My fifth data update for 2023 looks at profitability, a business quality that seemed to have lost its resonance in a decade that gave top billing to growth and user numbers, but was rediscovered again, perhaps temporarily, during 2022. bit.ly

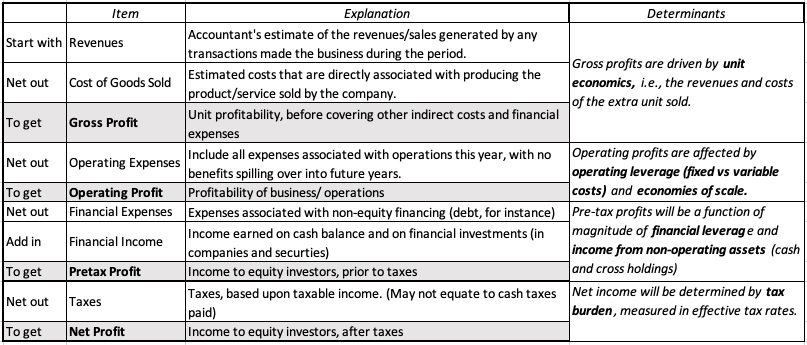

To set the table, I start by laying out the different measures of profit that we encounter in income statement, and the business economics that drive the magnitude with each. My apologies if you find it too basic and simplistic. bit.ly

At the risk of stating the obvious, it is much easier to be monwy with gross income, but money losing becomes more common as you go down the income statement, one reason that people abandon PE ratios for EV to EBITDA. bit.ly

Even for companies that are money making, the drop in profitability as you go from gross to operating to net income should make you suspicious of any company that flaunts it gross margin numbers. bit.ly

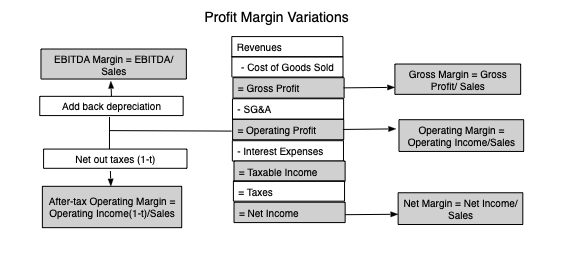

Scaling profits to revenues yields margins, and in addition to gross, operating and net margins, you can also add on EBITDA and after-tax operating margins. There is too much loose talk around margins. bit.ly

