1/104

The Ultimate Tokenomics Mega Thread 🫡

What to Look for in a Project for your Next x100 🧵👇

The Ultimate Tokenomics Mega Thread 🫡

What to Look for in a Project for your Next x100 🧵👇

2/104

This piece provides a comprehensive overview of tokenomics, showing why it is important and how well-designed tokenomics can be implemented.

This piece provides a comprehensive overview of tokenomics, showing why it is important and how well-designed tokenomics can be implemented.

3/104

We leverage the structure provided by @BinanceResearch, complementing it with other primary sources and practical case studies of different tokenomics.

We leverage the structure provided by @BinanceResearch, complementing it with other primary sources and practical case studies of different tokenomics.

4/104

> Tokenomics can be defined as the study of determining and evaluating the economic characteristics of a cryptographic token to understand how various incentives affect the supply and demand of a token and its price.

> Tokenomics can be defined as the study of determining and evaluating the economic characteristics of a cryptographic token to understand how various incentives affect the supply and demand of a token and its price.

5/104

It includes all of the following design categories:

• Initial supply and allocation to the team, investors, community, and other stakeholders;

• Methods of distribution: token purchases, airdrops, grants, and partnerships;

It includes all of the following design categories:

• Initial supply and allocation to the team, investors, community, and other stakeholders;

• Methods of distribution: token purchases, airdrops, grants, and partnerships;

6/104

• The revenue split between users, service providers, and protocol;

• Treasury size, structure, and intended uses;

• Emission schedule including inflation, mint/burn rights, and supply caps;

• Coin governance including voting, escrow and vesting;

• The revenue split between users, service providers, and protocol;

• Treasury size, structure, and intended uses;

• Emission schedule including inflation, mint/burn rights, and supply caps;

• Coin governance including voting, escrow and vesting;

7/104

• Miner and validator compensation such as fees, emissions, and penalties;

• Usage of protocol’s native tokens versus external tokens (e.g. ETH, USDC).

• Miner and validator compensation such as fees, emissions, and penalties;

• Usage of protocol’s native tokens versus external tokens (e.g. ETH, USDC).

8/104

For founders, figuring out the right tokenomics might make the difference between success and failure. For investors, assessing the tokenomics of a token is fundamental before deciding to invest.

For founders, figuring out the right tokenomics might make the difference between success and failure. For investors, assessing the tokenomics of a token is fundamental before deciding to invest.

9/104

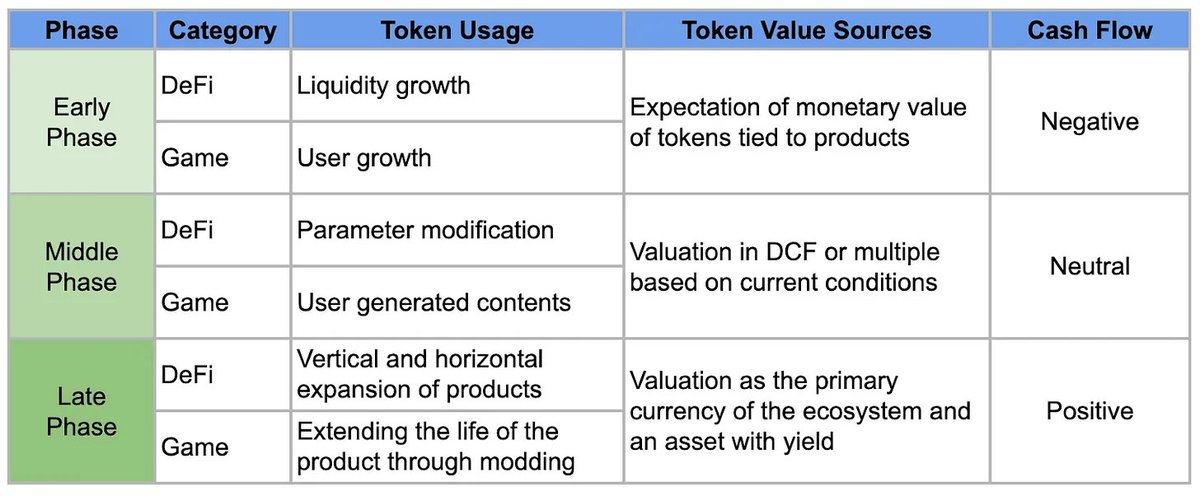

Perfect tokenomics do not exist. Different protocols require different systems put in place to ensure proper functioning and alignment of interest between demand and supply. A DeFi protocol will have different tokenomics than a Gaming protocol.

Perfect tokenomics do not exist. Different protocols require different systems put in place to ensure proper functioning and alignment of interest between demand and supply. A DeFi protocol will have different tokenomics than a Gaming protocol.

10/104

Before even thinking about the delicate balance of factors in a well-rounded tokenomics, let’s take a step back.

Before even thinking about the delicate balance of factors in a well-rounded tokenomics, let’s take a step back.

11/104

The first question a protocol should be asking is: do I really need a token? For some, minting a token might be just an easy way out to cash on the project and rug the community. For others, their use case may require a token.

The first question a protocol should be asking is: do I really need a token? For some, minting a token might be just an easy way out to cash on the project and rug the community. For others, their use case may require a token.

12/104

Not all projects have a token, and not all need a token. In the long run, good projects with strong fundamentals will always win over those with bad fundamentals.

Why would a protocol require a token?

1. Economic Reasons;

2. Structural Reasons.

Not all projects have a token, and not all need a token. In the long run, good projects with strong fundamentals will always win over those with bad fundamentals.

Why would a protocol require a token?

1. Economic Reasons;

2. Structural Reasons.

13/104

1. Economic Reasons

Tokens help companies raise capital to maintain and grow the business, they are more dynamic and have more use cases that are not possible with other forms of fundraising.

1. Economic Reasons

Tokens help companies raise capital to maintain and grow the business, they are more dynamic and have more use cases that are not possible with other forms of fundraising.

14/104

For instance, only accredited investors can invest in equities during an IPO - compare that to an ICO in 2017. Raising funds from early users is also an important marketing tool to attract an initial critical mass and user base that is interested in the project.

For instance, only accredited investors can invest in equities during an IPO - compare that to an ICO in 2017. Raising funds from early users is also an important marketing tool to attract an initial critical mass and user base that is interested in the project.

15/104

This means that tokens can be more dynamic in their nature and provide more use cases than alternative means of funding.

This means that tokens can be more dynamic in their nature and provide more use cases than alternative means of funding.

16/104

2. Structural Reasons

Tokens can be employed for governance purposes and can contribute to the decentralization of a protocol (e.g. in a DAO).

2. Structural Reasons

Tokens can be employed for governance purposes and can contribute to the decentralization of a protocol (e.g. in a DAO).

