The India Rising story posits that the next decade will see India displace China as the growth engine of the world. That may or may not be true, but the Hindenburg short selling thesis on the Adani Group tests the weakest links in the India story. bit.ly

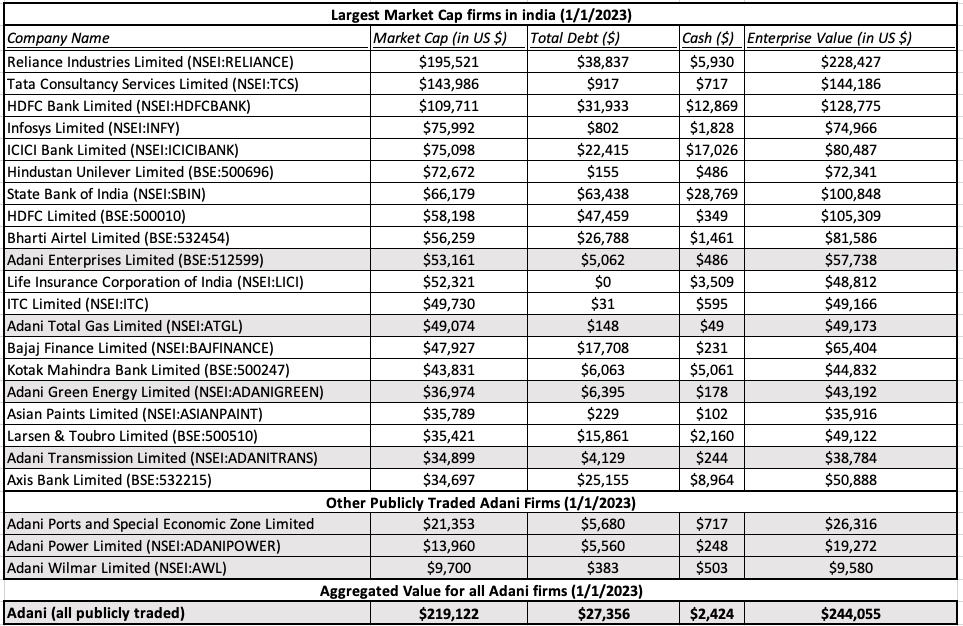

The Adani Group, with Adani Enterprises as flagship, and six other listed Adani companies has risen like a phoenix, and at the start of 2023, it commanded a cumulated market cap of $220 billion, making Gautam Adani the 2nd richest man in the world. bit.ly

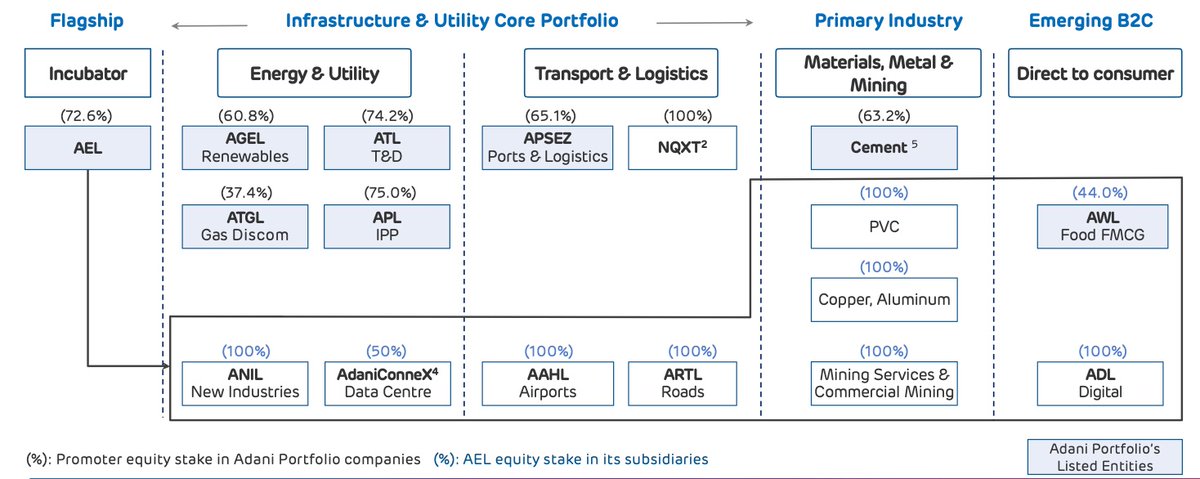

The Adani Group, while spread across businesses, is focused on infrastructure businesses- ports, airports, gas transmission lines & energy - with a footprint in consumer foods. Here is the company's own description of their businesses in 2023: bit.ly

