Grab announced its Q1 quarterly earnings recently

TLDR: Money burning continues, but at a slower rate

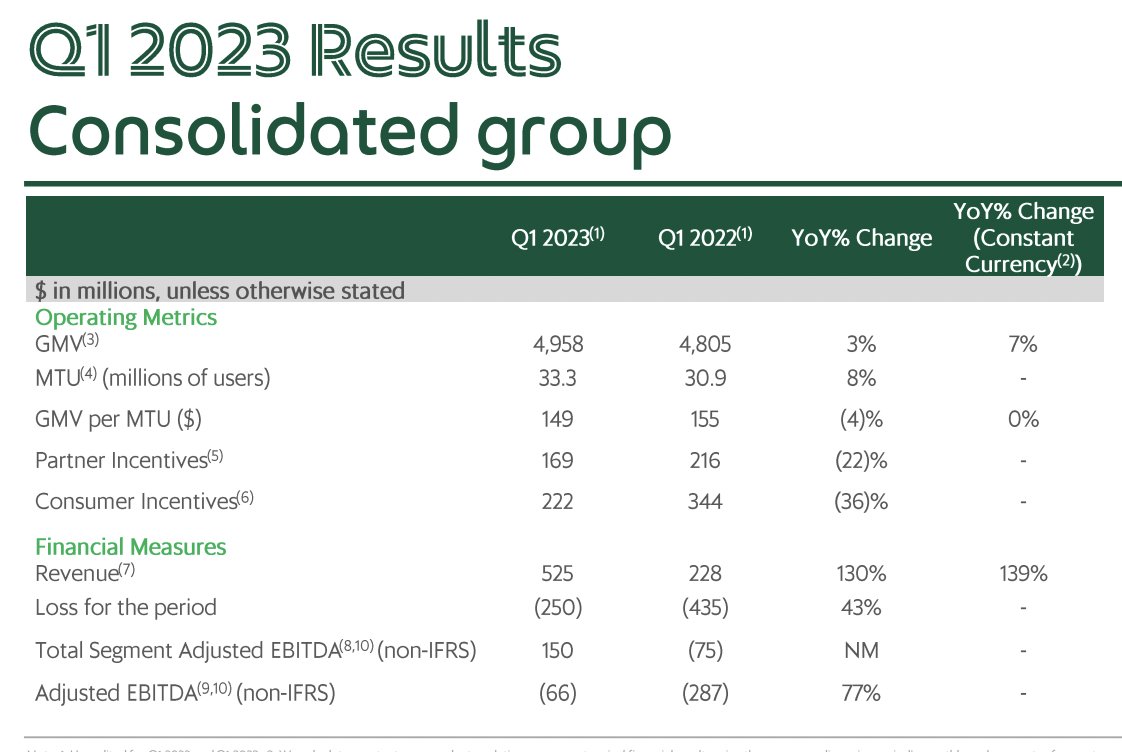

Q1 performance

Gross Merchandise Value (GMV): USD4.96 bil (+3% yoy)

Rev: USD525 mil (+139% yoy)

Net loss: -USD250 mil (improved 43% from USD435 mil yoy)

1/n

TLDR: Money burning continues, but at a slower rate

Q1 performance

Gross Merchandise Value (GMV): USD4.96 bil (+3% yoy)

Rev: USD525 mil (+139% yoy)

Net loss: -USD250 mil (improved 43% from USD435 mil yoy)

