Even after 75 years of independence and over 10 government schemes, why is having a roof over one’s head still a distant dream for many Indians?

Despite being a basic necessity, owning a house is a luxury for too many.

A thread on India's affordable housing crisis!

Despite being a basic necessity, owning a house is a luxury for too many.

A thread on India's affordable housing crisis!

In India, affordable urban housing is a major problem because house prices are 6-10 times the prices in some comparable Asian economies.

The estimated housing shortage in India

- 2012: ~1.9 crore

- 2018: 2.9 crore

This is a rise of 54% in 6 years. Households from the Economically Weaker Section category (earning ~₹20k/month) get affected by this shortage the most.

- 2012: ~1.9 crore

- 2018: 2.9 crore

This is a rise of 54% in 6 years. Households from the Economically Weaker Section category (earning ~₹20k/month) get affected by this shortage the most.

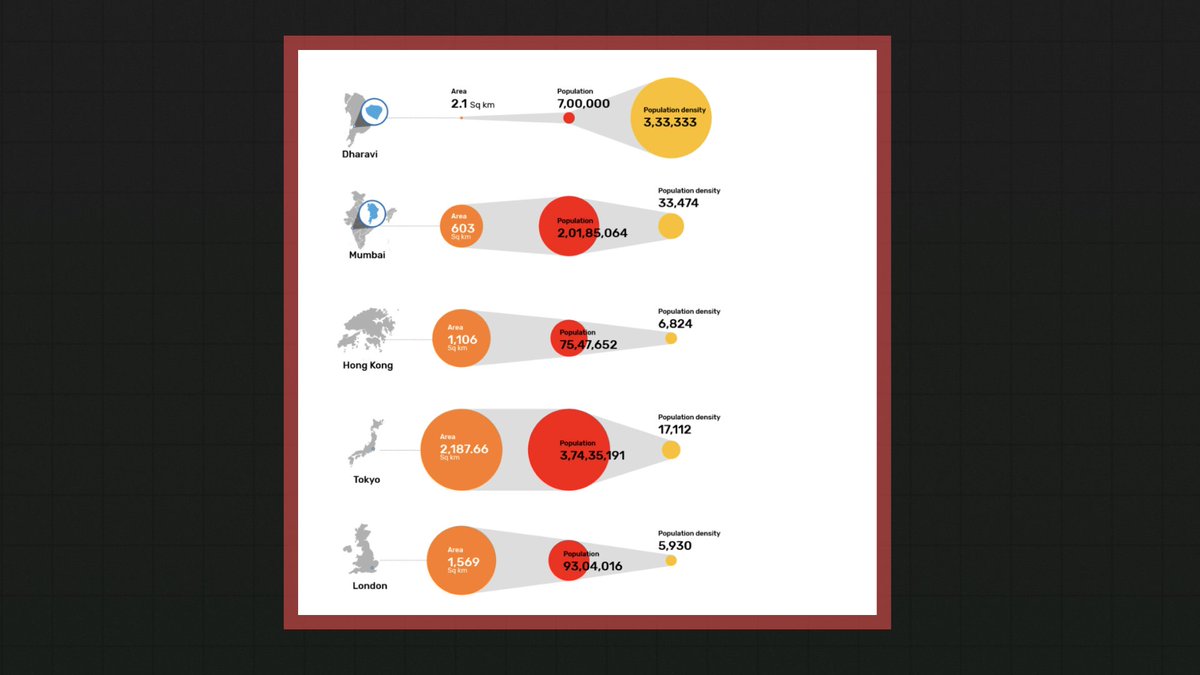

Even today, over 24 lakh people in urban areas do not have shelter, and in major cities, at least 7 crore people live in slums.

In Dharavi, out of a population of 10 lakh people, only 100 households own land or tenements.

In Dharavi, out of a population of 10 lakh people, only 100 households own land or tenements.

