How to get 100x superb returns with low effort📈

Here is a rarely discussed strategy where you don't need to research all the new projects, or even scroll Twitter every day😵.

It takes advantage of herding behavior, and gives you a edge

Momentum Strategy!👇

Here is a rarely discussed strategy where you don't need to research all the new projects, or even scroll Twitter every day😵.

It takes advantage of herding behavior, and gives you a edge

Momentum Strategy!👇

1/

Contents:

1⃣ Background on momentum strategy

2⃣ Momentum applied to crypto

3⃣ Improvements and variants

Contents:

1⃣ Background on momentum strategy

2⃣ Momentum applied to crypto

3⃣ Improvements and variants

2/

1⃣ Background

Momentum is well-established phenomenon for stocks, first documented by Jeegadesh and Titman in their seminal papers.

The principle is simple: best past performers will be best future performers.

1⃣ Background

Momentum is well-established phenomenon for stocks, first documented by Jeegadesh and Titman in their seminal papers.

The principle is simple: best past performers will be best future performers.

3/

In behavioral finance, momentum is explained as a result of a cognitive bias called herding behavior.

Herding behavior occurs when individuals make investment decisions based on the actions of others, rather than on their own independent analysis and evaluation.

In behavioral finance, momentum is explained as a result of a cognitive bias called herding behavior.

Herding behavior occurs when individuals make investment decisions based on the actions of others, rather than on their own independent analysis and evaluation.

4/

When a stock has shown strong returns, investors tend to pile into the stock, driving up its price even further.

This creates a positive feedback loop, as more investors are drawn to the stock because of its recent performance.

When a stock has shown strong returns, investors tend to pile into the stock, driving up its price even further.

This creates a positive feedback loop, as more investors are drawn to the stock because of its recent performance.

5/

This, in turn, leads to further price appreciation, which attracts even more investors.

Sounds familiar, degens?!

This, in turn, leads to further price appreciation, which attracts even more investors.

Sounds familiar, degens?!

6/

Momentum for stocks can be easily translate into a systematic strategy.

The rules are:

🔹Select a universe of tradable stocks, for example SP500 stocks

🔹Rank the stocks by 12 months performance

🔹Invest 1/10 of your portfolio in each of the top 10 stocks

🔹Repeat each month

Momentum for stocks can be easily translate into a systematic strategy.

The rules are:

🔹Select a universe of tradable stocks, for example SP500 stocks

🔹Rank the stocks by 12 months performance

🔹Invest 1/10 of your portfolio in each of the top 10 stocks

🔹Repeat each month

7/

To be precise, performance is measured as return of a stock, calculated as P/P365 - 1 where:

🔹P is last close price

🔹P365 is price close 365 days ago

To be precise, performance is measured as return of a stock, calculated as P/P365 - 1 where:

🔹P is last close price

🔹P365 is price close 365 days ago

8/

12 month is called the “formation period” (denoted by J) and 1 month is called “holding period” (denoted by K).

These are parameters that can be changed. 12 and 1 are just the “traditional parameters” that worked well in the past for stocks.

12 month is called the “formation period” (denoted by J) and 1 month is called “holding period” (denoted by K).

These are parameters that can be changed. 12 and 1 are just the “traditional parameters” that worked well in the past for stocks.

9/

Basically the strategy buys past winners (in terms of performance), hold them for a month, and then repeats the process.

You can see that this is something that can be easily implemented in a spreadsheet and requires just an hour per month!

Basically the strategy buys past winners (in terms of performance), hold them for a month, and then repeats the process.

You can see that this is something that can be easily implemented in a spreadsheet and requires just an hour per month!

9/

2⃣ Momentum for cryptos

But now the question is: does moment work for cryptos?

Yes and no…

2⃣ Momentum for cryptos

But now the question is: does moment work for cryptos?

Yes and no…

10/

What could possibly go wrong with the strategy?

A couple of things:

🔹 12 month formation period is too long. Many tokens rise and fall within few months.

🔹 1 month holding period is too long too. You won’t capitalize enough with such high timeframe.

What could possibly go wrong with the strategy?

A couple of things:

🔹 12 month formation period is too long. Many tokens rise and fall within few months.

🔹 1 month holding period is too long too. You won’t capitalize enough with such high timeframe.

11/

Panagiotis Tzouvanasa, Renatas Kizys, and Bayasgalan Tsend-Ayushb performed some simulations for cryptocurrency momentum using smaller values for J and K.

eprints.soton.ac.uk

Panagiotis Tzouvanasa, Renatas Kizys, and Bayasgalan Tsend-Ayushb performed some simulations for cryptocurrency momentum using smaller values for J and K.

eprints.soton.ac.uk

12/

They selected cryptocurrencies with at least $100 millions market cap and three years historical data.

They then used this sets of parameters for “formation period” J and “holding period” K:

🔹J=7,15,30

🔹K=7,15,30

🔹Top 6 vs 3 performers

They selected cryptocurrencies with at least $100 millions market cap and three years historical data.

