Key highlights from IG Petrochemicals Q3FY23 concall:

CMP: ₹ 424

Like and Retweet for Maximum Reach!

CMP: ₹ 424

Like and Retweet for Maximum Reach!

1. The company faced a subdued demand for PAN as this product finds applications in more than 20 user industries which include paints, plasticizers and pigments, these 3 contributing more than 50% to the company’ business.

There was slowdown in these 3 industries as China increased the anti-dumping duty on CPC pigment & also there was COVID-19 disturbance in China which led to shutdown of some of the CPC players in India. These CPC players formed 15-20% of the overall customer base of the company.

2.The company typically sold 10-15 % of their overall production to the CPC and pigment segment. India has 4 or 5 plants for CPC pigments out of which 3-4 were shut down for 1-2 months post the anti-dumping duty enforced by China and though

they have begun operations right now, the demand is only 50-60% of what it was before the shutdown.

3. The US introduced an antidumping duty of 400% on unsaturated polyester resins(UPR) in October 2023 and since UPR is a major market for PAN, the increase in antidumping duty led to a further decrease in PAN demand.

The company is expecting good demand for its PAN from February 2023 as the US withdrew the anti dumping duty on PAN in December 2023.

4. Revenues from non-phthalic anhydride business were Rs 129 crore vs Rs 40 crore in the previous quarter. The company has more than Rs 300 crore of cash in the balance sheet.

-The company made Rs 15 crores each from maleic anhydride(MAN) and diethyl phthalate(DEP) which form part of the non-phthalic anhydride business.

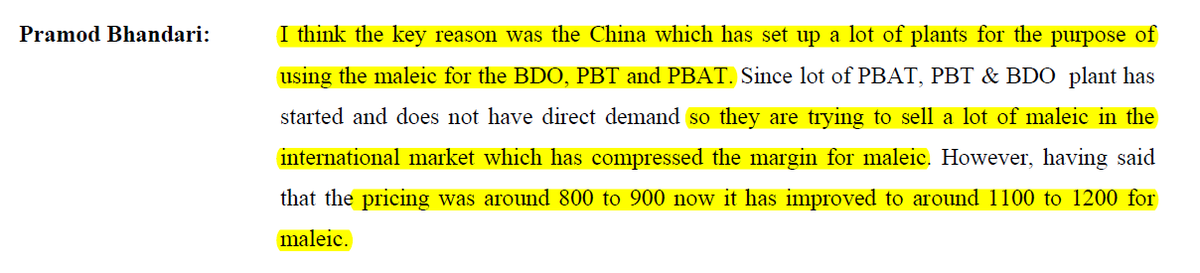

-The demand for MAN was weak as China put up capacities for BDO, PBT and PBAT which use MAN as a precursor. China has also been

-The demand for MAN was weak as China put up capacities for BDO, PBT and PBAT which use MAN as a precursor. China has also been

selling a lot of MAN in the international market which led to a compression in margins. The pricing for MAN has however improved from Rs 800-900/kg to Rs 1100 to Rs 1200/kg.

-The company is expecting Rs 100 crores from MAN on an annualized basis once the demand for MAN improves.

-The company is expecting Rs 100 crores from MAN on an annualized basis once the demand for MAN improves.

5. The management is confident of achieving the target of Rs 430 crore from non-PAN products by FY25 which will be almost 30% of revenue contribution from non-PAN business.The long-term target of the management is to get 50% of revenues from these products.