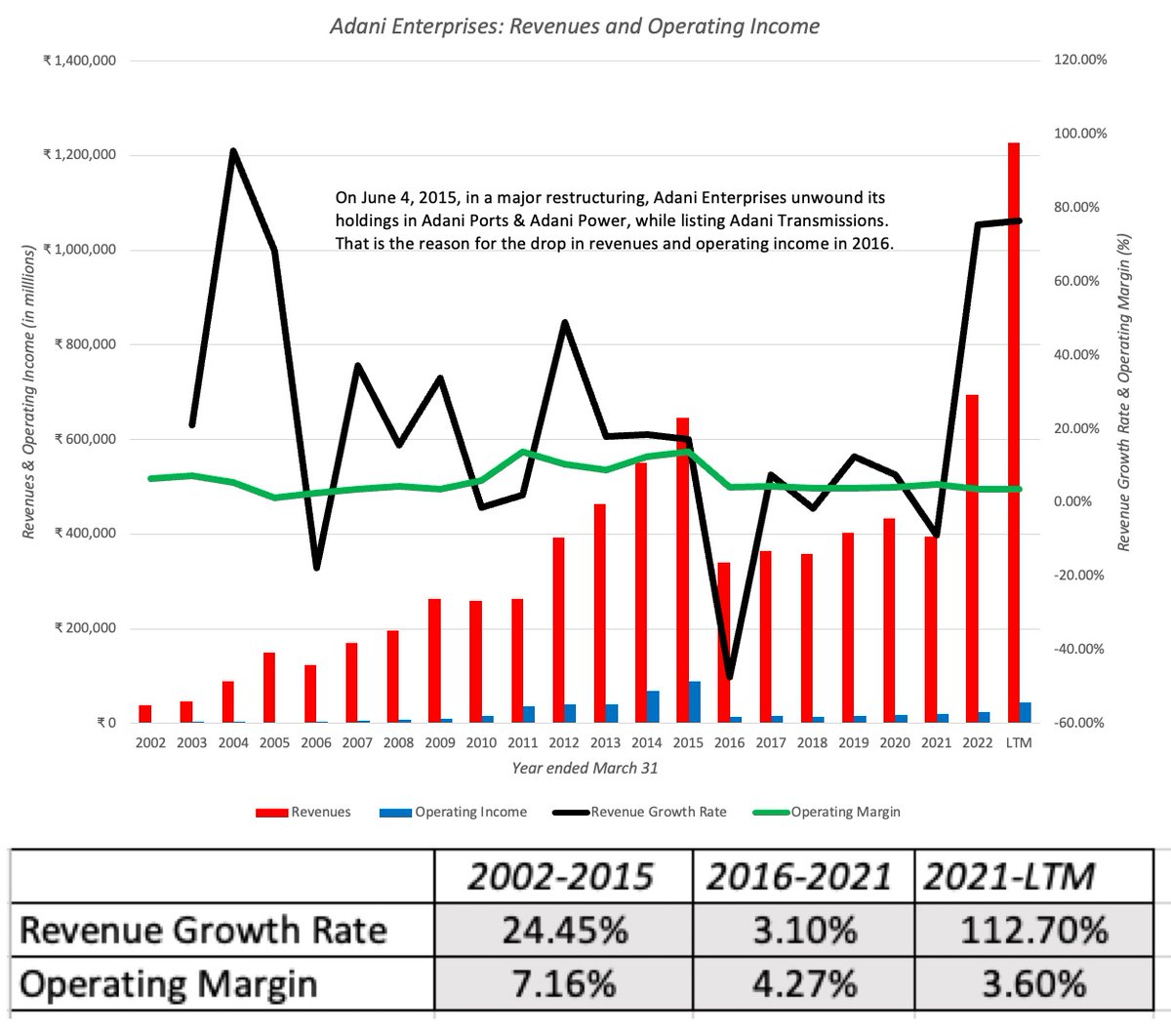

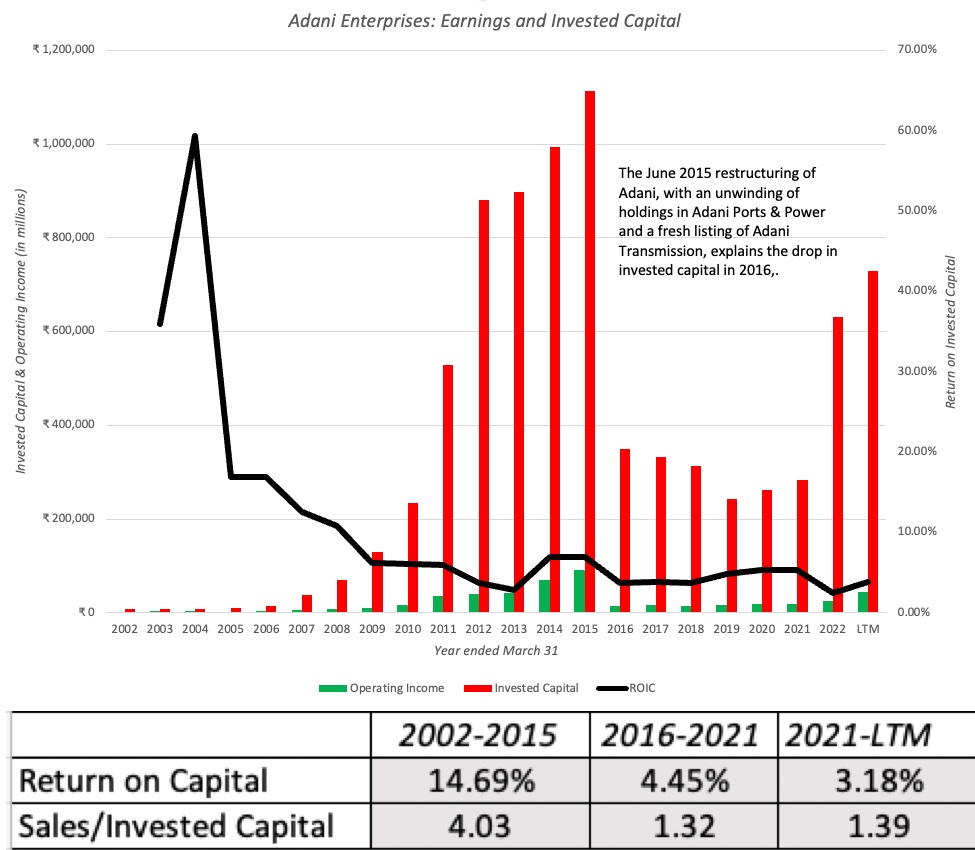

Adani Enterprises has seen revenues rise over the last two decades, but profitability has lagged, partly because investments take time to pay off and partly because it is in low-margin businesses: bit.ly

Not surprisingly, these infrastructure businesses have required immense amounts of capital investment over time, and the company's invested capital has climbed with its revenues. bit.ly

