WHAT IS GOING ON IN THE USA (EU next) BANKING SYSTEM. 3d

as most of you know, SVB failed. It is the second biggest banking failure in the USA since 2008

Since rumors spread on thursday 9 of March, the stock tanked.

1/n

as most of you know, SVB failed. It is the second biggest banking failure in the USA since 2008

Since rumors spread on thursday 9 of March, the stock tanked.

1/n

the FDIC stepped in on Friday 10th. Full resolution. No bail out. Bail in actually.

see my tweet

that is IMHO the only way to preserve the banking system, isolate the risk "vertically", do not create domino

Basically isolating the shit from the fan

2/n

see my tweet

that is IMHO the only way to preserve the banking system, isolate the risk "vertically", do not create domino

Basically isolating the shit from the fan

2/n

ofcourse there are effects. and big also. 97.3% of $175bn deposits are above the guarantee threshold of $250K

Hence those depositors would have to wait the result of SVB asset sale to get some money back

3/n

Hence those depositors would have to wait the result of SVB asset sale to get some money back

3/n

but bailing-out would have moved SVB risk to the system, signaling that in any bank failure good banks will be called-in to rescue bad banks, in order to bail out depositirs, bond holders or else

this would imply spreading out risk. We did it in Italy

4/n

this would imply spreading out risk. We did it in Italy

4/n

Few years ago we created Atlante, an all-banks backed fund to rescue 2 small banks depositors.

It ended up in crashing all banks stocks, and spread widening. Shit did hit the fun...lets say

Contagion was "institutionalised"

A mistake by amateurs (yeah Bank of Italy)

5/n

It ended up in crashing all banks stocks, and spread widening. Shit did hit the fun...lets say

Contagion was "institutionalised"

A mistake by amateurs (yeah Bank of Italy)

5/n

but...why is this happening now? is this systemic? the system is falling down?

Simple answer is not possible.

As you all know the Inflation genie is out of the lamp

Fed and ECB are raising rates (too late too little IMHO but nevermind)

6/n

Simple answer is not possible.

As you all know the Inflation genie is out of the lamp

Fed and ECB are raising rates (too late too little IMHO but nevermind)

6/n

Hence banks that live out of interest margin and other revenues from investments or commission on services, will have to re-price the asset side (loans) and the liability side (deposits)

did they do that? well..

for sure on the asset side they started. But on the liability?

7/n

did they do that? well..

for sure on the asset side they started. But on the liability?

7/n

the chart below is M1 in USA. Cash, bank deposits....money equivalent stuff

Never in the history we saw M1 on the negative side. Ever.

That calls for deposit outflow

7/n

Never in the history we saw M1 on the negative side. Ever.