17/104

They are used to ensure incentive alignment between all parties:

1. Users — want to have certainty about transaction costs, and security about the availability of services;

2. Founding Team — want to sustain and grow their company and make money;

They are used to ensure incentive alignment between all parties:

1. Users — want to have certainty about transaction costs, and security about the availability of services;

2. Founding Team — want to sustain and grow their company and make money;

18/104

3. Investors (token holders = speculators) — want the value of their tokens to go up as platform use goes up.

3. Investors (token holders = speculators) — want the value of their tokens to go up as platform use goes up.

19/104

4. Miners (in a Proof-of-work network) — want steady, safe income. Miners typically sell their tokens to fund their operations exerting strong selling pressure on the token — on Proof-of-Stake networks, stakers have similar incentives.

4. Miners (in a Proof-of-work network) — want steady, safe income. Miners typically sell their tokens to fund their operations exerting strong selling pressure on the token — on Proof-of-Stake networks, stakers have similar incentives.

20/104

According to Binance Research, “subsidization via a token can only happen if the token holds some value in the open market, which in turn, can only happen if the token is effective in capturing the value generated by the protocol itself or offers another form of utility”

According to Binance Research, “subsidization via a token can only happen if the token holds some value in the open market, which in turn, can only happen if the token is effective in capturing the value generated by the protocol itself or offers another form of utility”

21/104

This term is usually referred to as Value Accrual: how well the token captures the value created by the protocol. This in turns contributes to whether there is external demand for the token and how desirable it is to hold it.

This term is usually referred to as Value Accrual: how well the token captures the value created by the protocol. This in turns contributes to whether there is external demand for the token and how desirable it is to hold it.

22/104

Let’s now focus on the two different aspects of Tokenomics: Supply and Demand.

Let’s now focus on the two different aspects of Tokenomics: Supply and Demand.

23/104

To simplify:

• Supply: the number of people willing to sell their tokens;

• Demand: people willing to buy.

The balance between demand and supply defined the token price.

To simplify:

• Supply: the number of people willing to sell their tokens;

• Demand: people willing to buy.

The balance between demand and supply defined the token price.

24/104

What aspects to take into consideration with regard to Supply and Demand?

1. Supply Side: allocations, vesting period, emissions, and airdrops;

2. Demand Side: governance, token utility, and interest alignment.

What aspects to take into consideration with regard to Supply and Demand?

1. Supply Side: allocations, vesting period, emissions, and airdrops;

2. Demand Side: governance, token utility, and interest alignment.

25/104

1. Supply

• “Based on supply dynamics alone, how should I expect the price of a given token to behave?”

• “Will the token become more scarce, or is value likely to deteriorate via inflation?”.

1. Supply

• “Based on supply dynamics alone, how should I expect the price of a given token to behave?”

• “Will the token become more scarce, or is value likely to deteriorate via inflation?”.

26/104

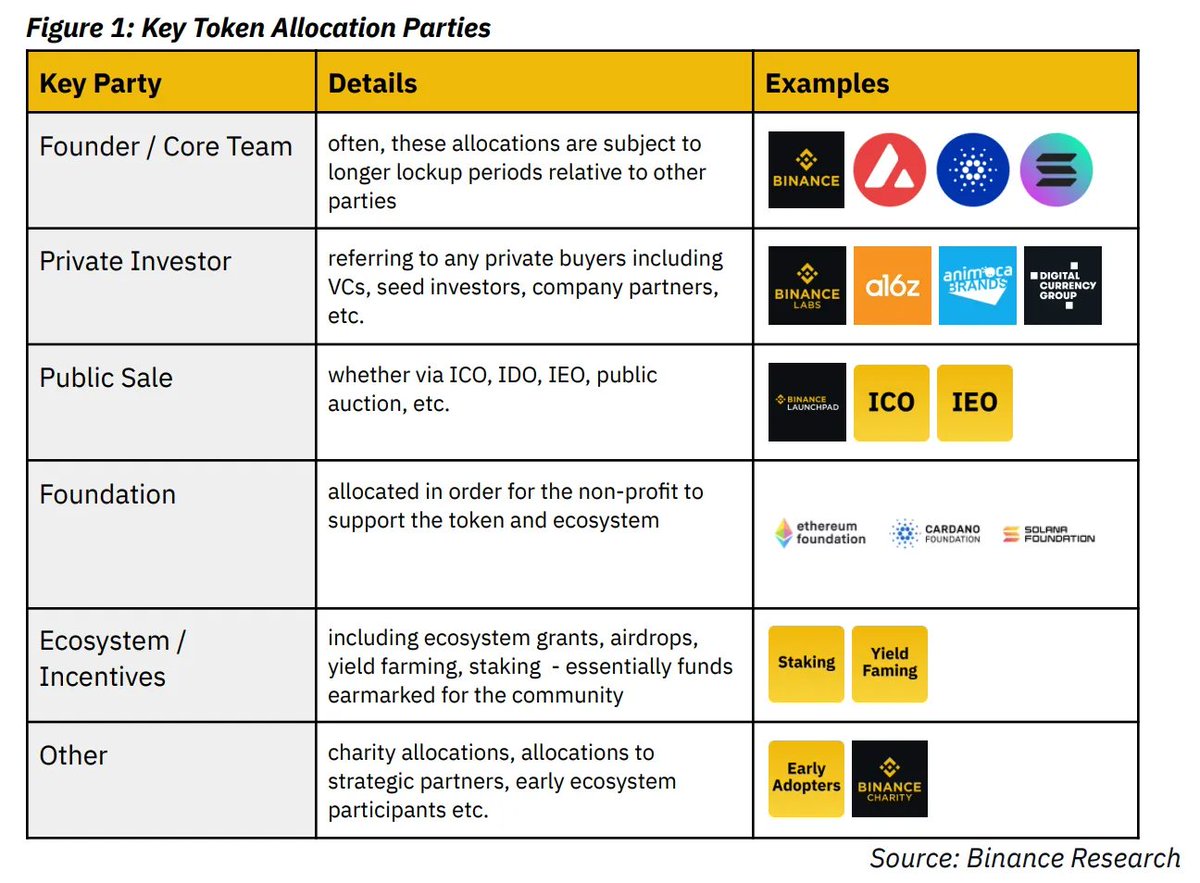

1.1 Allocations

How will the token supply allocate to the different parties?

This initial aspect is fundamental to align the incentives between key parties and determine the dynamics between early investors and users who will purchase the token on the secondary market.

1.1 Allocations

How will the token supply allocate to the different parties?

This initial aspect is fundamental to align the incentives between key parties and determine the dynamics between early investors and users who will purchase the token on the secondary market.

27/104

This poses initial questions to the team:

1. Should they raise VC capital knowing that this will introduce selling pressure when the token will be released in the market?

This poses initial questions to the team:

1. Should they raise VC capital knowing that this will introduce selling pressure when the token will be released in the market?

