#Chemcon Speciality Chemicals Ltd.

A Techno-Funda 🧵on Chemcon Speciality Chemicals Ltd.(CSCL)

CMP - 290

Technical View 👇

A Techno-Funda 🧵on Chemcon Speciality Chemicals Ltd.(CSCL)

CMP - 290

Technical View 👇

About :

Co. is manufacturer of speciality chemicals. They are:

👉Only Manufacturer of HMDS in India & 3rd largest manufacturer Worldwide

👉Only Manufacturer of Zinc Bromide in India

👉Largest Manufacturer of CMIC Worldwide

👉Largest Manufacturer of Calcium Bromide in India

Co. is manufacturer of speciality chemicals. They are:

👉Only Manufacturer of HMDS in India & 3rd largest manufacturer Worldwide

👉Only Manufacturer of Zinc Bromide in India

👉Largest Manufacturer of CMIC Worldwide

👉Largest Manufacturer of Calcium Bromide in India

Key Business Segments: 👇

HMDS Applications in👇

👉Pharmaceuticals as a silylating agent in drugs manufacturing

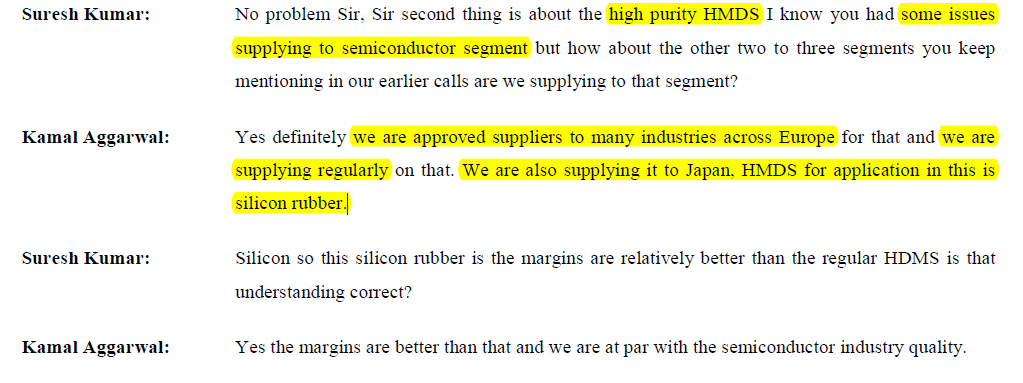

👉Semiconductor: Surface treatment agent of diatomite, white carbon black, titanium & blond additives of photoresist

👉Organic Synthesis: Precursor to many bases common in organic synthesis

👉Pharmaceuticals as a silylating agent in drugs manufacturing

👉Semiconductor: Surface treatment agent of diatomite, white carbon black, titanium & blond additives of photoresist

👉Organic Synthesis: Precursor to many bases common in organic synthesis

CMIC Applications in👇

👉mainly used in pharmaceutical industry as a key intermediate for anti-AIDS, anti-hepatitis B drug Tenofovir

👉used in synthesis of other antiviral drugs

👉mainly used in pharmaceutical industry as a key intermediate for anti-AIDS, anti-hepatitis B drug Tenofovir

👉used in synthesis of other antiviral drugs

Oilwell Completion Chemicals

👉Calcium Bromide- used as a completion & work-over fluid to control wellbore pressures in upstream oil & gas operations

👉Zinc Bromide- used to prepare non-damaging liquids

👉Sodium Bromide used to form clear workaround & drilling fluids.

👉Calcium Bromide- used as a completion & work-over fluid to control wellbore pressures in upstream oil & gas operations

👉Zinc Bromide- used to prepare non-damaging liquids

👉Sodium Bromide used to form clear workaround & drilling fluids.

