India majorly has 3 kinds of consumers

• Who is scared of Credit Cards

• Who don’t know how to use it effectively

• Who maximise the Benefits, Power Users

I have over 30+ Credit Cards

And here are Some Practical Insights

• Who is scared of Credit Cards

• Who don’t know how to use it effectively

• Who maximise the Benefits, Power Users

I have over 30+ Credit Cards

And here are Some Practical Insights

First of all

Personal Finance is ‘Personal’

It’s absolutely fine if you use cash & UPI and don’t use Credit Cards

It’s also great if you have multiple Credit Cards and leveraging them effectively

Social Media does Influence, Don’t let anyone make you feel bad otherwise

Personal Finance is ‘Personal’

It’s absolutely fine if you use cash & UPI and don’t use Credit Cards

It’s also great if you have multiple Credit Cards and leveraging them effectively

Social Media does Influence, Don’t let anyone make you feel bad otherwise

If you’re an Expert, you can skip reading this Thread

I’ll explain in layman terms from here

I’ll explain in layman terms from here

• Anjali just started her career, her monthly in hand salary is close to ₹1 Lakh

Here are Anjali’s Average Expenses

• Rent - ₹15,000

• Bill Payments - ₹2000

• Shopping - ₹5,000

• Grocery - ₹5,000

• Cabs/Public Transport- ₹5000

• Travel (Flights, Hotels) - ₹10,000

Here are Anjali’s Average Expenses

• Rent - ₹15,000

• Bill Payments - ₹2000

• Shopping - ₹5,000

• Grocery - ₹5,000

• Cabs/Public Transport- ₹5000

• Travel (Flights, Hotels) - ₹10,000

She spends close to ₹40,000-₹50,000 Every Month

That’s close to ₹4.8-₹6 Lakh Spends Every Year

That’s close to ₹4.8-₹6 Lakh Spends Every Year

She’s smart, Instead of paying from Bank Account (UPI, Debit Cards)

She use 2-3 Credit Cards, it helps her

• Get Interest Free Credit

• Discount & Cashback

• Reward Points

• Airport & Railway Lounge

• Insurance Cover

• Purchase Protection

She use 2-3 Credit Cards, it helps her

• Get Interest Free Credit

• Discount & Cashback

• Reward Points

• Airport & Railway Lounge

• Insurance Cover

• Purchase Protection

On Yearly Basis

• She could earn 5% Value Back

• 10-20% Additional Savings

• 3-4 Free Fight Tickets

• Airline Memberships

• Free OTT Subscriptions & More

• She could earn 5% Value Back

• 10-20% Additional Savings

• 3-4 Free Fight Tickets

• Airline Memberships

• Free OTT Subscriptions & More

But what’s more important?

a) Anjali is a good actor and very disciplined with her finances

So for the transactions she made between 1-30/31st Last Months

Her Billing Date is 1st of Every Month, and Due Date is 20th

a) Anjali is a good actor and very disciplined with her finances

So for the transactions she made between 1-30/31st Last Months

Her Billing Date is 1st of Every Month, and Due Date is 20th

But she pays her Full Credit Card Bill right after statement generation

It has helped her build a Good Credit Score

It has helped her build a Good Credit Score

b) While her Bank has given ₹3 Lakh Credit Limit, she only uses the amount that she can pay back, she never overspend