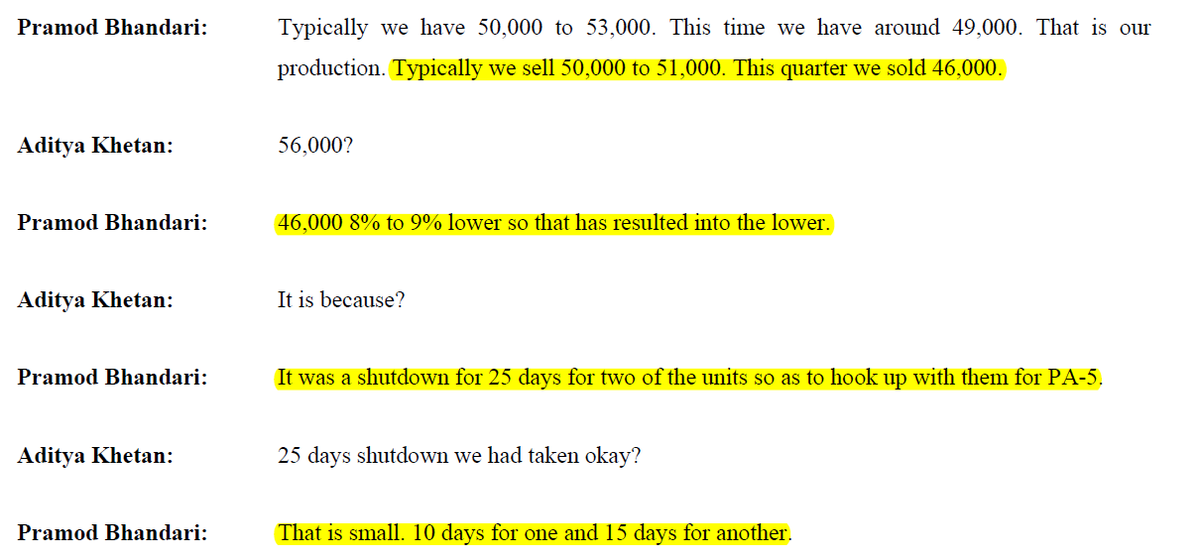

-The company typically sells 50-51K tons however, they sold 46000 MTPA in this quarter which was an 8-9% decline on a Q-o-Q basis as there was a 10 day shutdown for one unit and a 15 day shutdown of another unit so as to hook up with them for PA-5.

-The company expects to get back to normal volumes by the next quarter.

6. The company has incorporated the wholly owned subsidiary IGPL International Ltd for manufacturing downstream derivatives, marketing of PAN and sourcing of orthoxylene(OX).

The company is on track to commission its PA-5 unit which will manufacture Phthalic anhydride(PAN),

The company is on track to commission its PA-5 unit which will manufacture Phthalic anhydride(PAN),

MAN and Benzoic acid by March 2024. The total PAN,MAN and benzoic acid capacity of the company will increase to 2,75,100 MTPA, 9160 MTPA and 1250 MTPA respectively once this capacity comes online.

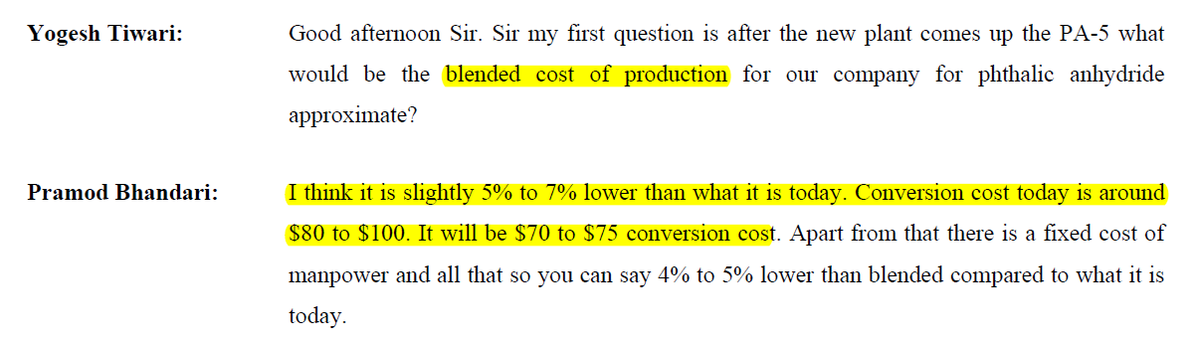

7. The cost of producing PAN in this new PA-5 facility will be 15-20% lower than the existing facilities as all the phthalic plants of the company are in the same location. The blended cost of production would be 5-7% lower than the existing cost and the conversion cost will

decrease from $80 to 100 to $70 to 75.

8. The company has spent Rs 150 crores for PA-5 and the project is almost 80-85% complete.

Along with PA-5, the company is working on 2-3 projects which are yet to be approved by the company board of directors.

Along with PA-5, the company is working on 2-3 projects which are yet to be approved by the company board of directors.

Loading suggestions...