I presented my thoughts on the diagnostic industry & the events that played out post covid last week (webinar link at the end of the thread🧵).

I explained the insides of the diagnostic industry in the webinar but, I think it is very well covered & most of us have some basic idea if not exhaustive about the functionality of the diagnostic industry.

I will try to add value to the displacement effect & the competition part – which has gained much attention post-pandemic in this thread.

Although to understand the nitty-gritty of the diagnostic industry, you can watch the video (tried to decode many aspects of the industry).

Although to understand the nitty-gritty of the diagnostic industry, you can watch the video (tried to decode many aspects of the industry).

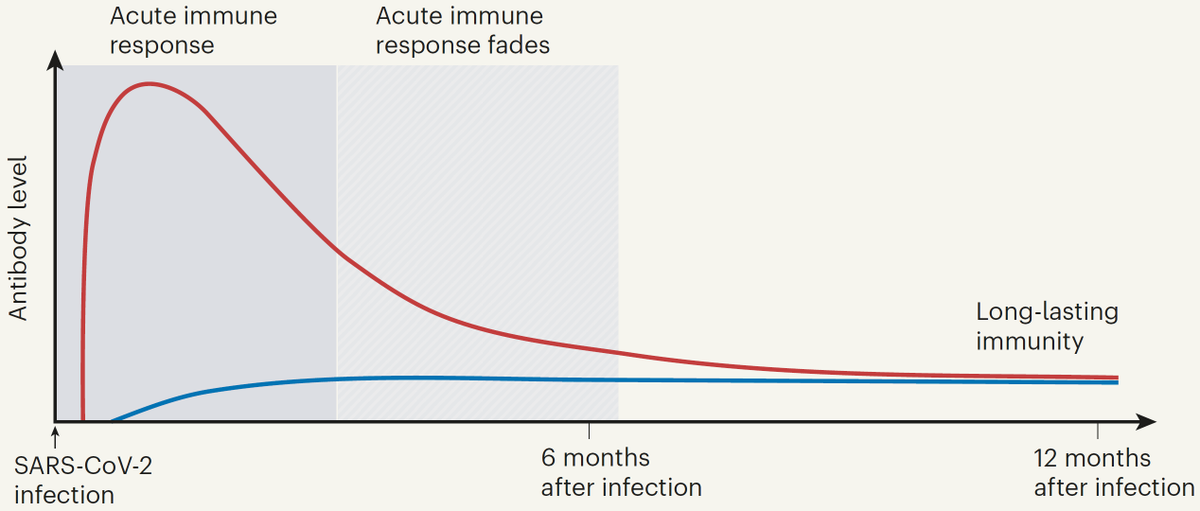

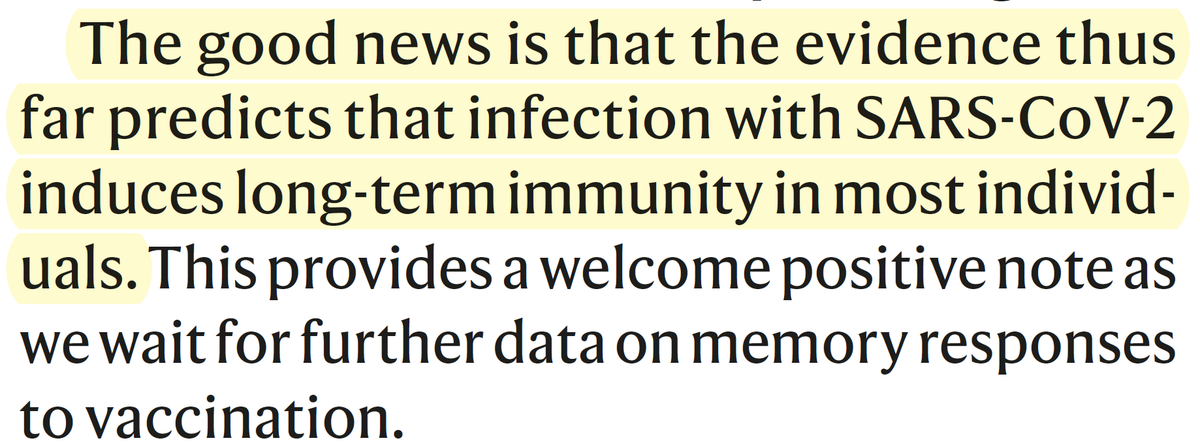

Post-covid, there’s been some noise around the improved immunity. Below are some extracts from a report published by Andreas Radbruch & Hyun-Dong Chang in July 2021.

Crux is - People get immune & fall less ill post-fading of covid (also known as the displacement effect/harvesting effect). But I have not come across any data that backs such a theory.