Unlike many others who overuse Credit Cards, fall into the Debt Trap

Anjali was always mindful about her financials and maintained discipline

Unlike many others who overuse Credit Cards, fall into the Debt Trap

Anjali was always mindful about her financials and maintained discipline

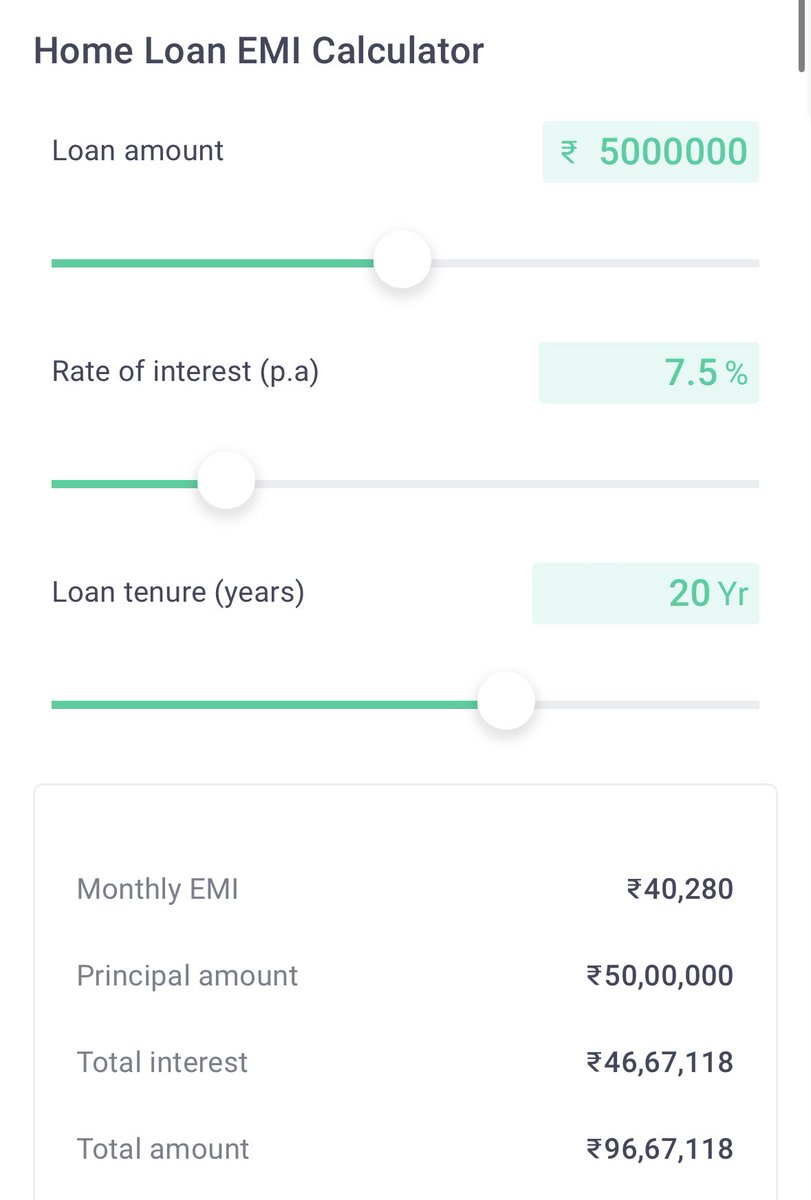

After 5 Years, She needed a Home Loan of ₹50 Lakh for 20 Years.

So what?

Since Anjali uses Credit Cards, never missed her Payments in the Last 5 years,

Her Credit Score is Excellent

She got the Home Loan at 7.5%

So what?

