The debt ceiling issues present a much greater risk than currently perceived.

Although prior concerns have proven to be mostly peripheral, today’s circumstances are quite unique.

To be clear:

The main problem relates to the potential consequences after an agreement.

👇👇👇

Although prior concerns have proven to be mostly peripheral, today’s circumstances are quite unique.

To be clear:

The main problem relates to the potential consequences after an agreement.

👇👇👇

During periods that require a debt ceiling extension, the Treasury cash balance for daily operations tends to be at extremely low levels, which is the case again today.

Once an agreement is reached, the government must issue debt promptly in order to sustain its functions due to the persistent fiscal deficit imbalance.

Note, however:

Over time, the issuance of Treasuries has been increasing steadily.

Note, however:

Over time, the issuance of Treasuries has been increasing steadily.

This time around, we anticipate an unprecedented surge in the amount of debt being raised in the ensuing months.

All else equal, this should exert major downward pressure on the price of these fixed-income instruments.

All else equal, this should exert major downward pressure on the price of these fixed-income instruments.

In the past, the lack of inflation concerns, the foreign investors' demand for Treasuries, the absence of bank failures due to these instruments, and the Fed’s ultra-dovish stance allowed the market to smoothly absorb the growing debt supply without significant disruptions.

Today, given the adverse macro environment, the emergence of a supply-side problem requires much greater attention.

It cannot be overstated that the US Treasury market serves as the cornerstone of the entire financial system.

The inflated valuation of financial assets hinges on a low cost of capital environment, making it a crucial factor in the overall economy.

The inflated valuation of financial assets hinges on a low cost of capital environment, making it a crucial factor in the overall economy.

It is worth noting that the recent positive developments related to a potential resolution of the debt ceiling have coincided with upward pressure on long-term interest rates.

Investors are beginning to recognize that the true risk this time around lies not in the failure to reach an agreement, but rather in the escalating and concerning nature of the debt problem.

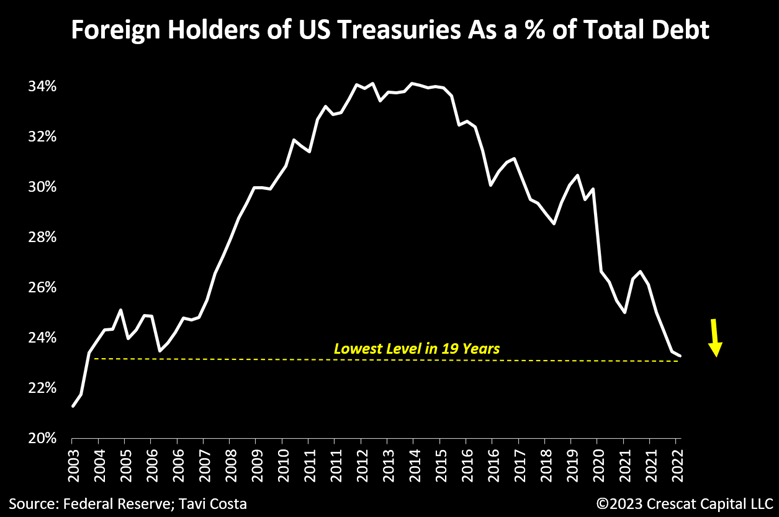

This problem is further amplified by the diminishing availability of Treasury buyers.

This problem is further amplified by the diminishing availability of Treasury buyers.

In the last 3 years, the responsibility of absorbing this debt fell on the Fed and US banks, but now both entities have withdrawn from that role.

Additionally:

Foreign investors have not been net purchasers of US Treasuries despite the substantial influx of issuances lately.

Additionally:

Foreign investors have not been net purchasers of US Treasuries despite the substantial influx of issuances lately.

The current lack of demand is indeed a growing problem that may ultimately necessitate the intervention of the Fed as the buyer of last resort.

We can recall the historic selloff of UK Gilts last year, triggered by a tax cut announcement that investors perceived as posing a significant risk to the country’s financial stability.

This situation led the BOE to reverse its QT course and intervene as a buyer of UK bonds.