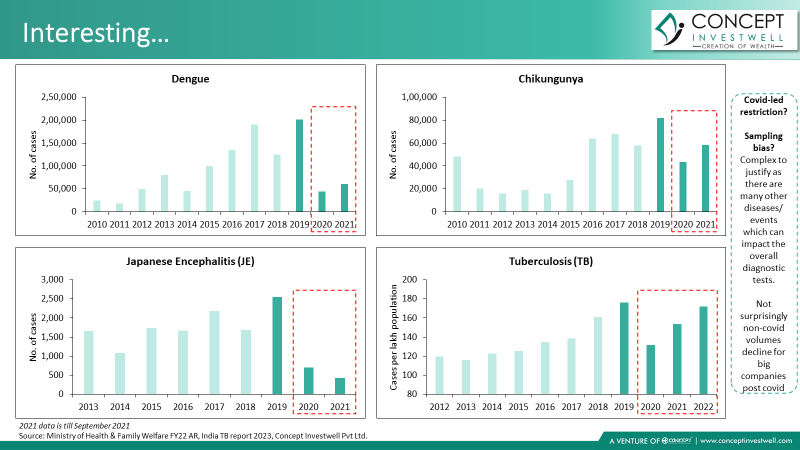

So I tried to get my hands on India’s illness data. Surprisingly, the cases of a few diseases such as Dengue, Chikungunya, Tuberculosis etc. have come down (below is an extract from one of my slides).

But there’s a lot of sampling bias. There are only 4 diseases that I have come across – it’s very challenging to get disease-specific data for the whole of India. There are many other diseases which impact the overall diagnostic tests.

There were also covid-led restrictions (lockdown for example) in the economy. Maybe people didn’t go for testing.

Thus, I can’t strongly conclude about the improved immunity of the people. There is no solid data that backs the theory as of now.

Thus, I can’t strongly conclude about the improved immunity of the people. There is no solid data that backs the theory as of now.

*Competition*

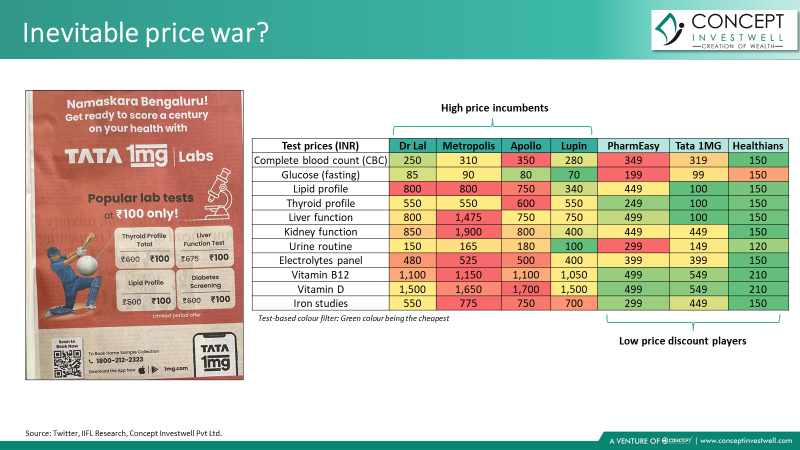

There have been a lot of negativities prevailing around the listed (incumbents) diagnostic companies post the entry of new organized big pocket players – be it Reliance, Tata and some new start-ups.

New entrants are trying to out beat incumbents via price war.

There have been a lot of negativities prevailing around the listed (incumbents) diagnostic companies post the entry of new organized big pocket players – be it Reliance, Tata and some new start-ups.

New entrants are trying to out beat incumbents via price war.

One question that comes to mind is – Is lower pricing the way to acquire customers? Deepak Sahni (@dsahni_01) – founder of Healthians (A Gurgaon-based diagnostic company incorporated in 2015) answered aptly in one of his interviews.

On the other hand, Gaurav Agarwal (@agarwal_gaurav) – Co-founder of Tata 1MG in one of the interviews (post the INR 100 advertisement) said that the pricing depends on how successful this campaign goes (higher volumes will bring economies of scale & hence sustainability).

Before going into the details of scaling, let me show you some interesting data.

