⭐️ Ambo Agrictec ⭐️

A continuing thread on fundamental & business analysis...

I consider myself no expert in this field- but I'm willing to learn and dig as much as I can.

I could go horribly wrong.

A continuing thread on fundamental & business analysis...

I consider myself no expert in this field- but I'm willing to learn and dig as much as I can.

I could go horribly wrong.

Business overlook:

- Manufacturing of premium biscuits

- Potato chips, extruded snacks,

- edible oils, specialty tea, and specialty-packed food items

- trading of Crude Linseed Oil, and Soybean Meal.

- Manufacturing of premium biscuits

- Potato chips, extruded snacks,

- edible oils, specialty tea, and specialty-packed food items

- trading of Crude Linseed Oil, and Soybean Meal.

Basic ratios to look at:

🟢 Mcap: 35cr (explained below)

🔴 PE: 30

🟢 ROCE: 21%

🟢 ROE: 38%

🟢 ROE: 5%

🔴 D/E: 2.75

🟢 EPS: ₹68

🟢 Promoter holding: 65%

🟢 P/BV: 0.16

🟢 Book Value: ₹241 😳

🟢 10 year sales growth: 17%

🟢 3 year profit growth: 40%

🟢 Mcap: 35cr (explained below)

🔴 PE: 30

🟢 ROCE: 21%

🟢 ROE: 38%

🟢 ROE: 5%

🔴 D/E: 2.75

🟢 EPS: ₹68

🟢 Promoter holding: 65%

🟢 P/BV: 0.16

🟢 Book Value: ₹241 😳

🟢 10 year sales growth: 17%

🟢 3 year profit growth: 40%

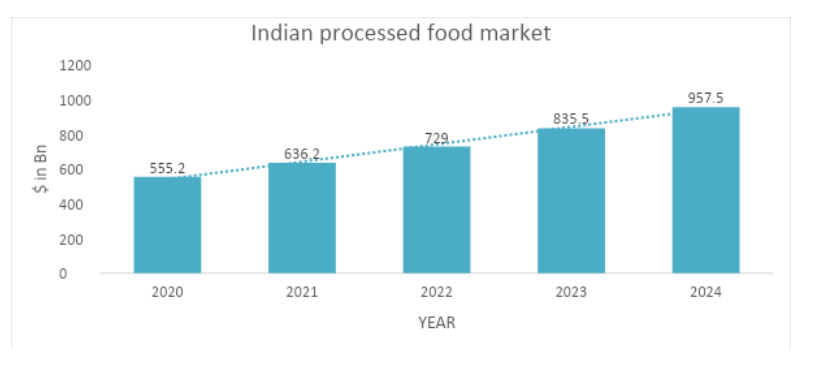

Market Size:

A market cap of just 35cr looks pretty lucrative to me given the industry in which the company has placed itsel

The Indian Food processing Industry has increased substantially from ₹1.34 lakh crore in 2014-15 to ₹2.37 Lakh crore in 2020-21, at a CAGR of 9.97%

A market cap of just 35cr looks pretty lucrative to me given the industry in which the company has placed itsel

The Indian Food processing Industry has increased substantially from ₹1.34 lakh crore in 2014-15 to ₹2.37 Lakh crore in 2020-21, at a CAGR of 9.97%

- The Indian food processing industry is poised for huge growth, given we're the world's 6th largest country aggregating for 32% of the country’s total food market.

- Recession Proof and Govt support: co is beneficiary of Pradhan MantriKisan SAMPADA Yojana (PMKSY)

- Recession Proof and Govt support: co is beneficiary of Pradhan MantriKisan SAMPADA Yojana (PMKSY)

- A new Production Linked Incentive scheme (PLIS) for Food Processing Sector is being implemented to support the creation of global food manufacturing champions. The scheme incentivizes investment and will promote exports and employment in

the sector.

the sector.

- The govt. has put in place an investor-friendly

policy wherein 100% FDI is allowed for food products manufacturing.

- The total FDI inflow in the food processing sector during the last 5 years ending 2021-22 is USD 3.54 billion.

policy wherein 100% FDI is allowed for food products manufacturing.

- The total FDI inflow in the food processing sector during the last 5 years ending 2021-22 is USD 3.54 billion.