Since Anjali uses Credit Cards, never missed her Payments in the Last 5 years,

Her Credit Score is Excellent

She got the Home Loan at 7.5%

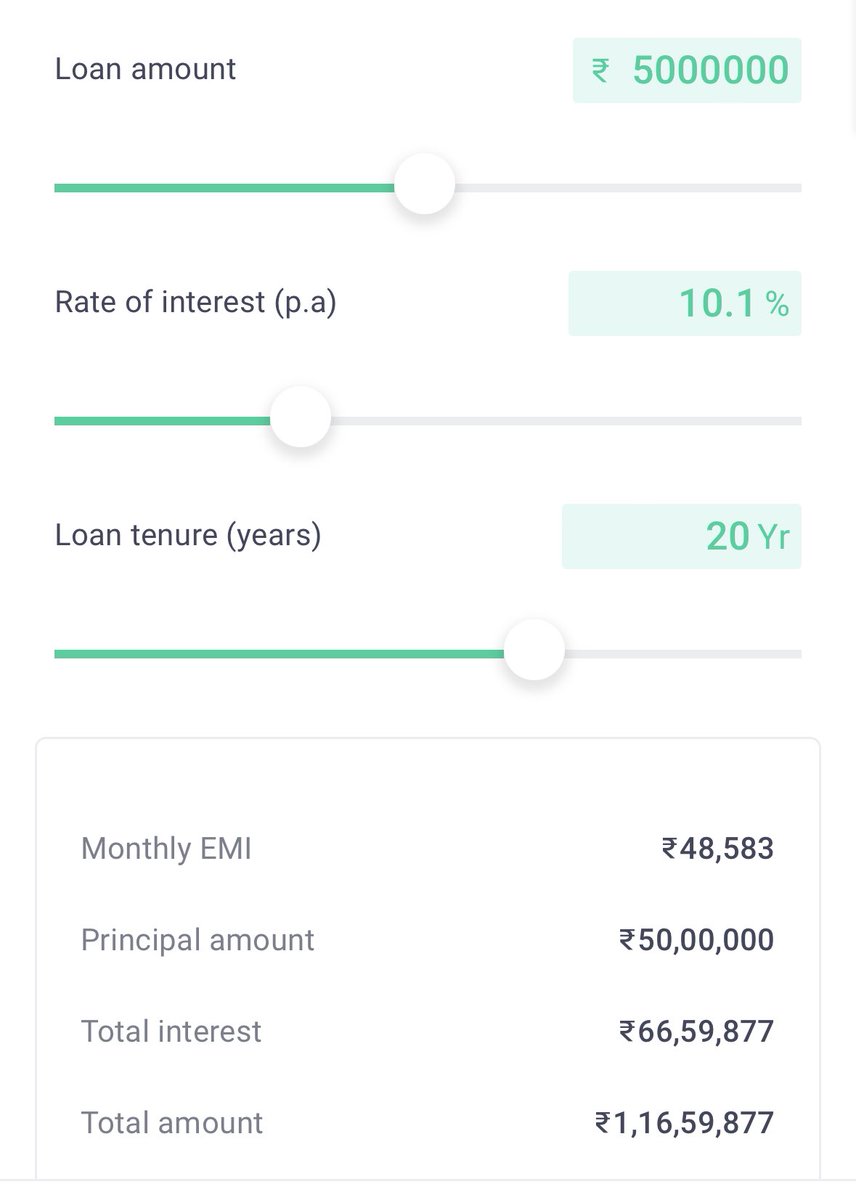

But when Sumit, her colleague went to the Bank. The Bank quoted 10.1% Interest Rate because Sumit had no Credit History or Credit Score

Sumit is ‘New to Credit’ Ecosystem

So Bank can’t really know if Sumit won’t default on his loans

Sumit is ‘New to Credit’ Ecosystem

So Bank can’t really know if Sumit won’t default on his loans

You see?

Sumit is paying ₹20 Lakh Extra because of Higher Interest Rates (Since he don’t have any Credit Score)

Over ₹20 Lakh difference in the Interest Amount of Home Loan, just because of Great Credit Score?

Sumit is paying ₹20 Lakh Extra because of Higher Interest Rates (Since he don’t have any Credit Score)

Over ₹20 Lakh difference in the Interest Amount of Home Loan, just because of Great Credit Score?

Important Point - Note that these numbers are based on assumption, actual interest rate and calculation might vary depends on case to case

I’ve personally & professionally seen people not getting the best Interest Rates, Premium Credit Cards because of No or Low Credit Score