28/104

VC capital is not evil as such but introduces a different set of incentives whereby investors expect their equity to increase in value;

VC capital is not evil as such but introduces a different set of incentives whereby investors expect their equity to increase in value;

29/104

2. Should the team rather raise funds through an ICO-style raise or a public sale?

3. What % of the funds should be dedicated to the creation of ecosystem grants, airdrops or staking?

2. Should the team rather raise funds through an ICO-style raise or a public sale?

3. What % of the funds should be dedicated to the creation of ecosystem grants, airdrops or staking?

30/104

The study of allocations requires much thought and depends on the strategic direction the team chooses. Initially, most protocols minted their tokens through an ICO, IDO, IEO public sale, but this trend has been slowing down.

The study of allocations requires much thought and depends on the strategic direction the team chooses. Initially, most protocols minted their tokens through an ICO, IDO, IEO public sale, but this trend has been slowing down.

31/104

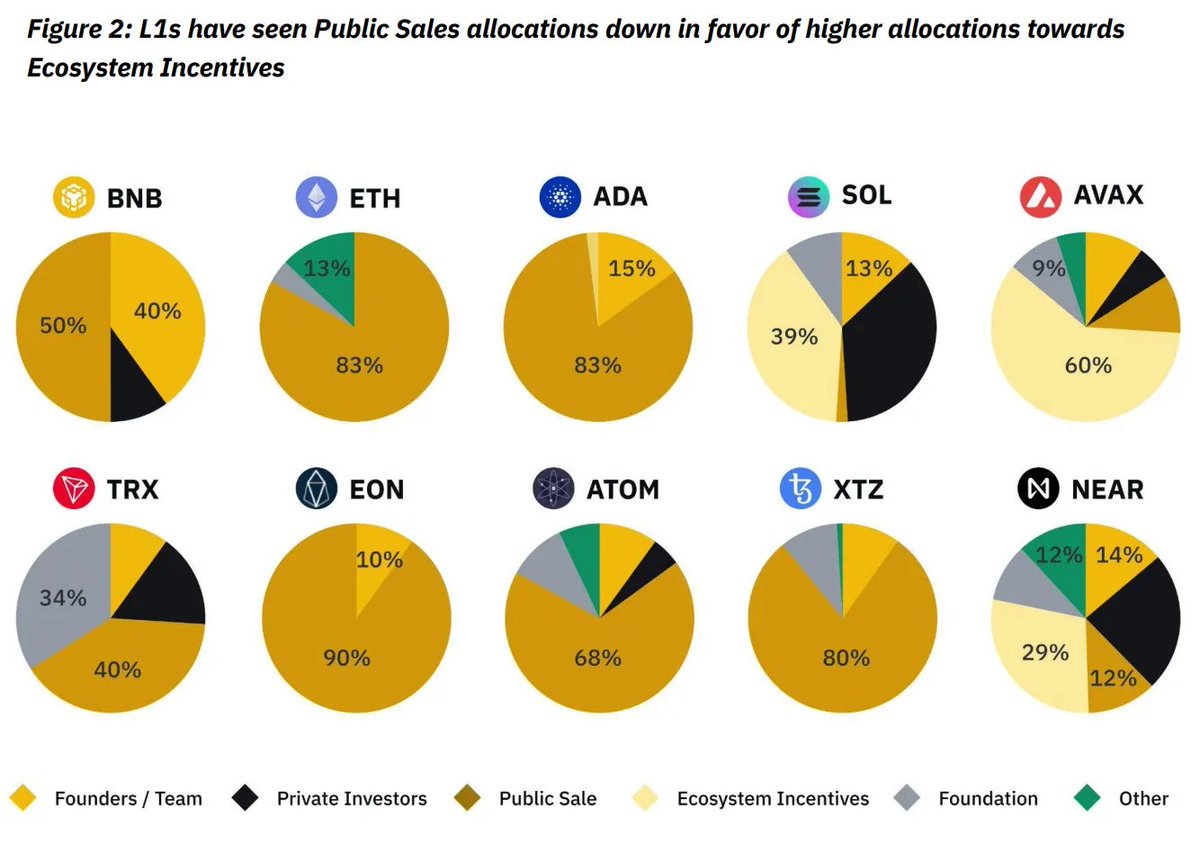

For instance, L2 protocols prefer to distribute tokens through airdrops rather than a public sale to ensure an initial critical mass of users for their product and to reward early adopters.

For instance, L2 protocols prefer to distribute tokens through airdrops rather than a public sale to ensure an initial critical mass of users for their product and to reward early adopters.

32/104

L1 blockchains have also seen “public sales allocations down in favor of higher allocations towards ecosystem incentives”.

L1 blockchains have also seen “public sales allocations down in favor of higher allocations towards ecosystem incentives”.

33/104

Why did they do so? If we think about the main objective of launching an L1 the answer becomes clear.

The value of an L1 is mostly derived from the ecosystem built on top of it.

Why did they do so? If we think about the main objective of launching an L1 the answer becomes clear.

The value of an L1 is mostly derived from the ecosystem built on top of it.

34/104

Since there are way too many blockchains, they have to fight for market share and tokens are being destined for more “value-accretive” purposes to incentivize market participants.

Since there are way too many blockchains, they have to fight for market share and tokens are being destined for more “value-accretive” purposes to incentivize market participants.

35/104

A successful mechanism to attract developers and users is through Ecosystem Incentives such as development grants, the creation of a foundation, and airdrops.

A successful mechanism to attract developers and users is through Ecosystem Incentives such as development grants, the creation of a foundation, and airdrops.

36/104

From the chart above we can also observe how this practice has consolidated throughout time, with latecomers such as Near, Avax, and Sol, relying on them more than Bnb, Ada, or Eth.

From the chart above we can also observe how this practice has consolidated throughout time, with latecomers such as Near, Avax, and Sol, relying on them more than Bnb, Ada, or Eth.

37/104

Some key aspects and risks to take into account with regard to Allocations are:

1. Centralization Risks:

a. Do the Founders and Investors control a disproportionate % of the total supply? For L1, the average is usually at ~32% average.

Some key aspects and risks to take into account with regard to Allocations are:

1. Centralization Risks:

a. Do the Founders and Investors control a disproportionate % of the total supply? For L1, the average is usually at ~32% average.

38/104

b. Who controls the ecosystem incentives or the Foundation?

2. Rewards:

a. What is the correct reward balance between developers and early adopters?

b. Should the focus be on grants, direct allocations or aidrop?

b. Who controls the ecosystem incentives or the Foundation?

2. Rewards:

a. What is the correct reward balance between developers and early adopters?

b. Should the focus be on grants, direct allocations or aidrop?

39/104

c. What is the correct balance between early rewards and future incentives?

c. What is the correct balance between early rewards and future incentives?