REVENUE CONTRIBUTION:

HMDS - 51% revenue sare in FY22

CMIC – 26% revenue share in FY22

Bromides – 23% revenue share in FY22

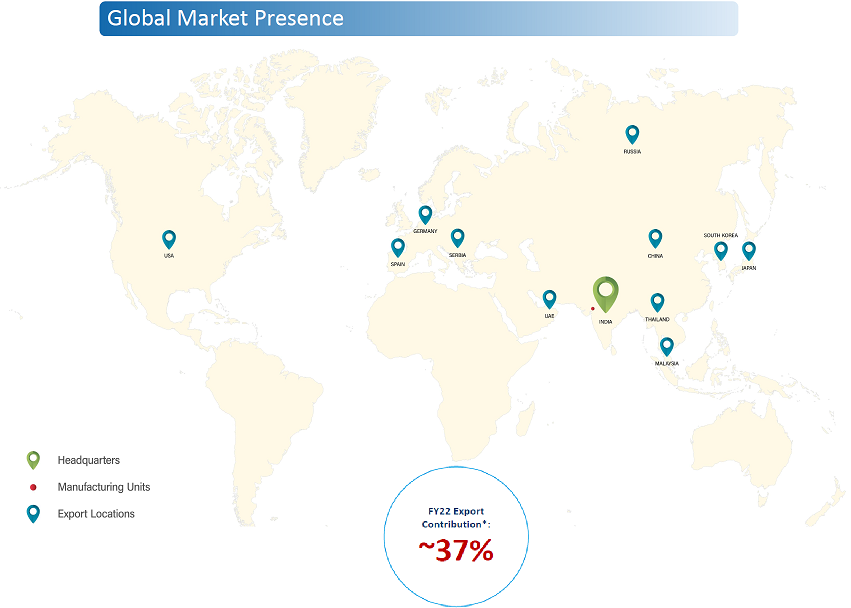

Majorly Manufacturing Exports contributes to 37% from

USA, UAE

Japan, Italy

Spain, Russia

China, Malaysia

Germany, Thailand

& South Korea

HMDS - 51% revenue sare in FY22

CMIC – 26% revenue share in FY22

Bromides – 23% revenue share in FY22

Majorly Manufacturing Exports contributes to 37% from

USA, UAE

Japan, Italy

Spain, Russia

China, Malaysia

Germany, Thailand

& South Korea

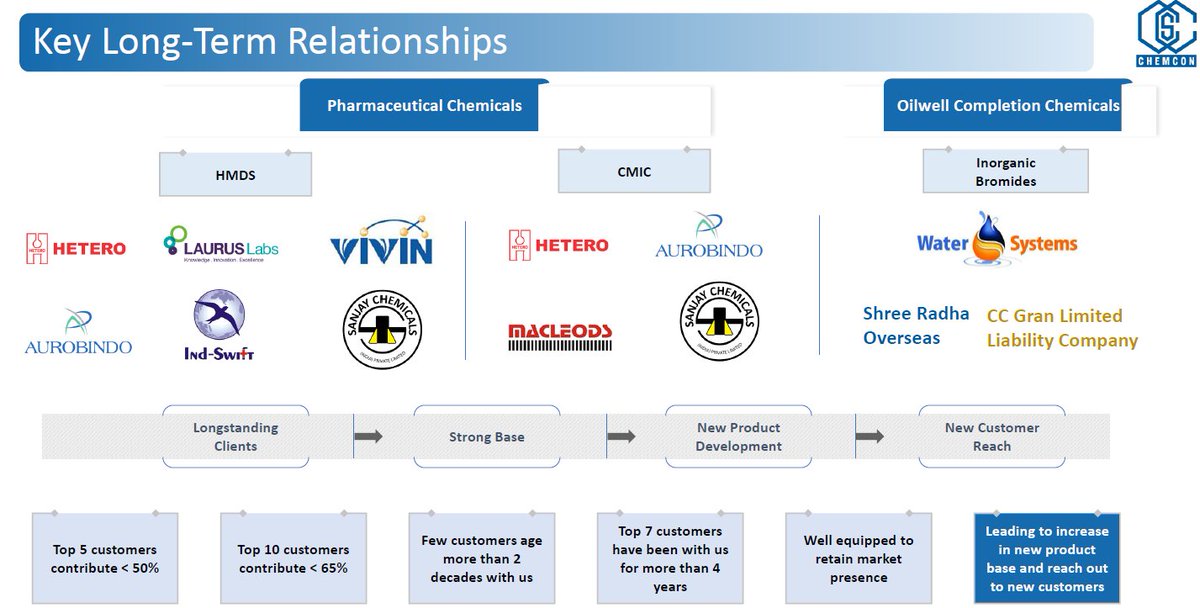

KEY CLIENTELE :

👉Long-Term healthy Relationships with Clients.

