Kalpataru power transmission limited conducted their Q3 FY23 conference call on 9th February 2023.

“Target to generate 3 billion dollar revenue and have an ROCE of above 22% by FY 25”

Here are the key takeaways…

“Target to generate 3 billion dollar revenue and have an ROCE of above 22% by FY 25”

Here are the key takeaways…

Overview

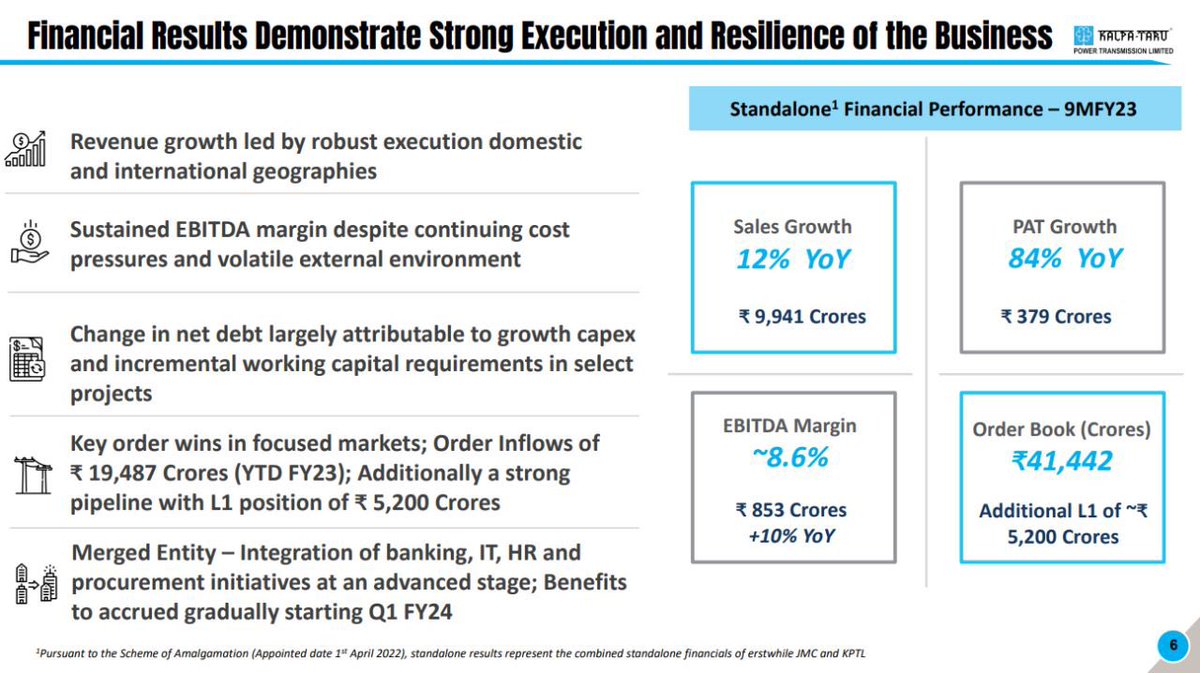

- Company has delivered strong growth during this period.

