biax in FY21 & a 6% margin for the coex division in FY21.

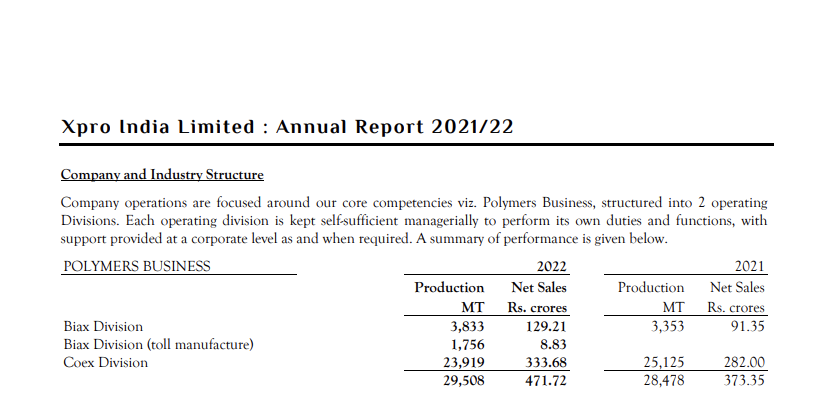

In fact, looking at FY22 annual report, we find the tonnage & revenue split which tells us about the average realization.

340 rs / kg for biax,

140 rs / kg for coex

In fact, looking at FY22 annual report, we find the tonnage & revenue split which tells us about the average realization.

340 rs / kg for biax,

140 rs / kg for coex

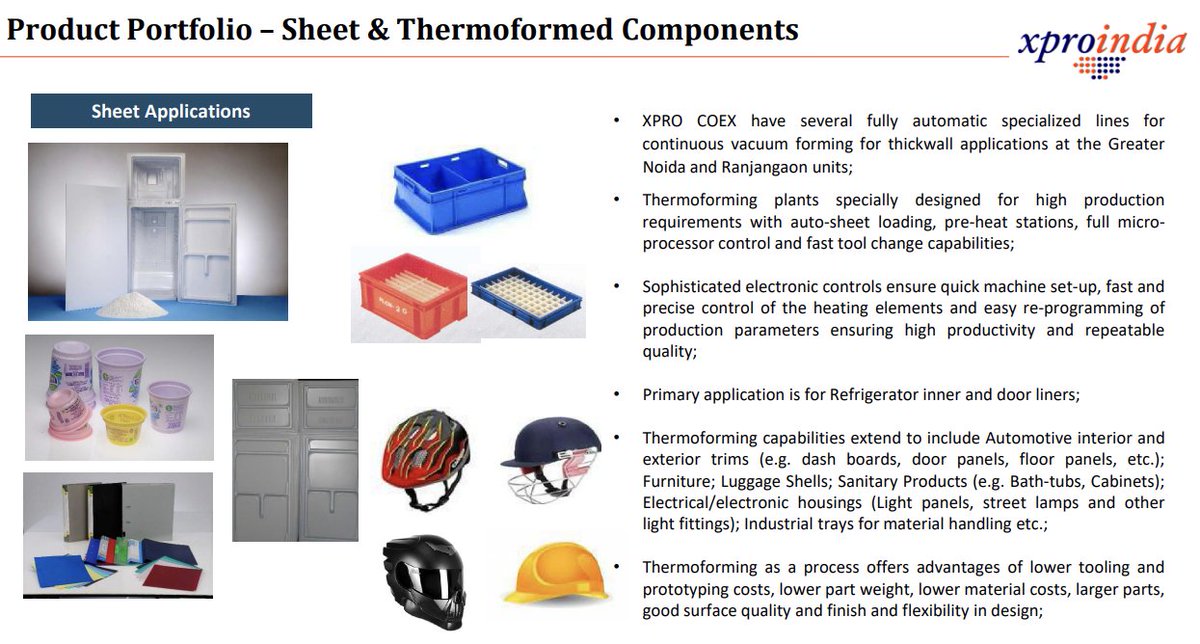

The coex division films are primarily used in making inner lining of the refrigerators.

Xpro Cast Films are produced on the most sophisticated multilayer coextrusion film lines. I think we understand now why xpro has 70% market share in this division.

