The European growth model will be under severe pressure over the next decade.

A thread.

1/

A thread.

1/

Between 2000-2020, Europe delivered an average +1.5% real GDP growth per year

That's pretty decent, considering:

- These 20 years include the GFC and the debt crisis;

- The inherent fragility of the European architecture (one monetary policy, 19 different fiscal policies)

2/

That's pretty decent, considering:

- These 20 years include the GFC and the debt crisis;

- The inherent fragility of the European architecture (one monetary policy, 19 different fiscal policies)

2/

The European growth model did okay for 2 decades necause its two sources of leverage were hardly under any pressure.

Europe's growth model is based on:

- Cheap economic leverage (energy, labor, supply chains)

- Cheap financial leverage (low rates)

The pressure is now on!

3/

Europe's growth model is based on:

- Cheap economic leverage (energy, labor, supply chains)

- Cheap financial leverage (low rates)

The pressure is now on!

3/

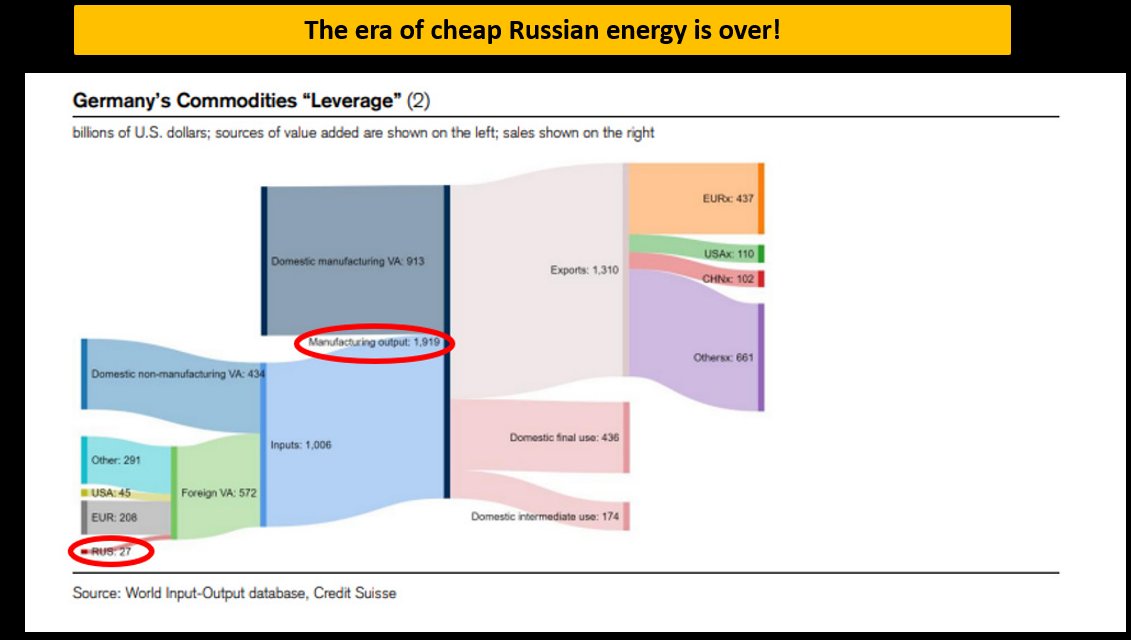

Take Germany

$2 trillion of manufacturing output built on cheap and readily available energy (e.g. Russian gas)

This export-oriented model was also based on outsourcing labor and production

That means relying on just-in-time supply chains and foreign labor

The pandemic...

4/

$2 trillion of manufacturing output built on cheap and readily available energy (e.g. Russian gas)

This export-oriented model was also based on outsourcing labor and production

That means relying on just-in-time supply chains and foreign labor

The pandemic...

