1/ François Rochon recently released Giverny Capital's 2022 Annual Letter

It was once again refreshing after a tough year in the stock market, and the podium of errors was pretty interesting

🧵 with some highlights

It was once again refreshing after a tough year in the stock market, and the podium of errors was pretty interesting

🧵 with some highlights

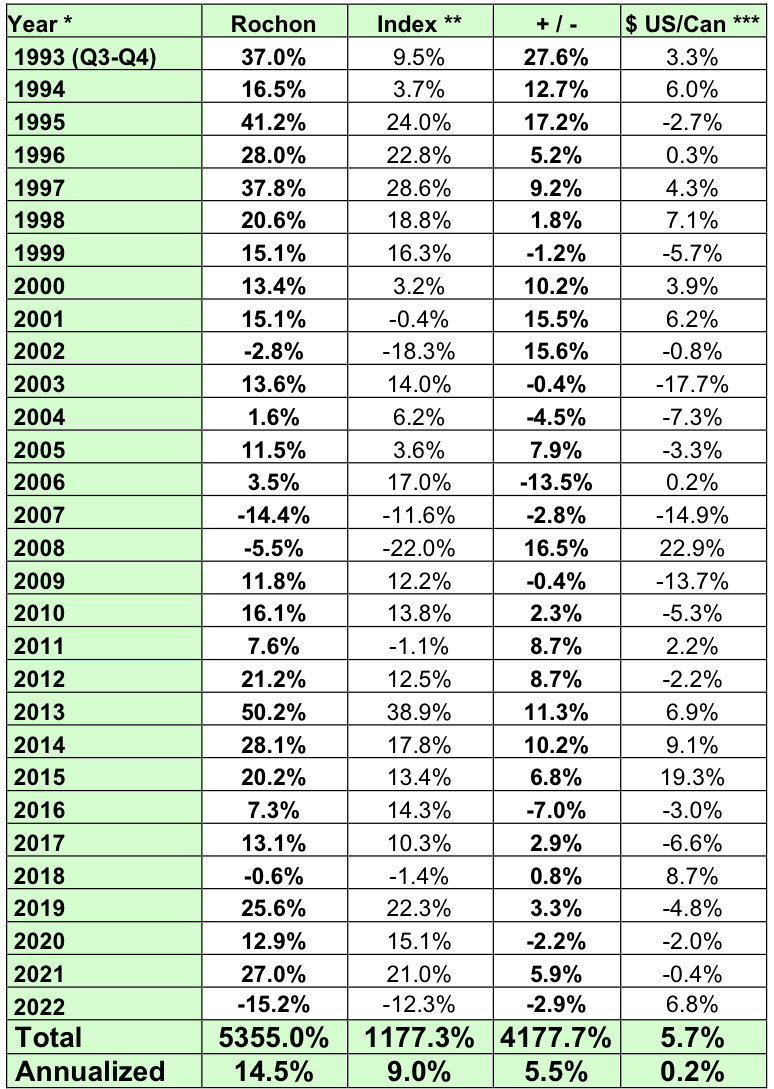

2/ The Rochon Global Portfolio was down 15.2% in 2022, its worst year on record. It was Giverny's second down year since 2008 and its 4th down year overall (30 years)

Since 1993, Giverny has compounded at a CAGR of 14.5%, leading to a total return of 5355%:

Since 1993, Giverny has compounded at a CAGR of 14.5%, leading to a total return of 5355%:

3/ 2022 performance enjoyed a 4.6% tailwind from currency (as it's reported in CAD). This said, currency has "only" been a 0.2% annual tailwind during the 30 years.