This situation led the BOE to reverse its QT course and intervene as a buyer of UK bonds.

In our strong opinion:

The US is primed to have its own BOE moment.

The US is primed to have its own BOE moment.

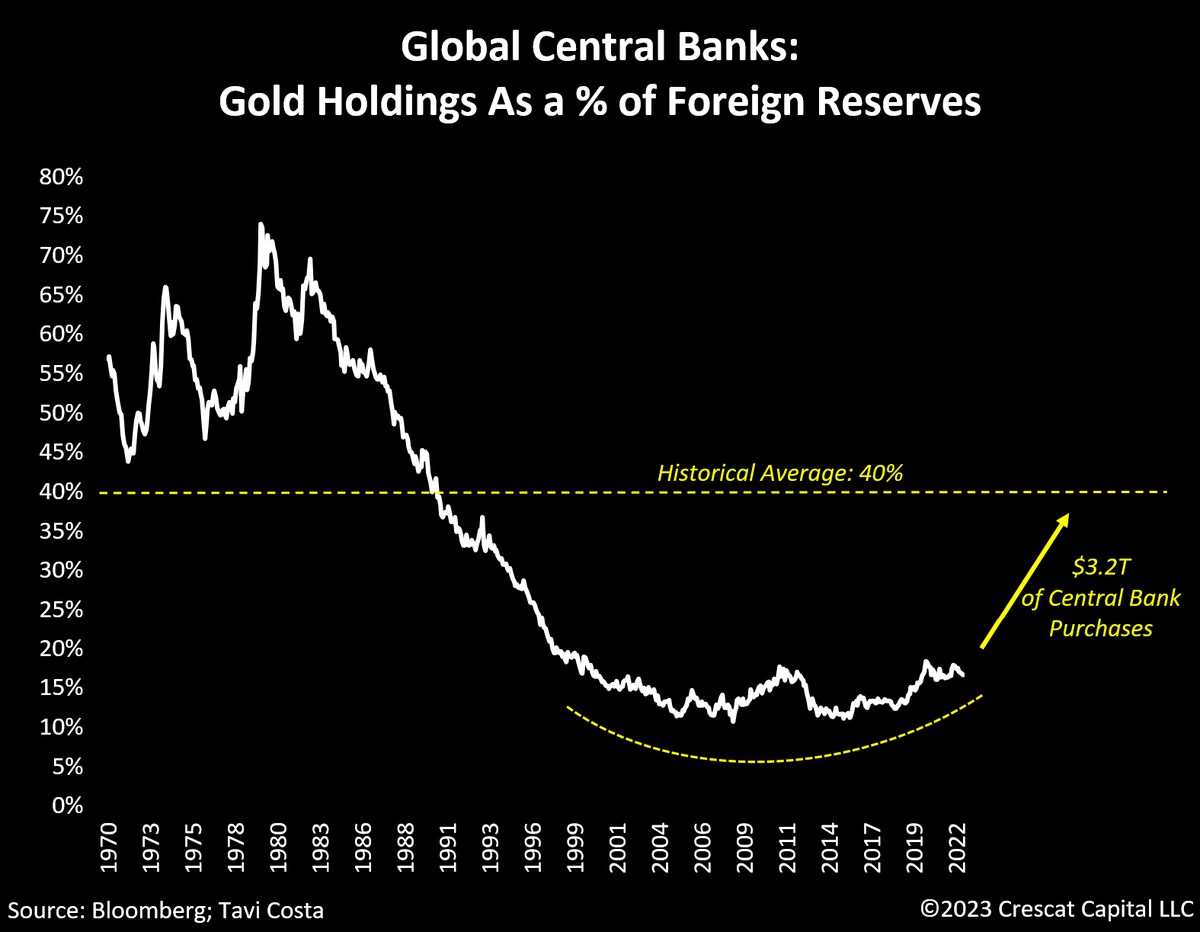

Given the dire levels of global debt, foreign central banks are compelled to prioritize enhancing the quality of their international reserves to support their monetary systems.

In essence, these institutions function similarly to traditional businesses that require high-quality assets on their balance sheets to establish financial stability.

