Key highlights from Steelcast Ltd Q3FY23 Concall:

CMP: ₹ 485

Like and Retweet for Maximum Reach!

CMP: ₹ 485

Like and Retweet for Maximum Reach!

1. The company has clocked a volume of 4000-4100 tons for Q3FY23. The target of the company is to do 5000 tons per quarter. The company plans to get 16,000 tons of volume in FY23 about 20-21K tons per annum in FY24.

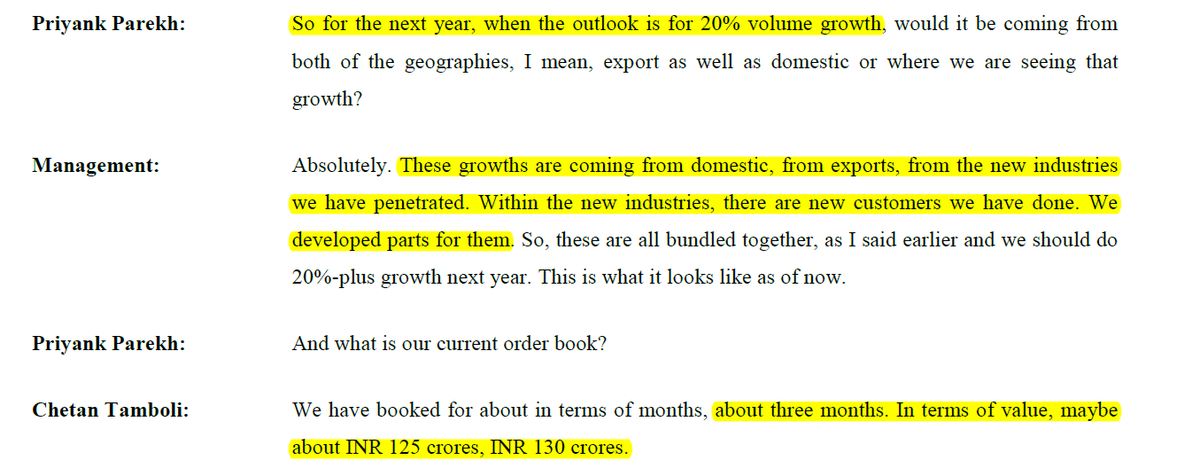

2. The outlook of the company is for a 20% volume growth next year which would be coming from both the domestic and export markets, new customers in new industries where the company has successfully penetrated and from the existing customers and industries.

The current order book of the company is of 3 months with the value being ₹125 - ₹130 crores.

3. The company’s customers give them a clear order visibility of 12 months with the company getting confirmed orders within the first 3 months hence, the company is confident of achieving its projected target.

4. The company is in talks to supply their products to the US railroad. The inspection part of the supply certificate is done and the entire internal process is expected to be completed by February 2023 end.

The company will start selling orders as soon as they get the customers who need the AAR approvals.

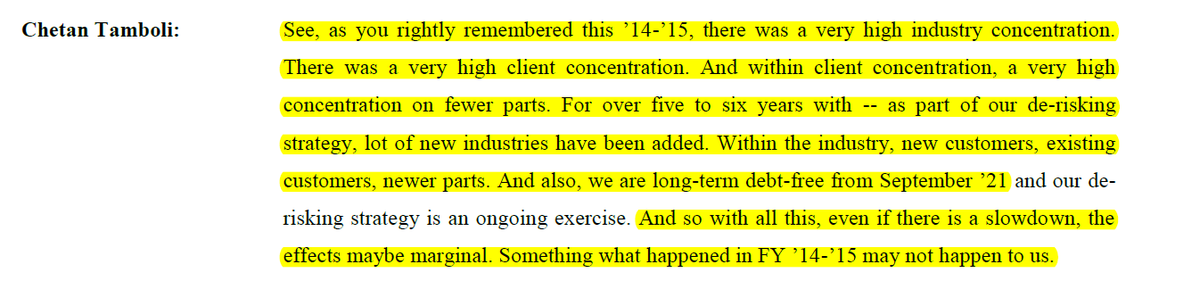

5. The company is consistently adding new customers from various industries and became long-term debt free from September 2021 which was part of their de-risking strategy in the last 4-5 years.