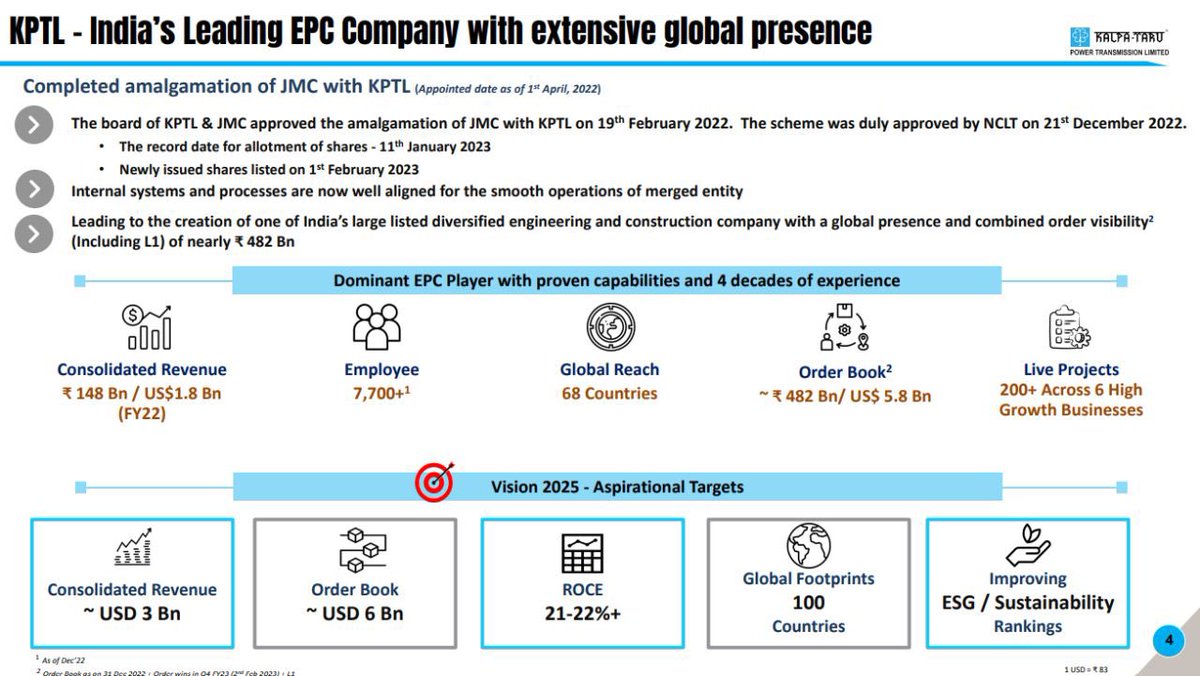

- With the completion of its merger the company has turned out to be the largest listed and diversified engineering and construction company.

- Company has delivered strong growth during this period.

- With the completion of its merger the company has turned out to be the largest listed and diversified engineering and construction company.

- Now the company aims to bring up an amalgamation of banking and various other industries to leverage their current position in best way possible.

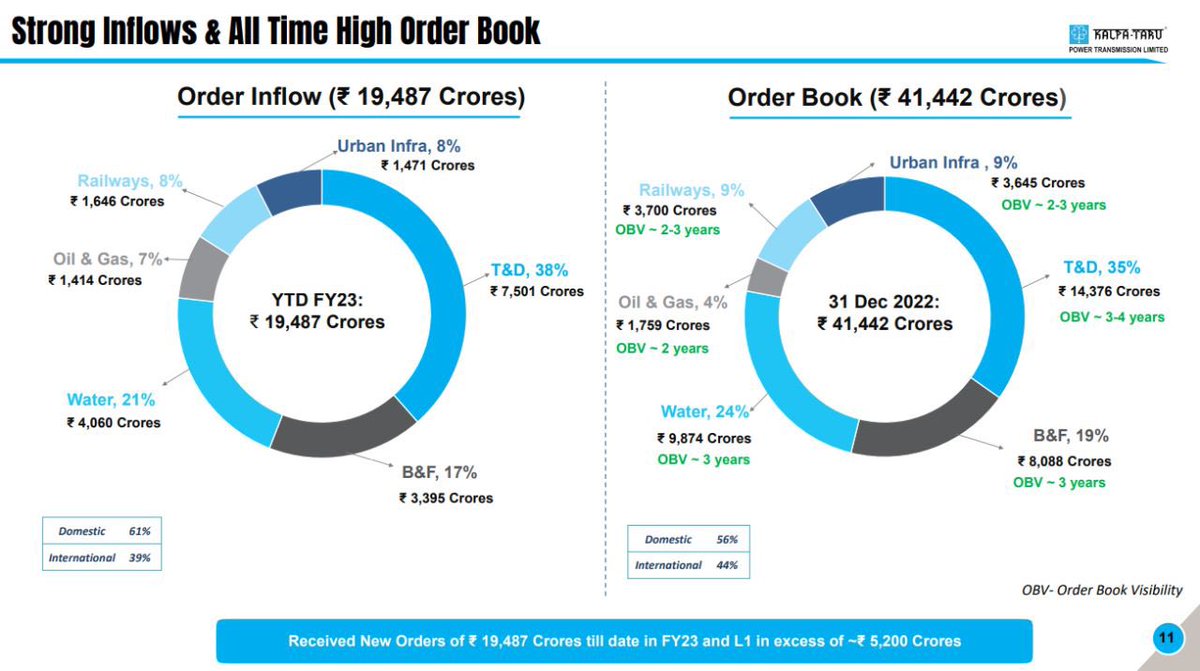

- In T&D business, with new order growth coming up they expect to beat past records sooner.

- In T&D business, with new order growth coming up they expect to beat past records sooner.

- With the new budget they expect to do more in the railways segment and on T&D though the growth was declined an upshift of 10-15% can be seen easily.

- In B&F business, the company grew 30% due to robust execution and healthy order book.

- This trend is expected to be continued, and same things goes for their Water business.

- They currently have 30 water businesses and expect further break through in this segment.

- This trend is expected to be continued, and same things goes for their Water business.

- They currently have 30 water businesses and expect further break through in this segment.

- For oil and gas business, they are now capable to participate in 6-7 countries making their international portfolio stronger then ever.

- For the railways though there has been a decline in their growth they tend to close old projects and soon try to grab new markets.

- For the railways though there has been a decline in their growth they tend to close old projects and soon try to grab new markets.

- In unban infra space, even though they have less proportion they generated highest revenue of 41% growth during this period due to improved execution of new projects in global market.

