Key highlights from Bodal Chemicals Q3FY23 Concall:

CMP: ₹ 62.6

Like and Retweet for Maximum Reach!

CMP: ₹ 62.6

Like and Retweet for Maximum Reach!

1. There has been a slowdown in the US and Europe which are the major markets for the company. The slowdown has been going on for the last 6 months due to rising inflation and uncertain geopolitical scenarios.

China’s growth has been sluggish due to zero COVID policy which has impacted the prices of commodities around the world which include dyestuff and dye intermediates.

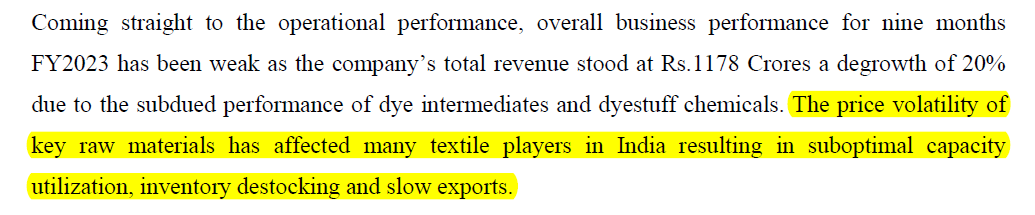

2. The situation is almost similar in India where many Indian textile players have been impacted to due to price volatility of key raw materials leading to suboptimal capacity utilization, inventory destocking and slow exports.

3. The dye intermediates manufacturers in India are under pressure due to slow demand from the dyestuff consuming industries like textiles, leather, paper and others.

The company expects some nominal improvement in the dye intermediates business going forward with a good demand coming in the next 3-4 months.

4. Zhejiang and Longhseng are the 2 largest players in H Acid and Vinyl Sulphone which are dye intermediates made by the company.

4. Zhejiang and Longhseng are the 2 largest players in H Acid and Vinyl Sulphone which are dye intermediates made by the company.

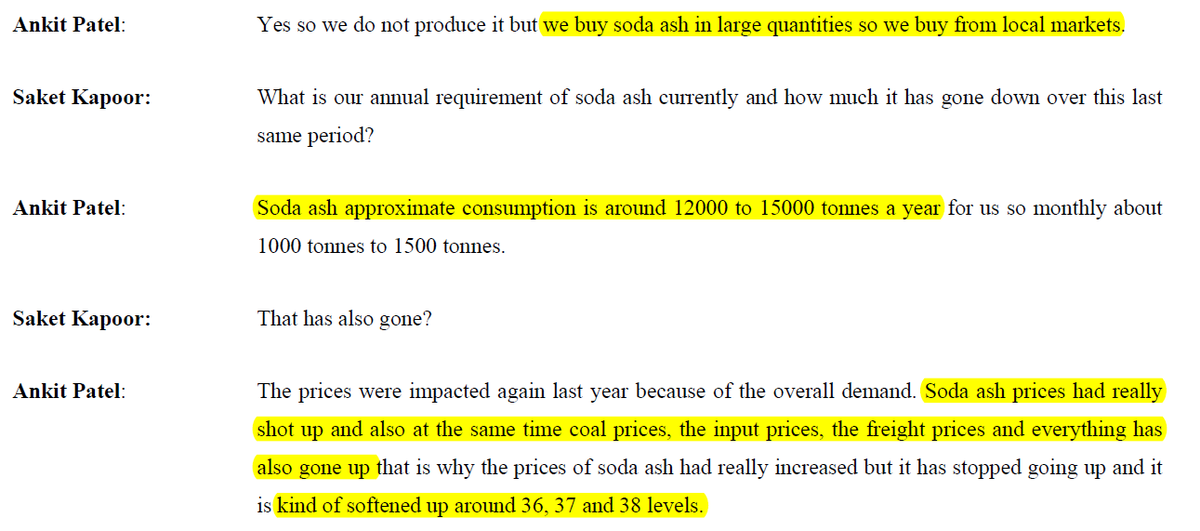

5. The company buys soda ash from local markets for production of dyestuff where the company’s approximate annual consumption is 12000 to 15000 TPA which has been impacted right now due to spike in soda ash prices, coal prices, input prices and freight prices.

5. There was a lower production in Q3FY23 for the Chlor Alkali products as it was undergoing a technology upgradation and capacity expansion which led to almost 70-80% of October month being wasted.

This carried forward to the basic chemicals business where there was a lower production in November 2022 as the company took an annual shutdown for government agencies, boiler inspection and some other maintenance.

6. The company was earlier producing 55000 to 60000 MTPA annually for the chlor alkali products before undergoing the technology upgradation and once the technology upgradation is complete, the company can produce as much as 90,000 MTPA which is almost a 50% jump in volume,

the total capacity of Chlor Alkali being 99,000 MTPA. The company will attain full capacity utilisation by FY24.

7. The total capex done for Chlor Alkali is ₹310 crores out of which about ₹150 crores was spent for the acquisition of Siel Chemical Complex (SCC) and the remaining amount was spent for modernization, capacity expansion and some normal replacement capex.

8. One of the customers of the company is setting up a chlorinated paraffin wax(CPW) plant which is traditionally a chlorine pipeline for almost all the plants across India. The company already has 4 CPW plants in the vicinity of their Chlor Alkali plant at Rajpura,

Punjab and the 5th one is coming up. The customer will get the EC within 12 months, and they will buy 60 TPD of chlorine from the company by pipeline.

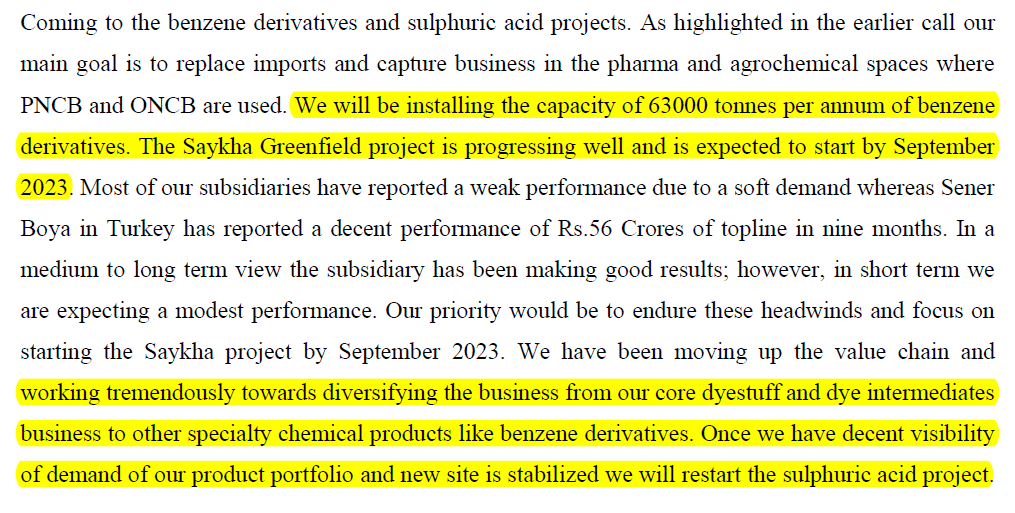

9. The Saykha Greenfield project for the expansion of benzene and sulphuric acid and their derivatives is on track and the 63,000 MTPA benzene derivatives plant is expected to come online by Q2FY24 or September 2023.

10. The strategy of the company is to diversify their business from the core dyestuff and dye intermediates business to other products like sulfuric acid and benzene and their derivatives.

The company right now has put the sulphuric acid expansion on hold and they will resume this project once they have a clear visibility of demand for their product portfolio.

Loading suggestions...