👉Long-Term healthy Relationships with Clients.

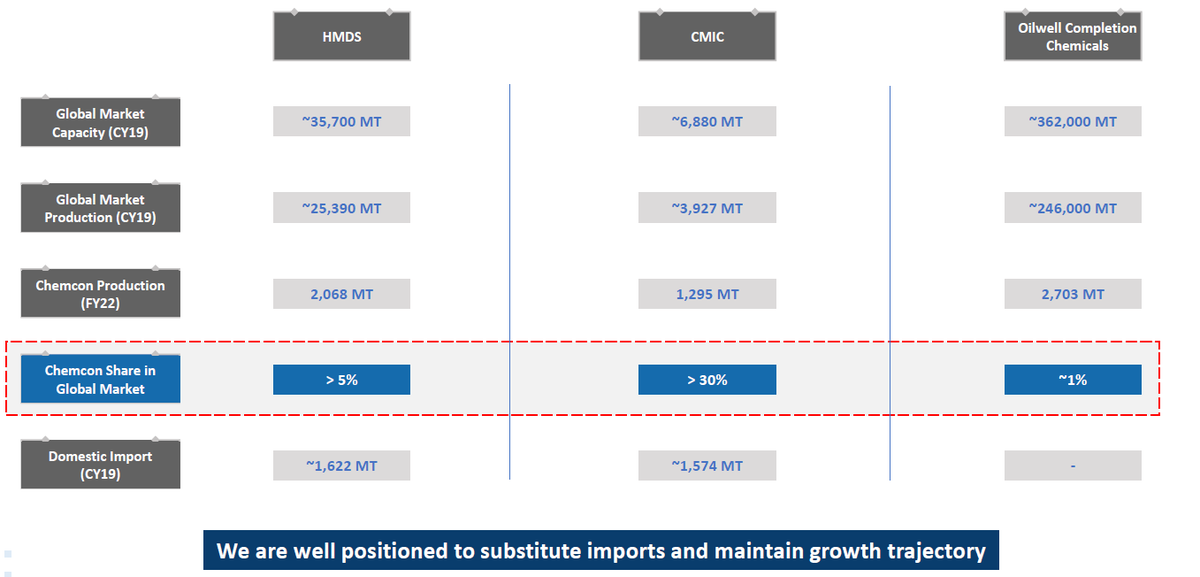

CHEMCON'S MARKET SHARE IN GLOBAL MARKET👇

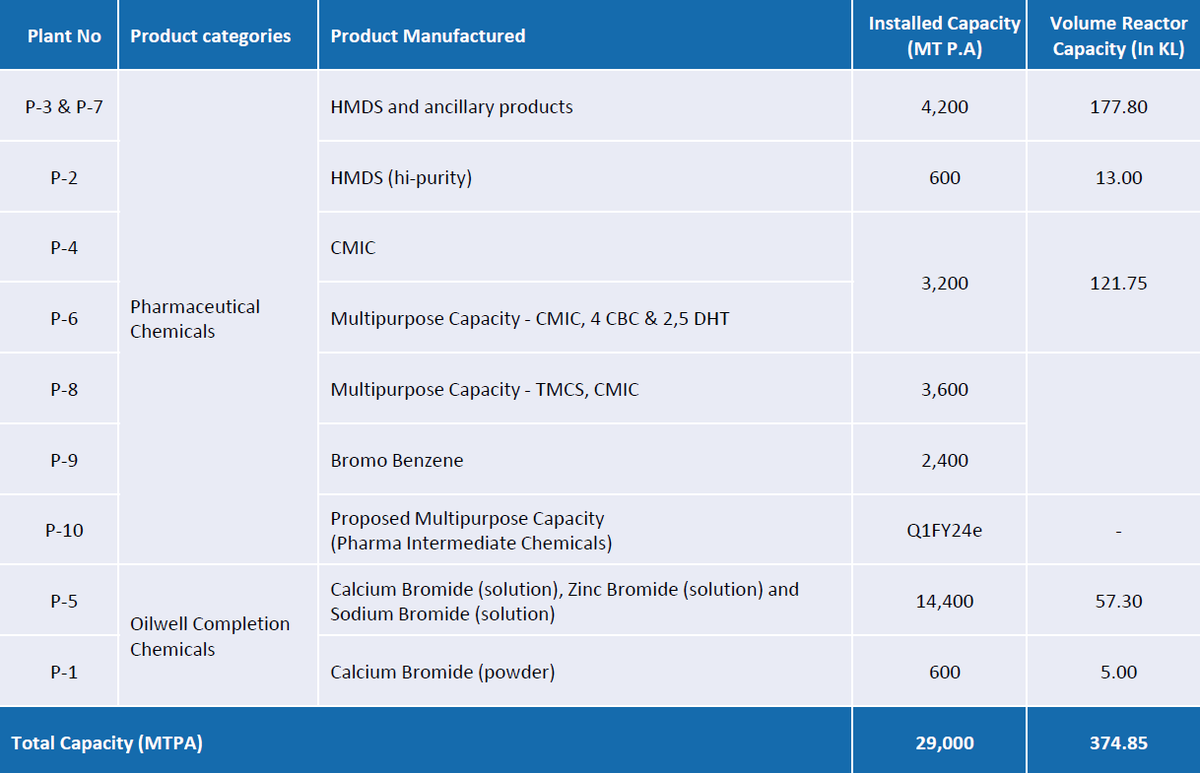

Manufacturing Units:👇

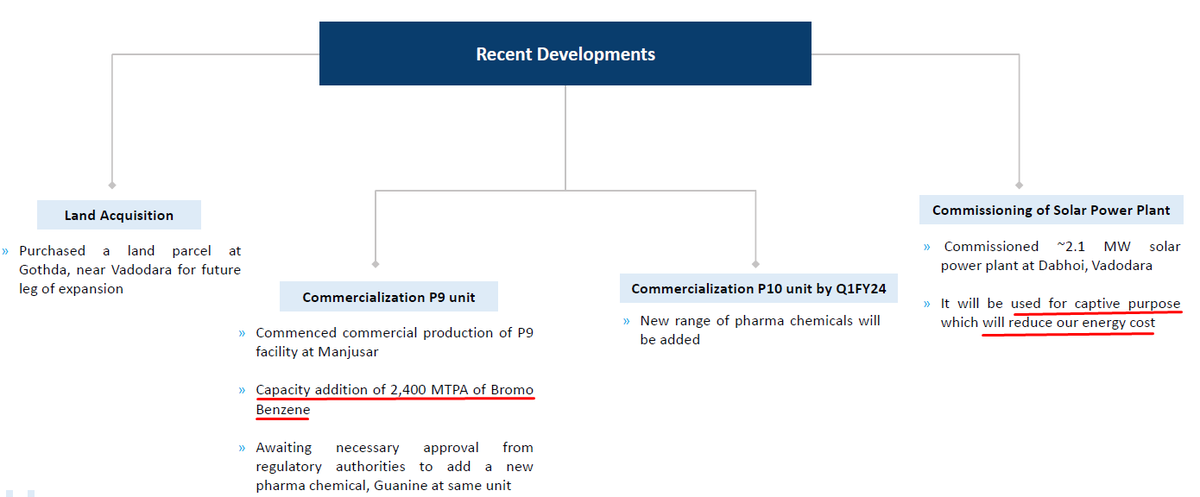

👉Co announced successful commencement of P9 facility by adding 2400 MTPA of Bromo Benzene product

👉Co. guides to commence P-10 facility from FY24 which is currently under construction stage

👉Co. acquired adjacent land which is for further expansion

👉Co announced successful commencement of P9 facility by adding 2400 MTPA of Bromo Benzene product

👉Co. guides to commence P-10 facility from FY24 which is currently under construction stage

👉Co. acquired adjacent land which is for further expansion

UPDATE on CAPEX 👇

FIANCIAL PARAMETERS :

Stock P/E - 15.6

Promotors holding - 74.5%

ROE- 16.3%

ROCE - 20.9%

Debt free Co.