They then used this sets of parameters for “formation period” J and “holding period” K:

🔹J=7,15,30

🔹K=7,15,30

🔹Top 6 vs 3 performers

13/

The exact rules of the strategy are:

🔹Select the coins with at least $100 millions market cap

🔹Rank them according to the performance of the last J days performance

🔹Buy the top 6 or 3 top performers allocating the same caputal to each

🔹Repeat the process every K days

The exact rules of the strategy are:

🔹Select the coins with at least $100 millions market cap

🔹Rank them according to the performance of the last J days performance

🔹Buy the top 6 or 3 top performers allocating the same caputal to each

🔹Repeat the process every K days

14/

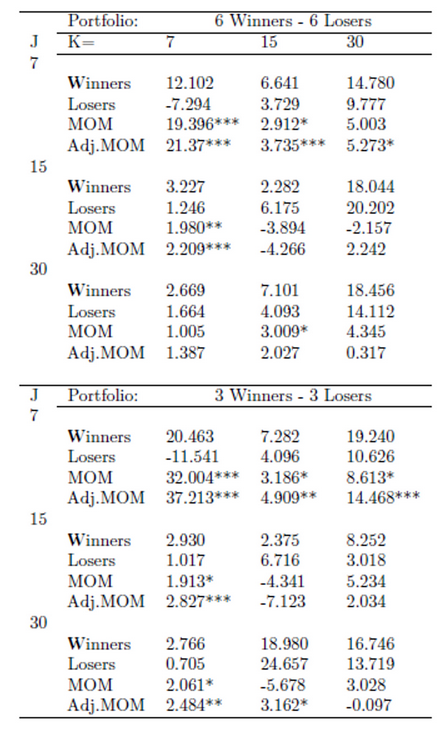

The table below shows weekly returns for the strategies corresponding to the above parameters.

The momentum strategy that I am discussing here corresponds to the “Winners” row.

The table below shows weekly returns for the strategies corresponding to the above parameters.

The momentum strategy that I am discussing here corresponds to the “Winners” row.

15/

The best performing strategy has parameter J=K=7 and buys the top 3 performance tokens.

It returns 20% per week on average.

If you do the math, compounding 20% per week seems that $1 dollar invested would turn into $13,104 ($13 thousands!) at the end of the year…

The best performing strategy has parameter J=K=7 and buys the top 3 performance tokens.

It returns 20% per week on average.

If you do the math, compounding 20% per week seems that $1 dollar invested would turn into $13,104 ($13 thousands!) at the end of the year…

16/

Should we really expect this number?

I don’t think so for two reasons…

🔹In every backtest there is some overfitting (live results will be lower than historical ones).

🔹Volatility and performance of tokens will inevitably reduce over time, as the market grows and matures.

Should we really expect this number?

I don’t think so for two reasons…

🔹In every backtest there is some overfitting (live results will be lower than historical ones).

🔹Volatility and performance of tokens will inevitably reduce over time, as the market grows and matures.

17/

As a rule of thumb, I think it is quite reasonable to cut simulation results by 30% to account for overfitting.

And I would cut another 30% to account for future reduced volatility and performance.

As a rule of thumb, I think it is quite reasonable to cut simulation results by 30% to account for overfitting.

And I would cut another 30% to account for future reduced volatility and performance.

18/

In the end, a 10% per week is a more reasonable estimation… that means an astonishing 140x on your capital in year!!!

In the end, a 10% per week is a more reasonable estimation… that means an astonishing 140x on your capital in year!!!

19/

3⃣ Variations

The paper also discusses two variations: long-short momentum and volatility-adjusted momentum.

Long-short momentum is similar to the original one discussed above, but it also short sells the worst performers (the “losers”).

3⃣ Variations

The paper also discusses two variations: long-short momentum and volatility-adjusted momentum.

Long-short momentum is similar to the original one discussed above, but it also short sells the worst performers (the “losers”).

20/

Results for long-short are good (look at “MOM” row in the table in 13/) I don’t think it is a viable option as not all tokens can be shorted.

Also, short selling has the risk of liquidation and it is not clear whether the authors of the paper took liquidations into account.

Results for long-short are good (look at “MOM” row in the table in 13/) I don’t think it is a viable option as not all tokens can be shorted.

Also, short selling has the risk of liquidation and it is not clear whether the authors of the paper took liquidations into account.

21/

Volatility-adjusted momentum is more interesting.

The idea is to target a specify volatility value for the portfolio.

Let’s call this target value “target_vol”, while “vol” is the volatility of the momentum strategy.

Volatility-adjusted momentum is more interesting.

The idea is to target a specify volatility value for the portfolio.

Let’s call this target value “target_vol”, while “vol” is the volatility of the momentum strategy.

22/

The capital invested at every portfolio rebalancing will be (current portfolio value) * min(1, (target_vol/vol)).

When the volatility of the portfolio will be higher than our target, we will invest less, to reduce risk.

The capital invested at every portfolio rebalancing will be (current portfolio value) * min(1, (target_vol/vol)).

When the volatility of the portfolio will be higher than our target, we will invest less, to reduce risk.

23/

Otherwise, when volatility is below our target, we will 100% of our capital.

That’s why the multiplier in the formula is capped at 1 ( min(1, (target_vol/vol)), this way we avois leverage.

Otherwise, when volatility is below our target, we will 100% of our capital.

That’s why the multiplier in the formula is capped at 1 ( min(1, (target_vol/vol)), this way we avois leverage.

24/

Unfortunately, results in the paper (Adj. MOM row in the table) are calculated only for the volatility adjusted long-short strategy.

Unfortunately, results in the paper (Adj. MOM row in the table) are calculated only for the volatility adjusted long-short strategy.

25/

Summarizing, long-only momentum strategy is a simple systematic strategy that can be implemented by everyone.

During a bull market we can expect this strategy to 100x the capital invested…

NFA, do your research!

Summarizing, long-only momentum strategy is a simple systematic strategy that can be implemented by everyone.

During a bull market we can expect this strategy to 100x the capital invested…

NFA, do your research!

26/

This thread is part of a series about investing, trading and alpha generation.

You missed my previous thread, check them out!

This thread is part of a series about investing, trading and alpha generation.

You missed my previous thread, check them out!

27/

Stimulated by the comments, I wrote a new thread discussing possible improvements of the strategy.

Thanks to all!

Thanks to all!

Loading suggestions...