Many investors over-obsess with currency (which they should do if they invest ST) but LT its impact is low

Many investors over-obsess with currency (which they should do if they invest ST) but LT its impact is low

4/ Of course, the above applies to relatively strong currencies. If someone invests in emerging markets with extremely volatile currencies then currency risk should definitely be a consideration imho

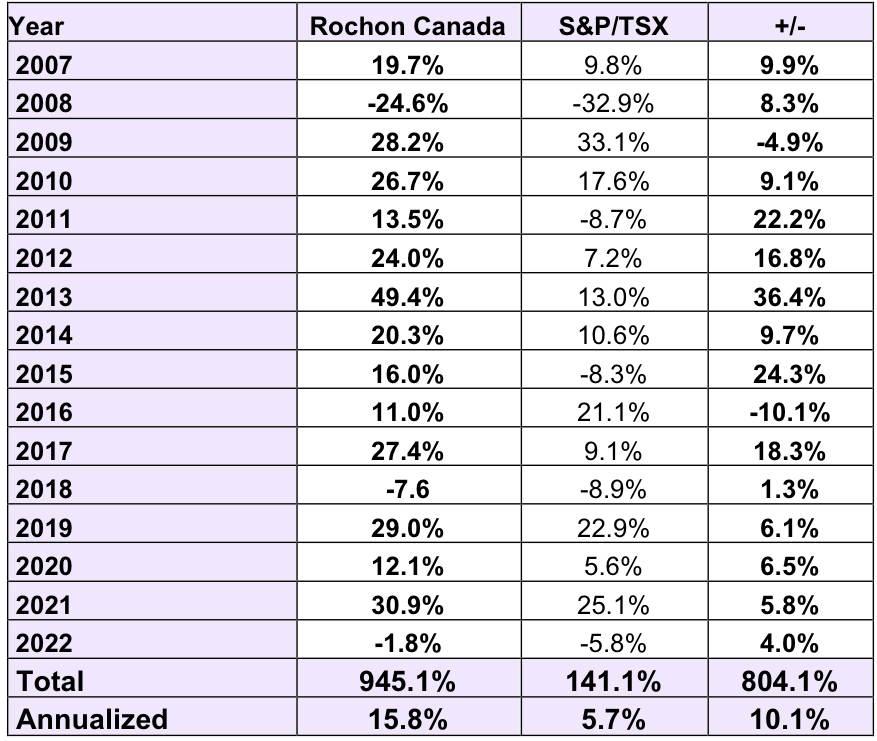

5/ In 2007 Giverny introduced a portfolio exclusively focused in Canadian equities

The portfolio is concentrated and its companies have performed well, leading to pretty outstanding outperformance

The portfolio is concentrated and its companies have performed well, leading to pretty outstanding outperformance

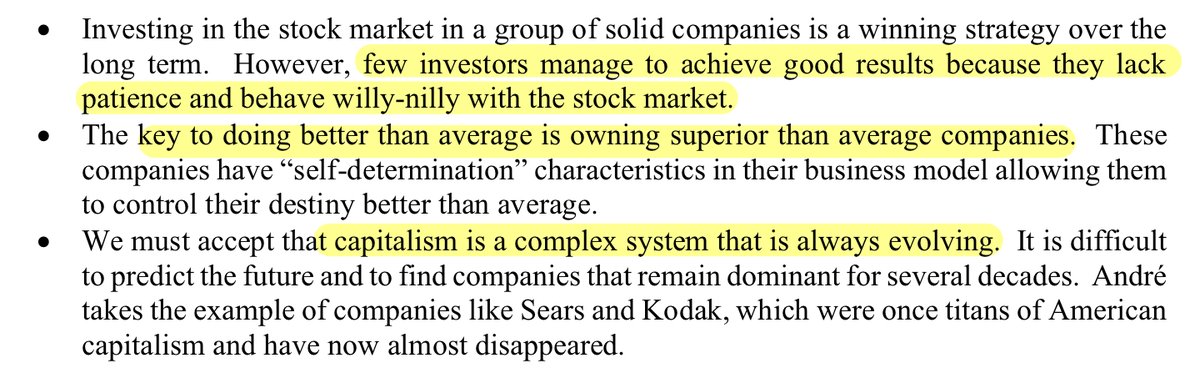

6/ Diversification is important for risk management, but the more stocks an investor holds, the more will their performance gravitate towards those of the indices