That calls for deposit outflow

7/n

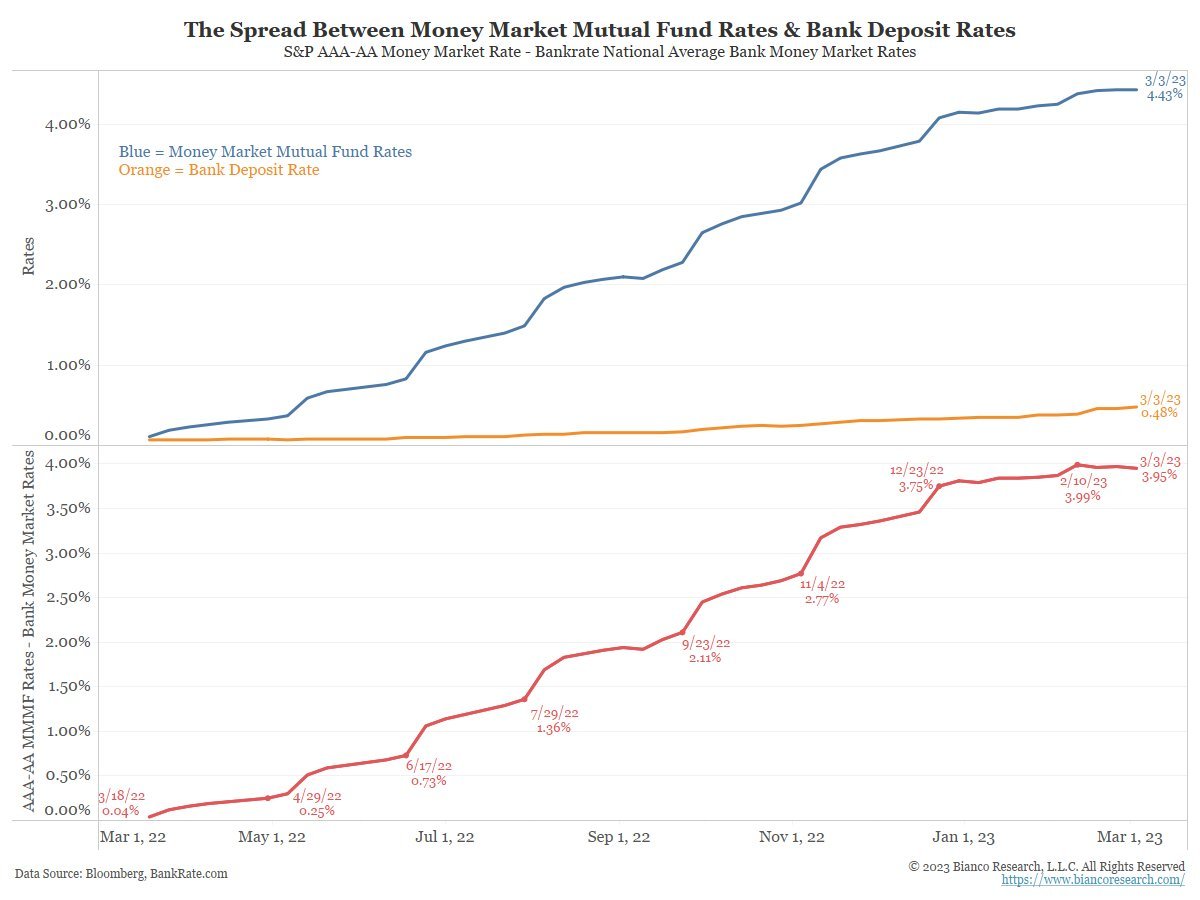

If we compare with M2 which includes Money Market Fund (MMF) by retail we can see that the effect is much lower.

Indicating MMF inflow

8/n

Indicating MMF inflow

8/n

why is that? and what this has to do with SVB?

Banks did not re-price deposits rates.

They are not paying you enough for leaving your money there. MMF are paying you more

chart by @biancoresearch

8/n

Banks did not re-price deposits rates.

They are not paying you enough for leaving your money there. MMF are paying you more

chart by @biancoresearch

8/n

why is that?

it is a bit technical...but i will try to make it simple

14 years of QE provided banks cheap deposits ( i sell my shit to the Fed, and the Fed credits some reserves to me which i can use to settle with other banks)

so there was no liquidity issue

8/n

it is a bit technical...but i will try to make it simple

14 years of QE provided banks cheap deposits ( i sell my shit to the Fed, and the Fed credits some reserves to me which i can use to settle with other banks)

so there was no liquidity issue

8/n

now, not only QE is over, but the Fed provides some 4.5% remuneration when u deposit money to it (via the so called reverse repo rate or RRP). It is the highest part of FED rate corridor