40/104

1.2 Vesting

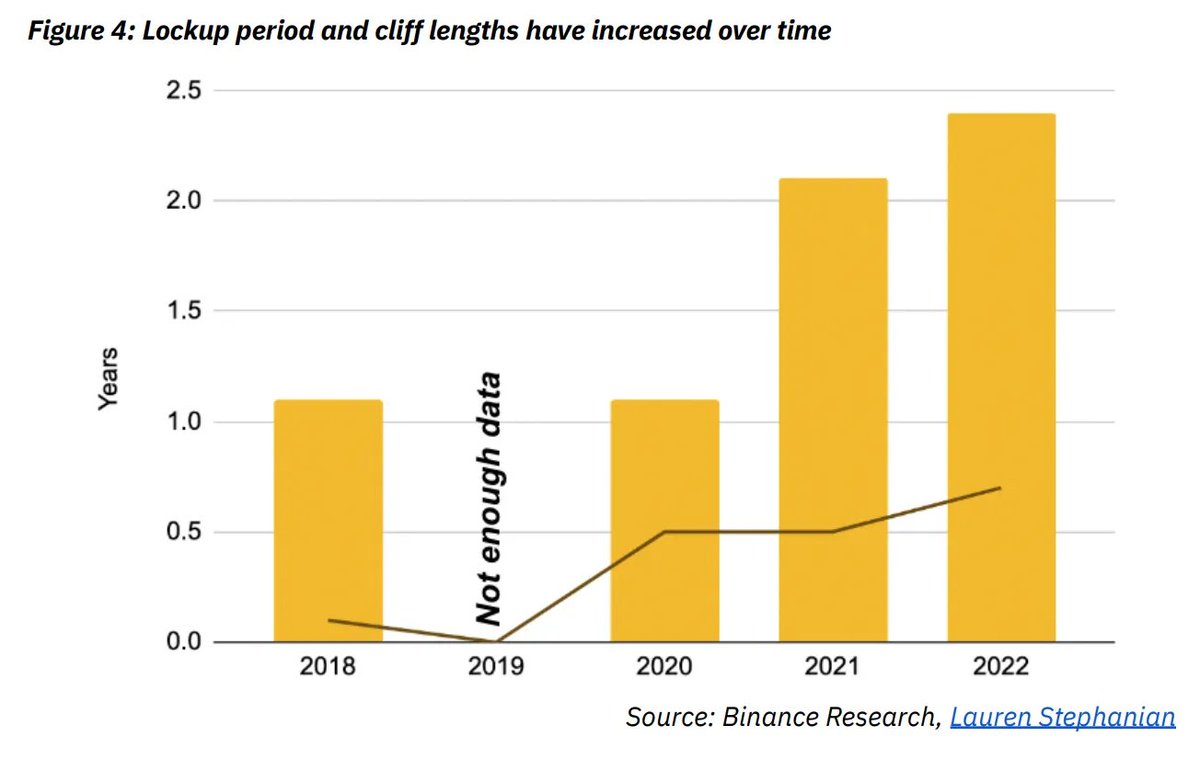

Most of the time, when investors participate in a token sale, they are subject to a vesting period, where the sale of the token is restricted.

1.2 Vesting

Most of the time, when investors participate in a token sale, they are subject to a vesting period, where the sale of the token is restricted.

41/104

The vesting schedule changes based on the different types of investors, VCs will have a longer schedule for instance, than public sale participants.

The vesting schedule changes based on the different types of investors, VCs will have a longer schedule for instance, than public sale participants.

42/104

Vesting can be:

1. Time-Based: for a determined period, with unlocking at established intervals;

2. Trigger-Based: after a determined event (e.g. mainnet release, exchange listing).

Vesting can be:

1. Time-Based: for a determined period, with unlocking at established intervals;

2. Trigger-Based: after a determined event (e.g. mainnet release, exchange listing).

43/104

Locking tokens is an important “incentivization tool to ensure that developer and insider motivations are aligned with those of token buyers” and to prevent large fluctuations in price.

Locking tokens is an important “incentivization tool to ensure that developer and insider motivations are aligned with those of token buyers” and to prevent large fluctuations in price.

44/104

If there would be no vesting, early investors would dump the token to secure gains as soon as it hits the market. They would have no incentive to hold.

If there would be no vesting, early investors would dump the token to secure gains as soon as it hits the market. They would have no incentive to hold.

45/104

Same for users, unfortunately, most of the retail investors and liquidity providers are mercenary capital, which moves where it is the most beneficial. They may join your L1 blockchain only to make sure to get their airdrops, and then move on to the next cow to milk.

Same for users, unfortunately, most of the retail investors and liquidity providers are mercenary capital, which moves where it is the most beneficial. They may join your L1 blockchain only to make sure to get their airdrops, and then move on to the next cow to milk.

46/104

To deal with this, projects have adapted as we can observe from the increase of lockup periods and cliff length by more than 100% from 2018 to 2022.

To deal with this, projects have adapted as we can observe from the increase of lockup periods and cliff length by more than 100% from 2018 to 2022.

47/104

The difficult efforts with regard to vesting are:

1. To make sure the lockup periods are balanced between the different groups of investors;

2. To ensure enough tokens are vested;

3. To avoid being targeted by mercenary capital.

The difficult efforts with regard to vesting are:

