Update: Axis Bank has completed acquisition of Citibank’s consumer business.

The Bank acquires:

🔸Rs 273 bn in assets

🔸Rs 400 bn of liabilities

for cash consideration of Rs 116.03 bn

Axis mgmt called it one the most complex acquisitions in India’s private banking history

🧵1/

The Bank acquires:

🔸Rs 273 bn in assets

🔸Rs 400 bn of liabilities

for cash consideration of Rs 116.03 bn

Axis mgmt called it one the most complex acquisitions in India’s private banking history

🧵1/

2/

Implied Equity value is Rs 149 bn, indicating a acquired valuation of 17.7x P/E based on FY22 earnings.

Deal appears favorable as it aligns with Axis' premiumization strategy and gives access to Citi’s

- Huge retail deposit base

- Affluent and profitable consumer franchise

Implied Equity value is Rs 149 bn, indicating a acquired valuation of 17.7x P/E based on FY22 earnings.

Deal appears favorable as it aligns with Axis' premiumization strategy and gives access to Citi’s

- Huge retail deposit base

- Affluent and profitable consumer franchise

3/

Some takeaways from Axis Bank conference call:

🔸ROE for Citi business comes at 21.7% and hence this business would be RoE accretive.

🔸Axis Bank had ROE of ~13% in FY22 and annualized ROE of 19.8% based on Q3FY23 results.

Some takeaways from Axis Bank conference call:

🔸ROE for Citi business comes at 21.7% and hence this business would be RoE accretive.

🔸Axis Bank had ROE of ~13% in FY22 and annualized ROE of 19.8% based on Q3FY23 results.

4/

🔸The acquisition was completed in an accelerated timeframe of 7 months post CCI approval and ahead of schedule.

🔸There is an estimated integration cost of Rs 15 bn (of which Rs 12 bn will be paid to Citibank) which is distributed over next 18 months (Sep 2024).

🔸The acquisition was completed in an accelerated timeframe of 7 months post CCI approval and ahead of schedule.

🔸There is an estimated integration cost of Rs 15 bn (of which Rs 12 bn will be paid to Citibank) which is distributed over next 18 months (Sep 2024).

5/

🔸P&L hit likely in Q4FY23: The cash purchase consideration will result in the formation of goodwill which Axis Bank will be writing off entirely in Q4.

🔸This will result in an accounting loss of Rs 50-60 bn towards one-time Goodwill cost, provisions, banker fees, etc

🔸P&L hit likely in Q4FY23: The cash purchase consideration will result in the formation of goodwill which Axis Bank will be writing off entirely in Q4.

🔸This will result in an accounting loss of Rs 50-60 bn towards one-time Goodwill cost, provisions, banker fees, etc

6/ Capital Adequacy (CAR)

🔸The deal will impact Axis Bank’s Tier 1 CAR by 180 bps from 15.5% to 13.8%, bringing it close to minimum required threshold

🔸Management highlighted that it does not need to raise capital immediately and has sufficient capital to fund organic growth

🔸The deal will impact Axis Bank’s Tier 1 CAR by 180 bps from 15.5% to 13.8%, bringing it close to minimum required threshold

🔸Management highlighted that it does not need to raise capital immediately and has sufficient capital to fund organic growth

7/

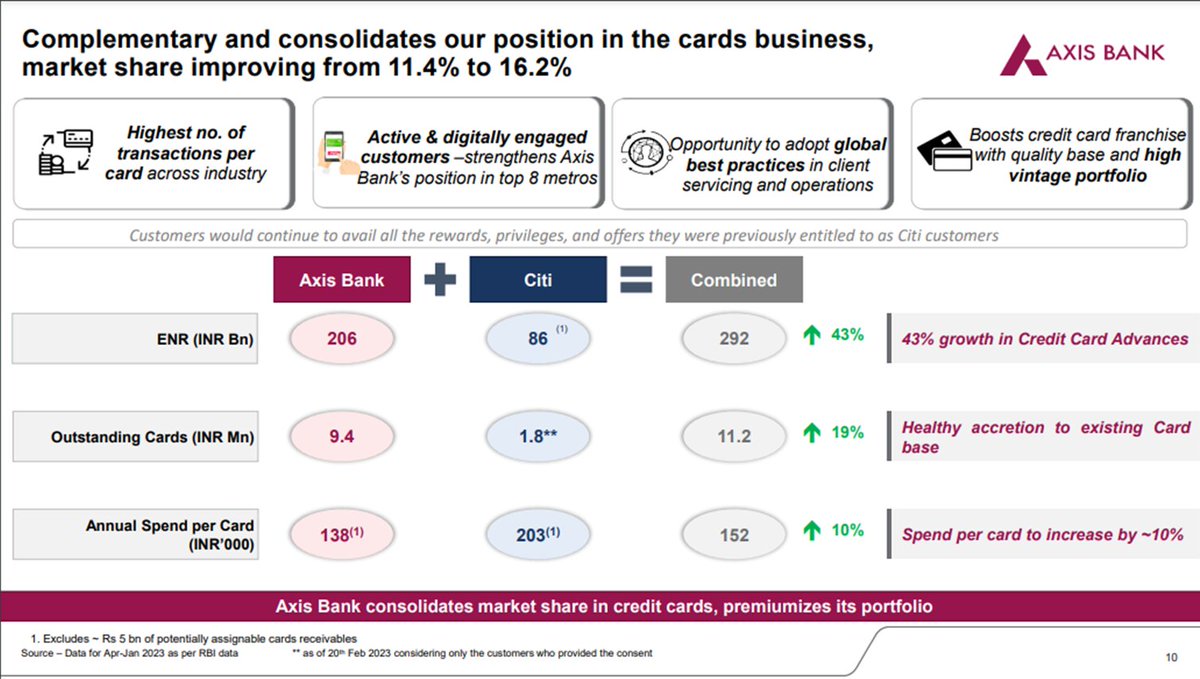

What does Axis Bank gain

🔸Access to Citi’s 6 Indian offices, 21 branches & 459 ATMs

🔸Credit card portfolio of 18 lakh+ premium customers with industry leading spends per card

Bank has taken explicit consent of customers before moving them to Axis from Citi

More details:

What does Axis Bank gain

🔸Access to Citi’s 6 Indian offices, 21 branches & 459 ATMs

🔸Credit card portfolio of 18 lakh+ premium customers with industry leading spends per card

Bank has taken explicit consent of customers before moving them to Axis from Citi

More details:

8/ What about Citibank's employees?

🔸Axis made offers to every Citi employee who was part of this transaction

🔸~96% of employees, accepted the offer across grades and locations (Total: ~3200)

As per mgmt, the offer by Axis Bank was no less favorable for the Citi employees.

🔸Axis made offers to every Citi employee who was part of this transaction

🔸~96% of employees, accepted the offer across grades and locations (Total: ~3200)

As per mgmt, the offer by Axis Bank was no less favorable for the Citi employees.

9/ Key risk:

In near term, the acquisition will not be financially accretive, and lead to a hit on Net worth (via Goodwill write-off) and CET-1 (due to capital allocation).

The indicated integration cost of Rs 15 Bn over next 2 years could need for make equity raise imminent.

In near term, the acquisition will not be financially accretive, and lead to a hit on Net worth (via Goodwill write-off) and CET-1 (due to capital allocation).

The indicated integration cost of Rs 15 Bn over next 2 years could need for make equity raise imminent.

Follow us at @ICICI_Direct for more such Equity market insights and updates.

Link to the top of thread:

Link to the top of thread:

Loading suggestions...