9/n

9/n

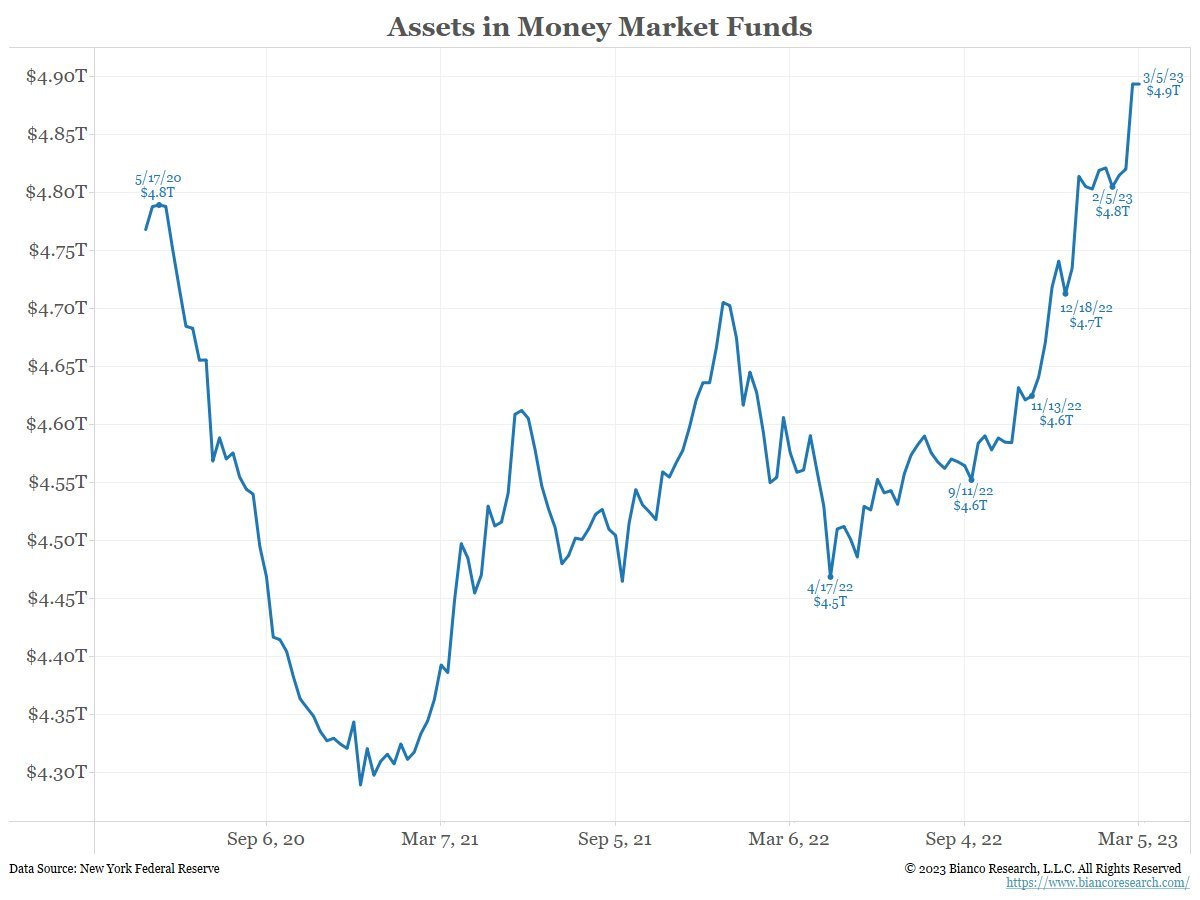

So bank deposits have a competitor.