1/n

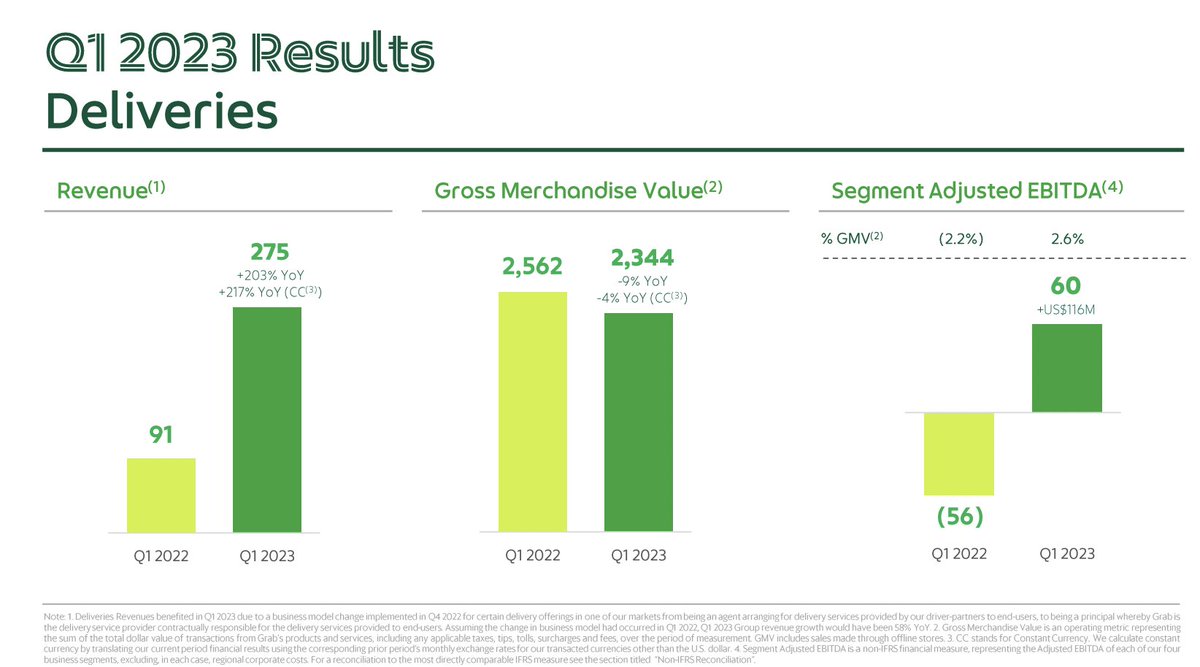

Grab is more a food delivery + grocery (Jaya Grocer parked under 'Deliveries' segment) than how it started out as ride-hailing biz

Deliveries

GMV: USD2.3 bil

Rev: USD275 mil (52.4% of total rev)

Mobility

GMV: USD1.22 bil

Rev: USD194 bil (36.9% of total rev)

2/n

Deliveries

GMV: USD2.3 bil

Rev: USD275 mil (52.4% of total rev)

Mobility

GMV: USD1.22 bil

Rev: USD194 bil (36.9% of total rev)

