1/ For crypto LPs, impermanent loss is unavoidable due to volatility (gamma) of assets.

But what if there was a way to long/short gamma? A way to earn extra yield and make impermanent gains?

Enter @Gammaswaplabs - the next primitive that will change DeFi forever

An ELI5 🧵

But what if there was a way to long/short gamma? A way to earn extra yield and make impermanent gains?

Enter @Gammaswaplabs - the next primitive that will change DeFi forever

An ELI5 🧵

2/ In this thread I’ll cover

👾Basic Concepts of Impermanent Loss (IL)

👾How LPs resemble option positions

👾Gammaswap Mechanism + Use cases

👾Roadmap & New Developments

👾Basic Concepts of Impermanent Loss (IL)

👾How LPs resemble option positions

👾Gammaswap Mechanism + Use cases

👾Roadmap & New Developments

3/ What is Impermanent Loss?

IL is best defined as the opportunity cost of providing liquidity to an AMM pool versus holding the assets and selling them directly. It occurs when the price of tokens in a LP pair changes in either direction.

IL is best defined as the opportunity cost of providing liquidity to an AMM pool versus holding the assets and selling them directly. It occurs when the price of tokens in a LP pair changes in either direction.

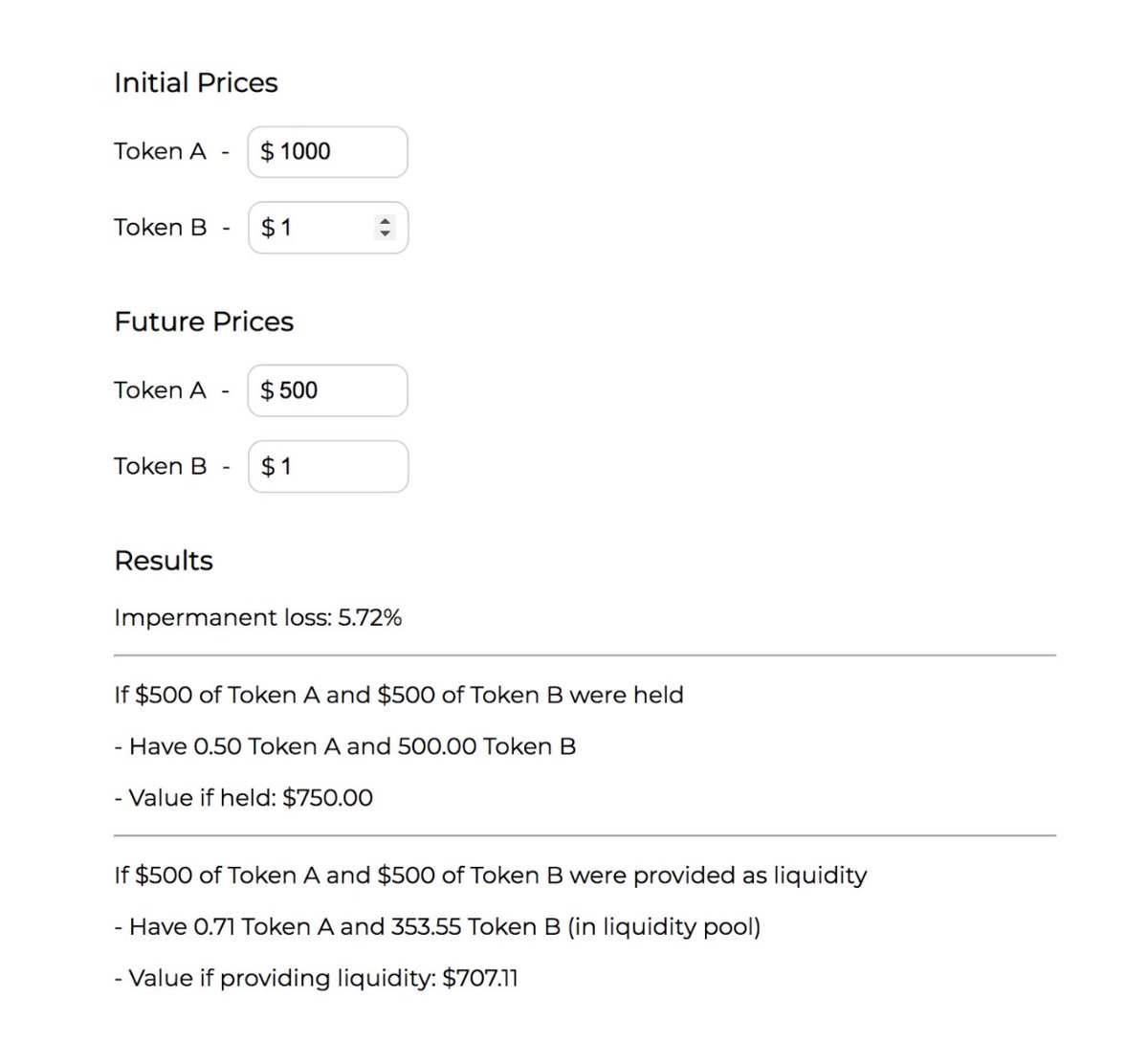

4/ The larger the price change (in either direction) of the underlying token pair, the larger the IL suffered by LPs. Compare the “Future Price of Token A” vs the “Value if held” vs “Value if providing liquidity” between the two screenshots