Following the end of the gold standard in 1971, central banks continued to purchase gold for the next decade.

At its peak, gold holdings constituted 72% of their overall balance sheet assets.

At its peak, gold holdings constituted 72% of their overall balance sheet assets.

Subsequently, due to a prolonged period of increase in interest rates, central banks opted to accumulate US debt at historically attractive valuations.

This occurred during a time when the world economy was also progressively becoming more globalized, which significantly fueled the substantial demand for Treasury instruments.

Consequently:

These instruments experienced nearly 30 years of continuous appreciation.

Other notable institutions such as pension and endowment funds soon followed suit, resulting in the highly favorable 60/40 portfolio position from the early 1980s until recently.

These instruments experienced nearly 30 years of continuous appreciation.

Other notable institutions such as pension and endowment funds soon followed suit, resulting in the highly favorable 60/40 portfolio position from the early 1980s until recently.

This dynamic created a structural effect where the high demand for Treasuries resulted in decreased interest rates, consequently contributing to inflated equity market valuations.

Now, foreign central banks have reversed their stance again.

They are significant buyers of gold while some have become major sellers of US debt.

They are significant buyers of gold while some have become major sellers of US debt.

Escalating geopolitical conflict has increased the importance of owning a neutral asset with no counterparty risk that also carries centuries of credible history as a haven.

Gold is the only asset that qualifies.

Gold is the only asset that qualifies.

Central banks have thus pivoted to being substantial buyers over the last several years leading to a rising percentage of gold ownership on their balance sheets.

As a % of FX reserves:

If this measurement were to return to its historical average of 40%, all else equal, it would be an injection of approximately $3.2 trillion of new capital into the gold market.

Price would have to be the reconciling factor in accommodating this demand.

If this measurement were to return to its historical average of 40%, all else equal, it would be an injection of approximately $3.2 trillion of new capital into the gold market.

Price would have to be the reconciling factor in accommodating this demand.

Since $3.2 trillion is 25% of the total value of all above-ground gold, or essentially all the gold ever mined, which now stands at $13 trillion:

A 25% upward adjustment in price would get the gold price to $2,500 an ounce.

A 25% upward adjustment in price would get the gold price to $2,500 an ounce.

More importantly:

This dynamic is expected to prompt other major institutions and individual investors to follow suit, triggering an even greater influx of capital into the gold and precious metals markets.

This dynamic is expected to prompt other major institutions and individual investors to follow suit, triggering an even greater influx of capital into the gold and precious metals markets.

We expect much of this new demand will flow into the mining industry where the deep value is substantially more compelling in this macro environment with multi-fold appreciation potential in companies with big, viable new and incipient discoveries.

Market correlations undergo changes when the macroeconomic regime itself undergoes a shift.

Traditional 60/40 portfolios experienced a rude awakening in 2022, which likely marked a turning point in the interrelationship of asset classes.

Traditional 60/40 portfolios experienced a rude awakening in 2022, which likely marked a turning point in the interrelationship of asset classes.

While both the equity and bond markets faced challenges simultaneously, gold showed exceptional resilience.

This recent market behavior is reminiscent of the other inflationary periods, particularly the 70s, although the circumstances then were very different from today.

This recent market behavior is reminiscent of the other inflationary periods, particularly the 70s, although the circumstances then were very different from today.

Given the substantial levels of debt and imbalances in asset valuations, it is unlikely for interest rates to rise in the same manner as they did in the 1970s over the next decade without causing a financial calamity.

Therefore:

In a world where policymakers must inevitably intervene to suppress the cost of debt, irrespective of the potential effectiveness of such actions, gold would likely emerge as a key monetary asset to own carrying centuries of credibility as hard money.

In a world where policymakers must inevitably intervene to suppress the cost of debt, irrespective of the potential effectiveness of such actions, gold would likely emerge as a key monetary asset to own carrying centuries of credibility as hard money.

It is worth noting that during the 1970s:

US 10-year interest rates averaged around 7.5%, making long-term Treasuries significantly more appealing in terms of valuation, with a price-to-earnings (P/E) ratio of 13x.

