While APL Apollo (MCap 33000cr) has been one of the BIGGEST success stories of the past decade (200x), a close competitor Surya Roshni (MCap 3300cr, inferior multiples vs APL) at present is revamping & reviving itself to be a prominent player!

A thread👇

1/10

A thread👇

1/10

Engaged in 2 businesses viz. 1) Steel Pipes (80% of Rev) & LED lighting/FMEG (20% of Rev), Surya is one of the most respected brands in both these segments within India (72% of Rev) & internationally (28% of Rev).

2/10

2/10

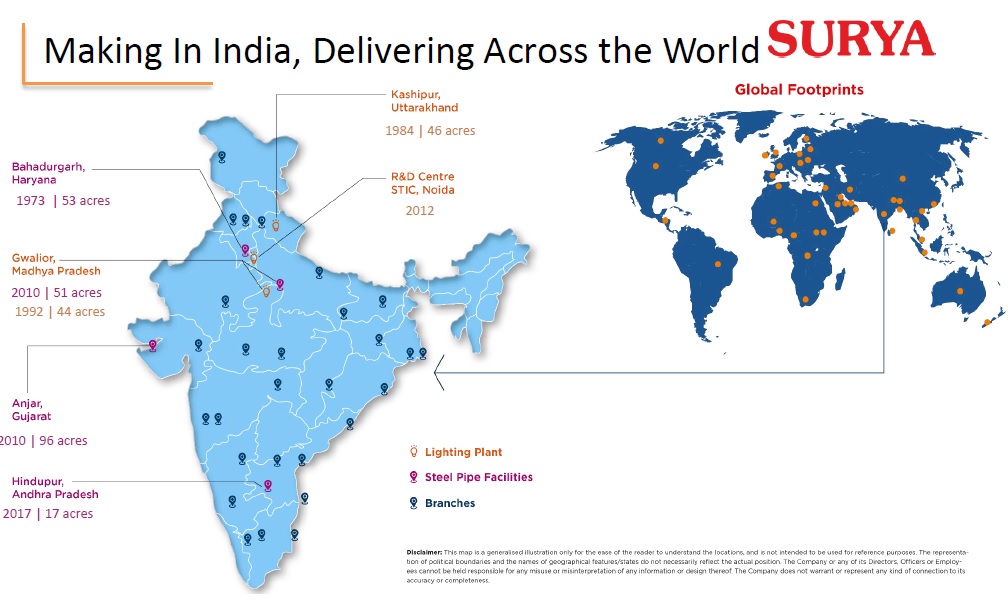

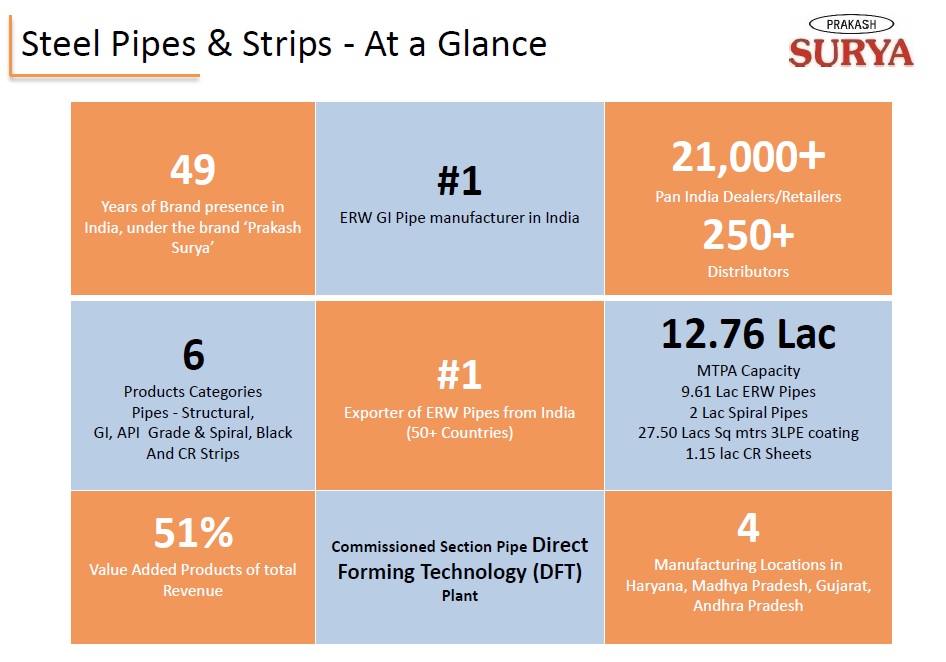

Steel biz: Co is the 2nd largest GI pipe manufacturer in India after APL & largest exporter of ERW Pipes. It has 2nd largest distributor network of 21000 Dealers in pipes (APL 50000). Surya has 4 Plants with combined capacity of 12 lac tons (APL 26 lac tons).