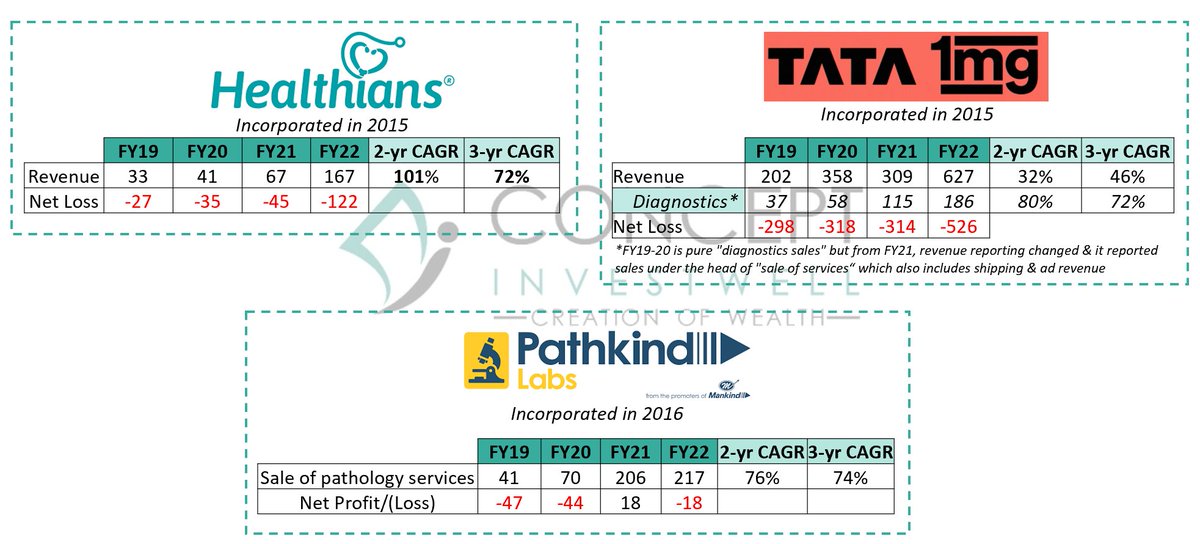

You might think that given the low prices, these startups like Healthians & Tata 1MG must have done extremely well, especially in the covid period as compared to the brick & mortar non-discount cos.

You might think that given the low prices, these startups like Healthians & Tata 1MG must have done extremely well, especially in the covid period as compared to the brick & mortar non-discount cos.

Let’s take Pathkind Labs (brick & mortar non-discount company) v/s Tata 1MG & Healthians. Look at the image below - a non-discount company performed better.

Pathkind Labs seems to be a decent peer as it is incorporated in 2016 as compared to Tata 1MG & Healthians (both in 2015).

Pathkind Labs seems to be a decent peer as it is incorporated in 2016 as compared to Tata 1MG & Healthians (both in 2015).

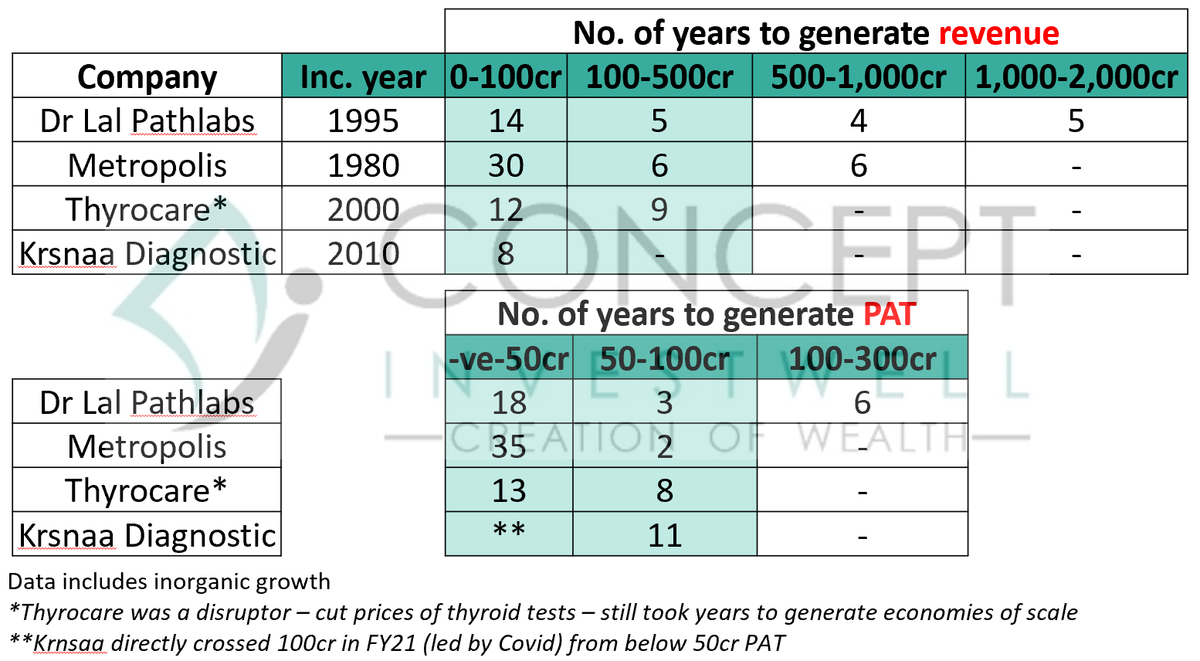

Scaling is particularly difficult in the diagnostic industry. The ones who have scaled took decades to do so. Observe the image below – the entry barrier might be low but the barrier to scale is very high.