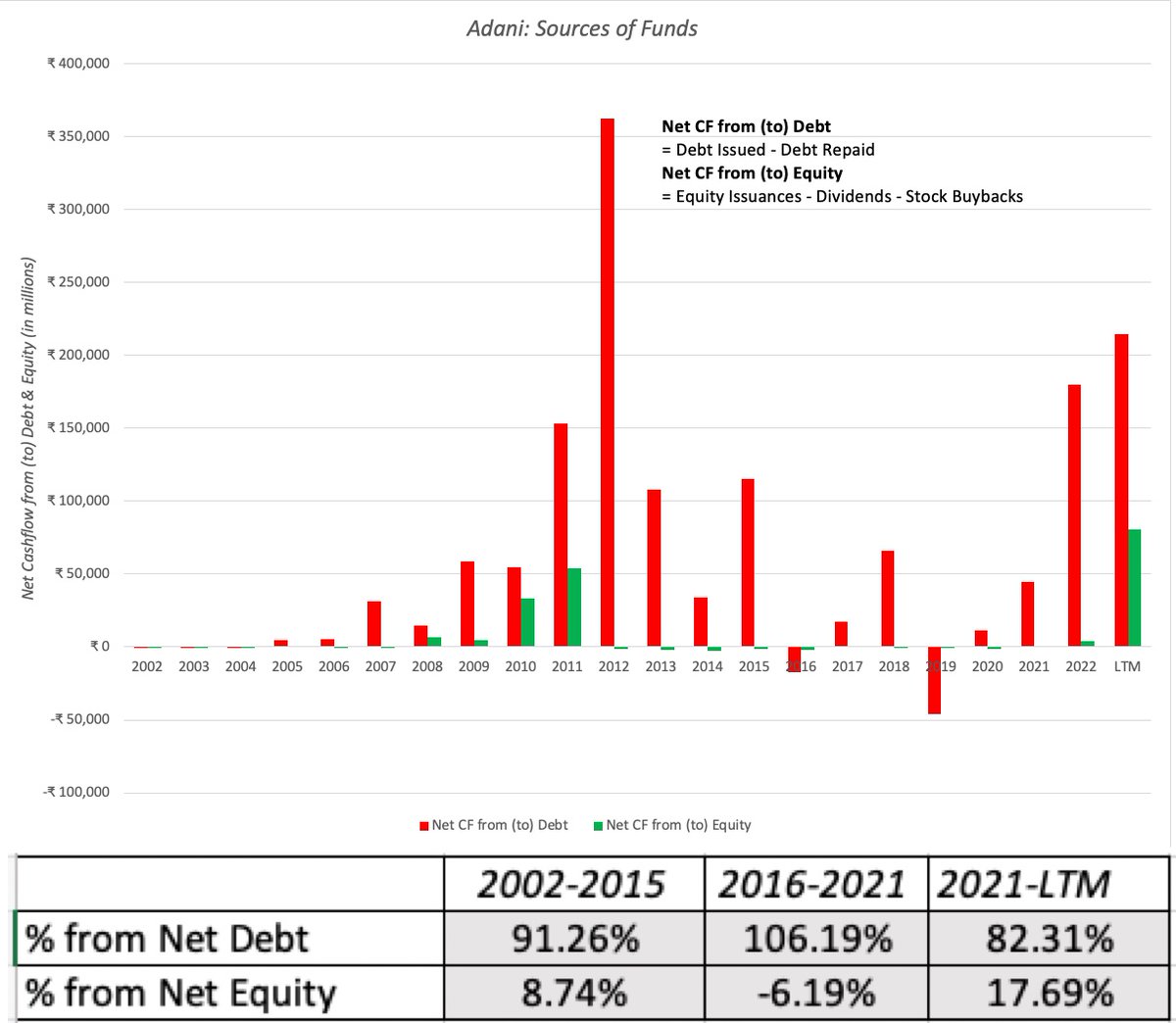

Those investments have been funded almost entirely with debt issuances, though there does seem to be a shift to equity in the last 18 months, driven by lender concerns about leverage & a high market price. bit.ly