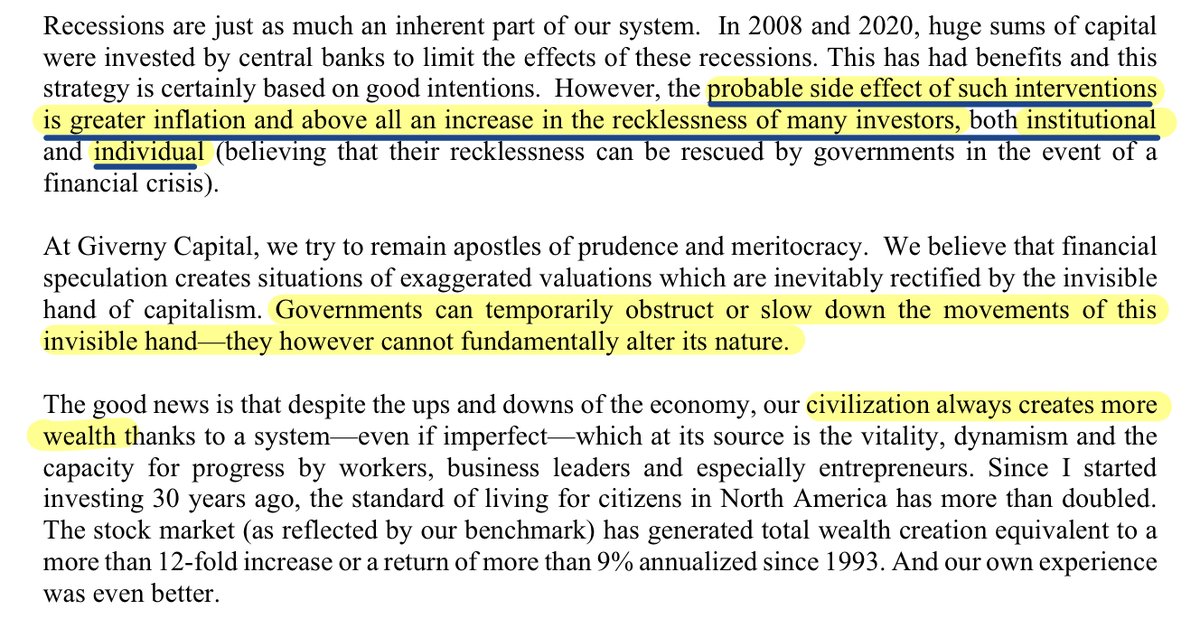

7/ François makes some comments on 2022, from which I would highlight the following paragraphs talking about how government intervention can only defer (but not avoid) economic forces

Capitalism is not a perfect model, but it creates wealth over the LT

Capitalism is not a perfect model, but it creates wealth over the LT

8/ These comments are followed by some comments related to the stock market

François attributes underperformance to not owning:

1. Natural resources companies

2. Low growth companies

These were the most resilient sectors but were absent from the portfolio

François attributes underperformance to not owning:

1. Natural resources companies

2. Low growth companies

These were the most resilient sectors but were absent from the portfolio

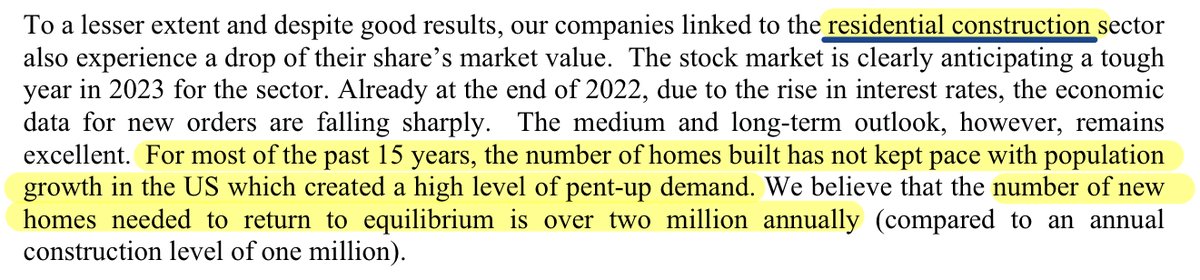

9/ He also makes the case for residential construction despite the short term challenges that might come in 2023