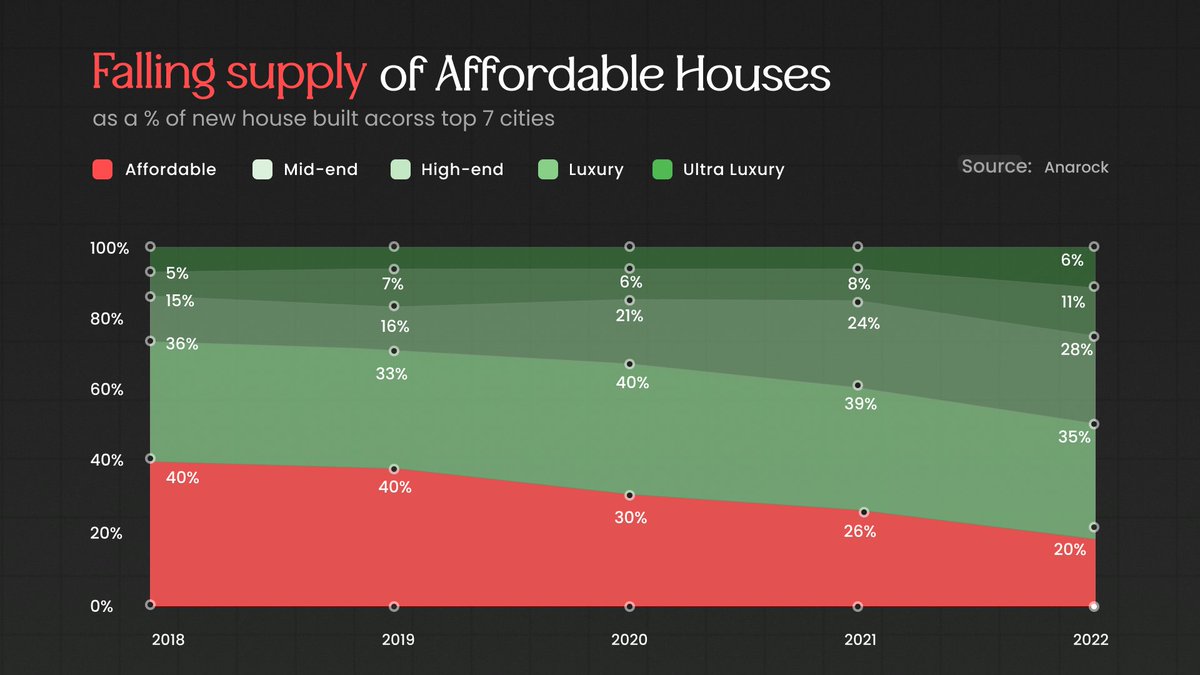

But shockingly, most of the new houses built are beyond the reach of low-income groups.

Out of 3.58 lakh houses built in the top 7 cities in 2022, only 20% were affordable houses.

Out of 3.58 lakh houses built in the top 7 cities in 2022, only 20% were affordable houses.

The supply is falling because of uncertainty for the developers.

Customers in the affordable segment are very price-sensitive.

Thus developers find it difficult to pass on any commodity (steel and cement) price rise. If they do, they fear losing out on the customers.

Customers in the affordable segment are very price-sensitive.

Thus developers find it difficult to pass on any commodity (steel and cement) price rise. If they do, they fear losing out on the customers.

Developers who build mid and luxury houses do not have to fear the same.

Also, the profit margin in the affordable segment ranges from about 8-10%, significantly lower than the mid and luxury segment.

Also, the profit margin in the affordable segment ranges from about 8-10%, significantly lower than the mid and luxury segment.

This is why medium and large developers build just 9% and 1% of affordable houses. Whereas small, informal developers build over 90% of them.

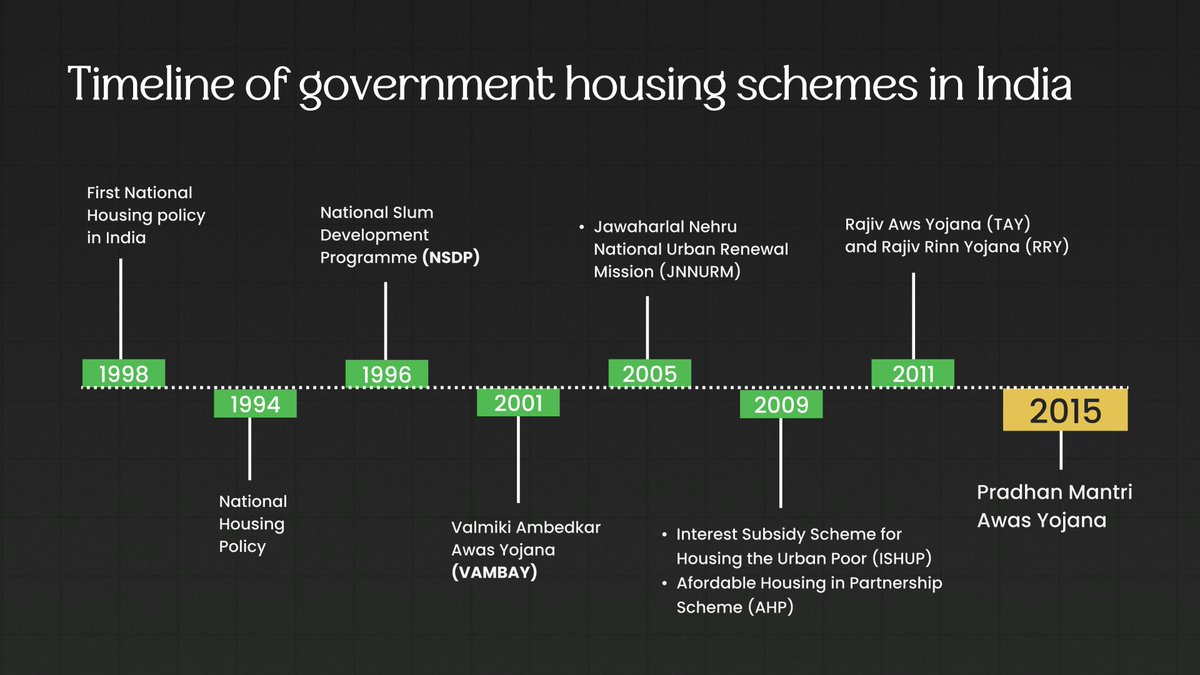

In 2015, the government introduced Pradhan Mantri Awas Yojana - Urban (PMAY-U) to solve the affordable housing puzzle.