The company hopes to remain resilient in event of a slowdown and won’t be affected to the extent it was affected in 2014-15.

6. The newer industries which the company has focused on over the last 2-3 years are locomotives, ground engaging tools , railroad and to some extent defence.

The defence parts would be going into the defence equipment's, ground engaging tools will be used for mining and earth-moving industries, the locomotive.

components will go into the locomotives made by companies like General Motors, Caterpillar and General Electric and the bogie parts will go into the railroad industry.

7. The peers of the company in steel foundry are PTC industries, Gujarat Intrux, Magna Electrosteel,

7. The peers of the company in steel foundry are PTC industries, Gujarat Intrux, Magna Electrosteel,

Simplex Castings and one player in the listed space.

8. The company plans to sustain the gross margins of 73% for the next few quarters with the assumption that raw material prices don’t move much.

8. The company plans to sustain the gross margins of 73% for the next few quarters with the assumption that raw material prices don’t move much.

However, the focus of the company is more towards increasing volumes and future growth than gross margins and EBITDA.

9. The company however will try to maintain EBITDA margins in the range of 20-25%.

9. The company however will try to maintain EBITDA margins in the range of 20-25%.

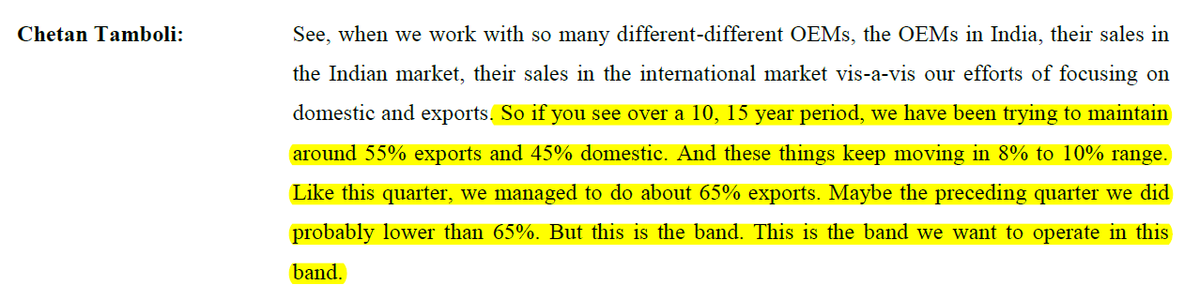

10. The company plans to keep the share between exports and domestic market in the 55:45 range over the long term though there may be some changes in the short term.

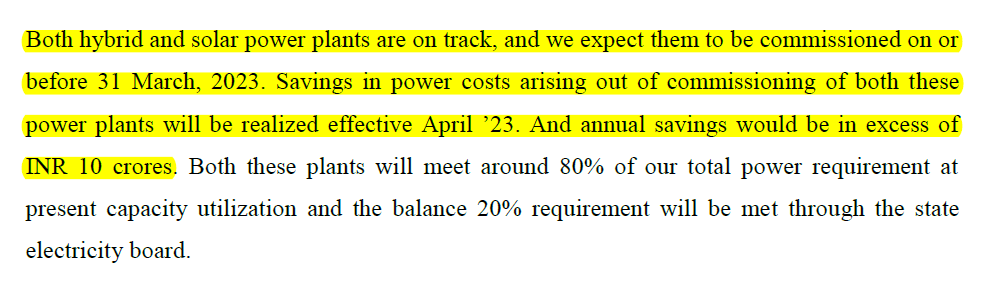

11. The hybrid and solar power plant projects are on track and expected to come onstream on or before 31 March 2023. The plan of the company is to set up a 5MW solar power plant in Gujarat for captive consumption and it has a 25 years signed PPA agreement for solar and

wind hybrid power projects. The savings in power costs from both these projects combined will be in excess of ₹10 crores on an annual basis with the benefits accruing from April 2023 onwards.

These plants will be enough to meet 80% of the total power requirement of the company with the balance being met by the state electricity board.

12. The company is right now at around 70% capacity utilisation and plans to achieve complete capacity utilisation by FY27.

13. The company will announce its capex plan in Q1FY24 once it has made its decision. The capex will preferably be a greenfield capex.

13. The company will announce its capex plan in Q1FY24 once it has made its decision. The capex will preferably be a greenfield capex.

Loading suggestions...