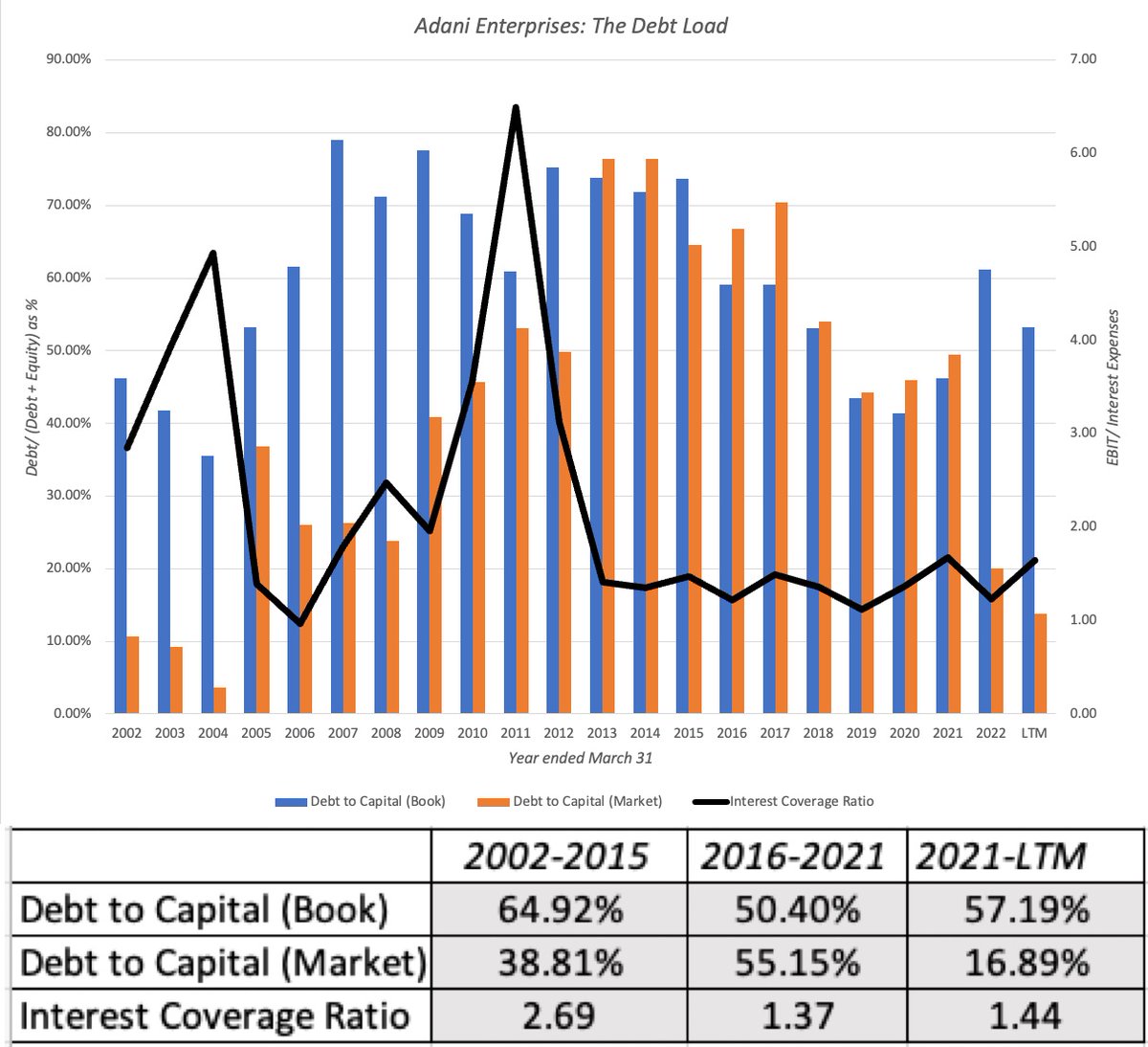

Adani Enterprise's debt metrics reflect this dependence on debt, and paint a picture of a company heavily burdened with debt, but one that is not viewed as being in distress (at least at the moment): bit.ly

The Adani family owns 73% of the outstanding shares in the group's publicly traded company, and that number has not changed appreciably in the last decade, even as the group has grown. bit.ly