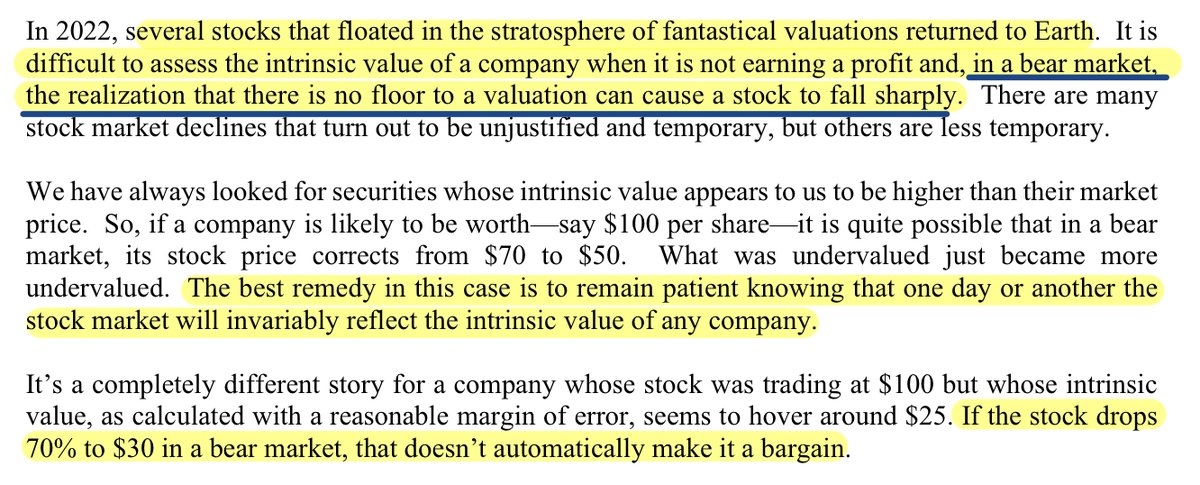

10/ The letter advises against buying companies with a lot of growth embedded in their stock prices. Sometimes these companies don't make money and thus don't have a floor on their valuations

11/ Uses $CSCO as an example.

Stock traded at 120 times earnings in the year 2000. Since then, EPS have compounded at 8% over 22 years, but the stock is down 20%

Stock traded at 120 times earnings in the year 2000. Since then, EPS have compounded at 8% over 22 years, but the stock is down 20%

12/ There's a good discussion on stock options and how they are an expense.

The bottom line is that companies spend quite a bit of FCF buying back stock to offset dilution from options and this FCF could have been used for other things, such as paying dividends to shareholders

The bottom line is that companies spend quite a bit of FCF buying back stock to offset dilution from options and this FCF could have been used for other things, such as paying dividends to shareholders

