HDFC Bank+HDFC are nearly 15% of the Nifty.

The Bank has added nearly 2.33 lakh crores of deposits last quarter!🤯🤯

The Bank has just posted its results!

A thread🧵analyzing each and every aspect of the HDFC Bank result!

Lets go👇

(1/18)

The Bank has added nearly 2.33 lakh crores of deposits last quarter!🤯🤯

The Bank has just posted its results!

A thread🧵analyzing each and every aspect of the HDFC Bank result!

Lets go👇

(1/18)

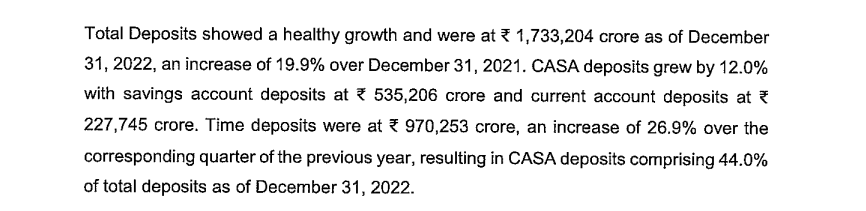

Spectacular deposit growth:-

The system deposit growth was at just 10%

HDFC Bank grew its deposits at a spectacular 20%.

This is the fastest among all the top private-sector banks.

The addition is really impressive

(2/18)

The system deposit growth was at just 10%

HDFC Bank grew its deposits at a spectacular 20%.

This is the fastest among all the top private-sector banks.

The addition is really impressive

(2/18)

Deposits growth is the only way to analyze lenders in an upcycle-

System deposit growth at 10%

HDFC Bank added 2.33 Lakh crore of deposits this quarter(growth of nearly 20%)

They added nearly one Kotak Bank in terms of deposits

The scale for HDFC Bank beats imagination

(3/18)

System deposit growth at 10%

HDFC Bank added 2.33 Lakh crore of deposits this quarter(growth of nearly 20%)

They added nearly one Kotak Bank in terms of deposits

The scale for HDFC Bank beats imagination

(3/18)

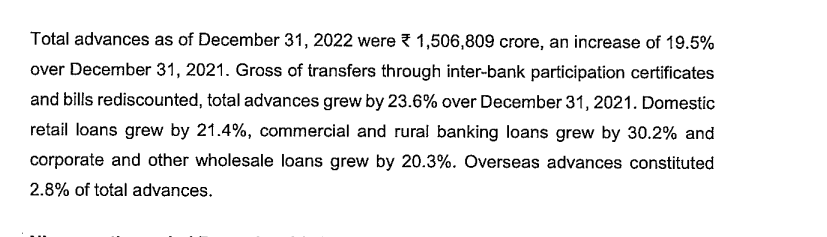

Loan growth:-

🏦The steady 20% growth is back

🏦Retail loan growth grew at 21.4%

🏦Commercial Banking by 30%

🏦Wholesale loans grew at 20%

Overall very steady numbers

(4/18)

🏦The steady 20% growth is back

🏦Retail loan growth grew at 21.4%

🏦Commercial Banking by 30%

🏦Wholesale loans grew at 20%

Overall very steady numbers

(4/18)

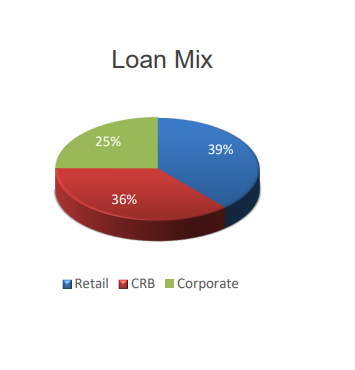

Retail loans now constitute only 39% of the total loan book!

They will not leave opportunities in commercial and wholesale banking!

This is the new HDFC Bank!

(6/18)

They will not leave opportunities in commercial and wholesale banking!

This is the new HDFC Bank!

(6/18)

Verdict:-

HDFC is back with a bang:-

For many quarters as HDFC Bank slowed down the retail loan growth, Analysts doubted them

Now

🏦The deposit growth is exceptional

🏦The missing retail growth is back!

(7/18)

HDFC is back with a bang:-

For many quarters as HDFC Bank slowed down the retail loan growth, Analysts doubted them

Now

🏦The deposit growth is exceptional

🏦The missing retail growth is back!

(7/18)

Net Interest Margin(NIM) Compression:-

Over the last many quarters, the falling NIMs were a concern!

As Interest rates on loan rise

and

Deposit rates go up slowly!