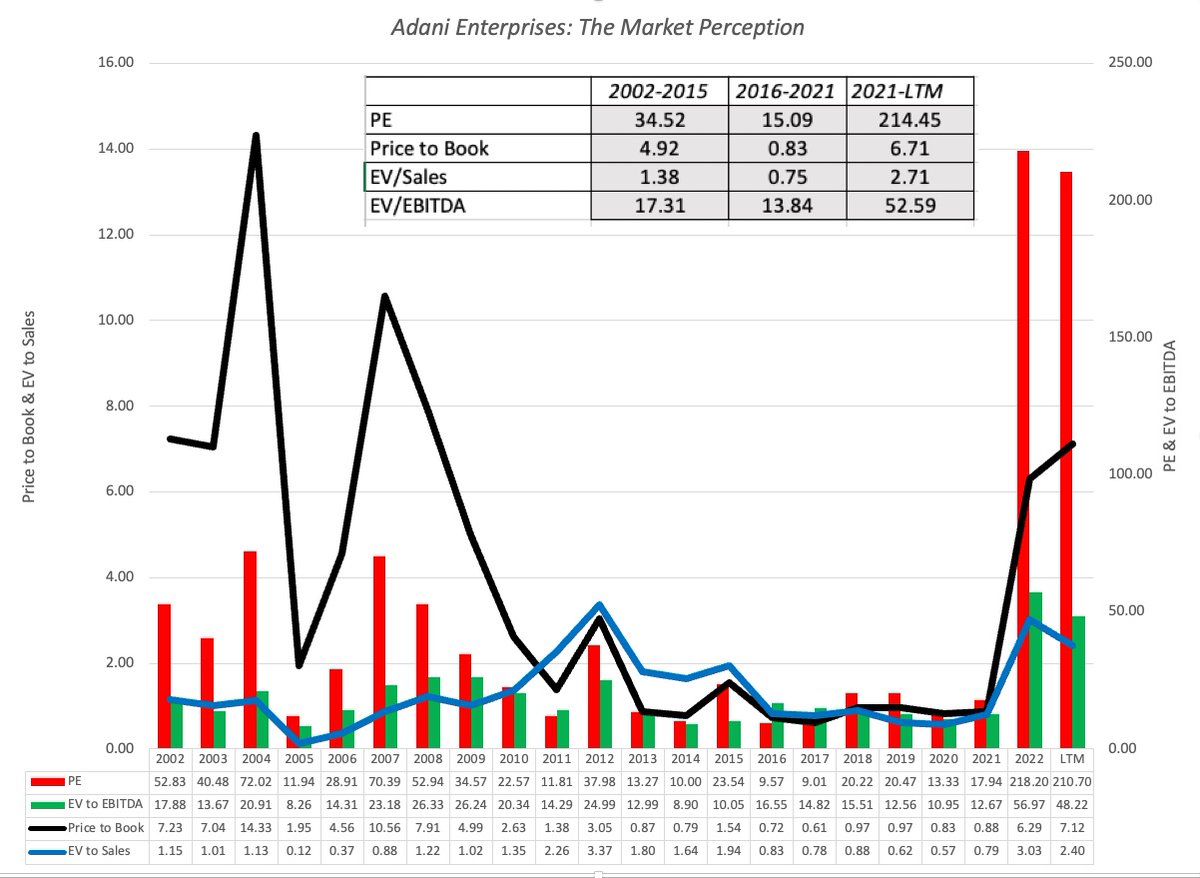

Notwithstanding the low profitability, the group's revenue growth and political connections have drawn investors to it, and its pricing metrics all registered quantum leaps in 2021 and 2022, a strange rush of exuberance for infrastructure businesses. bit.ly