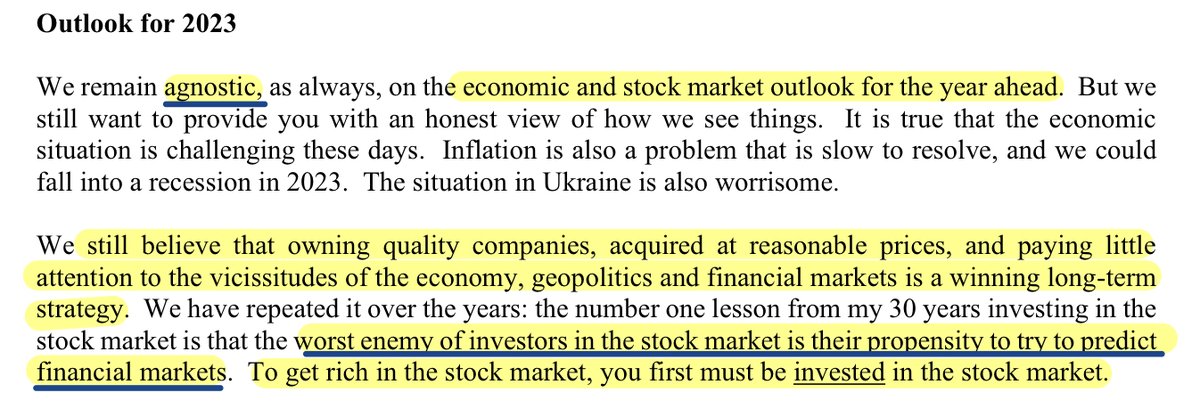

13/ Giverny's outlook for 2023 is what you would expect: agnostic and aiming to stay invested through thick and thin

14/ The "flavor of the day" continues to be crypto despite its bad performance in 2022:

"In our humble opinion, the intrinsic value of these objects of speculation appears to be totally arbitrary; so we continue to stay away from them."

"In our humble opinion, the intrinsic value of these objects of speculation appears to be totally arbitrary; so we continue to stay away from them."

15/ The podium of errors is pretty diverse. Two errors of omission and an error of selling too soon.

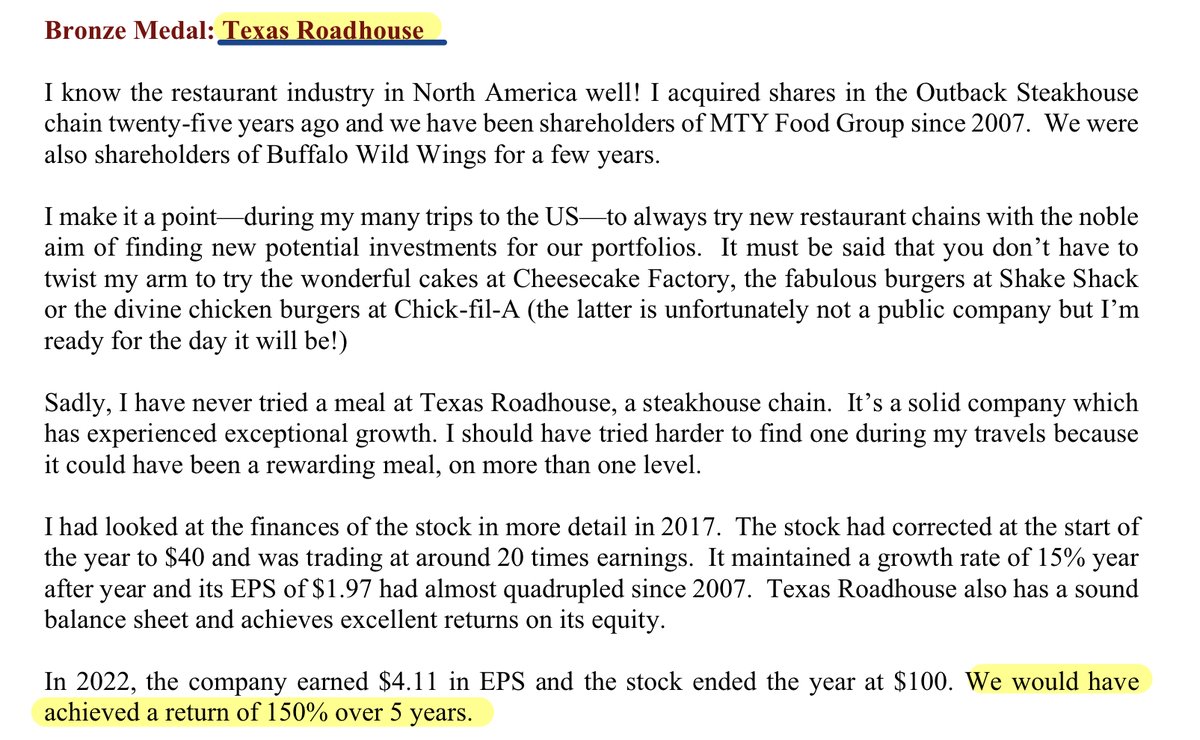

Bronze medal: Texas Roadhouse $TXRH

Missed a 150% return over 5 years:

