I have tried to write a complete thread on the options in greek. Hope you guys like and appreciate the effort.

Options Greeks include Delta, Gamma, Vega, Rho, and Theta.

A comprehensive explanation of how various #Option Greeks affect option prices.

A comprehensive explanation of how various #Option Greeks affect option prices.

1- delta

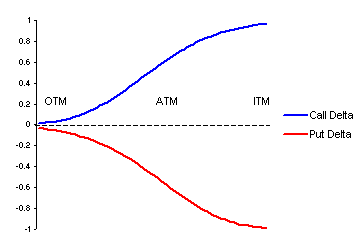

Delta is a way to measure how much the price of an option changes when the price of the underlying asset changes. In other words, if the price of the underlying asset goes up by 1 point, the delta amount will change the price of the option.

Delta is a way to measure how much the price of an option changes when the price of the underlying asset changes. In other words, if the price of the underlying asset goes up by 1 point, the delta amount will change the price of the option.

The delta of a call option is positive, whereas the delta of a put option is negative.

Delta value tends to head toward +1 for calls and -1 for puts as the options get closer and closer to being in the money

Delta value tends to head toward +1 for calls and -1 for puts as the options get closer and closer to being in the money

Good use for hedging the portfolio, determining the hedge ratio requires the use of significant greeks like a delta.

2-Gamma:

The gamma represents the rate of change of the delta about changes in the price of the underlying asset.

The option's delta will shift by gamma if the underlying asset's price moves up by 1 point.

There is a positive Gamma for long options (calls and puts)

The gamma represents the rate of change of the delta about changes in the price of the underlying asset.

The option's delta will shift by gamma if the underlying asset's price moves up by 1 point.

There is a positive Gamma for long options (calls and puts)

As an option moves from being at the money to being out of the money or in the money, its gamma lowers.

In this way of thinking, Delta is the velocity, and gamma is the acceleration, just like you learned in physics class.

In this way of thinking, Delta is the velocity, and gamma is the acceleration, just like you learned in physics class.

3- Vega:

Options Greek Vega (v) gauges an option price's sensitivity to the underlying asset's volatility. The option price will fluctuate by vega if the underlying asset volatility increases by 1%

Options Greek Vega (v) gauges an option price's sensitivity to the underlying asset's volatility. The option price will fluctuate by vega if the underlying asset volatility increases by 1%

A rise in vega generally corresponds to an increase in option value (both calls and puts), whereas a reduction in vega generally corresponds to a fall in option value (Call/puts)

Rising vega is beneficial to option buyers while falling vega is beneficial to option sellers.

Rising vega is beneficial to option buyers while falling vega is beneficial to option sellers.

4-Rho:

Because options prices are less susceptible to interest rates, Rho () is the least significant Option in Greek. If the interest rate rises by 1%, the option price rises by the same amount

Because options prices are less susceptible to interest rates, Rho () is the least significant Option in Greek. If the interest rate rises by 1%, the option price rises by the same amount

If interest rates rise, the value of the call option rises while the value of the put option falls.

Similarly, if interest rates fall, the value of the call option falls while the value of the put option rises.

Similarly, if interest rates fall, the value of the call option falls while the value of the put option rises.

5-Theta:

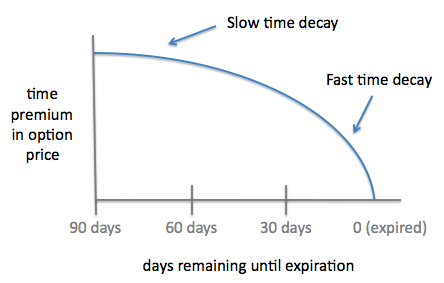

Theta is the most important Option Greek for an Option Seller. A way to measure how sensitive the price of an option is to how long it has until it expires. If the no. of days until the option expires goes down by one

Theta is the most important Option Greek for an Option Seller. A way to measure how sensitive the price of an option is to how long it has until it expires. If the no. of days until the option expires goes down by one

Both options have a negative theta. Because the expiry date is fixed, the premium will melt as the options approach their expiry date.

because it has more time until expiry, the value of the option for far expiry will be greater than the value of the option for near expiry

because it has more time until expiry, the value of the option for far expiry will be greater than the value of the option for near expiry

Loading suggestions...