Some of my clients at times say that I sound biased towards the health insurance products offered by HDFC Ergo. In my mind, hell ya ! I am positively biased as it is a question of my / my client's life. Thought to create a thread about it showing my biases. Pls RT for spread

It is the world of copy cats. If a product comes up with good features, others will quickly copy it. Copying T&Cs of a policy doesn't make a policy inherently strong vs other. Some facts from IRDAI's annual reports help to see this better.

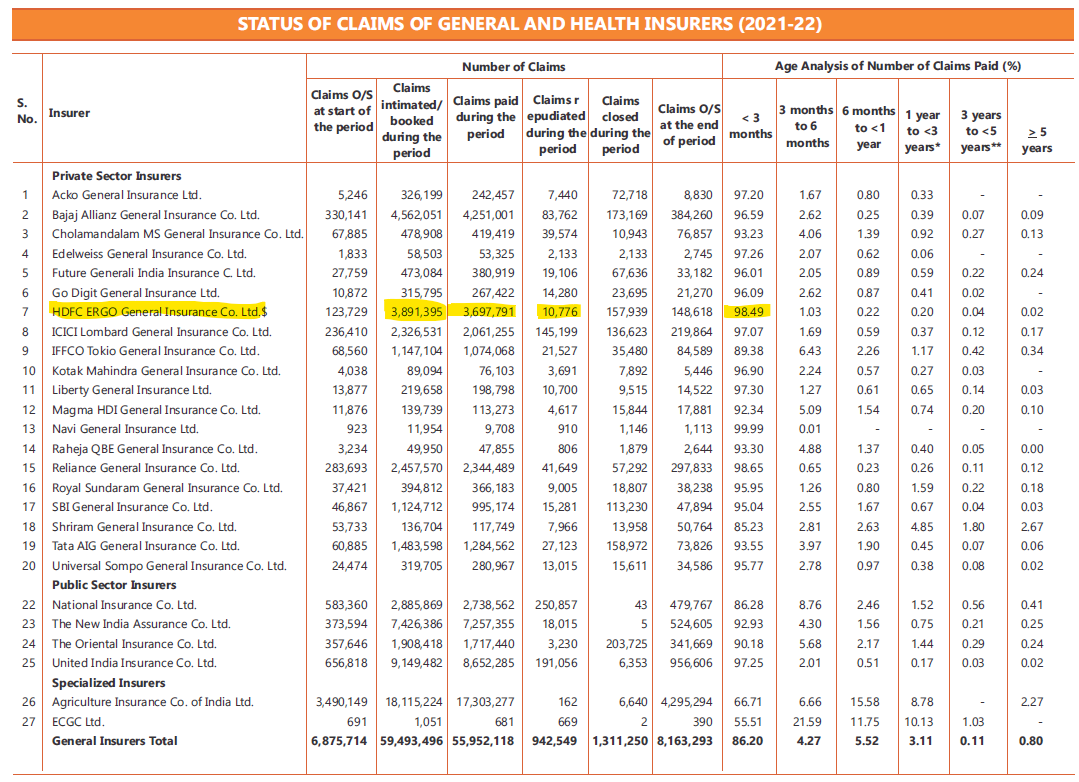

The status of claims received and settled across insurers. The biggies out there are Bajaj, HDFC, ICICI and then the PSUs.

HDFC settled 98.49% claims within 3 months.

A little misused section could be 'Claims Repudiated during the period' where the claim is rejected on T&C basis

HDFC settled 98.49% claims within 3 months.

A little misused section could be 'Claims Repudiated during the period' where the claim is rejected on T&C basis

It could take a legal battle to get a claim Repudiated into a normal category.

HDFC has lowest % claims under this area - 0.27% of total claim. Other comparables

ICICI - 6%

Bajaj - 1.8%

New India - 0.25% closest to HDFC, but their T&C of policies is an eye wash.

HDFC has lowest % claims under this area - 0.27% of total claim. Other comparables

ICICI - 6%

Bajaj - 1.8%

New India - 0.25% closest to HDFC, but their T&C of policies is an eye wash.

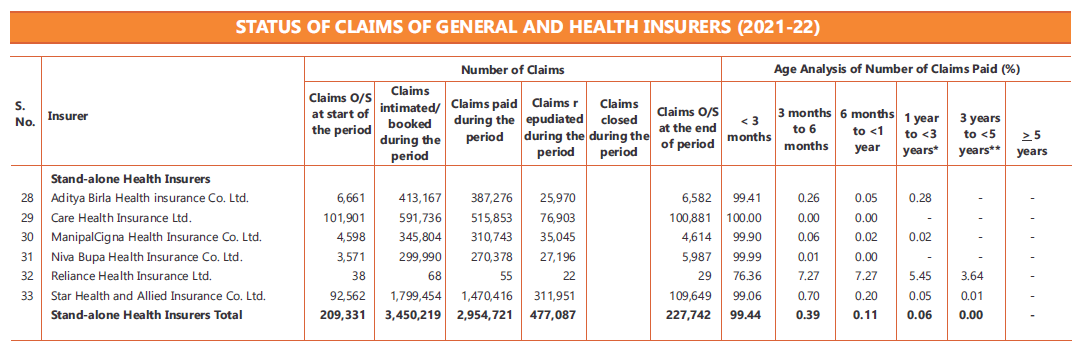

But Hey - where are those most hyped & sold (*mis) products of stand alone providers. See list below.