Look at this

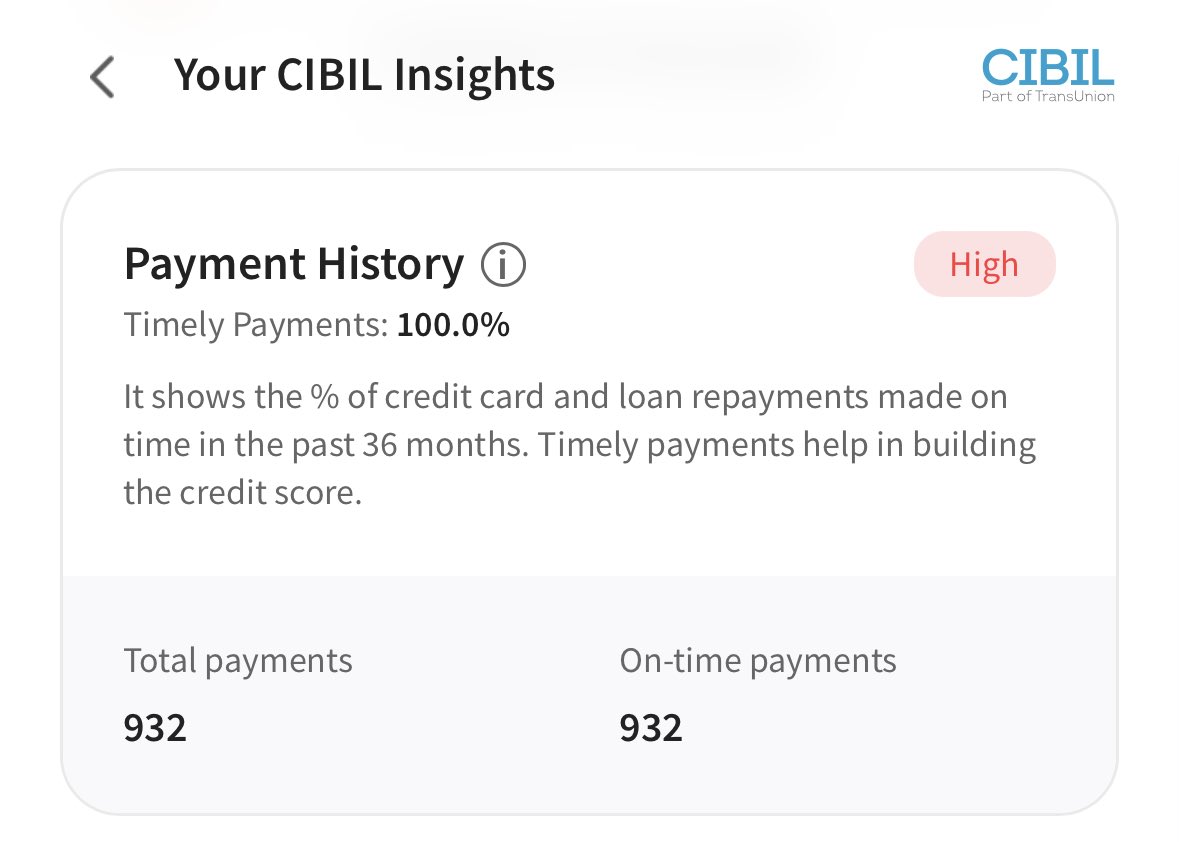

This is the Payment History Part of Credit Report

This is mine 😛

Because Anjali is an Imaginary Character

I’ve made 932/932 Payments on Time in the Last 6-7 Years

This is the Payment History Part of Credit Report

This is mine 😛

Because Anjali is an Imaginary Character

I’ve made 932/932 Payments on Time in the Last 6-7 Years

So what else a Credit Report Contains?

• Credit Utilisation

• Payment History

• Age of Credit Accounts

• Credit Mix (Loan & CCs)

• Recent Enquiries

• Credit Utilisation

• Payment History

• Age of Credit Accounts

• Credit Mix (Loan & CCs)