Yes, inflation & time value of money plays a big role – INR 1cr today is worth less compared to INR 1cr in the early 2000s. I am not debating on that part. This is just to showcase how much time it took for established diagnostic chains to become big.

~55-60% of the industry runs on doctor referrals. Winning a doctor’s trust is key as the majority of the treatment decision happens based on the test reports & if something wrong happens to the patient post-treatment,.....

the patient will not blame say Metropolis or Dr Lal’s test report. He/she will blame the doctor.

Another point to remember – In India, there are more than 1 lakh labs but less than 2% are NABL accredited. Big organized diagnostic chains can’t push growth just by buying out or partnering with an uncertified lab.

You might also think that Tata 1MG & Healthians crossed 100cr in less than 10 years. Remember covid revenue is baked in those numbers. Once covid is absent, scaling will normalize.

What happens when you can’t scale enough?

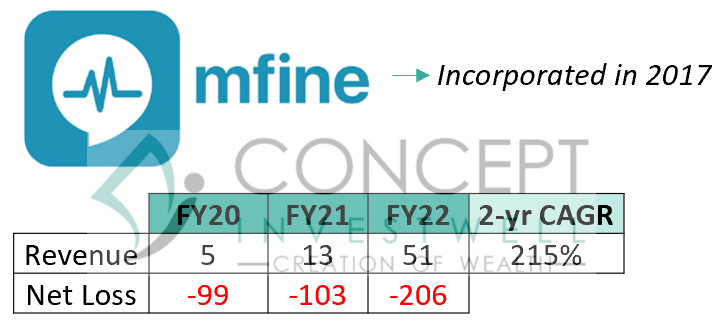

Let’s take a case study of Mfine - which was incorporated in 2017. FY22 revenue for Mfine was just INR 51cr. Remember that Tata 1MG & Healthians FY22 revenue was around INR 170-180cr.

Let’s take a case study of Mfine - which was incorporated in 2017. FY22 revenue for Mfine was just INR 51cr. Remember that Tata 1MG & Healthians FY22 revenue was around INR 170-180cr.

Mfine did a corporate restructuring in May’22 – fired 50% of employees & shifted their focus on more profitable areas such as corporate service and insurance partnerships. It increased the prices of diagnostic tests by almost 100% since Mar’22.

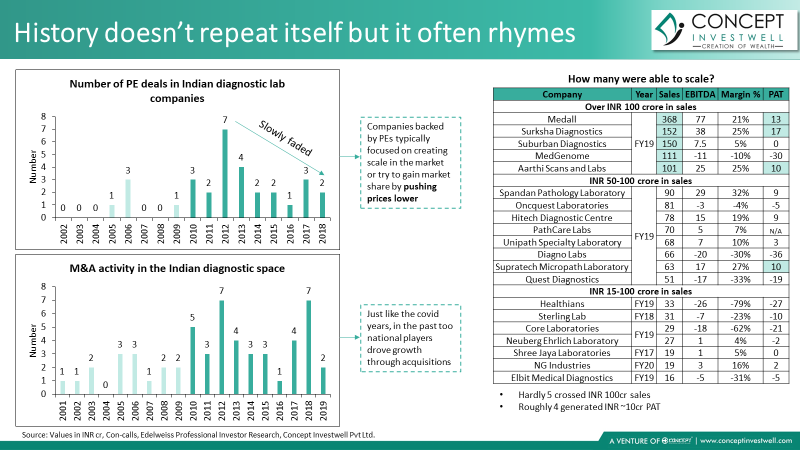

Competition is not new in the diagnostic industry. If you read the commentary section of the FY16 annual report of Dr Lal Pathlabs, you’ll find that the current scenario is the same.

Entry of new players is also not new. In the Q4FY22 con call of Metropolis, Ameera Shah (@AmeeraShah) said that the current cycle resonates to 2012-16 when a whole lot of new players entered the market, but very few could survive. Observe the extract from the presentation below.

Sidhhart Bhaiya sir (@sidd1307) tweeted a while back about disruption which I relate to after studying the history of the diagnostic industry.

This thread was just a summary of the key areas presented. If you like the work, please watch the video & share your views/suggestions.

Note: This is the 1st time when I presented in front of a camera (with recording) & a decent audience. I did fumble a bit. Pardon me. I’ll practice & improve on it in the coming times if at all I present something new.

youtube.com

youtube.com

Loading suggestions...