Biax films

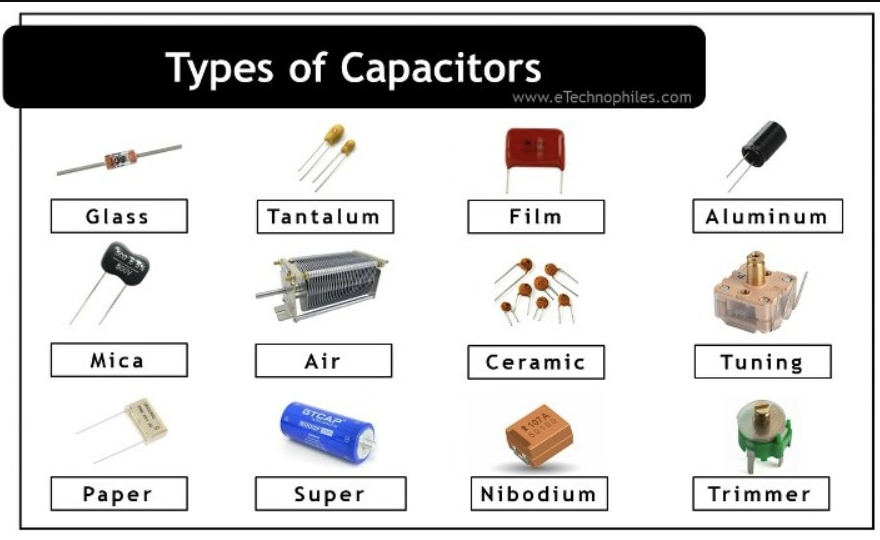

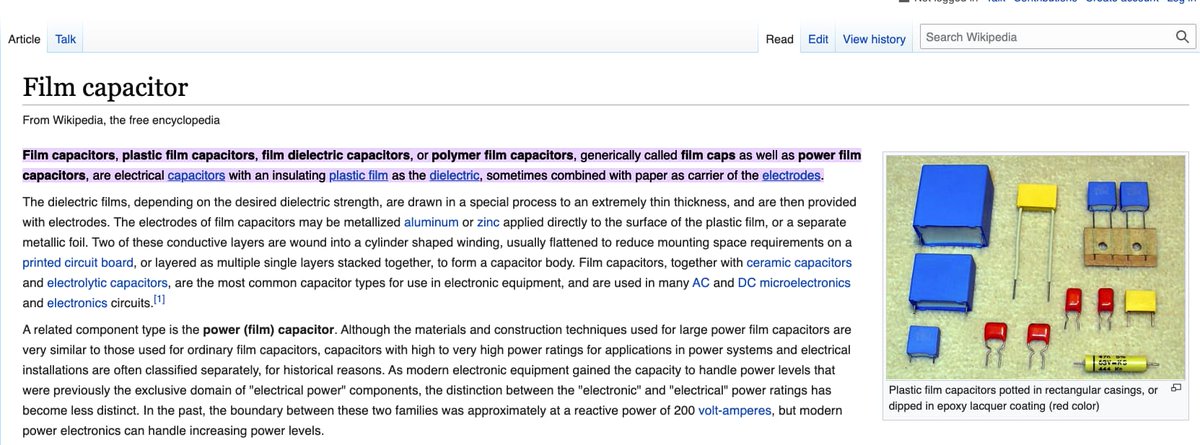

There are 3 kind of capacitors: Film capacitors, electrolytic capacitors, ceramic capacitors. Each of them have applications of their own.