US 10-year interest rates averaged around 7.5%, making long-term Treasuries significantly more appealing in terms of valuation, with a price-to-earnings (P/E) ratio of 13x.

In contrast, with a P/E ratio of 28x today:

If the rationale for owning these instruments is solely based on the premise that the system cannot endure substantially higher interest rates, then gold would be a far superior choice.

If the rationale for owning these instruments is solely based on the premise that the system cannot endure substantially higher interest rates, then gold would be a far superior choice.

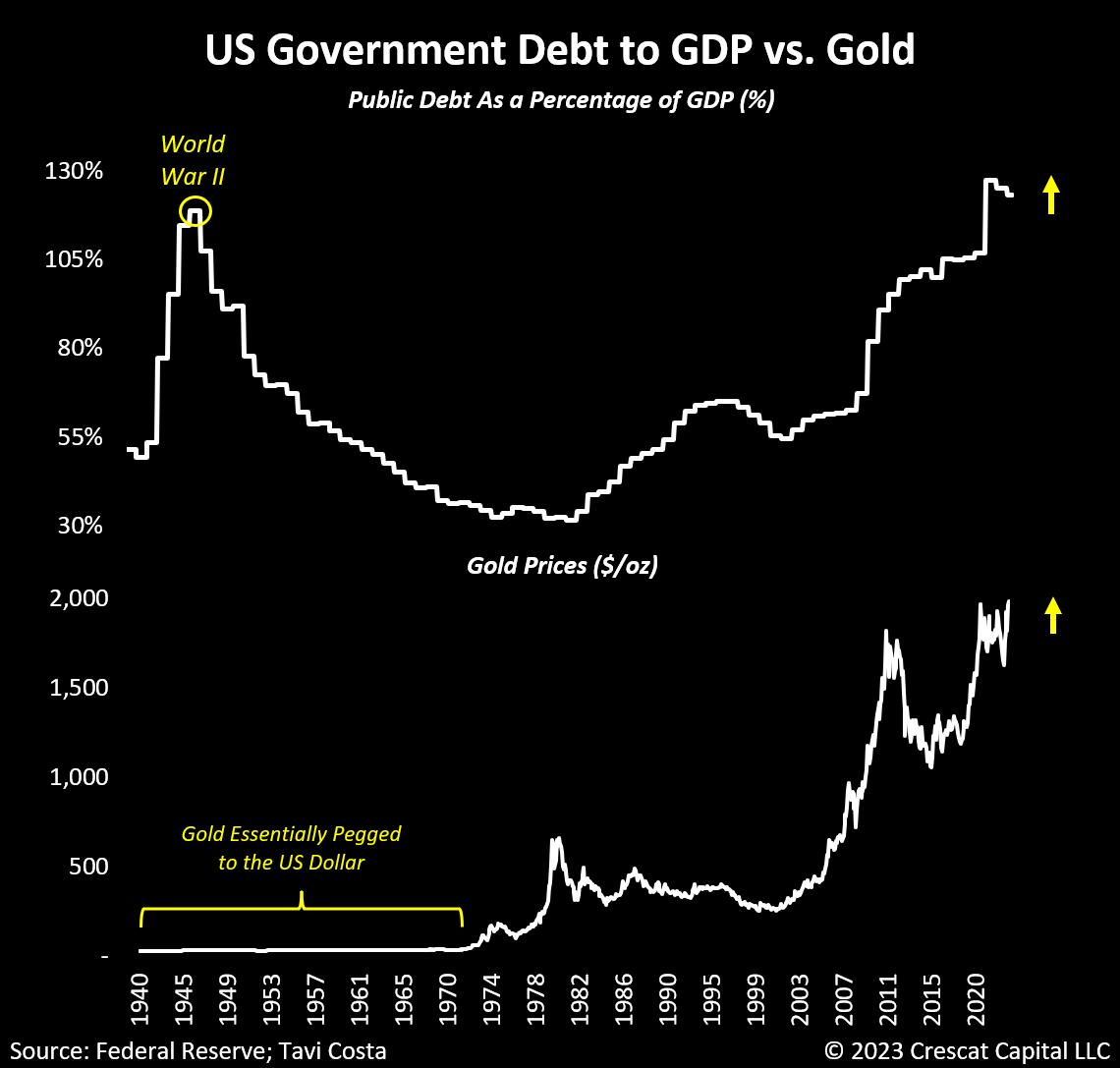

While the 1940s serve as an important historical parallel due to the seriousness of the current debt issue, there is a significant distinction:

During that period, gold was effectively tied to the US dollar, rendering it an impractical investment alternative.