5/ If you’re interested in learning more about how IL can affect your positions, I’ve linked the calculator for your perusal

dailydefi.org

Back to the topic at hand

dailydefi.org

Back to the topic at hand

6/ As such, LPs are properly incentivized as long as the yield they are receiving from trading fees surpasses the expected IL they face.

7/ Unfortunately for LPs, volatility is not perfectly correlated with trading volume. A shitcoin could have high volatility but measly volume.

8/ So in most situations, LPs aren’t properly compensated for the RISK of providing liquidity. This phenomenon is best explained using options from TradFi.

9/ A quick recap of options terminology before we proceed:

👾Strike price: price at which underlying asset of an option can be bought/sold

👾Call: option to buy an asset at strike

👾Put: option to sell an asset at strike

👾Strike price: price at which underlying asset of an option can be bought/sold

👾Call: option to buy an asset at strike

👾Put: option to sell an asset at strike

10/ Recap continued:

👾Premium: market price of an options contract collected by the writer (seller) of a call/put option

👾At The Money (ATM): when current price = strike price

👾Premium: market price of an options contract collected by the writer (seller) of a call/put option

👾At The Money (ATM): when current price = strike price

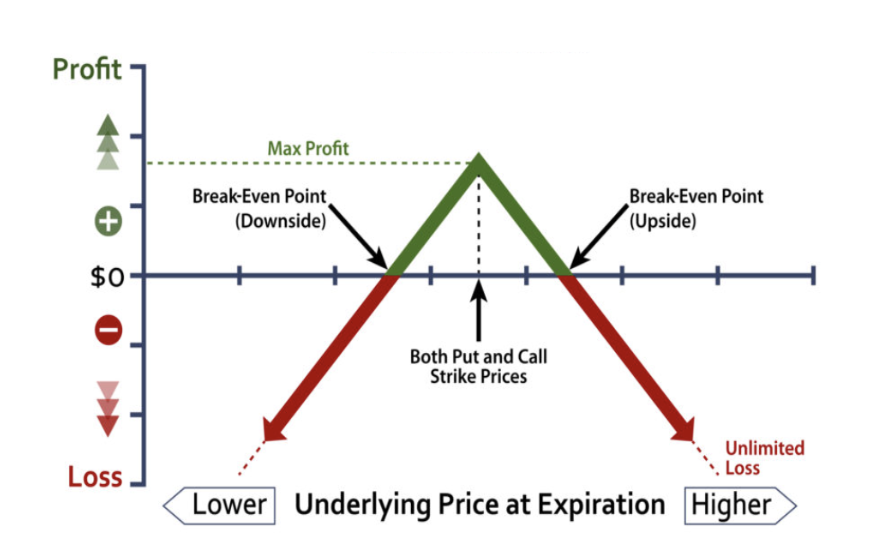

11/ The chart below shows the expected return of an LP. Notice how for all three curves, the returns decrease when the price moves in either direction.