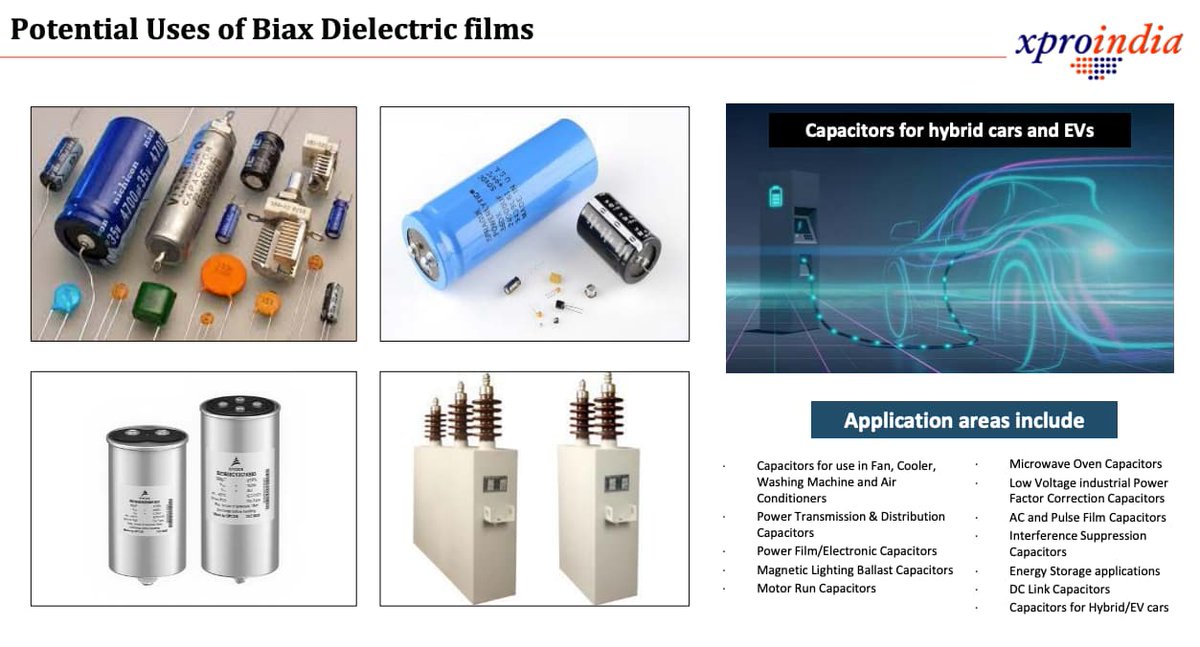

Xpro makes biaxial dielectric films which are used as a critical component in film capacitors (its the dielectric).

There are 3 kind of capacitors: Film capacitors, electrolytic capacitors, ceramic capacitors. Each of them have applications of their own.

Xpro makes biaxial dielectric films which are used as a critical component in film capacitors (its the dielectric).

All capacitors consist of electrodes (cathode & anode made up of metals generally) separated by a dielectric medium. Depending on the type of dielectric medium, the capacitor is classified. As: electrolytic capacitors have an electrolyte for dielectric

Xpro’s Biax Dielectric Films are specially designed polypropylene films manufactured by the stenter process on highly specialized equipment

(brucker) in controlled environmental & ultra clean room

conditions for a wide range of applications in the capacitors industry

(brucker) in controlled environmental & ultra clean room

conditions for a wide range of applications in the capacitors industry

These Films are available in thickness range of 3µ to15µ (lower thickness down to 2µ under development).

Dielectric films are ideally suited for high performance capacitors, both for normal and high temperature applications, high temperature super grade for AC aging and ripple current condition at elevated temperature.

Watch this video to understand applications for DC link film capacitors in EV power trains.

youtube.com

youtube.com

2. Growth & Capex

Xpro is the only biax film maker in India currently. For many years its biax division core profitability was suppressed due to the inverted duty structure which put duty on their raw material PP but not on import of films.

Xpro is the only biax film maker in India currently. For many years its biax division core profitability was suppressed due to the inverted duty structure which put duty on their raw material PP but not on import of films.

It has ~30% of market share with rest of 70% being imported. It is cost competitive with China despite lower scale. I did scuttlebutt talking to MD of one of largest capacitor makers in india through a firm called GLG.

My scuttlebutt tells me that domestic capacitor makers would prefer to source from xpro even if they had to pay 3-4% more. It is this import substitution market which Xpro will target in years to come.

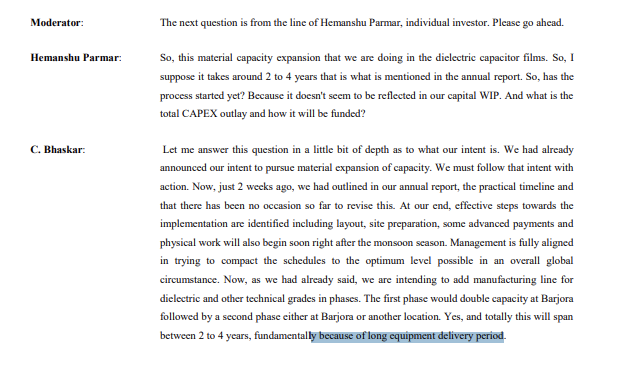

October 2021 XPRO announced 2 new lines for biax films. To be delivered in 2-4 years. 2 years finish in october this year. I expect 1 line to come late FY24 or early FY25. Next line in 1 year from then (median).