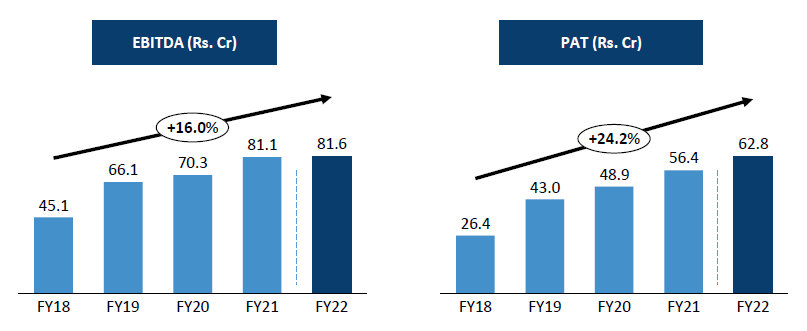

Strong Uptrend in Profit after Tax YoY

Stock P/E - 15.6

Promotors holding - 74.5%

ROE- 16.3%

ROCE - 20.9%

Debt free Co.

Strong Uptrend in Profit after Tax YoY

KEY GROWTH DRIVERS

👉Co product portfolio is well positioned to capitalize Import Substitute theme

👉Co. is expanding its product PF by adding new products & new applications segment like Agro-Chem

👉Co is also looking to reduce dependency on Chinese RM by backward integration

👉Co product portfolio is well positioned to capitalize Import Substitute theme

👉Co. is expanding its product PF by adding new products & new applications segment like Agro-Chem

👉Co is also looking to reduce dependency on Chinese RM by backward integration

KEY RISKS :

High Customer Concentration: Almost 59% of the revenue is generated from the top 5 clients. Any Customer loss may affect significantly.

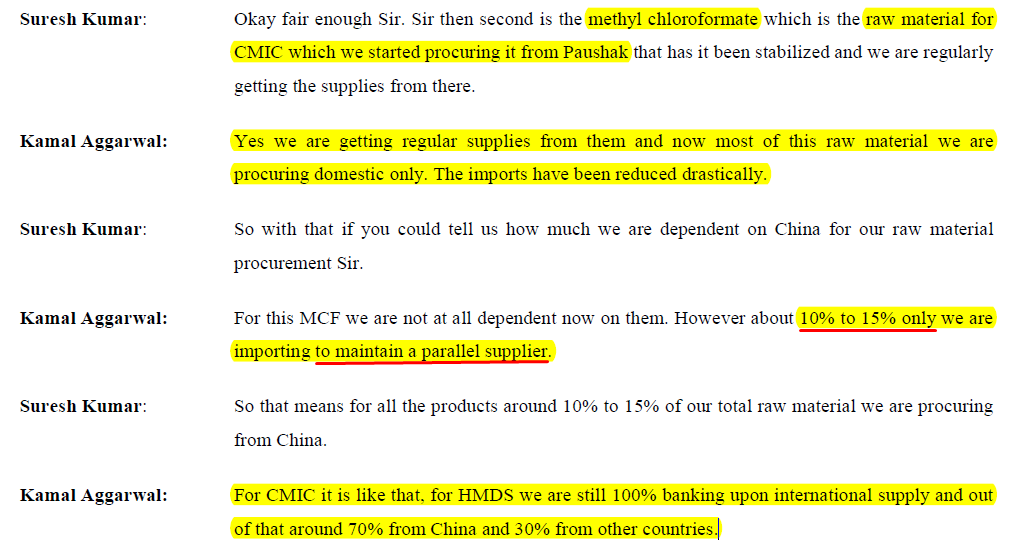

Dependency on China for procuring some of its raw materials.