This scheme was so big that it engulfed all such previous housing initiatives.

But did it actually work?

This scheme was so big that it engulfed all such previous housing initiatives.

But did it actually work?

The scheme had two objectives:

- build more houses (supply side)

- make those houses affordable (demand-side)

- build more houses (supply side)

- make those houses affordable (demand-side)

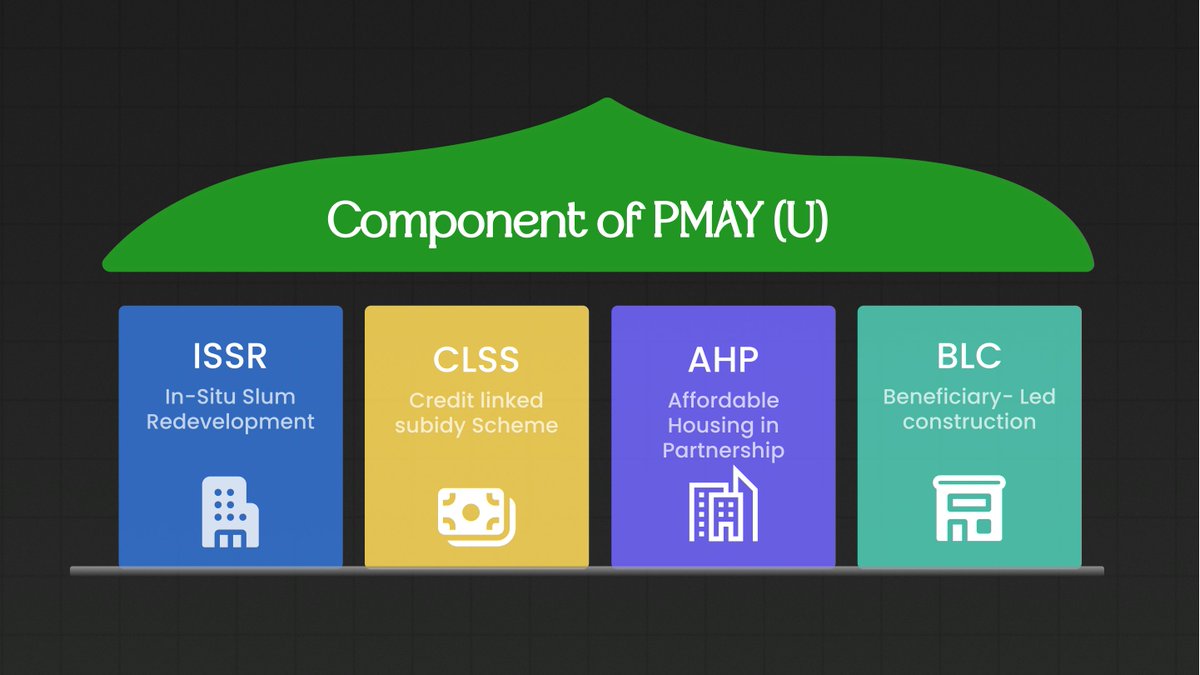

Supply-side measures:

1) Affordable Housing-in-Partnership (AHP): Developers that construct homes for low-income groups are given a ₹1.5 L subsidy per house.

1) Affordable Housing-in-Partnership (AHP): Developers that construct homes for low-income groups are given a ₹1.5 L subsidy per house.

Typically, an affordable house sells for ₹40 L, and assuming a 10% margin, the developer’s profit would be ₹4 L. And a ₹1.5 L subsidy on this is a very significant incentive.

2) In-situ Slum Redevelopment (ISSR):

Developers replace existing slums with apartment buildings on the same land.

Slum households receive free housing on their land.

Private developers complete the project and acquire the slum land in return.

This is a win-win for both.

Developers replace existing slums with apartment buildings on the same land.

Slum households receive free housing on their land.

Private developers complete the project and acquire the slum land in return.

This is a win-win for both.

Demand-side measures:

3) Beneficiary-Led Construction (BLC): Low-income households get a ₹1.5 lakh subsidy to build or improve their own homes.

4) Credit-Linked Subsidy Scheme (CLSS): An interest subsidy of 6.5% is provided for 20 years on housing loans.

3) Beneficiary-Led Construction (BLC): Low-income households get a ₹1.5 lakh subsidy to build or improve their own homes.

4) Credit-Linked Subsidy Scheme (CLSS): An interest subsidy of 6.5% is provided for 20 years on housing loans.