I expect the coex division to grow in line with growth in manufacturing of refrigerators in India. 10-15% in base case (in line with domestic production) & faster if export manufacturing of refrigerators takes off in a meaningful way.

newindianexpress.com

newindianexpress.com

The biax division can become 3x in 4 years (conservatively). Given it is highly profitable, blended profits will grow faster.

Do note that biax division is capex heavy so they will definitely need to raise some equity or debt to fund part of this expansion.

Do note that biax division is capex heavy so they will definitely need to raise some equity or debt to fund part of this expansion.

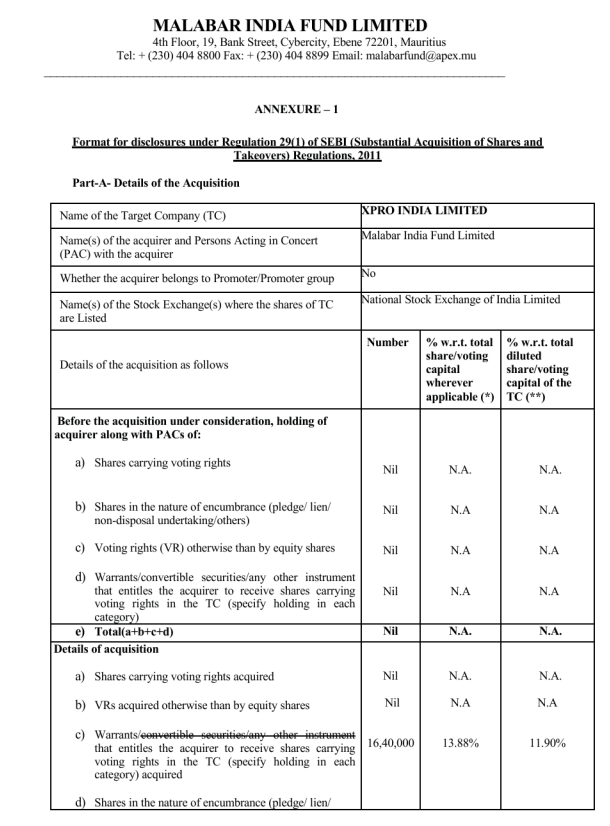

In fact they have already raised some warrants from malabar (one of best FII funds in india headed by Sumeet nagar sir).

Malabar through the warrants owns about >11% of xpro & these warrants will give xpro 100cr+ for funding the capex. More money might be needed.

Malabar through the warrants owns about >11% of xpro & these warrants will give xpro 100cr+ for funding the capex. More money might be needed.

While we are talking about share holding. It is interesting to note that @LuckyInvest_AK (ashish kacholia sir) owns ~4.45% of the company (~55 cr).

Overall, I estimate that profits might grow 4x in 5 years (conservatively).

3. Profitability

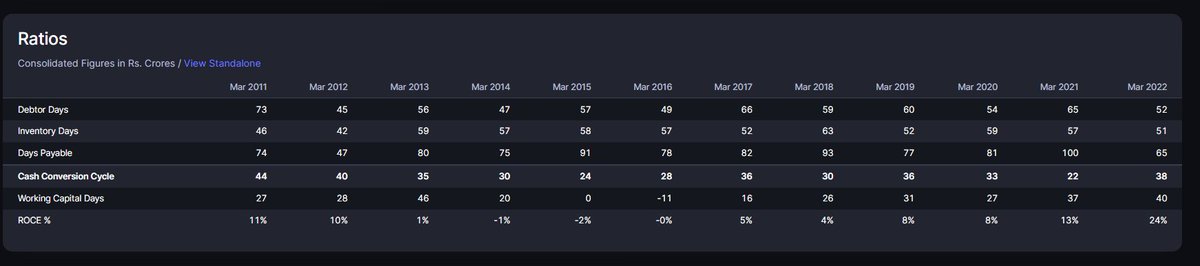

Now that the biax division contributions are increasing, we can naturally see this emerge in the ROE & ROCE of the co.

It is also noteworthy that their WC cycle is quite short at 40 days.