High Customer Concentration: Almost 59% of the revenue is generated from the top 5 clients. Any Customer loss may affect significantly.

Dependency on China for procuring some of its raw materials.

Q2FY23 CONCALL UPDATE:

👉Co. is procuring Raw Material for CMIC i.e, Methyl Chloroformate from Paushak on regular basis

👉P10 is expected to complete in Mar'23, so that Co. can expect the product out in Q1 2024. The new unit is into import substitute for agro chemical as pharma

👉Co. is procuring Raw Material for CMIC i.e, Methyl Chloroformate from Paushak on regular basis

👉P10 is expected to complete in Mar'23, so that Co. can expect the product out in Q1 2024. The new unit is into import substitute for agro chemical as pharma

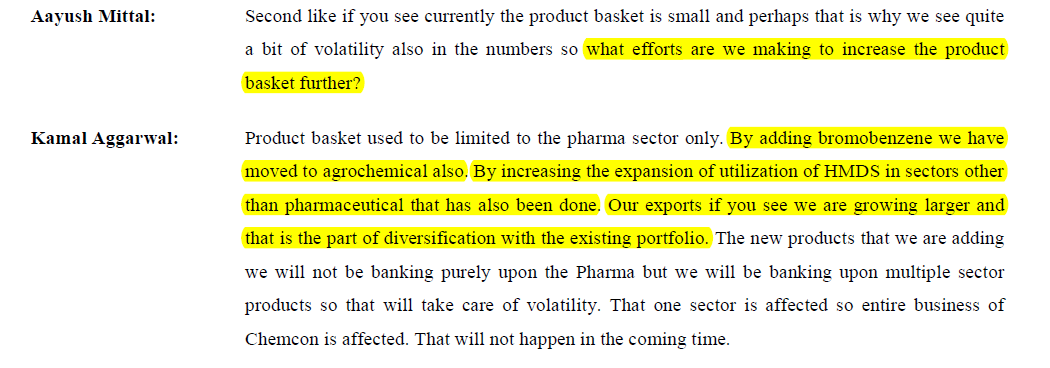

👉Co's efforts towards increasing the product basket towards Agro-Chem also to take care of the volatility affecting entire business of the Co. coz of focus only Pharma.

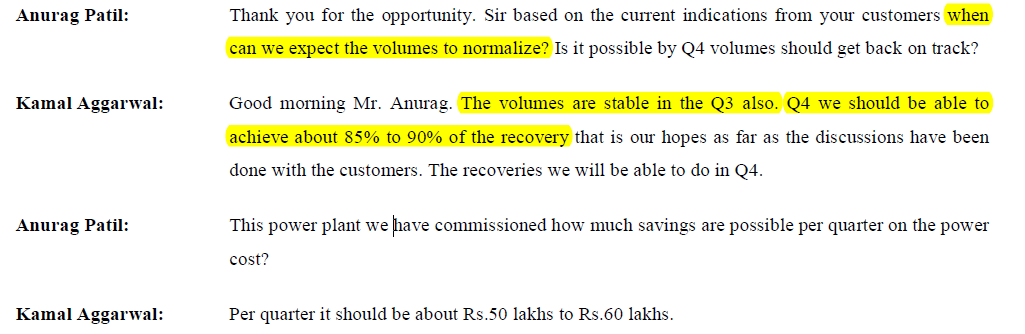

👉Mgmt is 100% confident that EBITDA per kg or may be gross profit per kg again moving to the normal level

👉Mgmt is 100% confident that EBITDA per kg or may be gross profit per kg again moving to the normal level

👉Mgmt expects that the Solar power plant commissioned at Dabhoi reduces the cost by Rs.50 lakhs to Rs. 60 lakhs per quarter.