Banks shy away from lending to low-income households due to the lack of formal income.

When they do, the rate would have to be much higher (~15%+) than a standard 9% home loan to account for risk.

When they do, the rate would have to be much higher (~15%+) than a standard 9% home loan to account for risk.

With the CLSS subsidising 6.5% of the interest, EMIs become affordable for customers. And banks who normally would not lend to these customers would also feel comfortable lending.

But there were problems with all of them.

But there were problems with all of them.

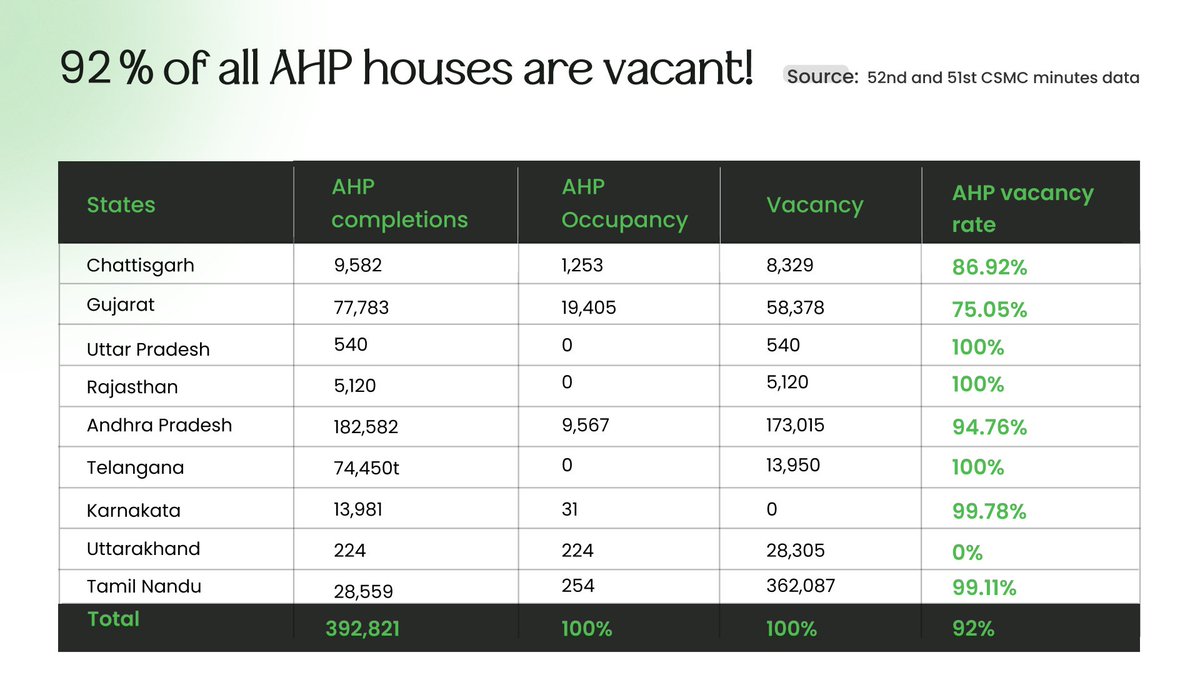

Due to high land costs, developers typically build AHP houses far from the city. But for the people, it does not make sense to live on the city's outskirts, far away from their workplace.

This explains why 92% of all AHP houses built are vacant.

This explains why 92% of all AHP houses built are vacant.

In-situ Slum Redevelopment scheme may sound promising - free housing for slums, developers acquire the land in return.