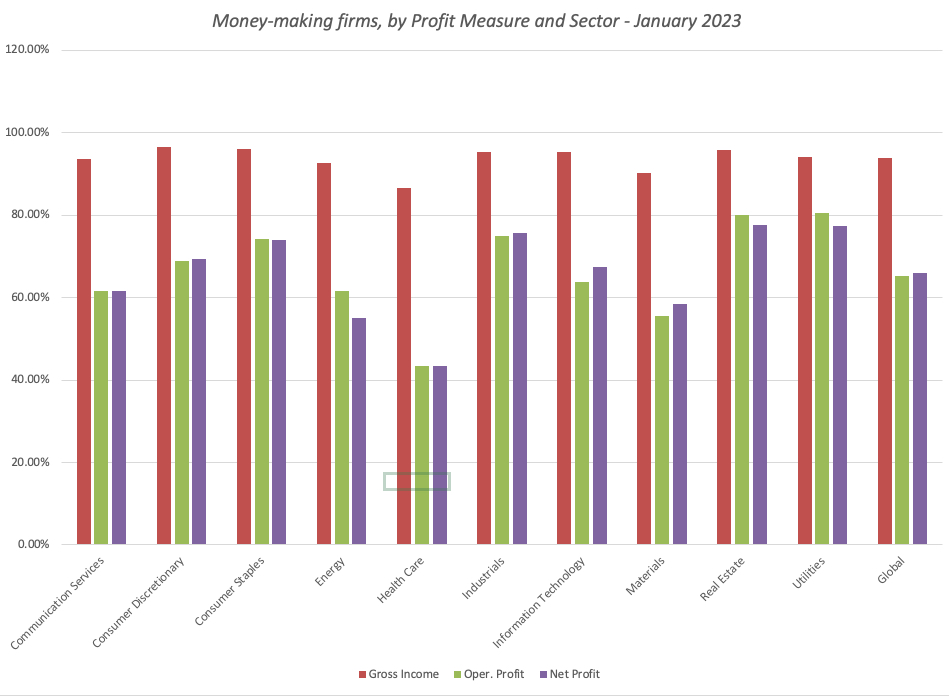

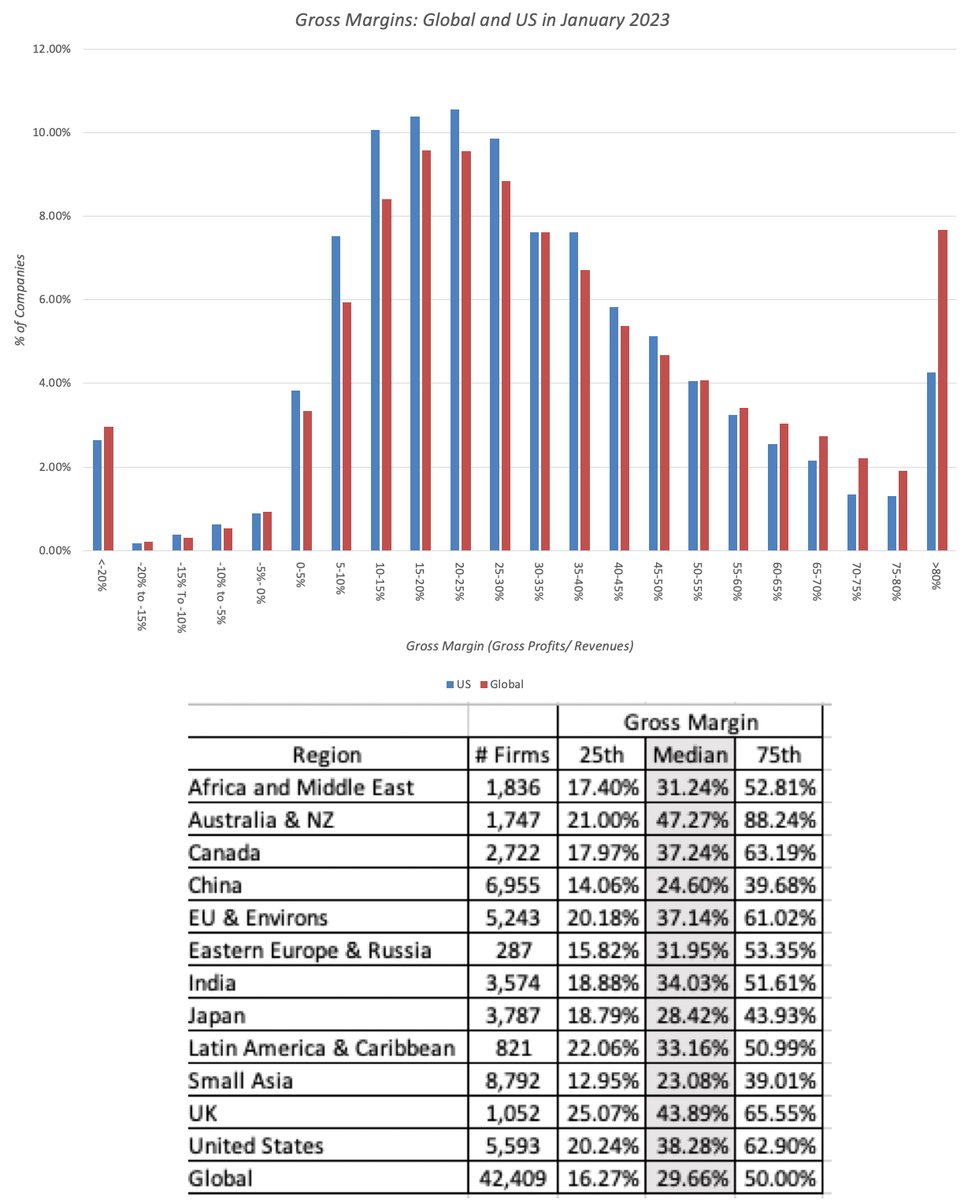

The distribution of gross margins across all non-financial, publicly-traded firms in the world yields a median value of 30% across all global firms, but differences across regions that can be attributed to different business mixes. bit.ly

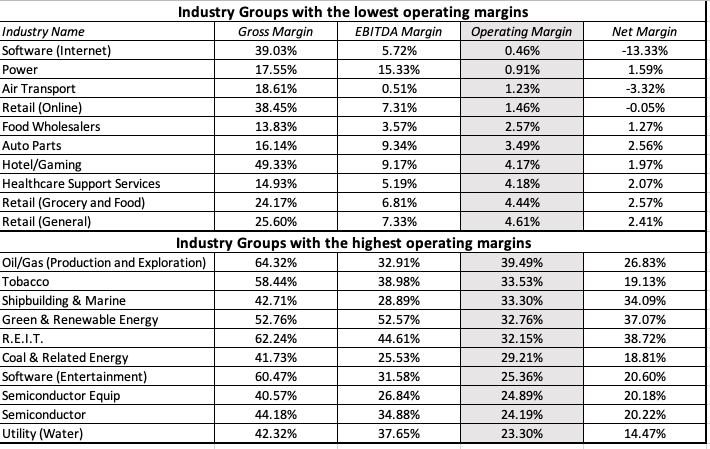

Looking at differences in margins across industry groupings, there are clear delineations between high and low margin industry groups, with business economics explaining divergences. bit.ly