1. To make sure the lockup periods are balanced between the different groups of investors;

2. To ensure enough tokens are vested;

3. To avoid being targeted by mercenary capital.

48/104

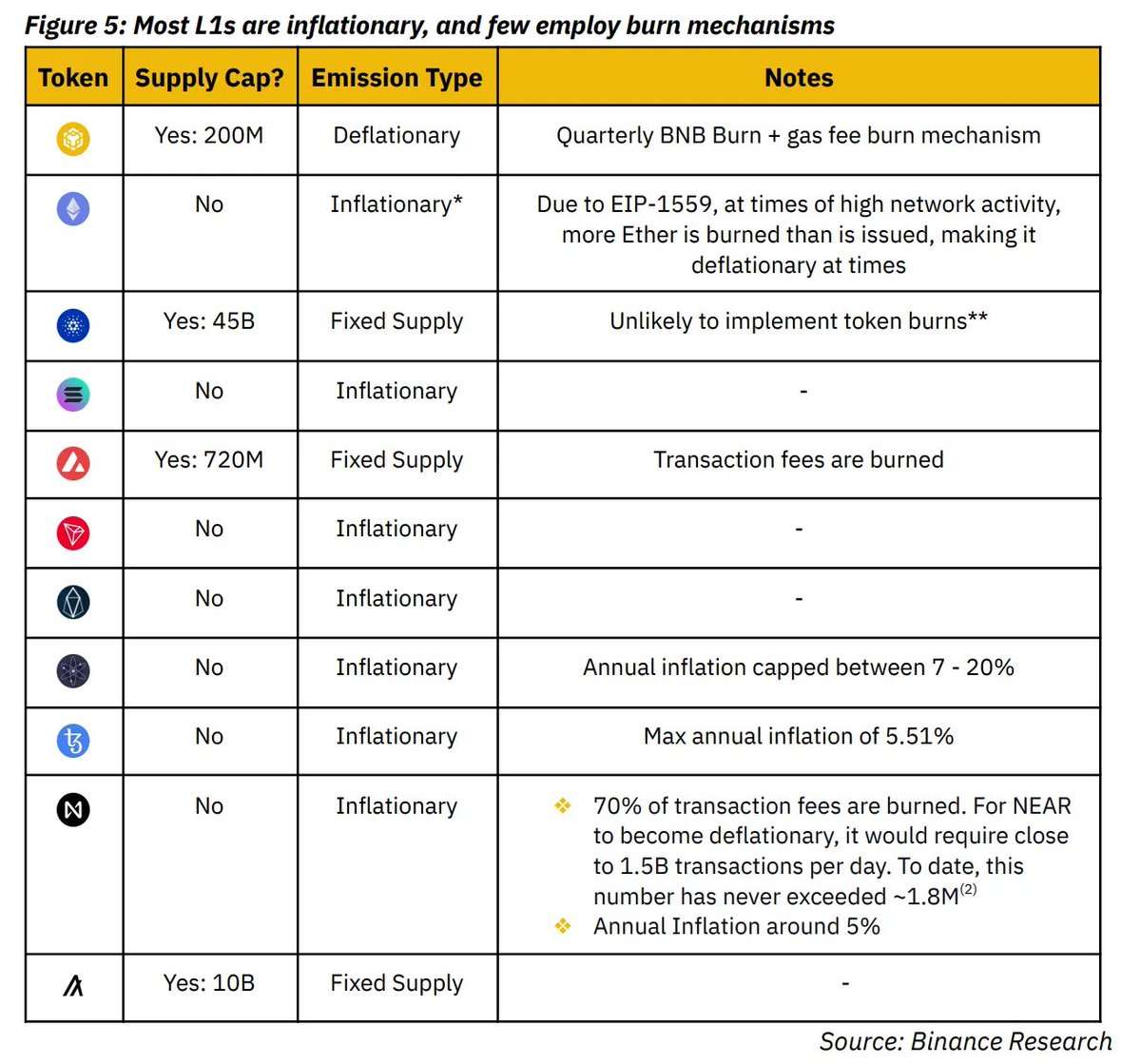

1.3 Emissions

Based on the rate of token emission, a token will be either inflationary or deflationary. Emissions directly impact the supply of a token and contribute to determining the selling pressure the protocol will face.

1.3 Emissions

Based on the rate of token emission, a token will be either inflationary or deflationary. Emissions directly impact the supply of a token and contribute to determining the selling pressure the protocol will face.

49/104

Notable mechanisms to reduce emissions include “burning" tokens as BNB does every quarter, or burning a percentage of the gas fee such as Ethereum does since POS.

Notable mechanisms to reduce emissions include “burning" tokens as BNB does every quarter, or burning a percentage of the gas fee such as Ethereum does since POS.

50/104

This contributes in turn to reducing emissions and selling pressure and makes the tokens deflationary.

This contributes in turn to reducing emissions and selling pressure and makes the tokens deflationary.

51/104

Why does every protocol aim to be deflationary?

> With increasing demand and a shrinking supply, the scarcity created and the resulting benefit to stakeholders is unquestionable.

Bitcoin is the perfect example of this argument.

Why does every protocol aim to be deflationary?

> With increasing demand and a shrinking supply, the scarcity created and the resulting benefit to stakeholders is unquestionable.

Bitcoin is the perfect example of this argument.

52/104

An inflationary token with a high annual deflation is in fact less attractive for investors, stakers, and liquidity providers.

An inflationary token with a high annual deflation is in fact less attractive for investors, stakers, and liquidity providers.

53/104

Users have to be mindful of emissions:

YES, you may be getting a 20% APY on your staked tokens. But what are the annual token emissions? You may even be losing money if their inflation is 25% for instance.

Users have to be mindful of emissions:

YES, you may be getting a 20% APY on your staked tokens. But what are the annual token emissions? You may even be losing money if their inflation is 25% for instance.

54/104

This is why protocols promising incredible APY are doomed to fail in the long term: they have to keep minting new tokens to reward stakers, but doing so increases the selling pressure.

This is why protocols promising incredible APY are doomed to fail in the long term: they have to keep minting new tokens to reward stakers, but doing so increases the selling pressure.

55/104

The price of the token depends on newcomers in the protocol, once this inflow stops, the token will free-fall.

The price of the token depends on newcomers in the protocol, once this inflow stops, the token will free-fall.

56/104

Nonetheless, emissions can be tweaked as a tool to incentivize users.

Nonetheless, emissions can be tweaked as a tool to incentivize users.

57/104

@PancakeSwap for instance, leveraged initially high emissions to attract an initial user base and reward liquidity providers, and then gradually slowed them down through the introduction of deflationary mechanisms.

@PancakeSwap for instance, leveraged initially high emissions to attract an initial user base and reward liquidity providers, and then gradually slowed them down through the introduction of deflationary mechanisms.

58/104

A useful metric that helps users to have a better understanding of the valuation of a token is the Fully Diluted Valuation (FDV).

A useful metric that helps users to have a better understanding of the valuation of a token is the Fully Diluted Valuation (FDV).

59/104

Compared to Market Capitalization, which only takes into account the circulating supply of a token, the FDV also includes the maximum supply, thus accounting for emissions.

Compared to Market Capitalization, which only takes into account the circulating supply of a token, the FDV also includes the maximum supply, thus accounting for emissions.

60/104

Some questions you can ask if a project has a high FDV:

> What does the scheduled release look like for the remaining coins? Will circulation double in a short time period, or is it a longer-term schedule? How much dilution is expected and how quickly?

Some questions you can ask if a project has a high FDV:

> What does the scheduled release look like for the remaining coins? Will circulation double in a short time period, or is it a longer-term schedule? How much dilution is expected and how quickly?

61/104

Your small cap token may have a MCAP of $1m, but with only 1% of their tokens circulating. The FDV is $100m, providing a much clearer idea of the real situation. And that’s why your 100x won’t happen.

Your small cap token may have a MCAP of $1m, but with only 1% of their tokens circulating. The FDV is $100m, providing a much clearer idea of the real situation. And that’s why your 100x won’t happen.

62/104

Ideally, a project should have a similar MCAP and FDV so that users would not be subject to extreme inflationary pressure and dilution.

Ideally, a project should have a similar MCAP and FDV so that users would not be subject to extreme inflationary pressure and dilution.

63/104

This is the case of Bitcoin, where after 10 years since its inception more than 90% of the total supply has been mined and is circulating.