12/ The above return profile resembles the payoff of a short straddle, a common TradFi options strategy where a trader sells an ATM call and an ATM put option, and collects a premium for each option sold

13/ The trader bets on the stability of the price of the underlying asset:

If the price increases, the trader loses money to the buyer of the call option

If the price decreases, the trader loses money to the buyer of the put option

If the price increases, the trader loses money to the buyer of the call option

If the price decreases, the trader loses money to the buyer of the put option

14/ Therefore, if the price moves past a breakeven threshold in either direction, the trader suffers a loss, effectively taking a short position on the volatility of these assets (shown below) since his profitability is dependent on minimal price fluctuation.

15/ AMM LPs adopt the same short position (short straddle) and bear the risk of IL when they provide liquidity. But in TradFi, straddle sellers receive an upfront option premium in exchange for betting against volatility (gamma) for a fixed term

16/ Whereas LPing exchanges volatility for a perpetual stream of payments from trading fees, which are often insufficient as incentives for providing liquidity, let alone as compensation for volatility risk

17/ Consequently, LPs are bleeding cash by selling perpetual short straddles without proper risk-reward bc there is no option to long volatility (i.e. no buyers to pay premium).

18/ LPs are not properly compensated for their risk, and the market is unable to bet on risk. Both factors discourage LPing and stunt liquidity growth in DeFi.

This is where @gammaswaplabs comes in

This is where @gammaswaplabs comes in

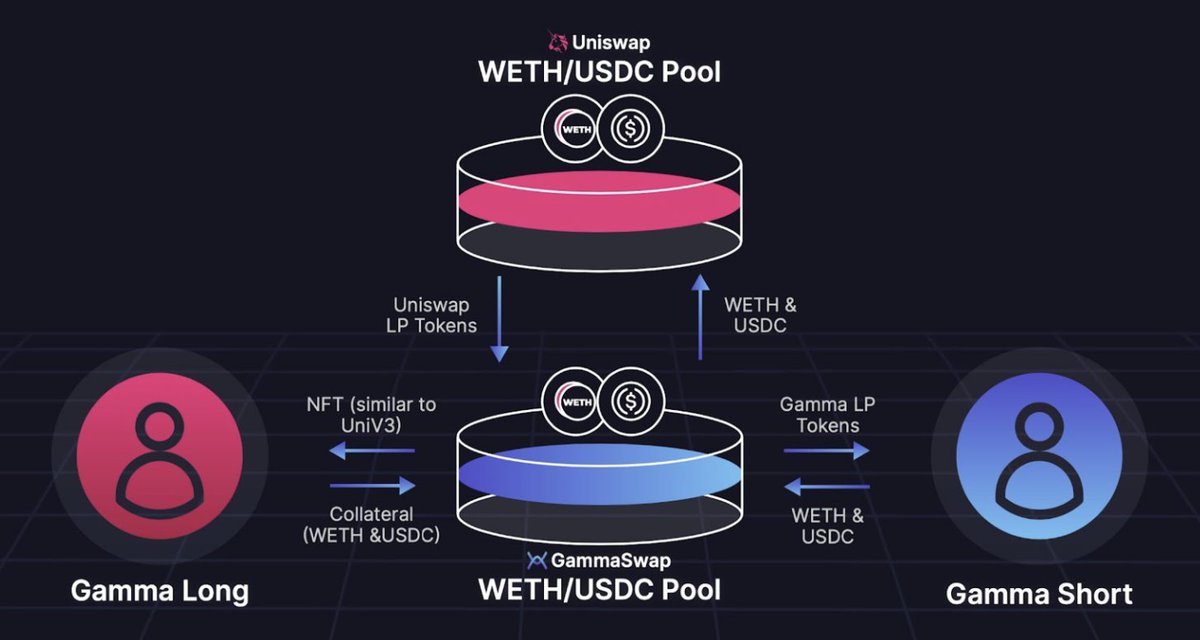

19/ Gammaswap solves these issues by creating an oracle free decentralized platform for trading volatility (gamma). The key innovation is the ability for traders to borrow LP tokens to receive the inverse payoff for IL, also known as impermanent gain