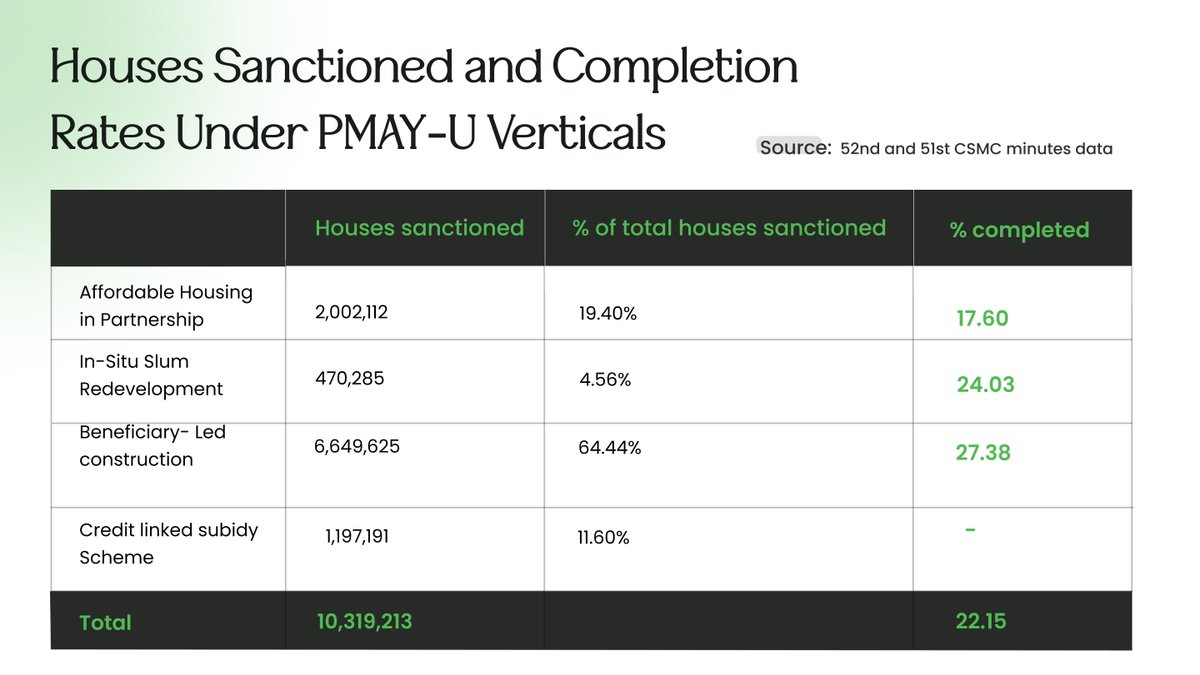

But it only accounts for a mere 4.5% of total sanctions under PMAY-U.

But it only accounts for a mere 4.5% of total sanctions under PMAY-U.

This is because this scheme only covers areas “notified” as a slum by the government.

But in India, 59% of urban slums are “non-notified”. Thus the benefits of these schemes simply don’t apply here.

But in India, 59% of urban slums are “non-notified”. Thus the benefits of these schemes simply don’t apply here.

The problem with Beneficiary-Led Construction:

To qualify for BLC, one must own some land. This leaves many ineligible for these housing schemes. And since the fund is transferred directly to the beneficiary, the problem of misusing the funds for other purposes is always there.

To qualify for BLC, one must own some land. This leaves many ineligible for these housing schemes. And since the fund is transferred directly to the beneficiary, the problem of misusing the funds for other purposes is always there.

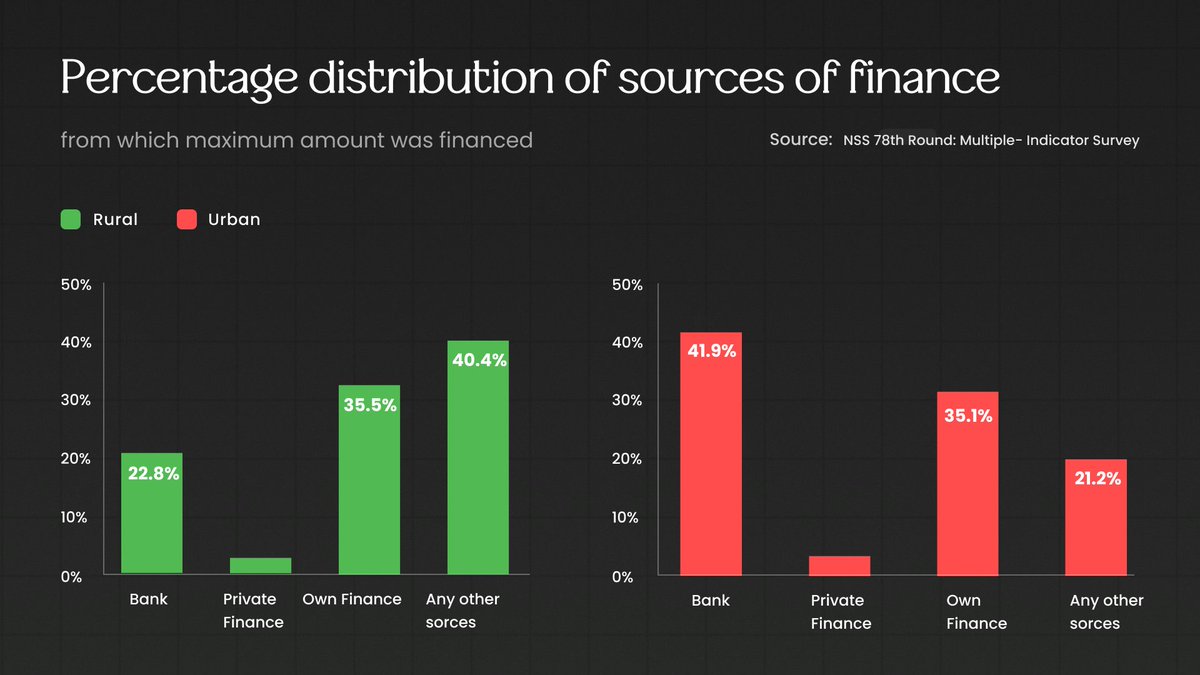

The Credit-Linked Subsidy Scheme (CLSS) subsidy also did little to expand the reach of housing loans.