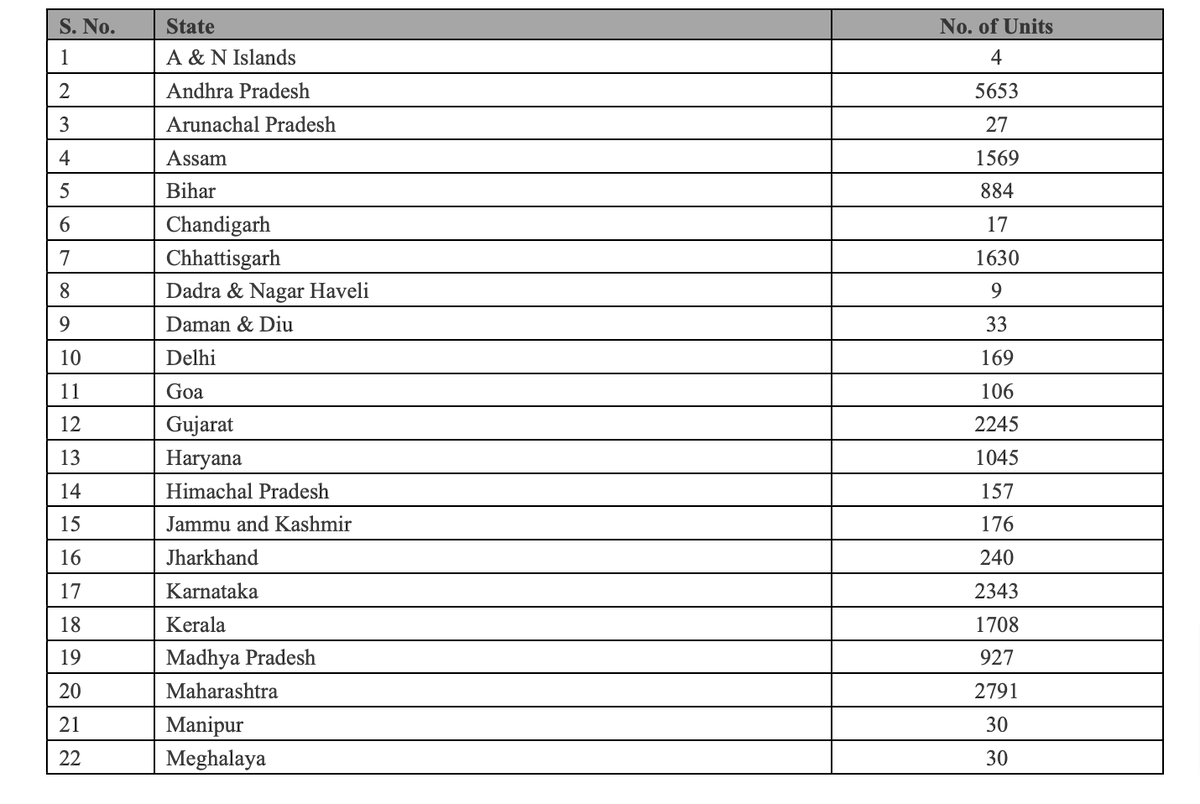

As per the latest Annual Survey of Industries (ASI) 2018-19, released by Ministry of Statistics and Programme Implementation, there are about 40,579 food processing units registered in India.

State-wise number of units as per ASI 2018-19are as under:

(Competitive field)

State-wise number of units as per ASI 2018-19are as under:

(Competitive field)

Why should you invest in food processing business-

Food Processing is a sunrise sector and even with the advent of large MNC players, there is always demand for locally processed food.

Food Processing is a sunrise sector and even with the advent of large MNC players, there is always demand for locally processed food.

The abundance of raw materials and better govt policies are also contributing factors for Food Processing units.

Regional taste preferences can be catered to only by a local brand & this in turn has given rise to a large number of local players who have huge market share in...

Regional taste preferences can be catered to only by a local brand & this in turn has given rise to a large number of local players who have huge market share in...

smaller areas esp Tier 2 and 3 cities.

The presence of good D2C marketing channels has

helped to promote regional brands to become national players as well... (cont.)