Primarily MMF

since rate went up. MMF assets grew. Bank deposits fell

charts again by @biancoresearch

10/n

Primarily MMF

since rate went up. MMF assets grew. Bank deposits fell

charts again by @biancoresearch

10/n

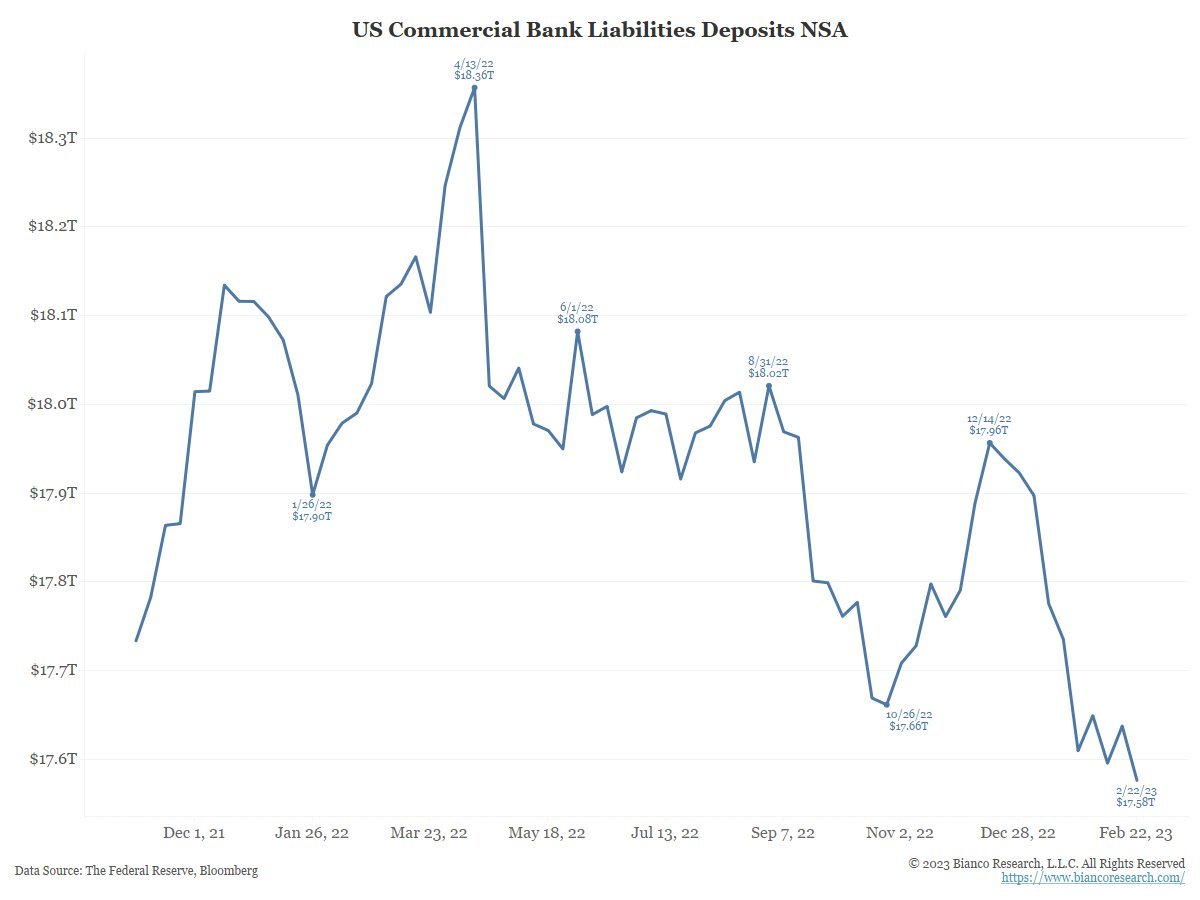

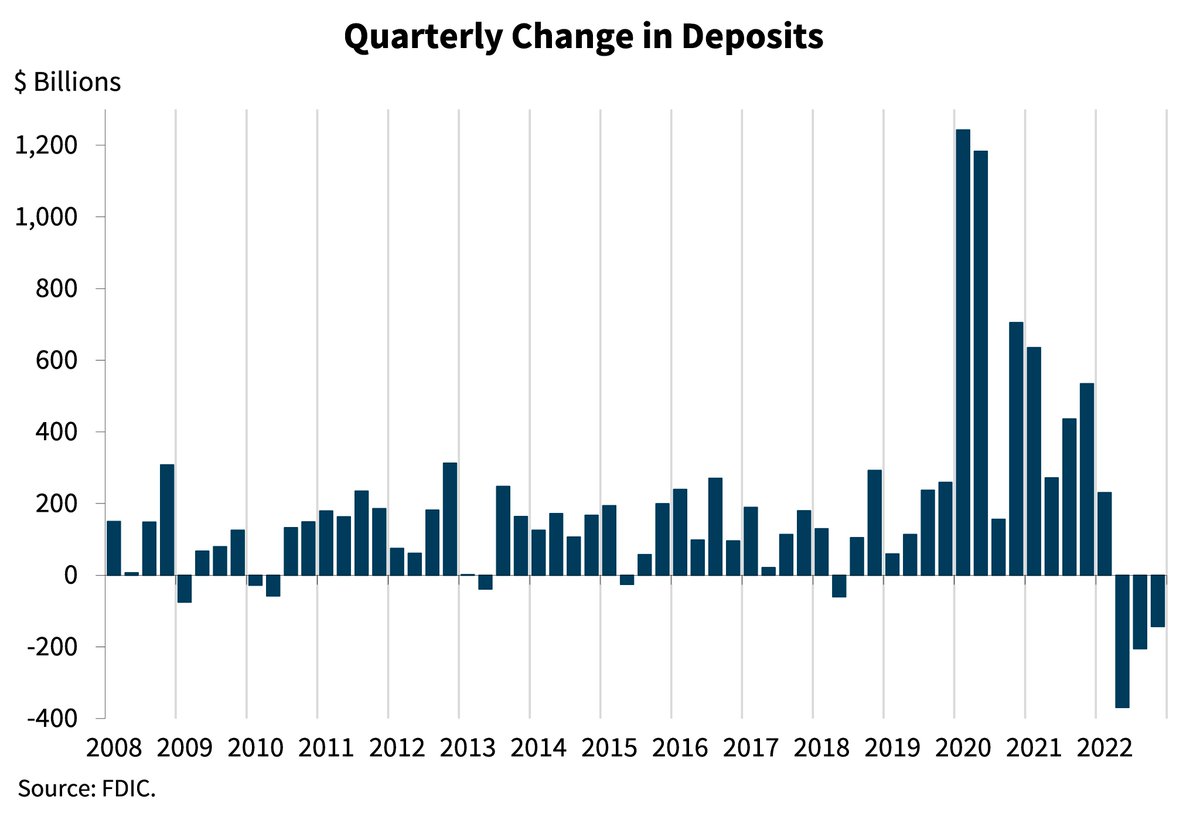

when banks have deposit outflow they can do few things

1) sell some assets and get the cash to reimbourse the depositors' claim

2) raise money via rights issue (equities), bonds, CD or the likes

12/n

1) sell some assets and get the cash to reimbourse the depositors' claim