I roll my eyes to see a 100% claims paid ratio being typed for Care. But they repudiated 13% of claims.

Star repudiated 17% claims. Niva at 9% levels.

I roll my eyes to see a 100% claims paid ratio being typed for Care. But they repudiated 13% of claims.

Star repudiated 17% claims. Niva at 9% levels.

Could these insurers reject their claims citing 'Repudiations' and then showcase a rosy 100% Claims being settled. Talking to clients, these insurers are taking their customers for a ride. But still sadly, most of these are being heavily marketed & Sold.

Lets now take a rain check and check my biases towards HDFC.

HDFC recd 38L claims and repudiated 10K.

Star recd 18L claims & repudiated 3L

Care 6L vs 77K

Niva 3L vs 27K

HDFC paid 10x more claims and rejected 2.7x less claims vs Niva. Ratios even better vs others.

HDFC recd 38L claims and repudiated 10K.

Star recd 18L claims & repudiated 3L

Care 6L vs 77K

Niva 3L vs 27K

HDFC paid 10x more claims and rejected 2.7x less claims vs Niva. Ratios even better vs others.

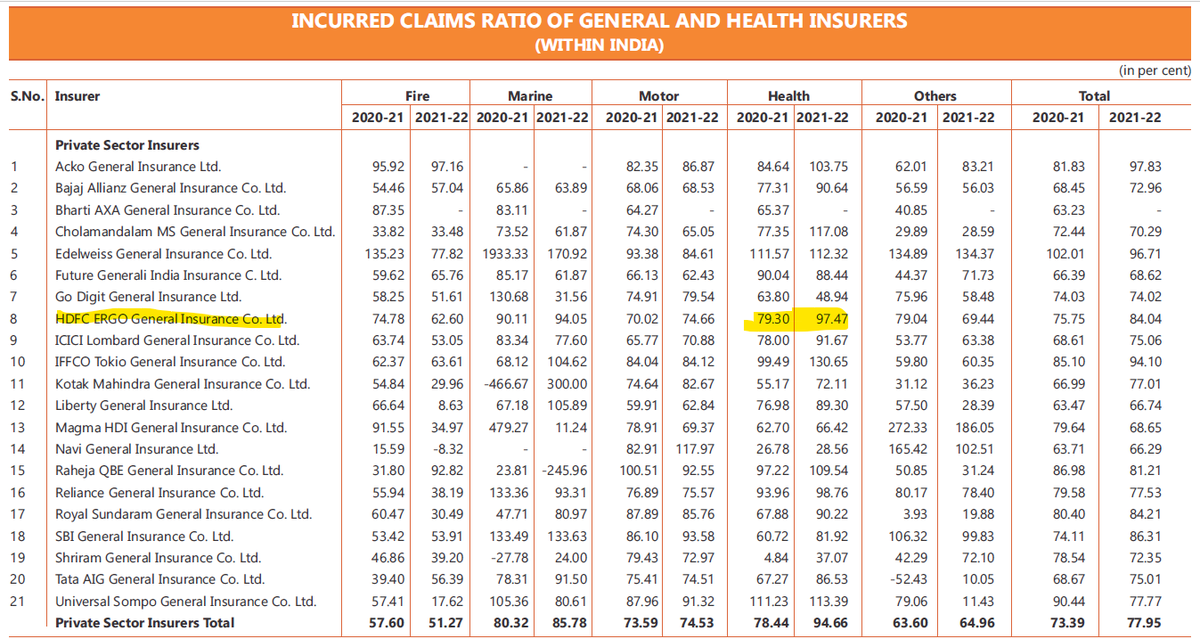

Next objective metric - Incurred Claim Ratio. This is the ratio of claims paid vs premiums collected. It is gives visibility of the sustainability of insurer. If your insurance Co is not collecting sufficient premiums to cover its cost (claims), you may see rough patches later.

I would want my insurer to make health profits, i.e. it should price the premiums at a competitive level to cover the cost of claims + take some profits home. If this ratio is above 100, that means Insurer is making loses (paying more claims than it earns). Bad news.

If ICR is between 50-90, it is good. I prefer in mid 70-80 ranges. Any number closer to 50 and lower, could mean

1. Insurer is rejecting claims

2. Pricing its product higher (diff in competitive markets)

So it is more 1 rather than 2.

1. Insurer is rejecting claims

2. Pricing its product higher (diff in competitive markets)

So it is more 1 rather than 2.

2021-22 report would have made most of the insurers bleed as they would have been paying claims through their nose owing to COVID claims. To get back to healthy levels, they would increase premiums. I remember HDFC was first one to increase premiums in 2022

The image below shows how ICR ratios of General insurers faired in 2021-22. HDFC was healthy at 79 in 2020-21, but then spiked upto 2021-22 to 97%. This was a harbinger of increasing premiums for a sane insurer.