Now that the biax division contributions are increasing, we can naturally see this emerge in the ROE & ROCE of the co.

It is also noteworthy that their WC cycle is quite short at 40 days.

As the product mix changes in favor of biax (due to faster growth) the profitability can grow faster & margins can expand even from here.

The asset tuns for biax division are < 1 (confirmed by my scuttlebutt with capacitor firm MD). I expect 25% or so ROCE for the company as a whole.

4. Industry trends

Vinod ji's speech at "Electronics Manufacturing in Mission Mode" by electronics industries association of India (EIAI).

Watch these videos to understand the industry trends.

Vinod ji's speech at "Electronics Manufacturing in Mission Mode" by electronics industries association of India (EIAI).

Watch these videos to understand the industry trends.

@tushar9590 's tweet on EMS trends In india:

In fact all videos uploaded on EIAI channel deserve to be seen 3 times over.

My scuttlebutt in this space tells me that the supply chain be roughly thought of as being following:

OEM => EMS players => Component makers.

OEM are brands like LG, Apple, Sony, Tata, Mahindra, Voltas

EMS are assemblers like dixon, amber, syrma, virtuoso etc.

OEM => EMS players => Component makers.

OEM are brands like LG, Apple, Sony, Tata, Mahindra, Voltas

EMS are assemblers like dixon, amber, syrma, virtuoso etc.

Component makers are players that make electronic components like Capacitors (Deki, Globe, tibcon, TDK india) , resistors (Shivalik in Shunts).

Now the OEMs are asset light. They outsource manufacturing. The EMS are also asset light since all they do is assembly.

Now the OEMs are asset light. They outsource manufacturing. The EMS are also asset light since all they do is assembly.

In assembly/EMS one can get asset turns as high as 10x or 20x. Its a low margin business. Government of india has taken many steps to promote EMS in india by putting duties on import of mobile phones.

Similar schemes & PLI are being provided for "manufacturing" (this is more like assembling) of while goods.

Read the PLI notification for white goods:

dpiit.gov.in

Read the PLI notification for white goods:

dpiit.gov.in

Components are much more asset heavy. margins are higher, capex requirement is higher. This is something beautifully explained in the video of vinod ji which i had shared. For the past decade india has not been cost competitive with China.

Even today, indian capacitor makers are about 5% or so costly than chinese imports. If the Indian government either provides 5% PLI to indian cap makers or puts 5% ADD on capacitor imports, the manufacturing of capacitors can take off in a large way.

My scuttlebutt tells me that with scale we can eventually become 10% cheaper than china & that is when true blue sky export of deeply backward integrated electronics will take off.