2) raise money via rights issue (equities), bonds, CD or the likes

12/n

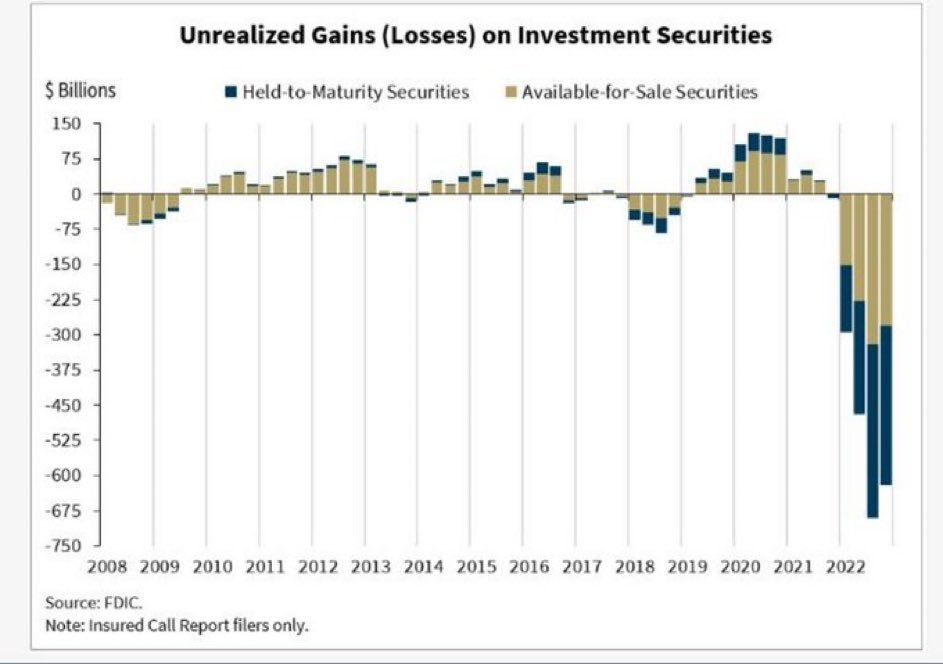

on 1) (selling assets) the rapid increase rate due to out of control inflation, has created some substantial losses on bank investment portfolios

from the same above link to FDIC' Gruenenberg speech

13/n

from the same above link to FDIC' Gruenenberg speech

13/n

so yeah, banks can sell but at a loss (NB in my calculation the loss is currently equivalent to circa 30% of CET1 of the USA banks)

