The fastest way to lose money in this market?

Trade the wrong strategy.

Over the last 12 months, the markets have been all over the place.

So use the Hurst exponent to pick the right trading strategy.

Here’s how to do it (in a few lines of Python):

Trade the wrong strategy.

Over the last 12 months, the markets have been all over the place.

So use the Hurst exponent to pick the right trading strategy.

Here’s how to do it (in a few lines of Python):

After reading this thread, you will be able to:

• Get market data with the OpenBB SDK

• Calculate the Hurst exponent

• Determine the type of market

But first, a quick primer on the Hurst exponent:

• Get market data with the OpenBB SDK

• Calculate the Hurst exponent

• Determine the type of market

But first, a quick primer on the Hurst exponent:

In case you’re unfamiliar with the Hurst exponent:

• Measure the long-term memory of a time series

• Captures mean reverting or trending behavior

• Traders use it for trading strategy selection

Another nice feature?

It scales from 0 to 1.

Here’s what it means:

• Measure the long-term memory of a time series

• Captures mean reverting or trending behavior

• Traders use it for trading strategy selection

Another nice feature?

It scales from 0 to 1.

Here’s what it means:

The Hurst exponent is always between 0 and 1.

• 0 to 0.5 - Mean reverting (use reversal strategies)

• 0.5 - Random (don’t trade)

• 0.5 to 1 - Trending (use trend-following strategies)

Use it to help find the right strategy for the market.

Let me show you how:

• 0 to 0.5 - Mean reverting (use reversal strategies)

• 0.5 - Random (don’t trade)

• 0.5 to 1 - Trending (use trend-following strategies)

Use it to help find the right strategy for the market.

Let me show you how:

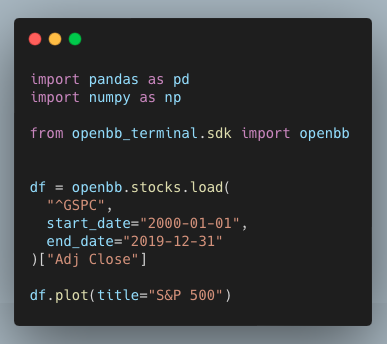

First, import the libraries and get data.

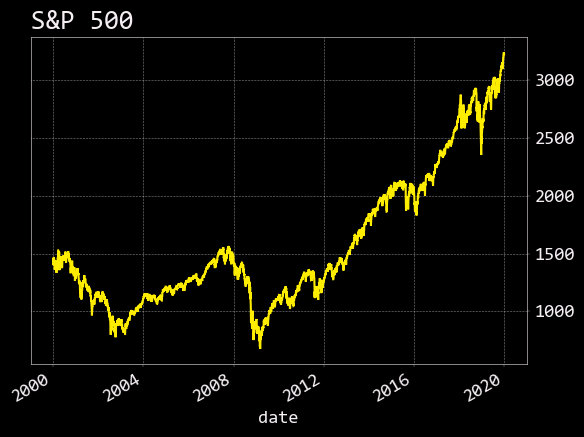

I grabbed 20 years of S&P 500 data and plotted it.

I grabbed 20 years of S&P 500 data and plotted it.

Over the long run, it looks like the S&P 500 has a pretty strong trend.

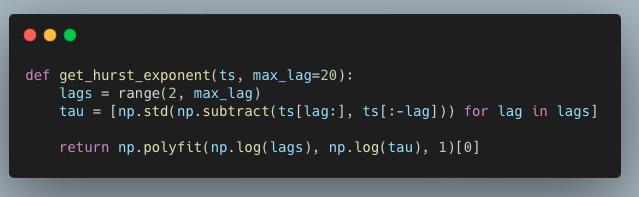

Use the Hurst exponent to quantify it.

Use the Hurst exponent to quantify it.

For each lag in the range, calculate the standard deviation of the differenced series.

Then calculate the slope of the log lags versus the standard deviations with polyfit.

Then calculate the slope of the log lags versus the standard deviations with polyfit.

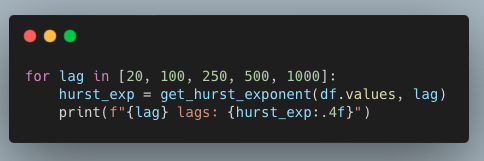

Take a look at how the lag parameter impacts the Hurst exponent.

This will print the Hurst exponent at different lags.

Over the entire time series, the S&P 500 is close to random.

In the shorter lags, there is evidence of mean reversion.

This will print the Hurst exponent at different lags.

Over the entire time series, the S&P 500 is close to random.

In the shorter lags, there is evidence of mean reversion.

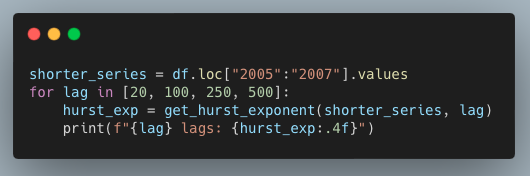

Now, zoom in on a specific period in time.

Just as the Great Financial Crisis hit, the S&P 500 was mean reverting.

In fact, with 500 lags, the Hurst exponent is close to 0.13.

Just as the Great Financial Crisis hit, the S&P 500 was mean reverting.

In fact, with 500 lags, the Hurst exponent is close to 0.13.

Instead of trading the same strategy in every market, use the Hurst exponent to pick the *right* strategy for the market.

• Get market data

• Calculate the Hurst exponent

• Determine the type of market

Now you can!

• Get market data

• Calculate the Hurst exponent

• Determine the type of market

Now you can!

The Hurst exponent is great for trading.

Want to keep this guide handy?

Hop back to the top and retweet the top tweet so you can find it later!

Here's the link:

Want to keep this guide handy?

Hop back to the top and retweet the top tweet so you can find it later!

Here's the link:

The FREE 7-day masterclass that will get you up and running with Python for quant finance.

Here's what you get:

• Working code to trade with Python

• Frameworks to get you started TODAY

• Trading strategy formation framework

7 days. Big results.

pythonforquantfinancemasterclass.com

Here's what you get:

• Working code to trade with Python

• Frameworks to get you started TODAY

• Trading strategy formation framework

7 days. Big results.

pythonforquantfinancemasterclass.com

Loading suggestions...