This is the case of Bitcoin, where after 10 years since its inception more than 90% of the total supply has been mined and is circulating.

64/104

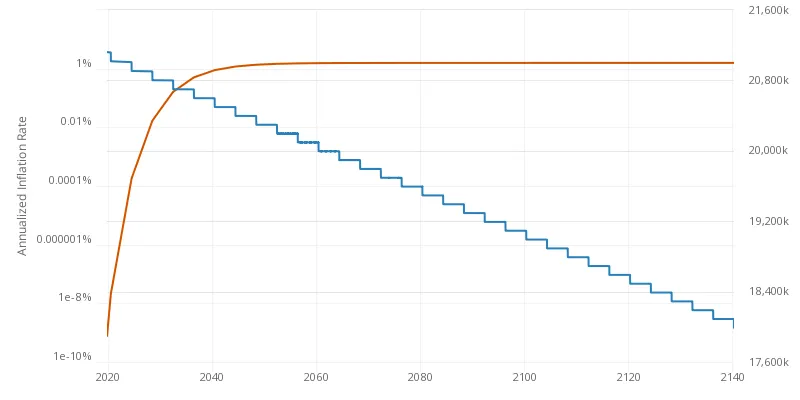

Bitcoin supply is fixed at 21 million and the halving mechanism ensures that every 4 years the amount of Bitcoin produced at each new block gets halved, reducing inflation.

Bitcoin supply is fixed at 21 million and the halving mechanism ensures that every 4 years the amount of Bitcoin produced at each new block gets halved, reducing inflation.

65/104

1.4 Airdrops

Airdrops are a useful tool to initially attract users but don’t contribute much as themselves to help retain them. Airdrops have experienced a revival, mostly propelled by L2 airdrops, notably Optimism and Arbitrum.

1.4 Airdrops

Airdrops are a useful tool to initially attract users but don’t contribute much as themselves to help retain them. Airdrops have experienced a revival, mostly propelled by L2 airdrops, notably Optimism and Arbitrum.

66/104

They are the most subject to mercenary capital and are frequently gamed by users trying to farm them.

> For example, 6.8% of the wallets participating in Optimism airdrops were flagged as Sybil attackers.

They are the most subject to mercenary capital and are frequently gamed by users trying to farm them.

> For example, 6.8% of the wallets participating in Optimism airdrops were flagged as Sybil attackers.

67/104

An interesting alternative to airdrops is lock drops, where airdrops are subject to a vesting period or to complete certain tasks, placing a focus on future engagement with the protocol, or a gamified airdrop, where users have and use the chain in order to qualify.

An interesting alternative to airdrops is lock drops, where airdrops are subject to a vesting period or to complete certain tasks, placing a focus on future engagement with the protocol, or a gamified airdrop, where users have and use the chain in order to qualify.

68/104

2. Demand

• “Are there incentives for users to drive demand or hold the token?”

• “What is the real utility of the token?”

• How can we align the incentives of the users with those of the protocol in a win-win situation?

2. Demand

• “Are there incentives for users to drive demand or hold the token?”

• “What is the real utility of the token?”

• How can we align the incentives of the users with those of the protocol in a win-win situation?

69/104

2.1 Governance

In most DAOs, governance rights are reserved for token holders.

This offers considerable utility to a token and contributes to driving demand.

2.1 Governance

In most DAOs, governance rights are reserved for token holders.

This offers considerable utility to a token and contributes to driving demand.

70/104

However, giving governance rights to token holders raises issues with regard to centralization and the proper way to weigh votes. If one token is one vote, then governance in decentralized protocols will be necessarily skewed towards big holders and whales.

However, giving governance rights to token holders raises issues with regard to centralization and the proper way to weigh votes. If one token is one vote, then governance in decentralized protocols will be necessarily skewed towards big holders and whales.

71/104

An example of this is what recently happened with Uniswap governance, where users found out that a16z controlled more than 4% of the total $UNI supply, a necessary quorum to pass governance proposals.

An example of this is what recently happened with Uniswap governance, where users found out that a16z controlled more than 4% of the total $UNI supply, a necessary quorum to pass governance proposals.

72/104

“Transparent and healthy governance can offer a lot of utility and drive the demand for a project”, but getting the model right is fundamental to safeguard decentralization and participation.

“Transparent and healthy governance can offer a lot of utility and drive the demand for a project”, but getting the model right is fundamental to safeguard decentralization and participation.

73/104

Other aspects that have to be carefully assessed include:

1. How much voting power does the team or initial investors have?

Other aspects that have to be carefully assessed include:

1. How much voting power does the team or initial investors have?

74/104

2. Arguably the one-coin-one-vote weakens the decentralized aspects of DAOs, how can they ensure the necessary checks and balances are put in place?

2. Arguably the one-coin-one-vote weakens the decentralized aspects of DAOs, how can they ensure the necessary checks and balances are put in place?

75/104

Most of the times protocols adopt “a gradual approach to decentralization with governance power being distributed out as community rewards are distributed”.

Most of the times protocols adopt “a gradual approach to decentralization with governance power being distributed out as community rewards are distributed”.

76/104

Both these governance examples are still limited; the next step forward in decentralized governance will be to shift rewards to users who contribute positively to the protocol to ensure value alignment.

Both these governance examples are still limited; the next step forward in decentralized governance will be to shift rewards to users who contribute positively to the protocol to ensure value alignment.