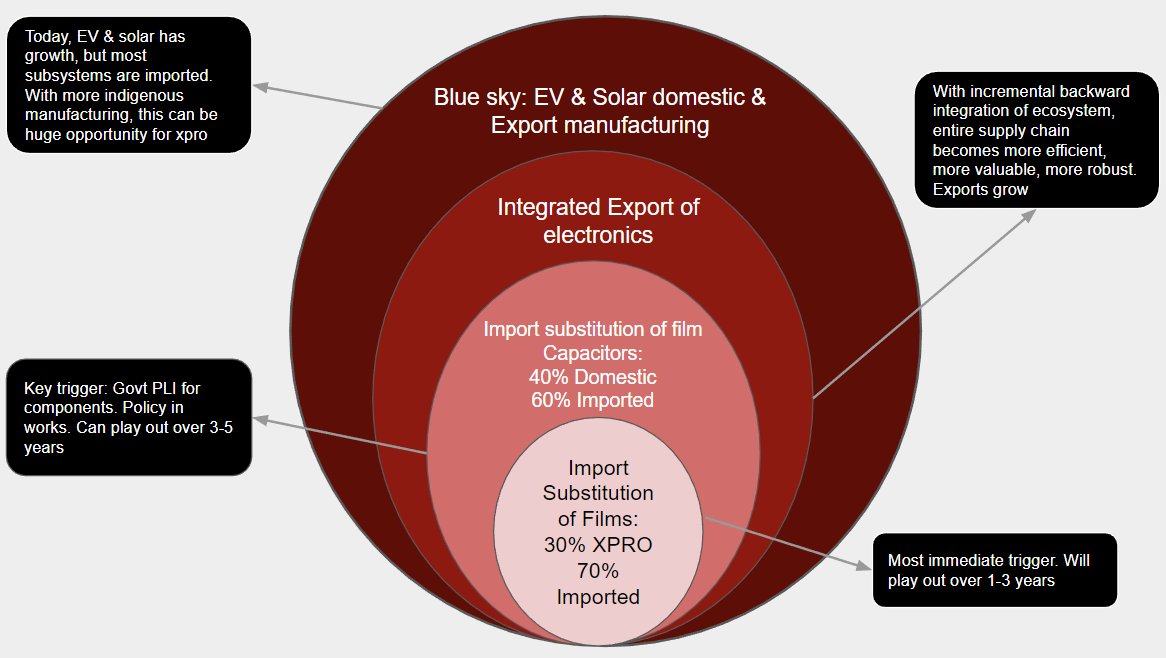

Opportunity set for XPRO is as follows:

Just the inner most circle has a good growth visibility. We are not even counting the outer circles in investment thesis. These are optionality we have. On labor, electricity, finance, land we are becoming cost competitive with china.

Just the inner most circle has a good growth visibility. We are not even counting the outer circles in investment thesis. These are optionality we have. On labor, electricity, finance, land we are becoming cost competitive with china.

5. Moat & competitive positioning

1. Difficult to make & master: Jindal bought treofan in 2018. Still hasnt been able to crack capacitor film making in india.

In fact few days ago, Jindal plant caught a huge fire bqprime.com

1. Difficult to make & master: Jindal bought treofan in 2018. Still hasnt been able to crack capacitor film making in india.

In fact few days ago, Jindal plant caught a huge fire bqprime.com

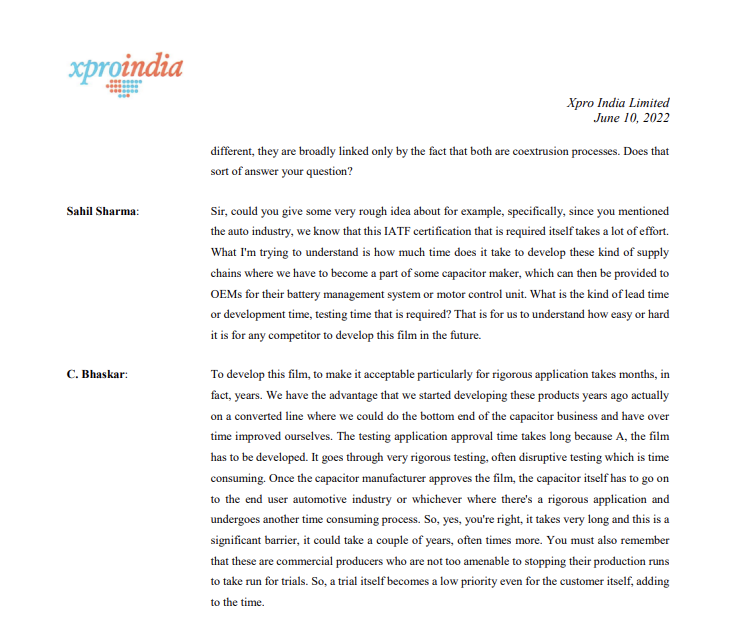

2. Need for Quality: my scuttlebutt tells me that these PP biax dielectric films come in different thicknesses. The thinnest ones (2-3 micron) are toughest to manufacture. Xpro has already mastered these.

For these type of films (which xpro does produce & manufacture), capacitor makers will be very careful about quality since these films go into critical applications & price is NOT the only determining factor.

3. Capital barrier: Making components is hard. The biax film unit has an asset turn of ~1. This means that there is a large capital needed to manufacture these at scale.

4. Supply chain robustness, switching costs: Xpro has to quality & test with Globe Capacitors(as an example). Then Globe with bosch (example). Then bosch with Tata motors. For globe to switch from xpro to X, is difficult.