3/10

3/10

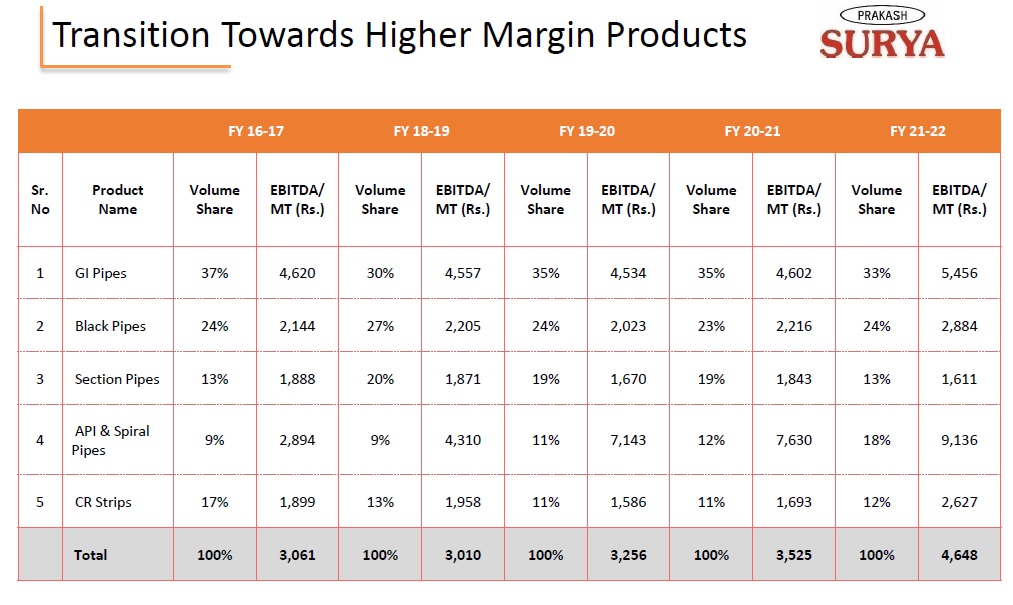

Expansion: 72ktpa capacity expansion to enable low-cost in-house production of GP & CR coil/ pipes -> increase production volumes across its ERW, black, galvanized, and pre-galvanized pipe portfolio. Large-diameter DFT products from facility commissioned at Gwalior

4/10

4/10

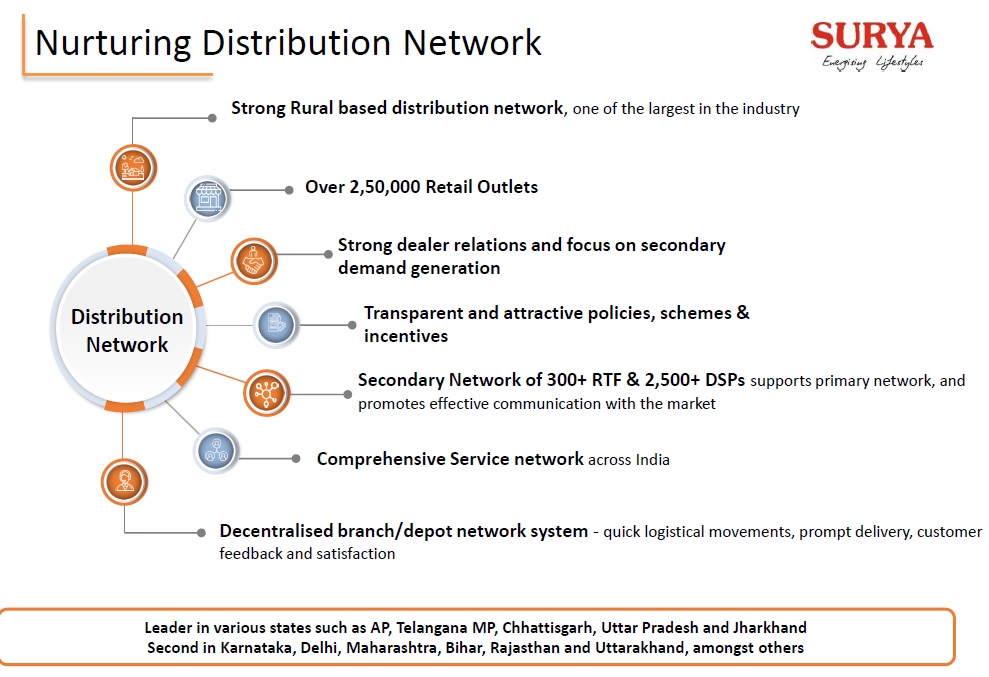

LED biz: It consists of bulbs, FMEG goods & PVC pipes. Surya is the 2nd largest player in LED bulb after Phillips, majorly targeting semi urban & rural mkts. It has a huge 2.5 lakh retail outlet base, second only to Bajaj electrical.

5/10

5/10

LED Focus: inc dealer network + product expansion -> sustainable growth, focus on brand building -> doubled A&M expenses to 30cr. Strong launch pipeline, increase presence in Tier 1 cities

6/10

6/10

Financials: Current net debt stands at 307cr & co plans to pay it off over the next 12 months. Current asset turns stands at 2.4x (vs 3.3x for APL), RoE stand at 16% (vs 22% for APL) & ROCE stands at 18% (vs 29% for APL). OB of 700cr.

7/10

7/10

Capex benefits: Well on track, 75cr capex in Steel division with high margin products. Next 2yrs no capex needed for growth. PLI capex of 25 Cr in LED, 5 Cr per year run rate, with incremental revenue target of 25 Cr per year.

8/10

8/10

Going Fwd: ERW structural pipes will pick up pace, industry CAGR of 17-20% expected. Co to grow rev at 12% but margins expansion to 10-11% from 8% will provide massive op leverage. On LED biz, co aims to take margins to 12% from 10% currently aided by 18% vol growth.

9/10

9/10

Valuations & view: While APL is in the league of legends, courtesy Sanjay Gupta; Surya is a credible name & widely respected brand/co (only brand APL talks about). We believe current valuation of 8x FY24 earnings or 5x FY24 EV/EBIDTA offers tremendous value.

10/10

10/10

Fun Fact: While APL Apollo grew Rev at 25% CAGR & PAT at 29% CAGR from FY12-22, Surya Roshni grew Rev at 10% CAGR and PAT at 15% CAGR. But Mcap for APL grew 200x vs 10x for Surya during the same FY12 to FY22 period.

Loading suggestions...