NIM has improved to 4.3%.

This should continue to improve as retail loan growth continues to come back!

(8/18)

Over the last many quarters, the falling NIMs were a concern!

As Interest rates on loan rise

and

Deposit rates go up slowly!

NIM has improved to 4.3%.

This should continue to improve as retail loan growth continues to come back!

(8/18)

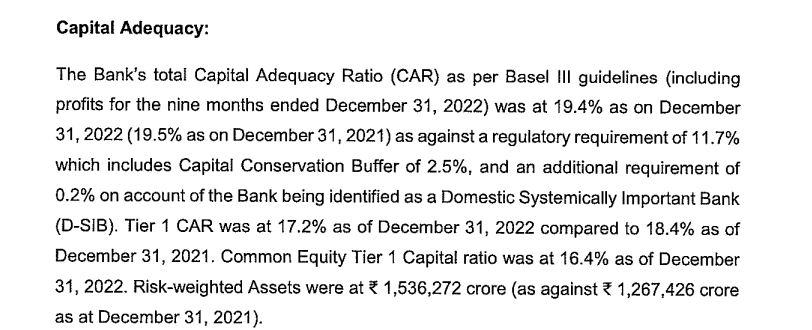

Capital Adequacy:-

The Bank is sitting on a Capital Adequacy of 19.4%

TIER-1 Capital Adequacy at 17.2%

Verdict:-

🏦The bank is adequately capitalized for now.

🏦To fund the merger and meet the regulatory framework the Bank will need to raise capital in the future

(9/18)

The Bank is sitting on a Capital Adequacy of 19.4%

TIER-1 Capital Adequacy at 17.2%

Verdict:-

🏦The bank is adequately capitalized for now.

🏦To fund the merger and meet the regulatory framework the Bank will need to raise capital in the future

(9/18)

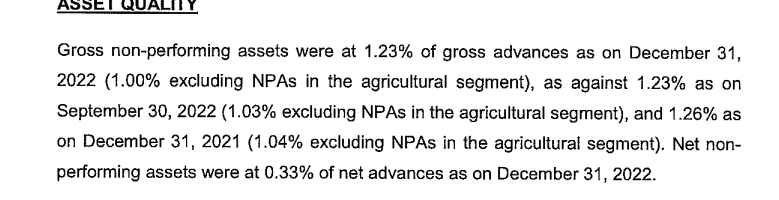

Asset quality:-

🏦The Gross NPAs raimes at 1.23%

🏦Agri Slippages continue to be high

🏦The PCR remains extremely strong at 73.2%

🏦The credit cost ratio came in at 0.74%(best in many quarters)

(10/18)

🏦The Gross NPAs raimes at 1.23%

🏦Agri Slippages continue to be high

🏦The PCR remains extremely strong at 73.2%

🏦The credit cost ratio came in at 0.74%(best in many quarters)

(10/18)

🏦13qtr low provisions; at Rs2805.4cr

🏦ROA is the highest ever at 2.24%

(11/18)

🏦ROA is the highest ever at 2.24%

(11/18)

Verdict:-

🏦COVID-19 problems are behind the Bank

🏦Credit costs have eased up

🏦Restructured book still needs to be monitored

Overall the bank is on a solid footing to capture future growth.

(12/18)

🏦COVID-19 problems are behind the Bank

🏦Credit costs have eased up

🏦Restructured book still needs to be monitored

Overall the bank is on a solid footing to capture future growth.

(12/18)

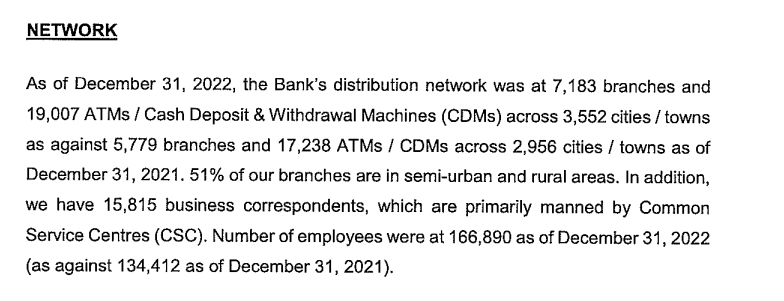

Branch Expansion-

The Bank opened branches aggressively

It opened 684 branches this quarter

The bank envisions to be 1-2 km of clients rather than the current 5-6 Km

Verdict-

The cost/Income ratio is up to 39.2%

This could inflate further for the bank in the near term

(13/18)