Since low-income households tend to have informal sources of income, they struggle to access formal housing finance. So, they are simply unable to benefit from CLSS.

Since low-income households tend to have informal sources of income, they struggle to access formal housing finance. So, they are simply unable to benefit from CLSS.

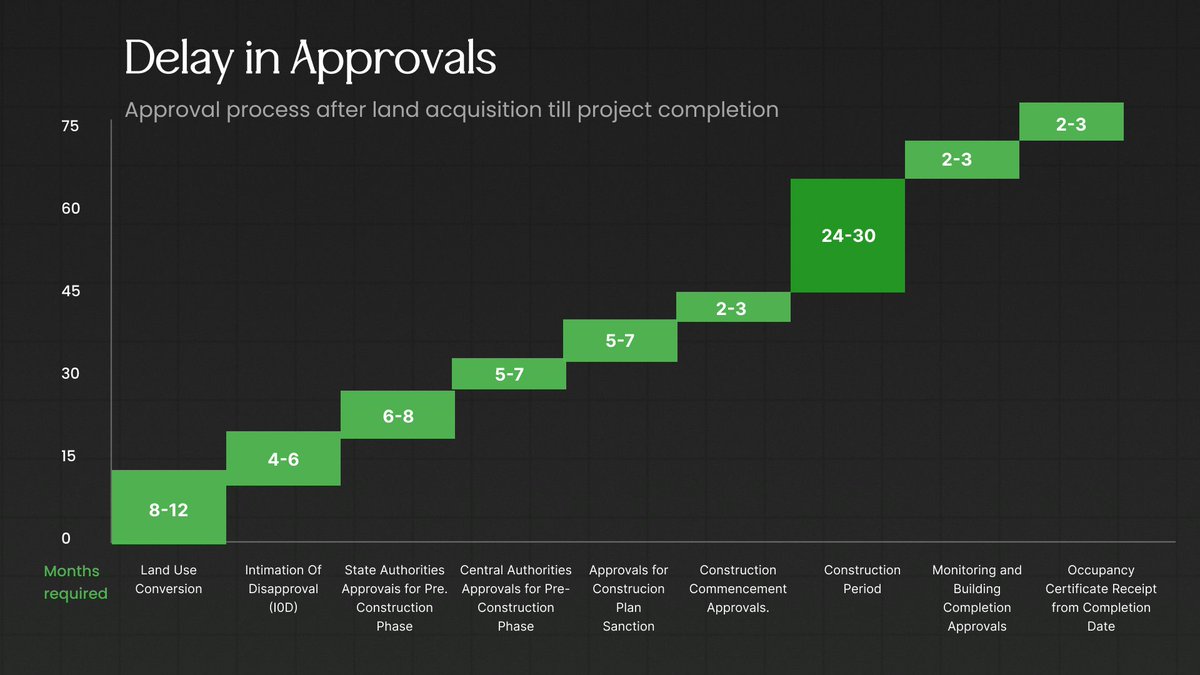

Apart from the above, statutory clearances are another major hurdle.

- Over 20-30 clearances are needed for each housing project, that too from multiple authorities.

- Even to start construction, it takes ~2 years to obtain all the approvals from the date of land acquisition.

- Over 20-30 clearances are needed for each housing project, that too from multiple authorities.

- Even to start construction, it takes ~2 years to obtain all the approvals from the date of land acquisition.

And since this is a price-sensitive segment, any delay in the completion of the project adds uncertainty for the developer. The price of raw materials can increase, the borrowing cost can go up, and the buyer can refuse to buy the property.

Owning a home is an emotional milestone for anyone.

And while PMAY has its share of problems to overcome, the government is aggressively taking new steps to make this dream of every Indian come true.

And while PMAY has its share of problems to overcome, the government is aggressively taking new steps to make this dream of every Indian come true.

Here are a few notable ones:

1) Reduction in GST

GST applicable on affordable housing is just 1%, whereas it is charged 5% on projects other than affordable housing units.

1) Reduction in GST

GST applicable on affordable housing is just 1%, whereas it is charged 5% on projects other than affordable housing units.