2/n

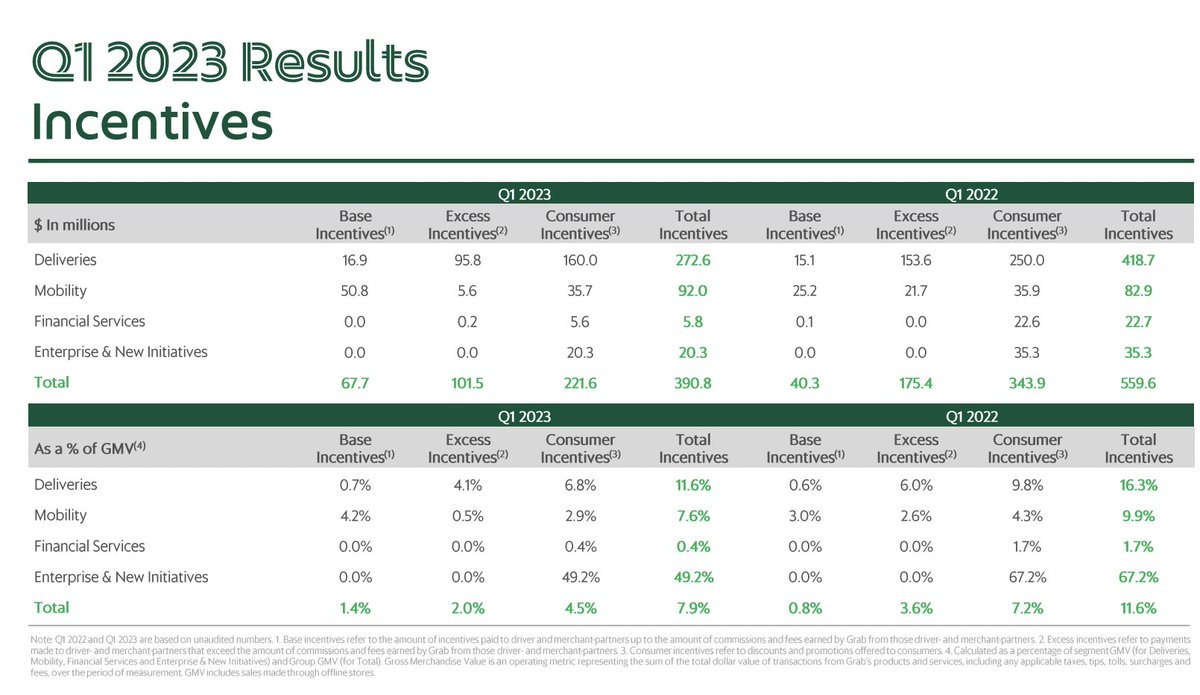

Have you felt like there isn't much promo codes, incentives etc on Grab?

For Deliveries, Grab has reduced it by slightly more than 1/3 yoy

For Mobility, it went up by 10.9% to USD92 mil

Inflation rising, subsidized lifestyle by Grab (and its investors) reducing - sad

3/n

For Deliveries, Grab has reduced it by slightly more than 1/3 yoy

For Mobility, it went up by 10.9% to USD92 mil

Inflation rising, subsidized lifestyle by Grab (and its investors) reducing - sad

3/n

All said and done, Grab still has net cash of USD4.99 bil on its balance sheet after deducting borrowings.

Grab CEO Anthony Tan said the company is on track to breakeven on adjusted EBITDA basis (in plain English, it will be loss making at net level) by Q4.

4/n

Grab CEO Anthony Tan said the company is on track to breakeven on adjusted EBITDA basis (in plain English, it will be loss making at net level) by Q4.

4/n

Is Grab a good investment?

Perhaps so for early investors. Not so for late stage investors

But, on an aggregate level-total invested vs market cap, well... it's market cap at close to USD11bil is lower. than total capital invested of USD16.5 bil. What you do you reckon?

5/5

Perhaps so for early investors. Not so for late stage investors

But, on an aggregate level-total invested vs market cap, well... it's market cap at close to USD11bil is lower. than total capital invested of USD16.5 bil. What you do you reckon?

5/5

Links:

1. Grab Q1 2023 presentation

malaysiakini.com

2. Grab Q1 2023 press release

investors.grab.com

1. Grab Q1 2023 presentation

malaysiakini.com

2. Grab Q1 2023 press release

investors.grab.com

malaysiakini.com/news/665945

K'tan Welfare Dept allocates RM4.5m monthly to help over 9k senior citizens

The department also spends over RM1.3m monthly assisting bedridden patients.

investors.grab.com/news-releases/…

Grab Reports First Quarter 2023 Results | Grab Holdings

Q1 2023 Revenue grew 130% year-over-year to $525 million 1 Q1 2023 Loss for the period improved by 4...

Interesting business and money insights delivered to your email inbox daily for free.

Join >10,000 Malaysian and grow smarter daily. Get your morning coffee news for free:

thecoffeebreak.co

Join >10,000 Malaysian and grow smarter daily. Get your morning coffee news for free:

thecoffeebreak.co

Loading suggestions...