Bronze medal: Texas Roadhouse $TXRH

Missed a 150% return over 5 years:

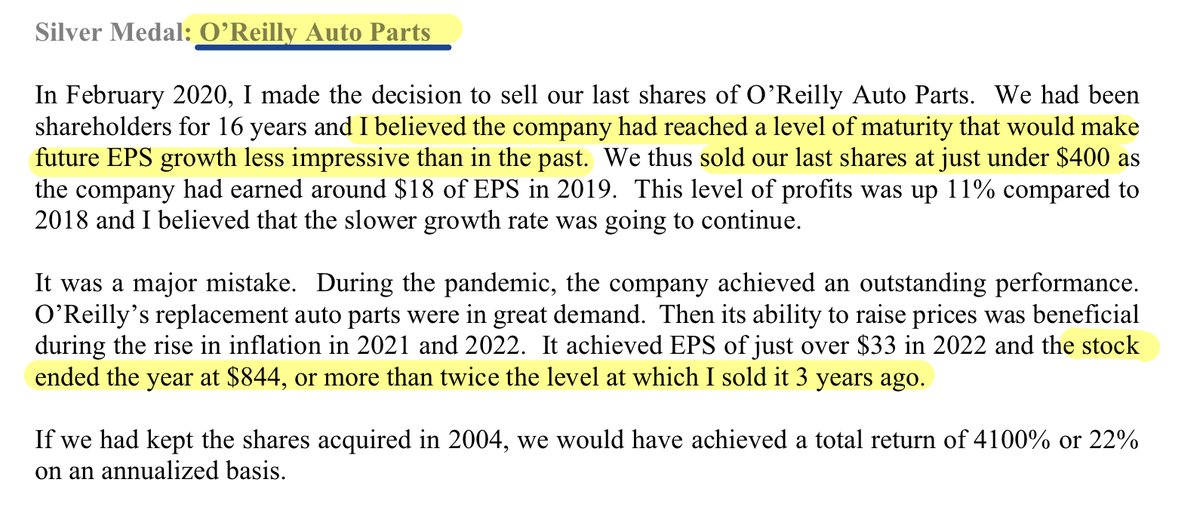

16/ Silver medal: O'Reilly $ORLY

Selling too soon made Giverny miss on a +100% move in three years, which would have equalled to a 22% CAGR since 2004

Selling too soon made Giverny miss on a +100% move in three years, which would have equalled to a 22% CAGR since 2004