This is what SVB did on thursday: to respond o deposit outflow,

14/n

This is what SVB did on thursday: to respond o deposit outflow,

14/n

SVB sold $21bn bond portfolio at a $2bn loss as the portfolio was 3yr duration, fixed rate circa 1.8%

Incredible IRR (interest rate risk) mismanagement, isnt it?

The Cfo had evidently better things to do during the superslow, super pre-advised rate tightening cycle

15/n

Incredible IRR (interest rate risk) mismanagement, isnt it?

The Cfo had evidently better things to do during the superslow, super pre-advised rate tightening cycle

15/n

Due to the 2bn loss, SVB took a capital hit. Therefore on Friday 10th it entered phase

2) raising equity (tweet #12) to calm depositors, and restor regulatory capital

The equity raise failed

FDIC went in

16/n

2) raising equity (tweet #12) to calm depositors, and restor regulatory capital

The equity raise failed

FDIC went in

16/n

all this to say that

1) Banks as a whole dont face a solvency issue even if the were to take all the losses on their bond portfolio tomorrow. Which they dont have to, as many banks have other assets, or enough liquidity to face outflows

17/n

1) Banks as a whole dont face a solvency issue even if the were to take all the losses on their bond portfolio tomorrow. Which they dont have to, as many banks have other assets, or enough liquidity to face outflows

17/n

NB: outflow from one bank goes to other bank or to MMF. But they stay in the system. Deposits do not disappear

2) Banks face a profitability risk instead becouse they will have to increase deposit rates (a cost on the P&L) if they dont want to incur in lethal risk

18/n

2) Banks face a profitability risk instead becouse they will have to increase deposit rates (a cost on the P&L) if they dont want to incur in lethal risk

18/n

the lethal risk being represented by a bank-run on low yielding deposits

3) by raising deposit rates (funding costs) profitabilty could be impaired if asset rates will not be repriced.

19/n

3) by raising deposit rates (funding costs) profitabilty could be impaired if asset rates will not be repriced.

19/n

And the latter (which has already been partially done) depends prett much on each bank credit underwriting/scoring profile

4) some banks which didnt manage IRR well could go under only if they will not be in the position to sell assets with a loss or raise equity/bonds

20/n

4) some banks which didnt manage IRR well could go under only if they will not be in the position to sell assets with a loss or raise equity/bonds

20/n

all in all i think the issue we are seeing these days have a fix

raising deposit rates

This will impair banks profitability, and future lending growth

but this is another story

21/21

raising deposit rates

This will impair banks profitability, and future lending growth

but this is another story

21/21

PS on tweet #5

that Atlante was a mistake by amatuers that know little on credit, i said it on the time of unfolding.

we sold banking stocks short when the day of announcement the banks were up 5% and my competitors were cheering it

my clients know that

just saying

that Atlante was a mistake by amatuers that know little on credit, i said it on the time of unfolding.

we sold banking stocks short when the day of announcement the banks were up 5% and my competitors were cheering it

my clients know that

just saying

tagging @Frances_Coppola due to my unforgivable shortcoming of not doing it before

PS #2 ON CONTAGION AKA ON HOW NOT TO MANAGE A BANK FAIL

Step 1) create a 'systemic bank bailout funds backed by all banks'

Step 2) crash the system

Ita vs eu banks since Atlante

How nice it was

@INArteCarloDoss @degiorgiod @jeuasommenulle @ThManfredi @ecommerceshares

Step 1) create a 'systemic bank bailout funds backed by all banks'

Step 2) crash the system

Ita vs eu banks since Atlante

How nice it was

@INArteCarloDoss @degiorgiod @jeuasommenulle @ThManfredi @ecommerceshares

Loading suggestions...