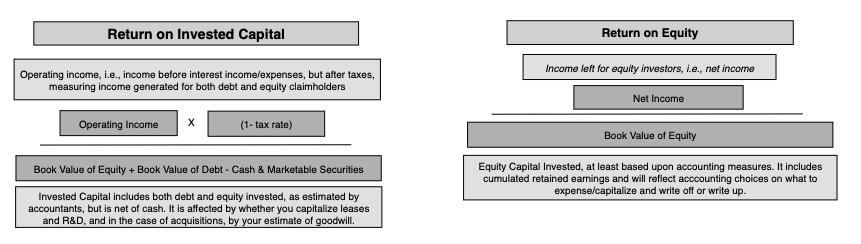

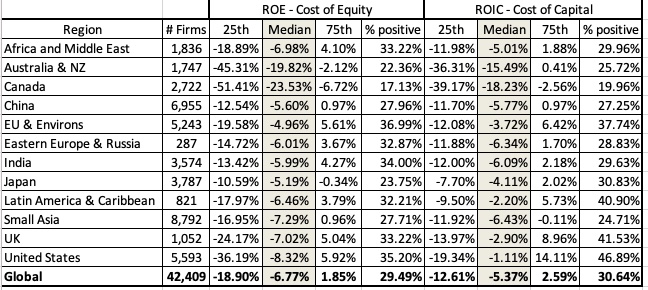

Scaling profits to invested capital generates accounting returns, either to equity investors (as a return on equity) or to all capital providers (as a return on invested capital). bit.ly

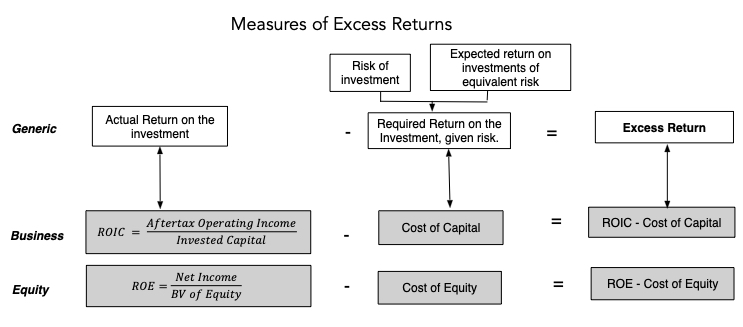

Comparing those returns on equity and capital to costs of equity and capital converts them into excess returns, and in the long term, for a business to create value, these excess returns have to be positive: bit.ly

Most global businesses struggled to generate positive excess returns in 2022, with 70% of all firms earning less than the cost of capital. For some, it was growing pains, for some, bad luck or a bad year, but for some, it was business turning bad. bit.ly

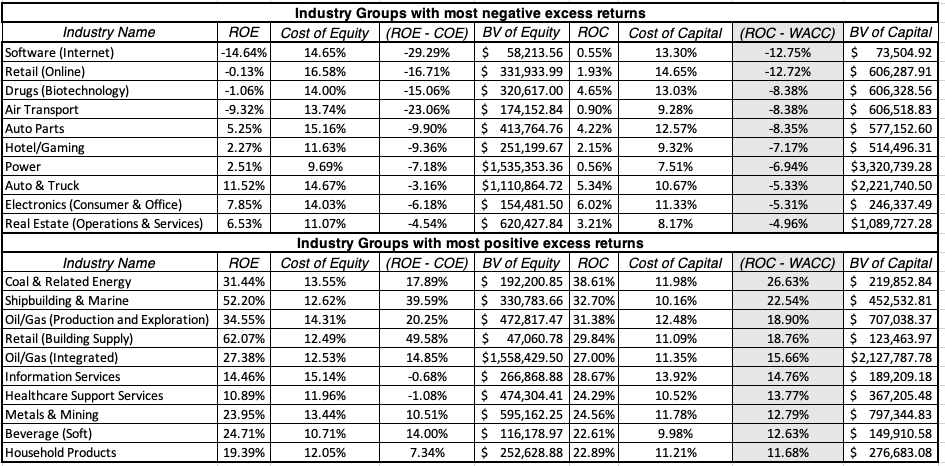

Within the market, though, there are sectors that deliver returns that exceed costs by a wide margin, just as there are sectors that are scrape the bottom of the barrel. bit.ly

The surge in cost of capital in 2022 made winning the value game more difficult for all companies. Investment regret is part of business, but hoping that costs of capital will revert back to 2021 levels is not a sensible strategy. bit.ly

Loading suggestions...