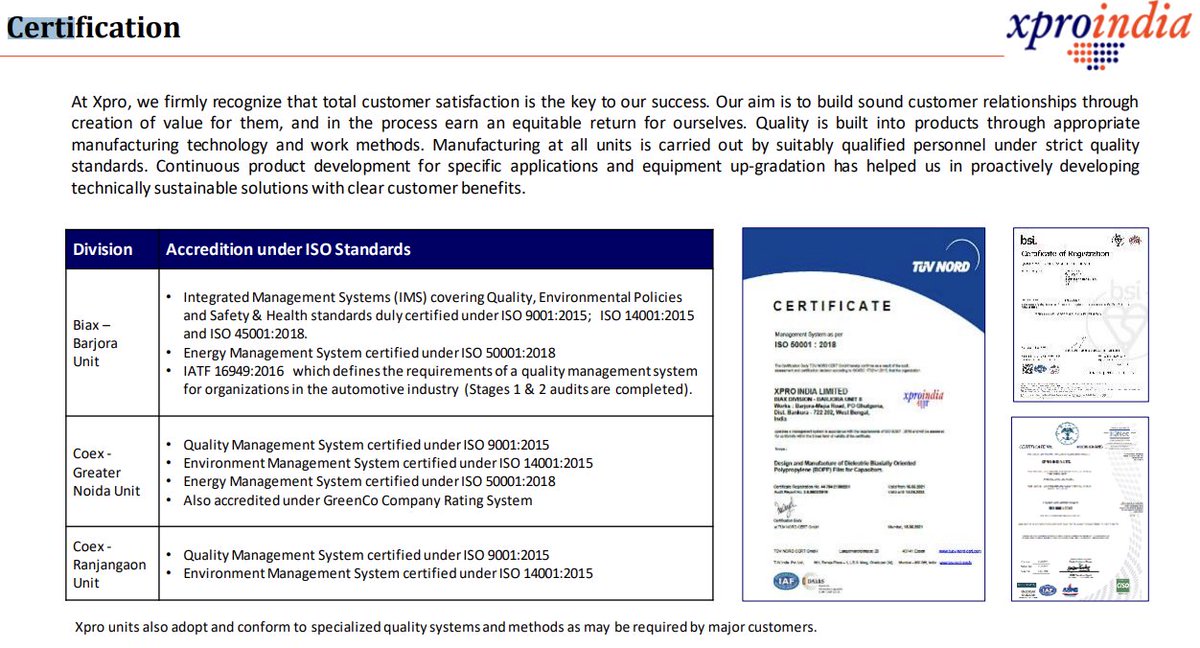

5. Multiple certifications required to ensure that plant & produce is of high quality.

Any new entrant needs all these.

Any new entrant needs all these.

6. Learning curve moat: Xpro has spent more than a decade manufacturing these films that too under inverted duty structure. Necessity is mother of all inventions.

Today, xpro is cost competitive with chinese film makers despite lower scale & without any duties being put on chinese films.

7. Most important one: Xpro has its own customizations & design for the machinery. This makes it difficult for any new entrant to just buy something off the shelf & compete.

6. Valuation

Xpro right now trades at around 20 time earnings. In december it was around 16-17x earnings which IMO is an attractive valuation given the growth, profitability, industry structure, competitive intensity & positioning.

Xpro right now trades at around 20 time earnings. In december it was around 16-17x earnings which IMO is an attractive valuation given the growth, profitability, industry structure, competitive intensity & positioning.

7. Position sizing

Xpro's growth in next 1-1.5 years will be low/slow. This is why i am not in a hurry to build a position.

Xpro's growth in next 1-1.5 years will be low/slow. This is why i am not in a hurry to build a position.

I consider my ~7% position to be a starting position which i intend to build to ~10-12% over time if valuations permit & conditioned on everything else (not finding better opportunities, the competitive positioning, industry structure, growth rates, opportunity size remaining…

…similar or better).

8. Risks & anti-thesis

1. With china opening up, there is always a risk of dumping & increased imports at each stage of value chain. A bet on xpro is essentially one on indian electronics manufacturing ecosystem. Supply chain is only as strong as its weakest link.

1. With china opening up, there is always a risk of dumping & increased imports at each stage of value chain. A bet on xpro is essentially one on indian electronics manufacturing ecosystem. Supply chain is only as strong as its weakest link.

2. The key bottleneck in scaling up is the backlog of machinery. If machinery gets delayed, our XIRR suffers & our holding period also goes up.

3. Jindal or other indian competitor successfully competing & increasing competitive intensity is another anti thesis.

If you like the thread, consider following me at @sahil_vi

Some of older company threads you might enjoy reading:

Some of older company threads you might enjoy reading:

That's all folks.

Have a happy weekend.

Have a happy weekend.

Loading suggestions...