21/ LPs (short gamma), deposit tokens of an LP pair into a vault. Gammaswap deposits the underlying assets into the AMM to provide liquidity

They earn yield from trading fees & additional interest payments (as risk compensation) from gamma longs who borrow their LP tokens.

They earn yield from trading fees & additional interest payments (as risk compensation) from gamma longs who borrow their LP tokens.

22/ Borrowers (long gamma) supply the underlying assets of the LP token as collateral and “borrows” LP tokens from Gammaswap (represented by an NFT position).

23/ Gammaswap then withdraws the underlying LP tokens from the AMM, and holds the assets separately (e.g. USDC & ETH) in a vault contract (opposite position of an LP). Synthetic LP tokens are created to track the borrowing + trading fees of the borrower’s position

24/ If the price of the LP assets move past a certain threshold, the $ value needed to “replenish” the borrowed LP tokens is LESS than the $ value of the LP tokens when they were borrowed

25/ E.g. Token A = $ETH; Token B = $USDC.

Gamma long borrows one LP token when $ETH = $1000. Price of $ETH drops from $500

Value if held = Value LP assets held separately in Gammaswap vault

Value if providing liquidity = Value of AMM LP token

Gamma long borrows one LP token when $ETH = $1000. Price of $ETH drops from $500

Value if held = Value LP assets held separately in Gammaswap vault

Value if providing liquidity = Value of AMM LP token

26/ As such, the borrower can close his position using less $$, and pocket the difference minus trading fees charged by Gammaswap and interest paid to gamma shorts.

27/ The impermanent loss suffered by LPs is earned by the borrower, hence the aptly named term, impermanent gain.

Additionally, impermanent gains for volatile/stable (e.g. ETH/USDC) token pairs are also delta neutral.

Additionally, impermanent gains for volatile/stable (e.g. ETH/USDC) token pairs are also delta neutral.