77/104

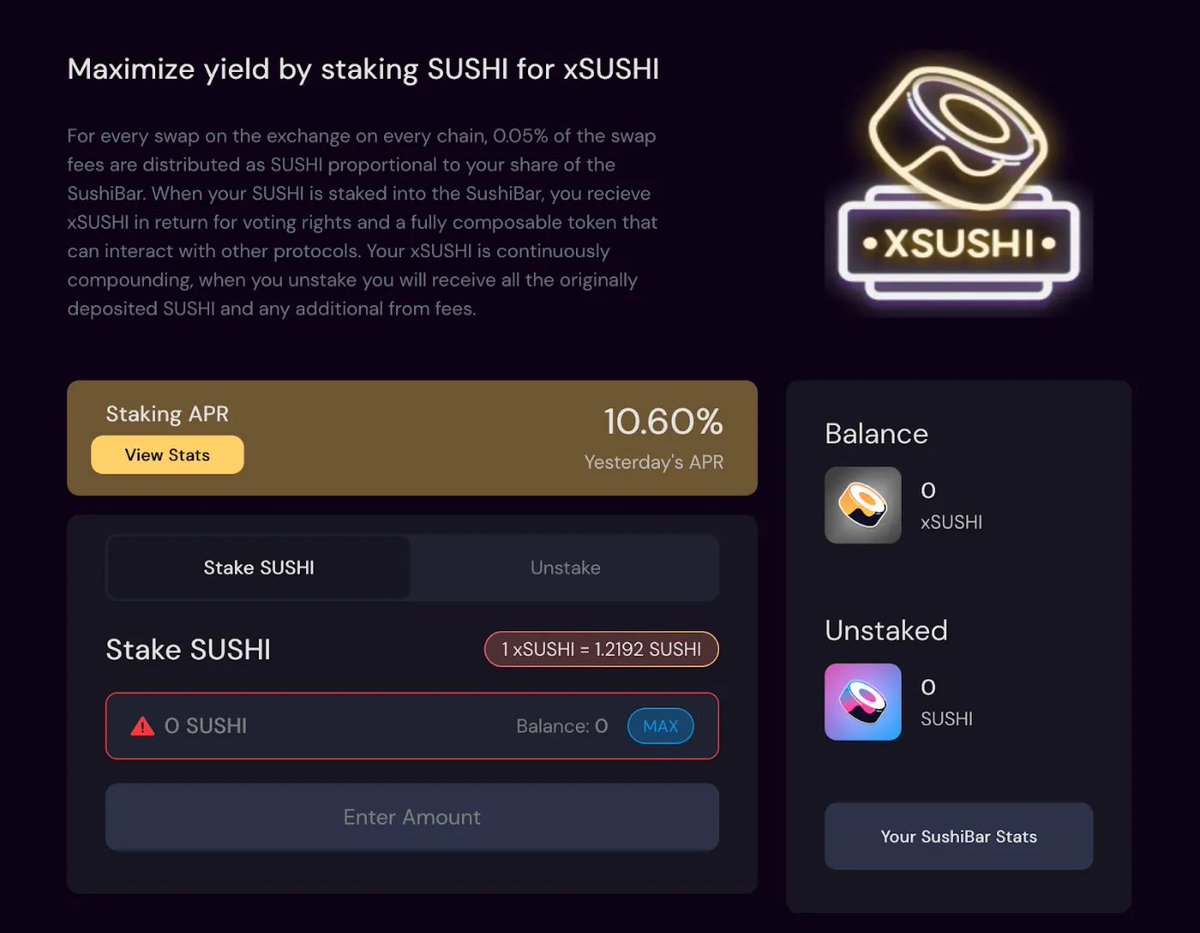

Another example of a token giving governance rights is xSUSHI, from @SushiSwap . Users can stake $SUSHI for xSUSHI and get voting rights and a % of the protocol earnings.

Another example of a token giving governance rights is xSUSHI, from @SushiSwap . Users can stake $SUSHI for xSUSHI and get voting rights and a % of the protocol earnings.

78/104

2.2 Utility

Ideally, a token utility would be the main driver of organic demand.

There is no better way to incentivize users to hold your tokens than attaching real utility to them.

2.2 Utility

Ideally, a token utility would be the main driver of organic demand.

There is no better way to incentivize users to hold your tokens than attaching real utility to them.

79/104

Tokens can serve multiple purposes, bringing utility to the token:

1. Right: e.g. governance rights, such as $UNI, xSUSHI;

2. Value Exchange: allowing for buying and selling as well as rewards for work and commitment;

Tokens can serve multiple purposes, bringing utility to the token:

1. Right: e.g. governance rights, such as $UNI, xSUSHI;

2. Value Exchange: allowing for buying and selling as well as rewards for work and commitment;

80/104

3. Toll: skin in the game (e.g. paying a fee to run smart contracts);

4. Function: allowing users to join a network, or be incentivized to participate in a game;

5. Currency: a form of currency by being a store of value and a medium of exchange;

3. Toll: skin in the game (e.g. paying a fee to run smart contracts);

4. Function: allowing users to join a network, or be incentivized to participate in a game;

5. Currency: a form of currency by being a store of value and a medium of exchange;

81/104

6. Earnings: revenue sharing through token incentives.

6. Earnings: revenue sharing through token incentives.

82/104

Trust also plays a fundamental role in token utility: token holders trust the token issuer to be able to enforce their rights and can be defined “as quantifiable representations of decentralized and disintermediated trust.

sciencedirect.com

Trust also plays a fundamental role in token utility: token holders trust the token issuer to be able to enforce their rights and can be defined “as quantifiable representations of decentralized and disintermediated trust.

sciencedirect.com

83/104

2.3 Interest Alignment

Good tokenomics have the ability to compensate individuals proportionally to the value they create. In fact, the right incentives can stimulate participation and encourage growth in a project.

2.3 Interest Alignment

Good tokenomics have the ability to compensate individuals proportionally to the value they create. In fact, the right incentives can stimulate participation and encourage growth in a project.

84/104

a. Revenue Sharing: can be done on-chain or off-chain, and involves airdropping token rewards, or buying tokens in the open market with the purpose of burning them.

a. Revenue Sharing: can be done on-chain or off-chain, and involves airdropping token rewards, or buying tokens in the open market with the purpose of burning them.

85/104

Let’s have a look at how different DEXes distribute their fees:

Let’s have a look at how different DEXes distribute their fees:

86/104

Notoriously Uniswap does not share fees with token holders. On the other hand, Curve shares a much higher % of their fees with token holders. The data is not recent and as such might have changed, but this chart is useful in showing the different approaches used by DEXs.

Notoriously Uniswap does not share fees with token holders. On the other hand, Curve shares a much higher % of their fees with token holders. The data is not recent and as such might have changed, but this chart is useful in showing the different approaches used by DEXs.

87/104

b. Vote Escrow: the “ve” model transforms liquidity providers into long-term stakeholders, by granting increased rewards and governance rights to those who lock the token for a longer time.

b. Vote Escrow: the “ve” model transforms liquidity providers into long-term stakeholders, by granting increased rewards and governance rights to those who lock the token for a longer time.

88/104

veTokenomics provide a new way for protocols to grow TVL without inflating the circulating supply. In practice, the lockup period allows the protocol to buy time to grow.

veTokenomics provide a new way for protocols to grow TVL without inflating the circulating supply. In practice, the lockup period allows the protocol to buy time to grow.

89/104

This rewards long-term-oriented participants while providing different rewards to token holders, based on their commitment.