Other Biggies too had similar outcomes.

Other Biggies too had similar outcomes.

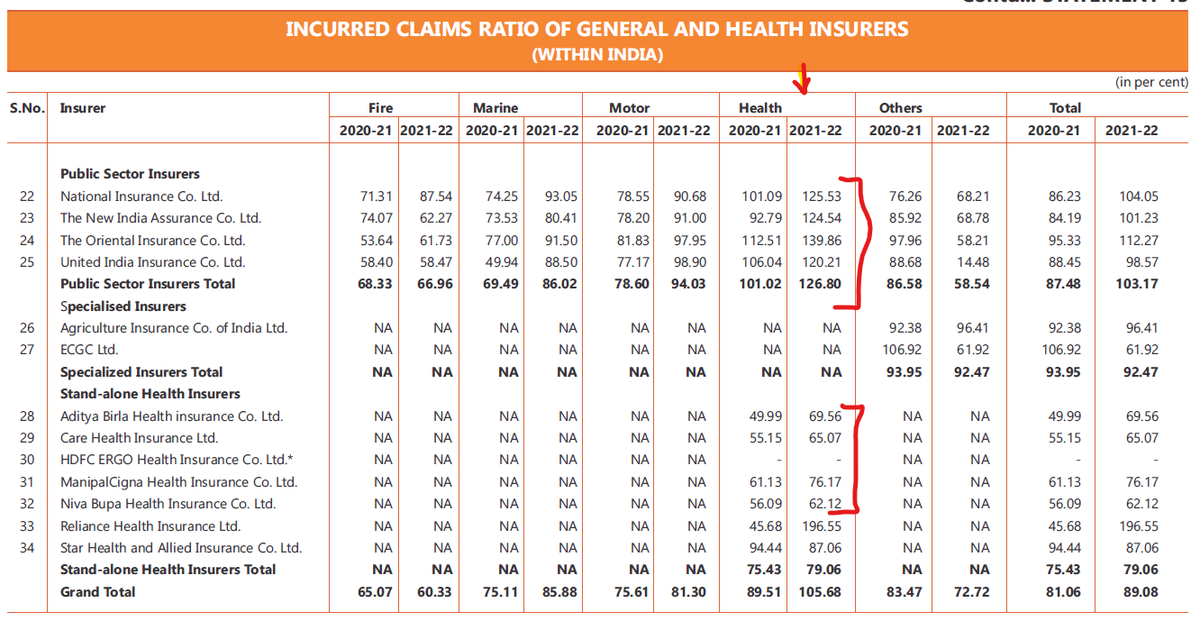

Lets look at how their other stand alone & PSU insurers faired.

PSU insurers were deep in red - above 100%. Paying more and pricing cheap. Signs of approaching risk on sustainability. How long can this continue. End of the day, the tax payer money gets burnt here.

PSU insurers were deep in red - above 100%. Paying more and pricing cheap. Signs of approaching risk on sustainability. How long can this continue. End of the day, the tax payer money gets burnt here.

But what about the Others - Care, Star, Niva & Manipal

Their ICRs sound like super. When their bigger counterparts were close to 100 in 2021-22, they are enjoying sub 70% ICR. Reading this in conjuction with their claims repudiation, this joins up the story a bit.

Their ICRs sound like super. When their bigger counterparts were close to 100 in 2021-22, they are enjoying sub 70% ICR. Reading this in conjuction with their claims repudiation, this joins up the story a bit.

The Claims repudiation for them tells us that they were 'repudiating' good part of the claims. Claim is a cost. Their cost went down just enough to cover their premiums. They didn't increase their premiums to allow for more costs or priced themselves too cheap.

I have been comparing the premiums of these insurers vs the Biggies. The Biggies ideally should enjoy economies of scale and hence be able to price their premiums lower. But in most cases their premiums are higher than the Stand alone insurers by a wide margin.

This makes me think - are the biggies not aware of what the market rates should be ? Or are the stand alone (Care / Star / Niva / etc.) are pricing themselves too low to grab market share. Unfortunately in Health insurance, lower premiums will pinch customers with rejections.

The study of ICR vs Claims details vs my awareness of Health insurance products in the industry, their terms and my personal experience of handling client claims make me believe that :

1. You can not undercut in Health insurance and maintain your claims. It will burn your Books.

1. You can not undercut in Health insurance and maintain your claims. It will burn your Books.

2. To preserve your Books, you may repudiate claims, in other words your clients will face claim rejections

3. If you price your products at a optimal level, you will loose market share.

4. In short run clients will benefit with reduced premium, it is a long term trap.

3. If you price your products at a optimal level, you will loose market share.

4. In short run clients will benefit with reduced premium, it is a long term trap.

SO looking into all these details again, I feel confident - yes I m biased. I tell my clients what I will do with my own life. I will not go down the quality route when it comes to life covers. I will not be penny wise pound foolish

What do U think? Views respected & appreciated.

What do U think? Views respected & appreciated.

@BeshakIN - a trusted Insurance well wisher in the Industry.

Loading suggestions...