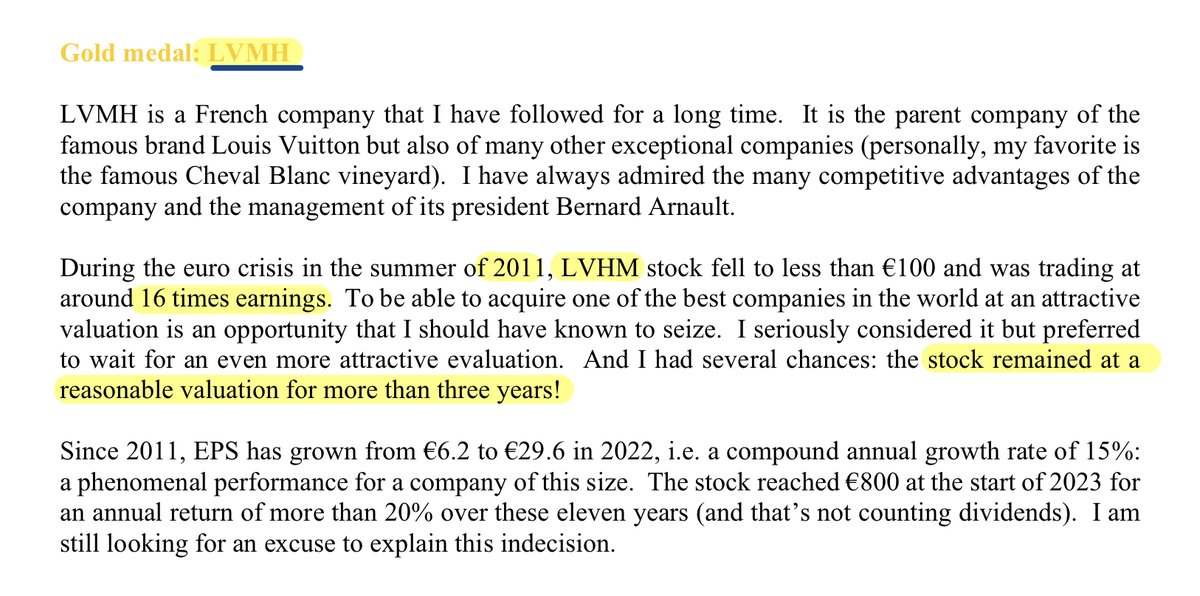

17/ Gold medal: Louis Vuitton $LVMH

Giverny missed a 20% CAGR since 2011 waiting for a better entry point

Giverny missed a 20% CAGR since 2011 waiting for a better entry point

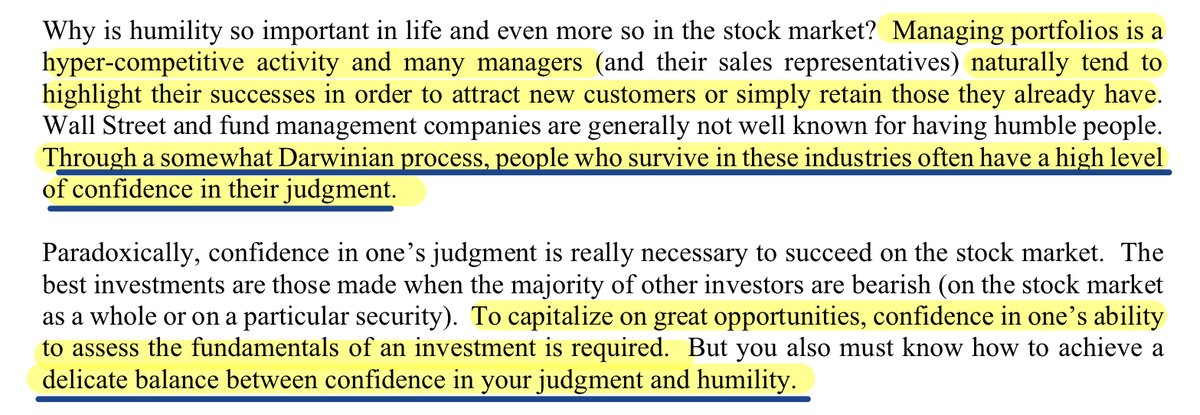

18/ The letter ends with a discussion of a vital quality for any investor: humility.

This was my favorite part:

This was my favorite part:

19/ And last but not least, François makes a list with the conclusions of his newly launched autobiography which can be summarize in:

1. Patience

2. High quality companies

3. Constant monitoring

1. Patience

2. High quality companies

3. Constant monitoring

20/ François was very kind to accept an invitation to the Best Anchor Stocks podcast, if you want to check that out you can do so below!

bestanchorstocks.substack.com

bestanchorstocks.substack.com

21/ Finally, here you have the link to the annual letter

givernycapital.com

givernycapital.com

Loading suggestions...