1/ With the recent electricity tariff increase, it seems likely the CEB's cashflow is now at least neutral. Wrote a piece about this, why it was likely unavoidable, and what financial challenges remain.

Following is a quick summary of key points

macrocolombo.substack.com

Following is a quick summary of key points

macrocolombo.substack.com

2/ Disclaimer - The numbers given are quite approximate, and not meant to be taken as exact figures. Also my personal views as usual.

I'm also intentionally leaving out the distributive impacts of this, will handle that in a separate piece later this week.

I'm also intentionally leaving out the distributive impacts of this, will handle that in a separate piece later this week.

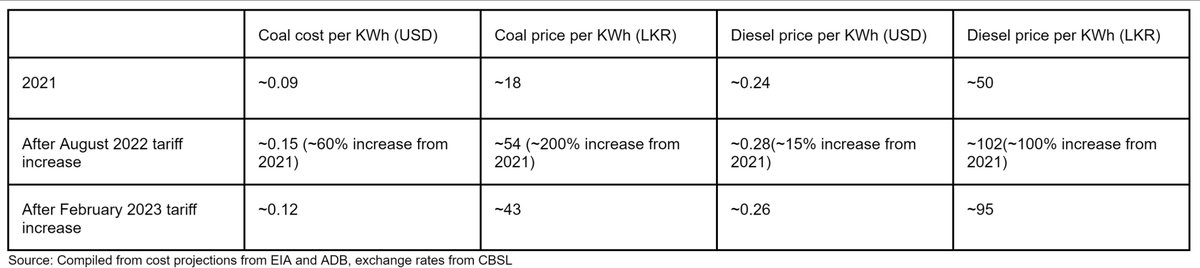

3/ The main message is this - CEB's generation costs rose massive from end-2021, as global energy prices shot up and the rupee value of this rose even more due to depreciation.

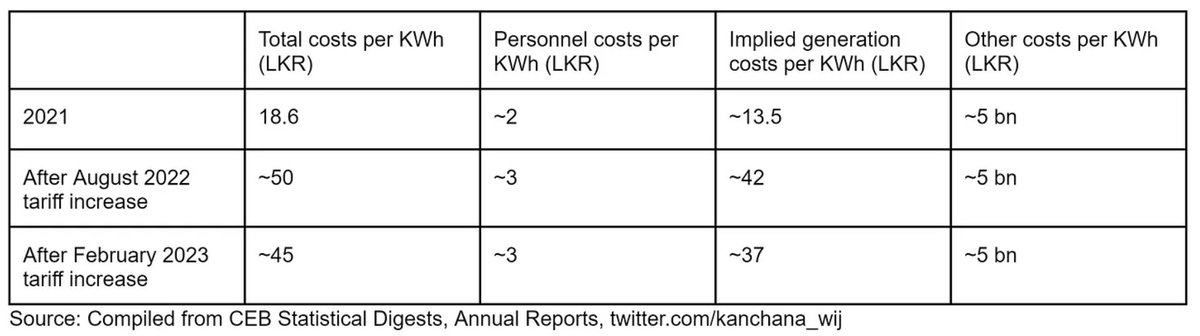

4/ Yes, there are very high personnel and administrative costs as well - in the past, these would have also accumulated for varied reasons include corruption.

But in the new context, these are only a smaller proportion of the costs. Generation costs are the bulk.

But in the new context, these are only a smaller proportion of the costs. Generation costs are the bulk.