During that period, gold was effectively tied to the US dollar, rendering it an impractical investment alternative.

Today, with prices unpegged, it is highly probable that capital will divert from US Treasuries and flow into gold.

We note that gold is the only macro asset trading near record prices today.

While there are inexorable fundamental drivers to push it much higher, from a technical perspective, the metal has recently encountered historical resistance after re-testing previous highs.

While there are inexorable fundamental drivers to push it much higher, from a technical perspective, the metal has recently encountered historical resistance after re-testing previous highs.

However:

Triple-top formations often prove to be temporary with prices eventually breaking out to the upside in a significant way.

Triple-top formations often prove to be temporary with prices eventually breaking out to the upside in a significant way.

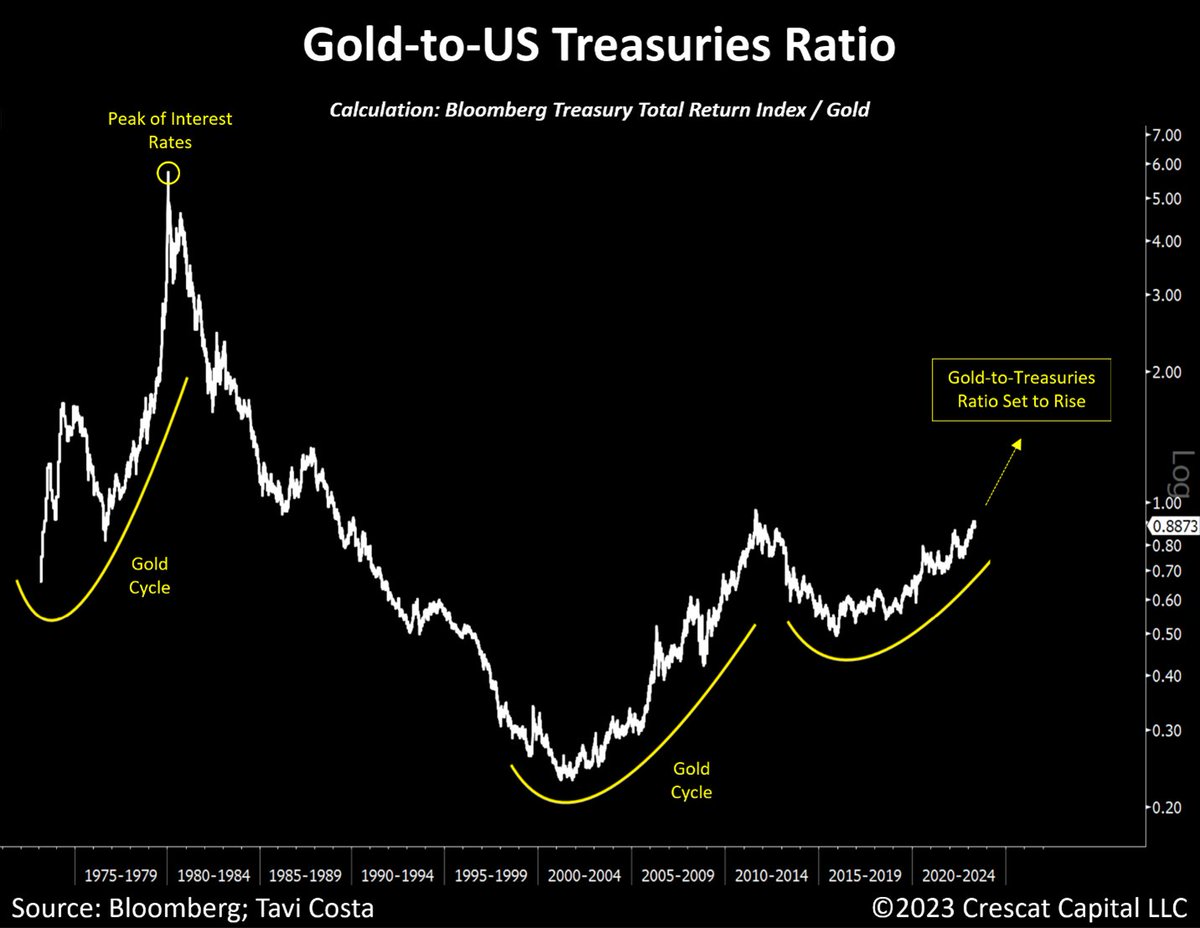

Once the metal decisively achieves record prices, it is likely to spark a new gold cycle.