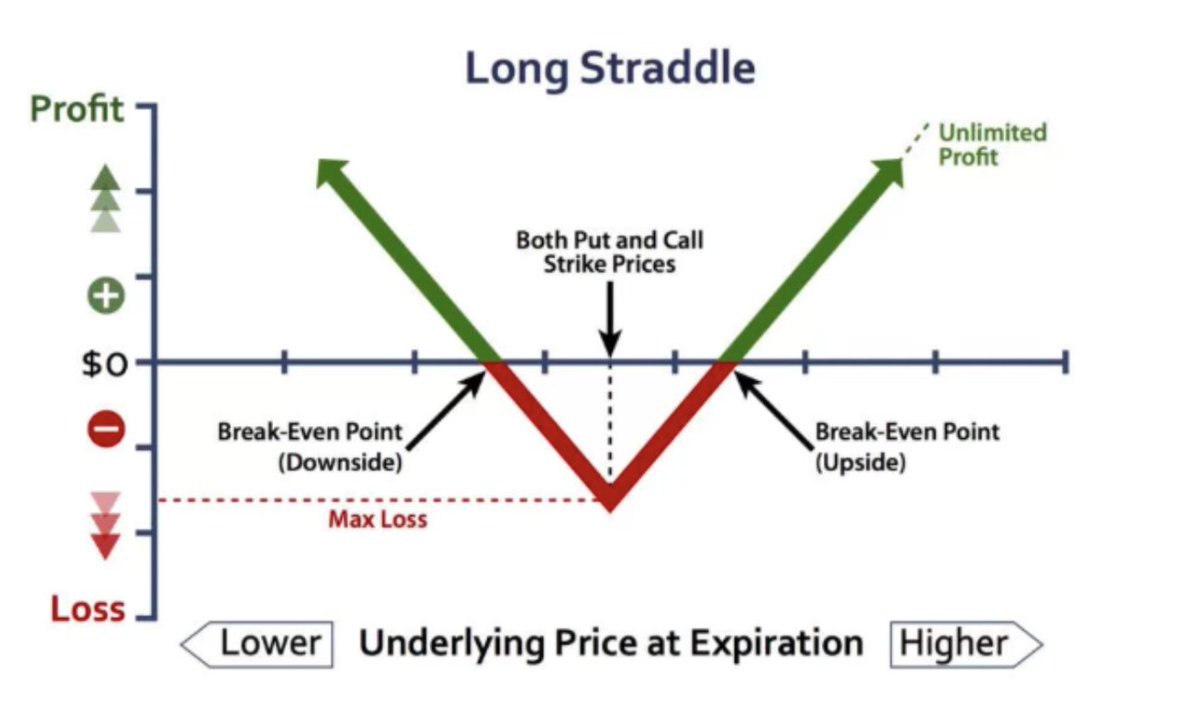

28/ It is worth noting gamma longs are not taking unidirectional bets. They are betting on fluctuations in either direction, i.e. a long straddle in TradFi options (opposite of a short straddle). This strategy is effective when unsure of market direction but expecting volatility

29/ Gammaswap’s upcoming features in their pipeline include:

👾Automated IL hedging vaults

👾DEX for volatility trading

👾Native volatility pools w/o underlying AMM

👾Automated IL hedging vaults

👾DEX for volatility trading

👾Native volatility pools w/o underlying AMM

30/ Also, Gammaswap co-founder @0xDevinG’s proposed token swap with @gmx_io was recently approved. GMX will stake GS tokens received to earn #realyield, and the GMX DAO will decide on how proceeds are used.

31/ Gammaswap will stake GMX for esGMX, and the proceeds will be used to fund future vaults and structured products for both entities. Neither party will sell tokens received.

Full proposal: gov.gmx.io

Full proposal: gov.gmx.io

32/ Other than hedged IL vaults & higher yields for ETH/GMX on Uniswap, the most interesting takeaway is the creation of synthetic calls and puts by combining Gammaswap’s long straddle with GMX’s perp futures

33/ Gamma synths will be composed differently vs GMX synths, which increases optionality for traders and drives fee generation for esGMX holders, further aligning incentives for GMX <> GS.

34/ More fees = more vaults and products = more fees = more vaults….you get the point

A huge win for both parties. TLDR: 🐂ish

A huge win for both parties. TLDR: 🐂ish

35/ Gammaswap also received a grant from @BalancerDAO to build products for their weighted pools as well as hedged IL vaults. Another testament to their utility and game-changing potential.

36/ If you wish to get involved, check out the official Gammaswap testnet guide for wrapped pools. Follow them on Twitter to get notified of their latest updates.

37/ I’m thinking of creating a detailed step-by-step flowchart for Gammaswap’s long / short mechanism (to be added to my research deck). Comment “impermanent gainz” if you want me to do so!

38/ Tagging some gigabrain impermanent gainers

@slappjakke

@Louround_

@CryptoDeFiGuy

@0xJamesXXX

@Patrick_Lung

@ThorHartvigsen

@0xTindorr

@eek637

@charlie_defi

@VoldiemortEth

@charliemktplace

@DegenSpartan

@DefiIgnas

@DeFi_Dad

@thiccythot_

@sgallardo_9

@LouisCooper_

@schizoxbt

@slappjakke

@Louround_

@CryptoDeFiGuy

@0xJamesXXX

@Patrick_Lung

@ThorHartvigsen

@0xTindorr

@eek637

@charlie_defi

@VoldiemortEth

@charliemktplace

@DegenSpartan

@DefiIgnas

@DeFi_Dad

@thiccythot_

@sgallardo_9

@LouisCooper_

@schizoxbt

Loading suggestions...