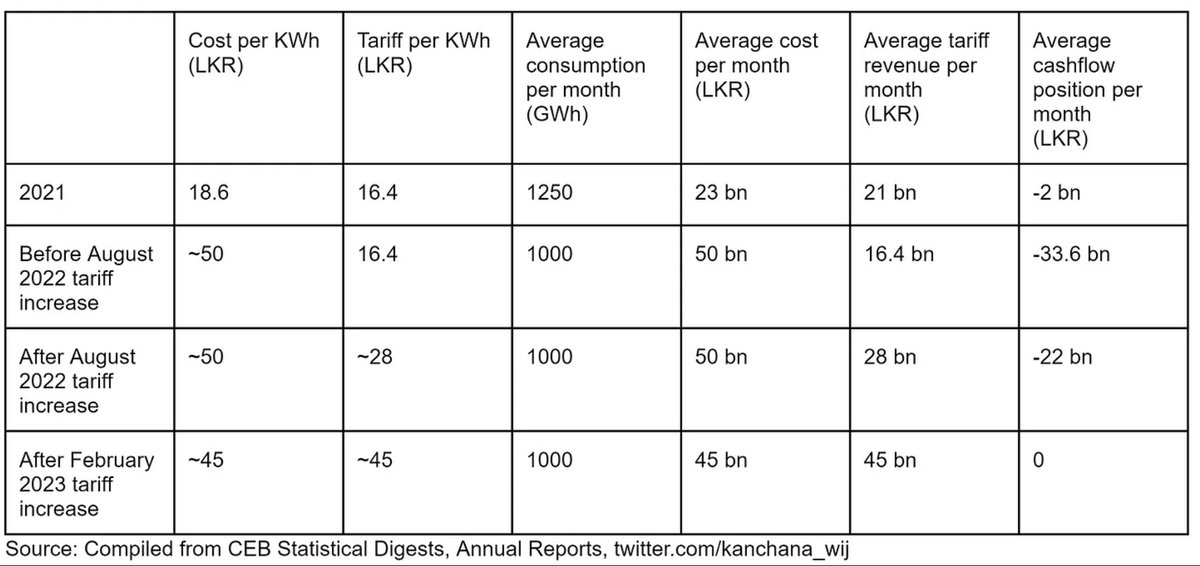

5/ The reality is that the CEB was likely heavily negative in its cashflow before the two tariff hikes. The August hike wasn't enough to account for the very large increase in costs in essence, but now, things are probably okay.

6/ In practice, this negative cashflow would have been bunched up in certain months (eg-around 100bn LKR needed for coal shipments in 1Q23).

The new tariff structure allows CEB to access credit to meet these payments (borrow LKR to buy USD, use the USD to pay for coal/fuel).

The new tariff structure allows CEB to access credit to meet these payments (borrow LKR to buy USD, use the USD to pay for coal/fuel).

7/ But that's just the current costs and the current cashflow. What about all the "losses" and mismanagement of the past?

All that is reflected in the debt burden of the CEB - likely around 900 bn LKR (around 3% of GDP!).

All that is reflected in the debt burden of the CEB - likely around 900 bn LKR (around 3% of GDP!).

8/ Most of this debt would be to the state banks - and the fact that this debt was always going to be difficult to pay back is now also a credit risk. Dealing with this (support from multilaterals) will also mean less space for multilaterals to finance the rest of the economy.

9/ Accountability for decisions that led to such a terrible situation needs to happen. I don't know how or whether it will. We can and must push for it in any case. I'm hoping that data like this can help towards such an end.

10/ But these 2 facts - the heavily negative cashflow and the insane debt burden probably explains why restructuring the CEB has been so slow.

If we take restructuring to mean privatization, would you buy an organization with such terrible financials?

If we take restructuring to mean privatization, would you buy an organization with such terrible financials?

11/ Now that the cashflow is dealt with, it's likely that some part of the restructuring process can move ahead. But the debt issue still remains.

How can we deal with this?

How can we deal with this?

12/ Reducing the cost of generation will be critical - but in the current financial context of the CEB, where would the money come from?

One possibility is some blended finance (multilateral+private sector) coordinated with the ADB.

One possibility is some blended finance (multilateral+private sector) coordinated with the ADB.

13/ Along with that, ringfencing the current debt will also help move ahead with the process of restructuring, ensuring that the impact of old debt doesn't overly restrict investment into the future.

14/ What these 2 points would mean, is that the government could move the debt to a specific entity and deal with it separately. Along with that, the actual energy investment could happen in a more directed and more transparent way.

15/ If not for the tariff increases, close to 1% of GDP of debt burden would have been added every year. It really shows how much of our current crisis actually is related to these energy subsidies (also remember, the knockon effect of higher consumption on imports)

16/ I have a strong view that the terribly handled financials of our energy sector is a critical part of our current crisis and the country's corruption story too. What else would you call it when state banks are forced to give nearly a TRILLION RUPEES to keep the CEB afloat?

17/ Fixing the CEB in particular (as well as the CPC, but that's another story) is essential to come out the crisis. It's a critical part of handling corruption in Sri Lanka as well. The costs of not handling it are far too high (consistent long blackouts and queues).

18/ However, I'm somewhat cautiously optimistic it will be done in the end. All we've seen so far has pointed towards at least the financial side being handled. It's also that things are so fragile, that no one can realistically lounge in inaction like before.

19/ There's also push from all parts of society to move into low-cost energy generation (though plenty of politics as well). I think there is strong enough of a push that will at least get this process started, especially if the CEB's restructuring continues to plod along.

20/ However, there are massive distributive impacts, and those haven't been handled well at all. Dealing with that will be a critical part of this whole puzzle of course. In a later piece, I'll explore what can be done separately as mentioned before.

21/ What we end up with won't be perfect of course, but there's a good enough chance that it will be a lot better than what we had before. That way, maybe the lights can stay on for much longer now.

Loading suggestions...