The presence of good D2C marketing channels has

helped to promote regional brands to become national players as well... (cont.)

The changing food habits, consumption patterns, low production costs, and food preferences have significantly contributed to the boom in the food processing industry

The food manufacturing sector will be led by the demand in retail and the rise of health-conscious consumers

The food manufacturing sector will be led by the demand in retail and the rise of health-conscious consumers

- The company is based out of Kolkata and has 1 Manufacturing unit & 1 packaging unit in West Bengal

💼 Product Portfolio:

→ Biscuits: Happy Bite, Marie, Crackers, Milk Biscuits, etc

→ Edible Oil: Happy heart

→ Vanaspati: AMBO GOLD

💼 Product Portfolio:

→ Biscuits: Happy Bite, Marie, Crackers, Milk Biscuits, etc

→ Edible Oil: Happy heart

→ Vanaspati: AMBO GOLD

→ Bengali Speciality Products: MAX HEALTH is premium brand for Bengali product range.

Starting from the most popular Gobindobhog Rice, it has several other product ranges like Posto Dana, Sona Moong Dal, Kasuni etc. which are favorites amongst the Bengali families

Starting from the most popular Gobindobhog Rice, it has several other product ranges like Posto Dana, Sona Moong Dal, Kasuni etc. which are favorites amongst the Bengali families

📊 FINANCIAL HIGHLIGHTS :

Revenue:

FY2020 → 7.3cr

FY2021 → 4.7cr (covid dent)

FY2022 → 9.4cr

Q1FY23 → 1.6cr

PAT:

FY2020 → 0.32cr

FY2021 → 0.19 (covid dent)

FY2022 → 1.2cr

Q1FY23 → 0.5cr

Revenue:

FY2020 → 7.3cr

FY2021 → 4.7cr (covid dent)

FY2022 → 9.4cr

Q1FY23 → 1.6cr

PAT:

FY2020 → 0.32cr

FY2021 → 0.19 (covid dent)

FY2022 → 1.2cr

Q1FY23 → 0.5cr

🔴 Top 5 customers (dealer network) contribute to 57% of the total revenue as per FY2023 annual report.

🔴 Top 5 raw material suppliers provide 62% of total input material used in manufacturing of end products.

🔴 Top 5 raw material suppliers provide 62% of total input material used in manufacturing of end products.

🔴🔴 Weakness/ Threats:

→ Market out-reach

→ Heavy dependence on raw material suppliers

→ High working capital requirement

→ Fluctuation in farm output

→ Natural calamity impact

→ Increased Competition from Big Players

→ Change in Government Policies

→ No entry Barriers

→ Market out-reach

→ Heavy dependence on raw material suppliers

→ High working capital requirement

→ Fluctuation in farm output

→ Natural calamity impact

→ Increased Competition from Big Players

→ Change in Government Policies

→ No entry Barriers

Production Capacity: (FY2022)

Biscuits-

Installed Capacity: 3750 MTPA

% of utilization: 70.2%

Biscuits-

Installed Capacity: 3750 MTPA

% of utilization: 70.2%

🟢 Positive points to note:

→ Company was listed in Dec' 2022 with a PE of just 8.80

→ Company raised 10.2cr via SME IPO and the entire portion was 100% fresh issue (big positive)

→ Average Return on Net Worth (RoNW) for FY2022 was 32%

→ Company was listed in Dec' 2022 with a PE of just 8.80

→ Company raised 10.2cr via SME IPO and the entire portion was 100% fresh issue (big positive)

→ Average Return on Net Worth (RoNW) for FY2022 was 32%

I'm not very good at this, pls correct me if I'm wrong- screener + prospectus both show a book value of ₹241, for the three months period ended June 30, 2022 (Not annualized)

and cmp is 37 so P/BV is 0.16 which is too cheap to even give it a 2nd thought.

and cmp is 37 so P/BV is 0.16 which is too cheap to even give it a 2nd thought.

🔴 The debt to equity is 2.75 which is a clear red flag- but promoters have commented that the funds raised via IPO will be used against debt reduction.

so we can only hope that this number falls in the coming quarters..

so we can only hope that this number falls in the coming quarters..

Loading suggestions...