The Bank opened branches aggressively

It opened 684 branches this quarter

The bank envisions to be 1-2 km of clients rather than the current 5-6 Km

Verdict-

The cost/Income ratio is up to 39.2%

This could inflate further for the bank in the near term

(13/18)

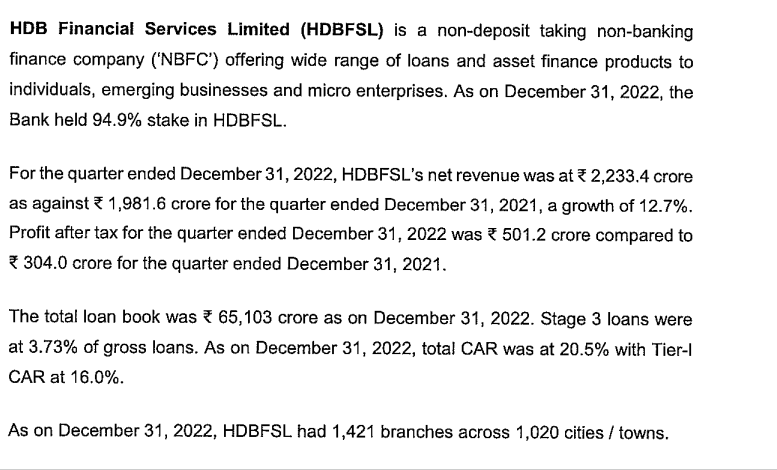

HDB Financial:-

COVID-19 had a severe impact on HDB Financial

The pain is now beginning to ease out.

🏦The revenues grew by 12.7%

🏦PAT showed growth of 501cr vs 304cr

🏦Stage-3 loans stood at 3.73% marginally improving from 4.99%

(14/18)

COVID-19 had a severe impact on HDB Financial

The pain is now beginning to ease out.

🏦The revenues grew by 12.7%

🏦PAT showed growth of 501cr vs 304cr

🏦Stage-3 loans stood at 3.73% marginally improving from 4.99%

(14/18)

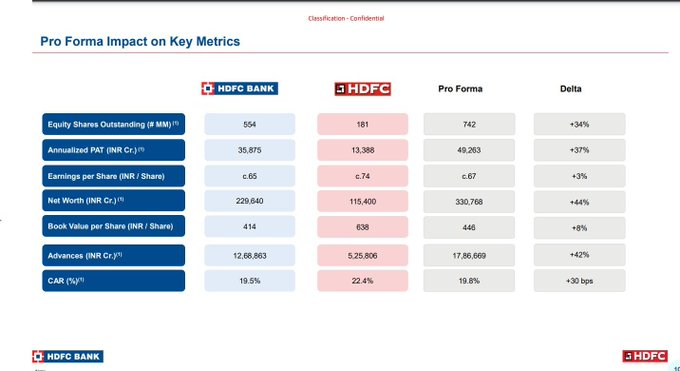

Merger Hangover on HDFC Bank:-

HDFC book will need CRR+SLR provisions.

The book coming from HDFC ltd doesn't have adequate SLR and CRR provisions.

To make those provisions the bank could need to shore up 80-90000cr of capital.

(15/18)

HDFC book will need CRR+SLR provisions.

The book coming from HDFC ltd doesn't have adequate SLR and CRR provisions.

To make those provisions the bank could need to shore up 80-90000cr of capital.

(15/18)

While getting the capital is not a problem.

This is will be a drag on the RoE of the bank in the near term.

The bank has asked for dispensation from the regulator.

However, the regulator is yet to respond.

(16/18)

This is will be a drag on the RoE of the bank in the near term.

The bank has asked for dispensation from the regulator.

However, the regulator is yet to respond.

(16/18)

So How is the result then?

There is nothing to get excited about

There is nothing to complain about

1. Asset quality has stabilized

2. Retail Loan growth is coming back

3. Bank is strongly capitalized to take advantage of future growth

(17/18)

There is nothing to get excited about

There is nothing to complain about

1. Asset quality has stabilized

2. Retail Loan growth is coming back

3. Bank is strongly capitalized to take advantage of future growth

(17/18)

Bank has done well on all parameters

Deposit growth is stunning!

It is now a business on an upward growth trajectory.

(18/18)

Deposit growth is stunning!

It is now a business on an upward growth trajectory.

(18/18)

Disclaimer:-

This is my study

Not an Investment Advise

Please consult your own investment advisor before investing.

This is my study

Not an Investment Advise

Please consult your own investment advisor before investing.

Loading suggestions...