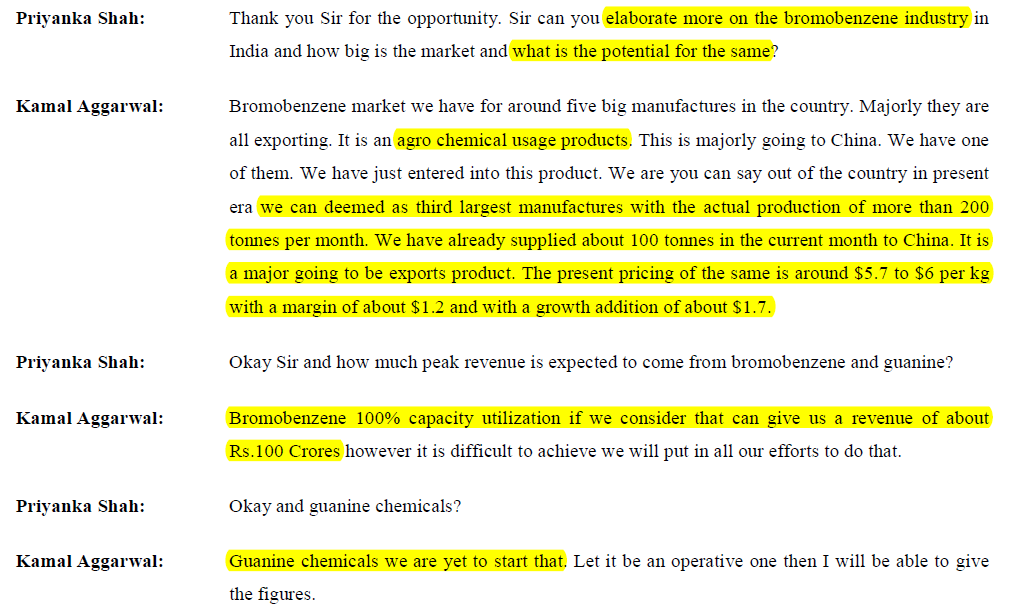

👉Mgmt's view on "bromobenzene" - It had already supplied 100 tons of bromobenzene in November to China. The pricing of this product is around $5.7 to $6/kg with a margin of $1.2.

👉@ 100% capacity utilization of Bromobenzene, Co. is expected a revenue of about Rs 100 Cr.

👉@ 100% capacity utilization of Bromobenzene, Co. is expected a revenue of about Rs 100 Cr.

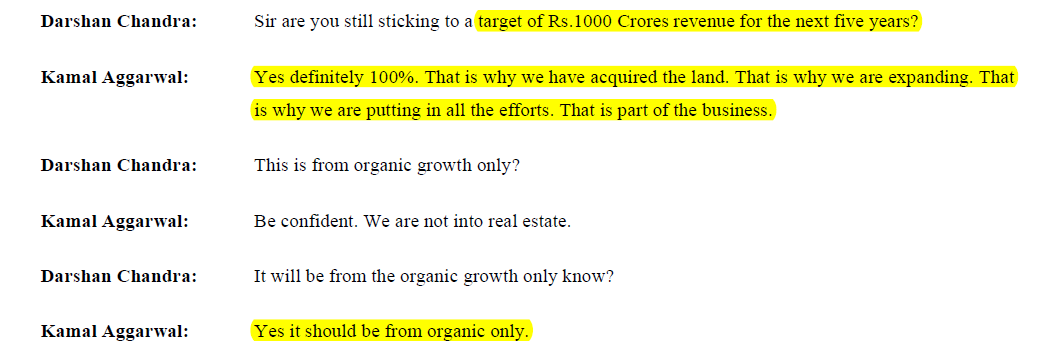

👉Mgmt vision of achieving a target revenue of Rs.1000 Crores in next five years.

👉Co. has almost achieved import substitution for HMDS and CMIC.

👉Mgmt is planning to discontinue the DHT & CBC products as they were not able to penetrate into the supply chain

👉Co. has almost achieved import substitution for HMDS and CMIC.

👉Mgmt is planning to discontinue the DHT & CBC products as they were not able to penetrate into the supply chain

Disc. - Technically, Holding tracking qty @ 325 with strict SL 260 WCB. Will review after Q3 results.

Thanks☺️

--END--

Thanks☺️

--END--

Loading suggestions...