Financials

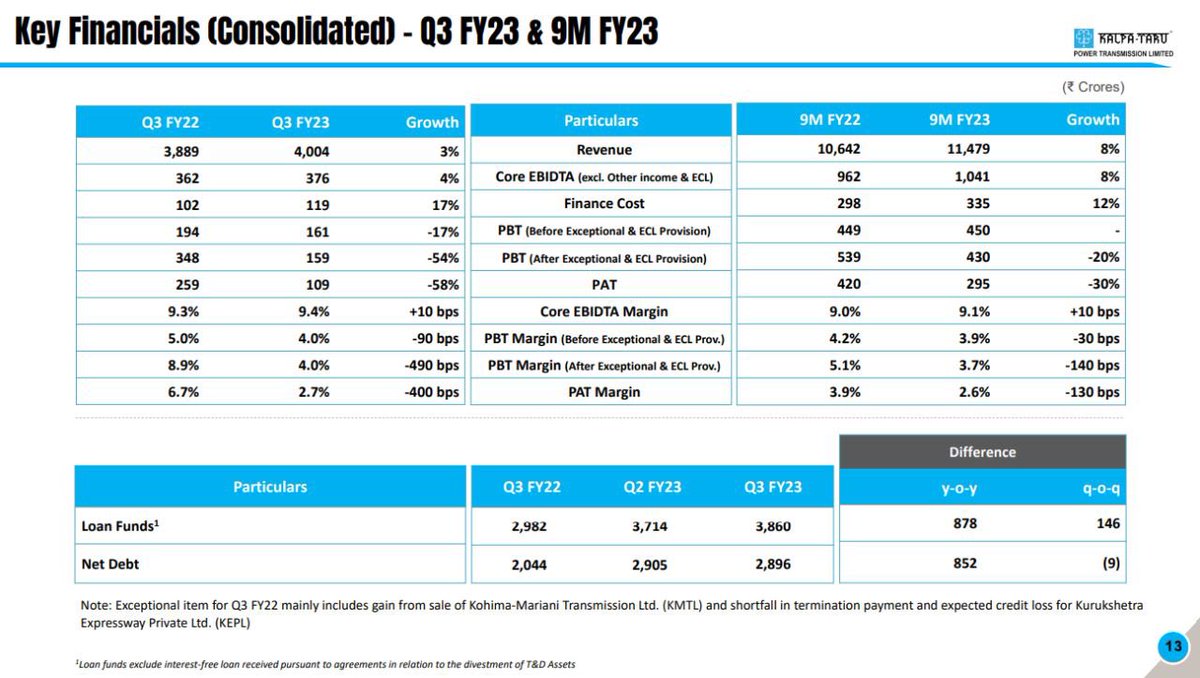

- During the period, revenue grew by 3% and 8% for 9 month period.

- This growth was possible due to reduction in their backlog in T&D business and lower warehouse utilisation.

- Their EBITDA stood around 9.4% and 9.1% levels.

- Their Pat margins stood around 2.7%.

- During the period, revenue grew by 3% and 8% for 9 month period.

- This growth was possible due to reduction in their backlog in T&D business and lower warehouse utilisation.

- Their EBITDA stood around 9.4% and 9.1% levels.

- Their Pat margins stood around 2.7%.

- Across the borders, their Sweden and Brazil business generated revenues of 280 crores and 95 crores respectively.

- Strong order book and effective management have helped the overall business.

- Due to merger, some revenues were not booked in the month of December.

- Strong order book and effective management have helped the overall business.

- Due to merger, some revenues were not booked in the month of December.

- The companies net debt stands around 2053 crores, this is been due to increase in incremental working capital and upcoming Capex opportunities.

- This levels are expected to be same for 23 and post that decline will be visible.

- This levels are expected to be same for 23 and post that decline will be visible.

- The company doesn’t expect to hire new contractors on domestic projects but for international business and water projects new teams are been expected to be created to cater jobs more efficiently.

- On receiving payments prior they use to face a bit issue in railway segment but now the things are sorted and processed in a very easily way.

- On domestic front, they are more adamant towards Gujarat and Rajasthan area for growth.

- On domestic front, they are more adamant towards Gujarat and Rajasthan area for growth.

- On margins, for standalone basis they haven’t changed any guidelines but on consolidated basis they have made a shifted towards lower levels.

Merger and other investments

- The merger with JMC limited was completed during the month of January 23 and new shares are been issued since 1st feb 23.

- They did take part in construction of Mauritius airport and are in the final stage of restructuring WEPL.

- The merger with JMC limited was completed during the month of January 23 and new shares are been issued since 1st feb 23.

- They did take part in construction of Mauritius airport and are in the final stage of restructuring WEPL.

- The company will start availing the benefits from Q1 FY 24. The benefits will be upwards on 100 crores on interest and principle benefit.

- On international markets with merger they plan to see a good bump up in their projects plans.

- On international markets with merger they plan to see a good bump up in their projects plans.

- For company they have set a simple rule wherein they will deploy more time to those segments where international business can be utilised in big opportunities.

- For last 9 months their Capex was approx of 500 crores and yet many are yet to be capitalised.

- For last 9 months their Capex was approx of 500 crores and yet many are yet to be capitalised.

- On their Ladakh projects they are facing a bit hiccup for tender orders but as things will get solved the company will update.

Loading suggestions...