4/

...challenged this model on many fronts

Cheap energy is not readily available anymore - there are alternatives, but they are more expensive to source or build voer time

Supply chains were broken, and CEOs are exploring in-sourcing some production - possible, but expensive

5/

Cheap energy is not readily available anymore - there are alternatives, but they are more expensive to source or build voer time

Supply chains were broken, and CEOs are exploring in-sourcing some production - possible, but expensive

5/

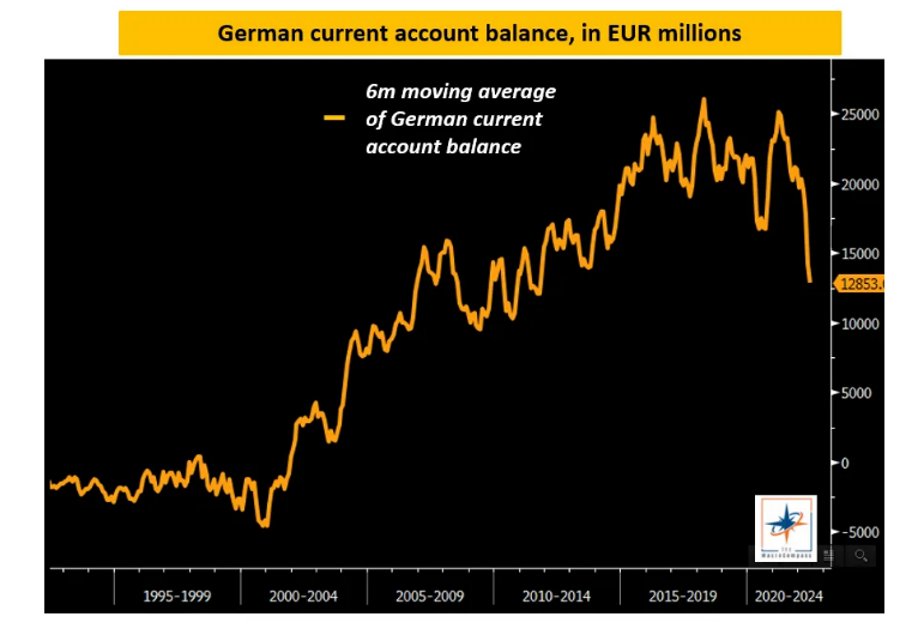

However you look at it, ''economic leverage'' based on cheap and readily available energy, labor and suppl chains is seriously challenged.

That's already visible in some of the current account balance statistics.

Long-term, this growth model seems under pressure.

6/

That's already visible in some of the current account balance statistics.

Long-term, this growth model seems under pressure.

6/

Remember, cheap economic leverage was the first pillar of the European 2000-2020 growth model.

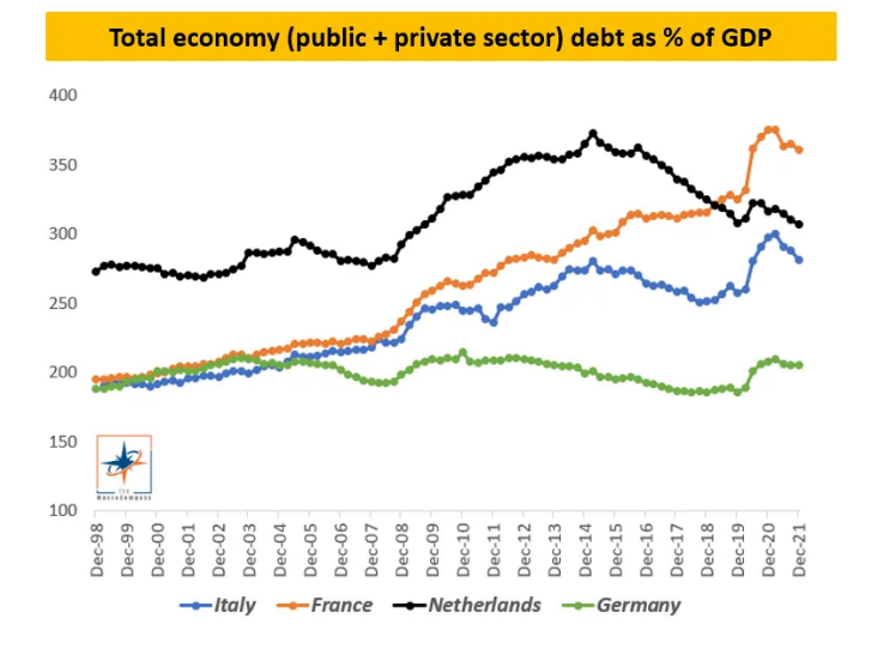

The second source of growth came from cheap financial leverage.