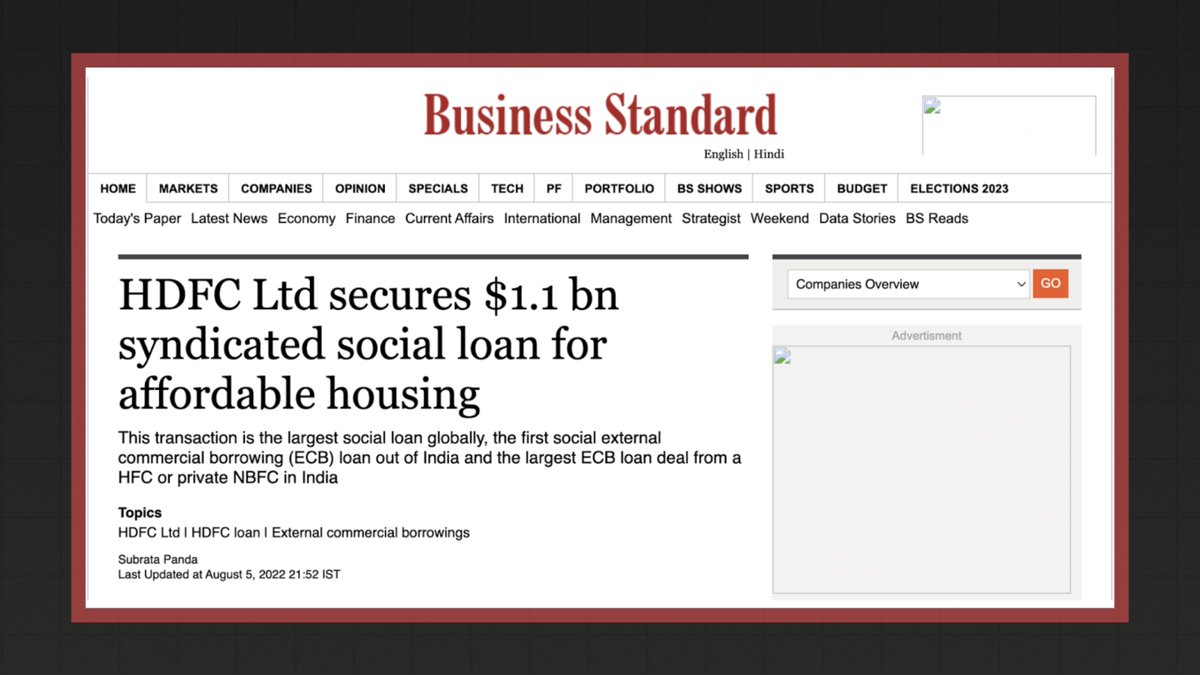

2) External Commercial Borrowings (ECBs)

This helps in lowering interest costs for developers and ensuring better capital availability.

HDFC recently took a $1.1 billion loan for affordable housing, making it the largest ECB loan deal from a housing finance company in India.

This helps in lowering interest costs for developers and ensuring better capital availability.

HDFC recently took a $1.1 billion loan for affordable housing, making it the largest ECB loan deal from a housing finance company in India.

3) Tax exemptions:

- 150% of capital expenditure on affordable housing is exempted from tax under section 35AD, Income Tax Act.

- 100% tax deduction on profits for construction of affordable housing projects under section 80-IBA till March 2021.

- 150% of capital expenditure on affordable housing is exempted from tax under section 35AD, Income Tax Act.

- 100% tax deduction on profits for construction of affordable housing projects under section 80-IBA till March 2021.

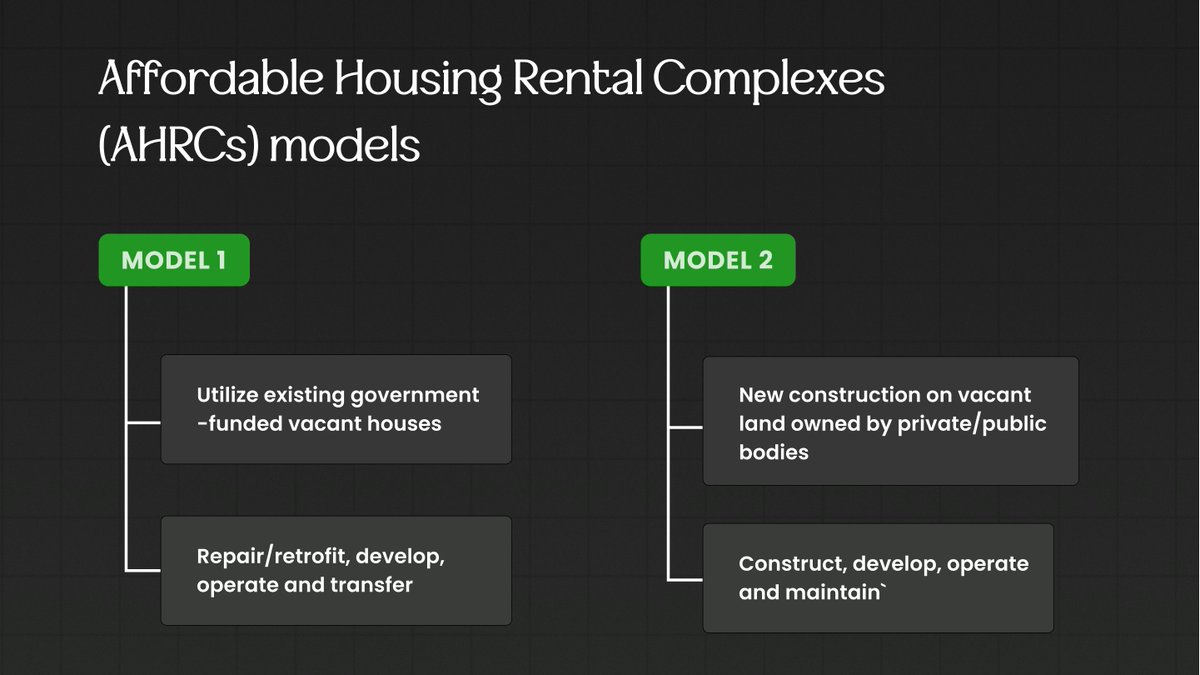

4) Affordable Rental Housing Complex (ARHCs)

This scheme was launched in June 2020 under PMAY. It provides rental housing for poor urban households at affordable rates.