• Recent Enquiries

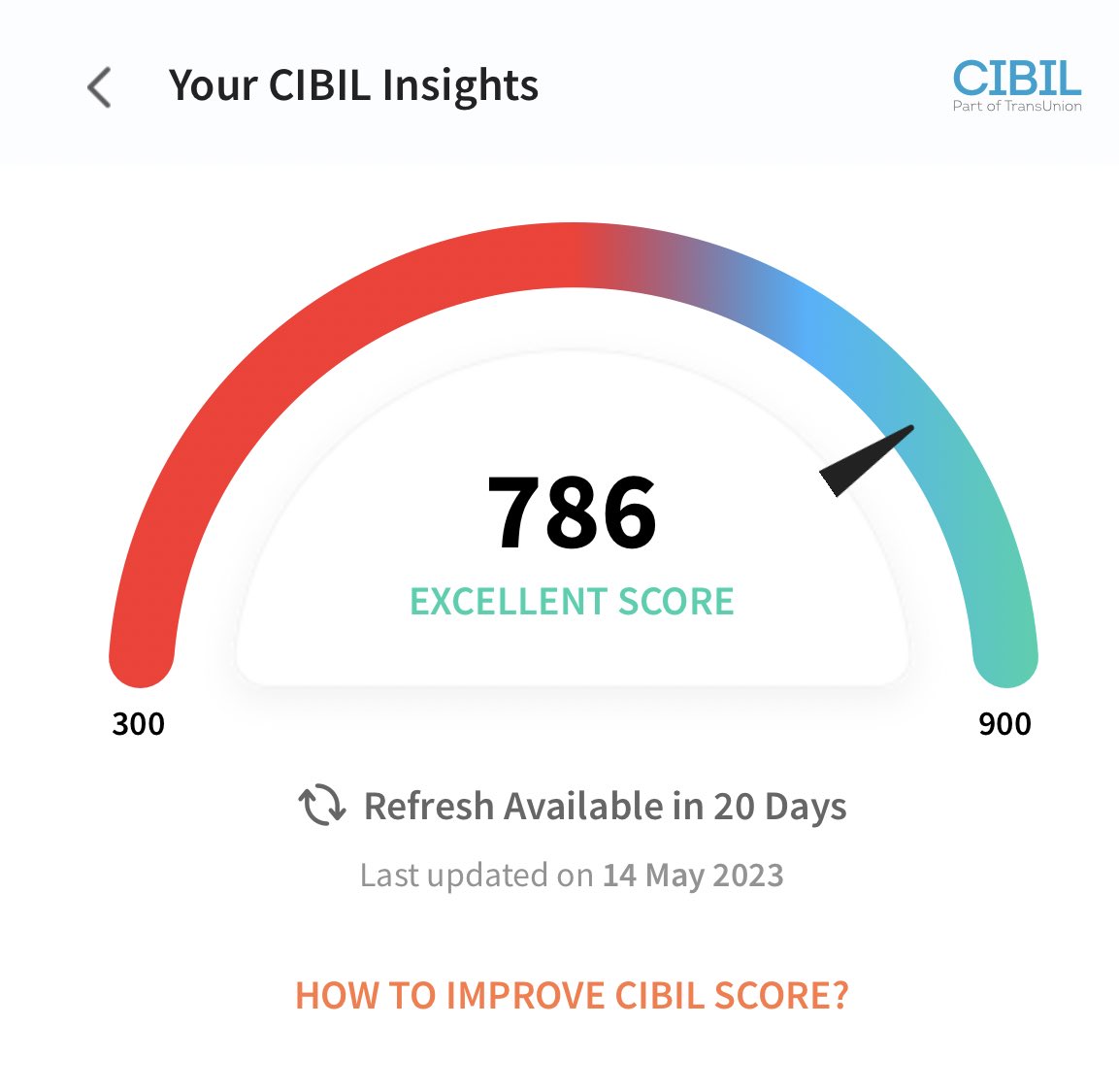

With all honesty, this is my CIBIL Score

(CIBIL is one of the Most Preferred Credit Bureau by Indian Banks)

(CIBIL is one of the Most Preferred Credit Bureau by Indian Banks)

Back to Story

Neha is a Cousin of Anjali, she was very Impressed the way Anjali manages her money

Neha also applied for a Credit Card, started using it without any discipline

She only paid Minimum Due every month instead of full payments, fell into dangerous Credit Card Trap

Neha is a Cousin of Anjali, she was very Impressed the way Anjali manages her money

Neha also applied for a Credit Card, started using it without any discipline

She only paid Minimum Due every month instead of full payments, fell into dangerous Credit Card Trap

Not only Neha ruined her Credit Score but she also ended up draining her Savings & Investment

Note that Credit Cards comes with Upto 48% Interest, Heavy Penalties & Many Other Such Charges

Note that Credit Cards comes with Upto 48% Interest, Heavy Penalties & Many Other Such Charges

So there are millions of Anjali, Sumit & Neha in India

Many times, they are told by their parents, friends, colleagues, LIC uncle etc that Credit Cards are bad and you’ll be bankrupt if you start using them

Many times, they are told by their parents, friends, colleagues, LIC uncle etc that Credit Cards are bad and you’ll be bankrupt if you start using them

They may be coming from their experiences, but we need to learn things from our end before taking any borrowed opinion

This is very important for subjects concerning our finance & health

This is very important for subjects concerning our finance & health

So as you read

Apart from Benefits & Rewards

Credit Cards also help build a Good Credit Score that will come extremely handy when you need it the most

Read, Research & Take Better Financial Decisions, Managing your Money is as Important as Earring it

Apart from Benefits & Rewards

Credit Cards also help build a Good Credit Score that will come extremely handy when you need it the most

Read, Research & Take Better Financial Decisions, Managing your Money is as Important as Earring it

This Thread is Part of an Upcoming Series where I’ll be explaining Practical Insights of Personal Finance & Credit Cards from Beginner to Advanced Level

We’ll also Read in the Next Few Weeks

• Best 5 Credit Cards for Starters

• How to Build a Good Credit Score

• Premium Credit Cards

• Airmiles & Loyalty Programs

• Free Credit/Debit Cards for Lounge Access

• Best 5 Credit Cards for Starters

• How to Build a Good Credit Score

• Premium Credit Cards

• Airmiles & Loyalty Programs

• Free Credit/Debit Cards for Lounge Access

Bonus Thread for Advanced Users

Vistara is my favourite Airline

Vistara is my favourite Airline

Hope these Insights are Helpful

Thanks for Reading

Appreciate the RT to Educate More People

Follow @Ravisutanjani For More

Thanks for Reading

Appreciate the RT to Educate More People

Follow @Ravisutanjani For More

Loading suggestions...