Summing up public and private debt/GDP, most European economies leveraged up to 250-300% of GDP.

And...

7/

The second source of growth came from cheap financial leverage.

Summing up public and private debt/GDP, most European economies leveraged up to 250-300% of GDP.

And...

7/

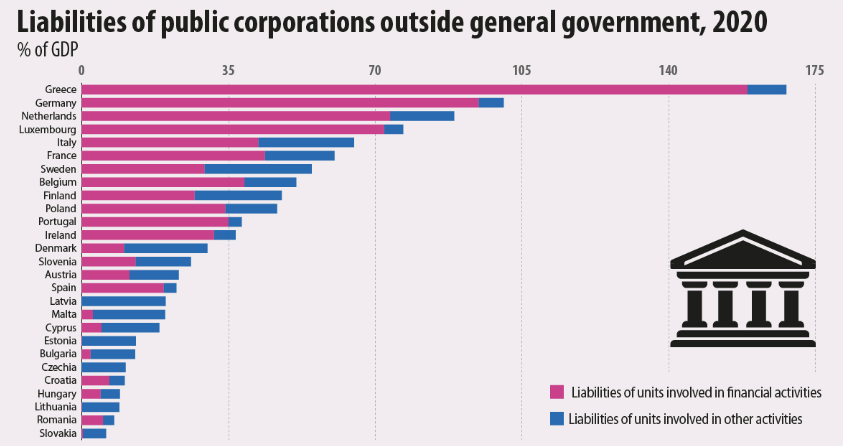

..before you say Germany doesn't have much debt, remember to sum up the one hidden by accounting tricks

The debt of many public corporations is not counted in official debt statistics, and some Northern European countries are making large use of it

Everyone in the same boat

8/

The debt of many public corporations is not counted in official debt statistics, and some Northern European countries are making large use of it

Everyone in the same boat

8/

Access to more and more credit boosted cyclical economic growth in Europe for years.

Obviously, for this pattern to continue debt needs to be ''affordable''.

But rates in Europe were zero or negative for a long period, and credit spreads very tight also due to QE.

9/

Obviously, for this pattern to continue debt needs to be ''affordable''.

But rates in Europe were zero or negative for a long period, and credit spreads very tight also due to QE.

9/

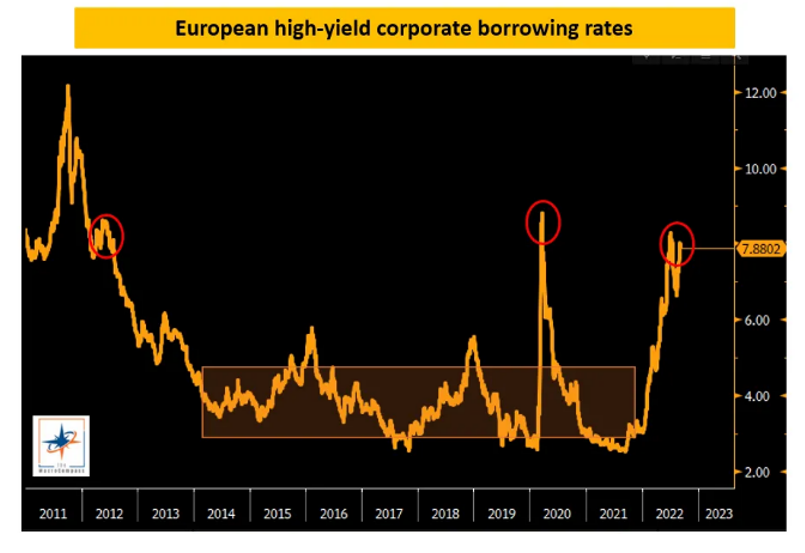

Zombie companies could borrow money for 5 years paying only 3-4% rates (!) between 2014 and 2021

When debt is so cheap, most business models can survive

But recently inflation has soared and the ECB has been forced to hike rates

Cheap financial leverage is no longer cheap

10/

When debt is so cheap, most business models can survive

But recently inflation has soared and the ECB has been forced to hike rates

Cheap financial leverage is no longer cheap

10/

Much higher borrowing rates matter not only for the corporate sector, but also for the housing market.