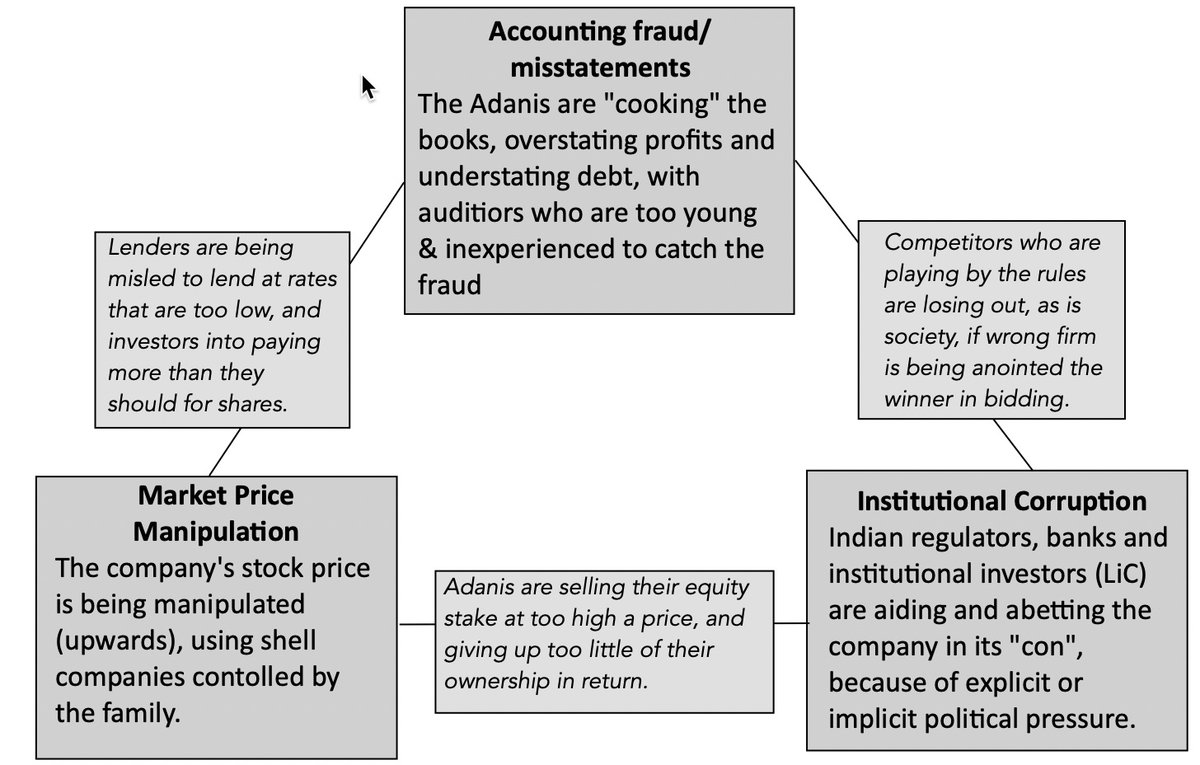

The Hindenburg short-selling thesis is long and detail-filled, some material, some word-of-mouth and some financial, but the core thesis is built around accounting legerdemain, price manipulation and institutional inertia & bias: bit.ly

I think that the group has played fast-and-loose with listing rules, used intra-party transactions to make itself look more credit-worthy & worked its political connections, but if these comprise a con, it has lots of company in India. bit.ly

The Adani Group has too much substance to be a con, but it has exploited the weakest links in the India story - family groups that put control first, a financial market where bullish momentum trading is prized and inertia-bound & political institutions. bit.ly

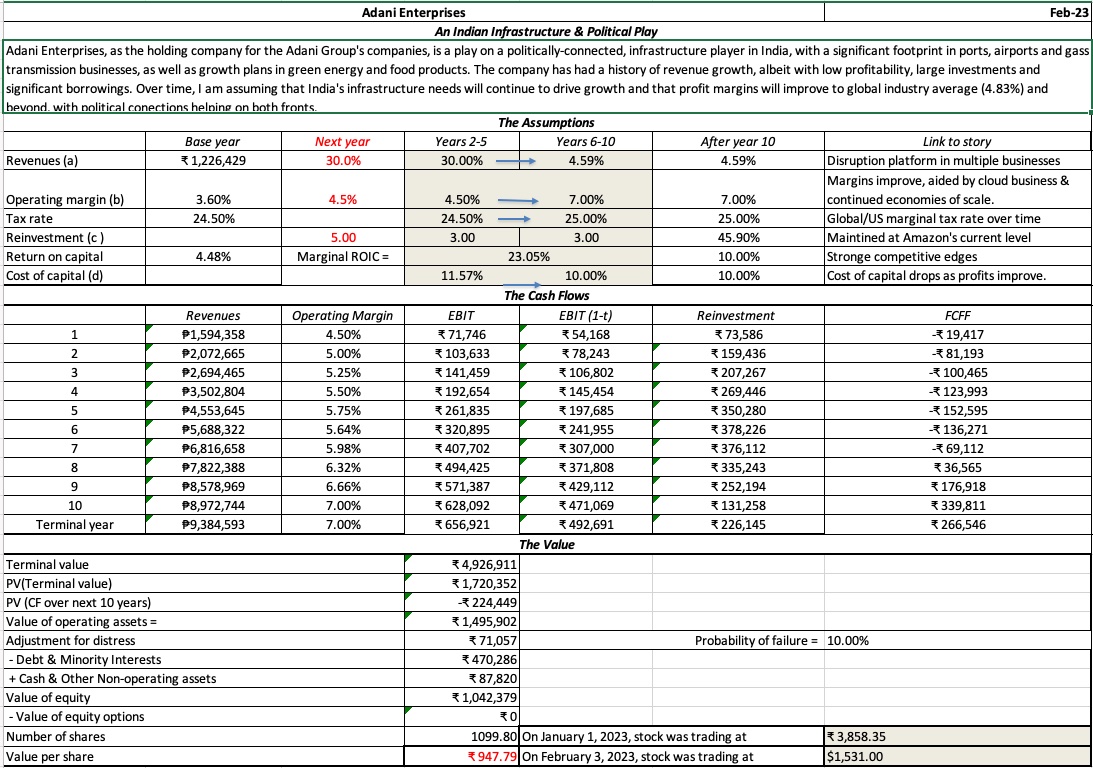

From a valuation perspective, even without factoring in the questions of fraud raised by Hindenburg, I find myself hard pressed to get to a value that is a quarter of the price at the start of 2023 & still higher than the price after last week's meltdown: bit.ly

This is Adani's story, but how India responds to it will affect the trajectory for the India story. It is a chance for Indian institutions (government, regulators, banks, exchanges) to start fixing their legacy problems, but those fixes will not be easy. bit.ly

Loading suggestions...