It has two models:

This scheme was launched in June 2020 under PMAY. It provides rental housing for poor urban households at affordable rates.

It has two models:

Model 1:

Vacant houses of previous government schemes are converted into rental complexes. There are ~88,000 such houses available across 13 states/UTs in India.

Vacant houses of previous government schemes are converted into rental complexes. There are ~88,000 such houses available across 13 states/UTs in India.

Model 2:

Many businesses have a parcel of land vacant on their sites/factories. This model incentivises employers to build housing units for the workers on these lands.

This benefits both the employers as well as the workers.

Many businesses have a parcel of land vacant on their sites/factories. This model incentivises employers to build housing units for the workers on these lands.

This benefits both the employers as well as the workers.

The workers get decent housing near their workplace, which increases productivity and efficiency.

The employers earn a steady revenue stream and get tax exemption on any gains from these units.

The employers earn a steady revenue stream and get tax exemption on any gains from these units.

If all of this picks up well, the housing industry will generate 13% of India’s GDP by 2025.

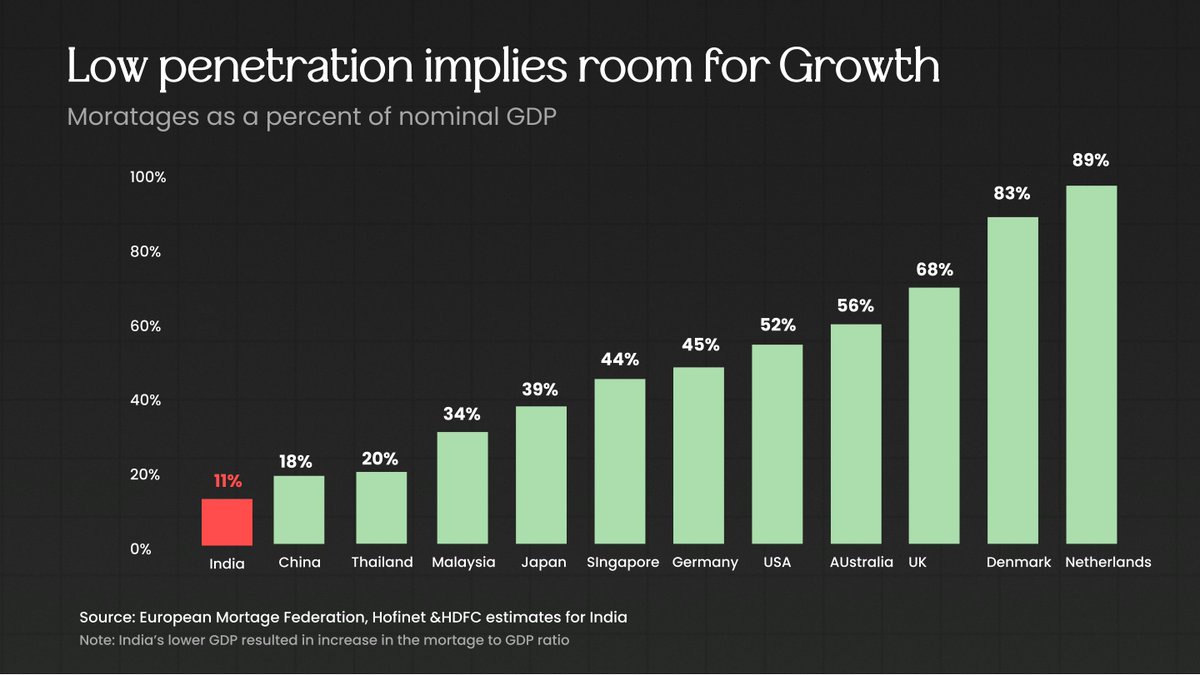

Also, given that mortgage to GDP is just 11% in India and a mere 4% in the affordable segment, there is massive room for HFC growth in India.

Also, given that mortgage to GDP is just 11% in India and a mere 4% in the affordable segment, there is massive room for HFC growth in India.

With this growth, the dream of escaping the slums and living a better life can become a reality for many people.

The government’s focus on the ‘Housing for All’ mission will ensure steady support to this sector, thus pushing it higher.

The government’s focus on the ‘Housing for All’ mission will ensure steady support to this sector, thus pushing it higher.

Loading suggestions...