Many have forgotten this, but the housing market can get very frothy in Europe too.

Spanish house prices 1996-2007: +300% (!).

And as a result of the ECB actions...

11/

Many have forgotten this, but the housing market can get very frothy in Europe too.

Spanish house prices 1996-2007: +300% (!).

And as a result of the ECB actions...

11/

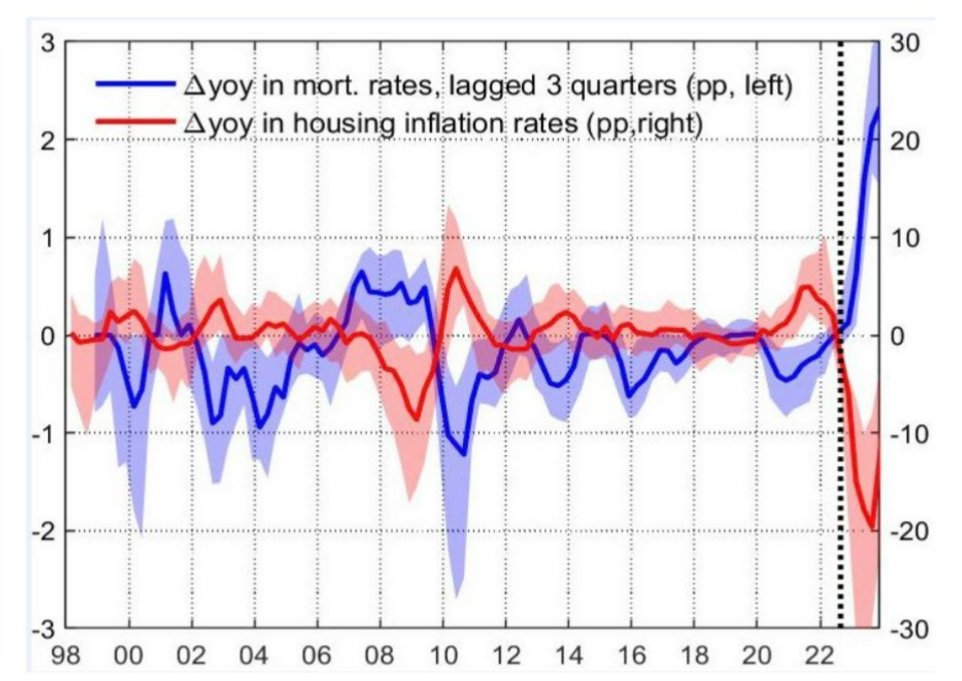

...20 and 30-year mortgage rates in Europe have spiked from 1.5% to 4.5% or so in a few quarters.

When mortgage rates move by 200-300 bps this quickly (blue, LHS) house prices drop by roughly 20% (red, RHS) with a 3-4 quarters lag.

This matters for Europe...

12/

When mortgage rates move by 200-300 bps this quickly (blue, LHS) house prices drop by roughly 20% (red, RHS) with a 3-4 quarters lag.

This matters for Europe...

12/

...because much of the ''wealth effect'' behind its growth model sits in the housing market and it could soon be shaken out.

In short, cheap financial leverage which allowed for large credit creation at a public and private level is not cheap anymore.

So, what happens...

13/

In short, cheap financial leverage which allowed for large credit creation at a public and private level is not cheap anymore.

So, what happens...

13/

...when your growth model is based on two sources of cheap leverage (economic and financial) and both get challenged at the same time?

Short-term, Europe can become creative and muddle through.

Long-term, it's much more tricky.

14/

Short-term, Europe can become creative and muddle through.

Long-term, it's much more tricky.

14/

If you enjoyed this thread and would like more macro insights and educational content, consider joining 130,000+ investors and subscribing to my free newsletter

👇

TheMacroCompass.substack.com

I wish you a lovely weekend!

15/15

👇

TheMacroCompass.substack.com

I wish you a lovely weekend!

15/15

Loading suggestions...