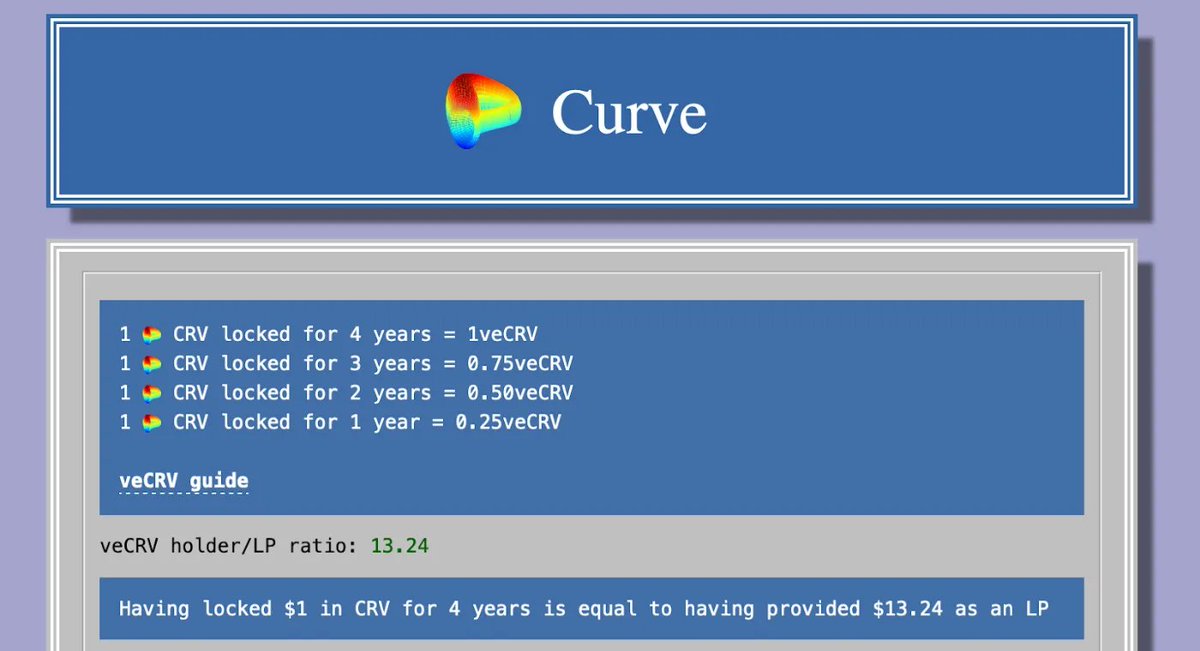

For example, in the veTokenomics of @CurveFinance :

1. The longer you lock, the more vote-escrowed CRV (veCRV) you get;

This rewards long-term-oriented participants while providing different rewards to token holders, based on their commitment.

For example, in the veTokenomics of @CurveFinance :

1. The longer you lock, the more vote-escrowed CRV (veCRV) you get;

90/104

1. Locking is irreversible, and tokens are not transferrable;

2. CRV lockers earn a % of the protocol revenue.

1. Locking is irreversible, and tokens are not transferrable;

2. CRV lockers earn a % of the protocol revenue.

91/104

Dual-Token Model

Some projects might introduce a two-token model to separate the functionalities of the different tokens.

Dual-Token Model

Some projects might introduce a two-token model to separate the functionalities of the different tokens.

92/104

In most cases of a dual-token model, we have:

1. Utility token: offering utility across the network (e.g. pay for transactions);

2. Governance token: guides the strategic direction of the project and contributes to development.

In most cases of a dual-token model, we have:

1. Utility token: offering utility across the network (e.g. pay for transactions);

2. Governance token: guides the strategic direction of the project and contributes to development.

93/104

This model in particular is leveraged by gaming protocols: a two-token model can help separate the governance and the in-game token. If they only had one token, it would be badly impacted by in-game transactions, leading to price impact and speculation.

This model in particular is leveraged by gaming protocols: a two-token model can help separate the governance and the in-game token. If they only had one token, it would be badly impacted by in-game transactions, leading to price impact and speculation.

94/104

Other examples include GMX and GLP, Axie infinity AXS, and SLP. In fact, one of the key aspects of a two-token system is that it allows the protocol to reward users without diluting the governance token.

Other examples include GMX and GLP, Axie infinity AXS, and SLP. In fact, one of the key aspects of a two-token system is that it allows the protocol to reward users without diluting the governance token.

95/104

Nonetheless introducing a two-model system also lead to increased complexity and the need to balance mechanisms between the two.

Nonetheless introducing a two-model system also lead to increased complexity and the need to balance mechanisms between the two.

96/104

Also, the team will have to be mindful of how much “utility” each token produces for users, as it will be less concentrated than a single token and thus be carefully assessed.

Also, the team will have to be mindful of how much “utility” each token produces for users, as it will be less concentrated than a single token and thus be carefully assessed.

97/104

Food for Thought:

1. A good tokenomics fosters long-term growth rather than short-term gains;

2. Being able to assess the different aspects involved in tokenomics is a fundamental skill to evaluate projects;

Food for Thought:

1. A good tokenomics fosters long-term growth rather than short-term gains;

2. Being able to assess the different aspects involved in tokenomics is a fundamental skill to evaluate projects;

98/104

3. Every small choice that the founding team takes when architecting a new protocol has to be carefully evaluated in relation to so many dynamics, and its consequences have to be assessed in relation to the impact they have on the whole system;

3. Every small choice that the founding team takes when architecting a new protocol has to be carefully evaluated in relation to so many dynamics, and its consequences have to be assessed in relation to the impact they have on the whole system;

99/104

Ethereum decided to have tx fees in their own token > to have token utility and make sure that transacting on the network has a minimal cost > to avoid the network being spammed > making block space expensive and creating a whole new economy about transactions.

Ethereum decided to have tx fees in their own token > to have token utility and make sure that transacting on the network has a minimal cost > to avoid the network being spammed > making block space expensive and creating a whole new economy about transactions.

100/104

Building a protocol requires the same patience as finding a balance between different stones.

Building a protocol requires the same patience as finding a balance between different stones.

101/104

Making sure all users are incentivized proportionally, that the token has utility and benefits from protocol value accrual, that investors will not dump, and that the team will have enough funding to be motivated and sustain developments is not an easy feature.

Making sure all users are incentivized proportionally, that the token has utility and benefits from protocol value accrual, that investors will not dump, and that the team will have enough funding to be motivated and sustain developments is not an easy feature.

102/104

Different protocols will need to tweak demand and supply dynamics in order to ensure long-term growth and protocol sustainability.

Different protocols will need to tweak demand and supply dynamics in order to ensure long-term growth and protocol sustainability.

103/104

Different consensus mechanisms will have a different set of actors participating: a Proof-of-work network has to find a balance between miners, developers, and users, while a Proof-of-stake system will have different dynamics involving users staking.

Different consensus mechanisms will have a different set of actors participating: a Proof-of-work network has to find a balance between miners, developers, and users, while a Proof-of-stake system will have different dynamics involving users staking.

104/104

What should be incentivized?

Food for thought.

What should be incentivized?

Food for thought.

I hope you've found this thread helpful.

Follow me @francescoglt for more.

Like/Retweet the first tweet below if you can:

Follow me @francescoglt for more.

Like/Retweet the first tweet below if you can:

A full article will be published tomorrow on my Substack for better reading.

Full article on my Substack!

fraxcesco.substack.com

fraxcesco.substack.com

Loading suggestions...