These cycles, characterized by long-term trends, have occurred only twice in the past 50 years:

During the 1970s and the 2000s.

These cycles, characterized by long-term trends, have occurred only twice in the past 50 years:

During the 1970s and the 2000s.

The current market conditions present an exceptionally strong array of fundamental and macro drivers for precious metals, arguably the most robust in history.

Allow me to share some of them.

Allow me to share some of them.

1) Central banks compelled to purchase gold to enhance the quality of their foreign exchange reserves;

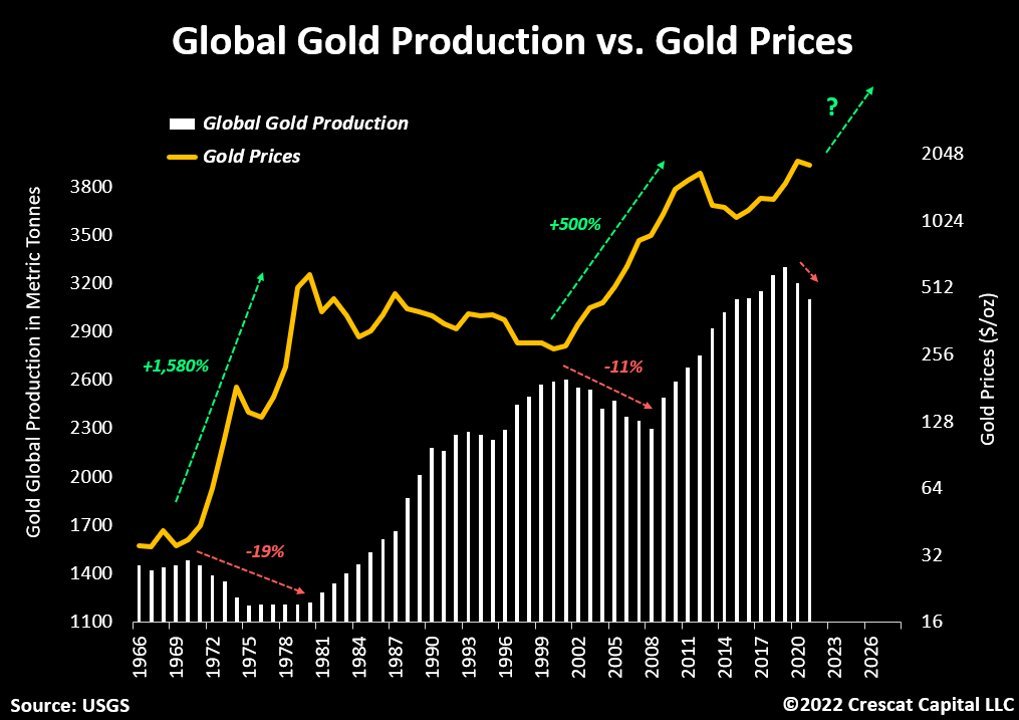

2) The likelihood of global gold production entering another secular decline, akin to the bull markets of the 1970s and 2000s which supports the supply side;

2) The likelihood of global gold production entering another secular decline, akin to the bull markets of the 1970s and 2000s which supports the supply side;

3) Failing 60/40 portfolios seeking alternative safe-haven assets;

4) Inflation expectations exceeding the historical average for this decade, driving the need for tangible assets;

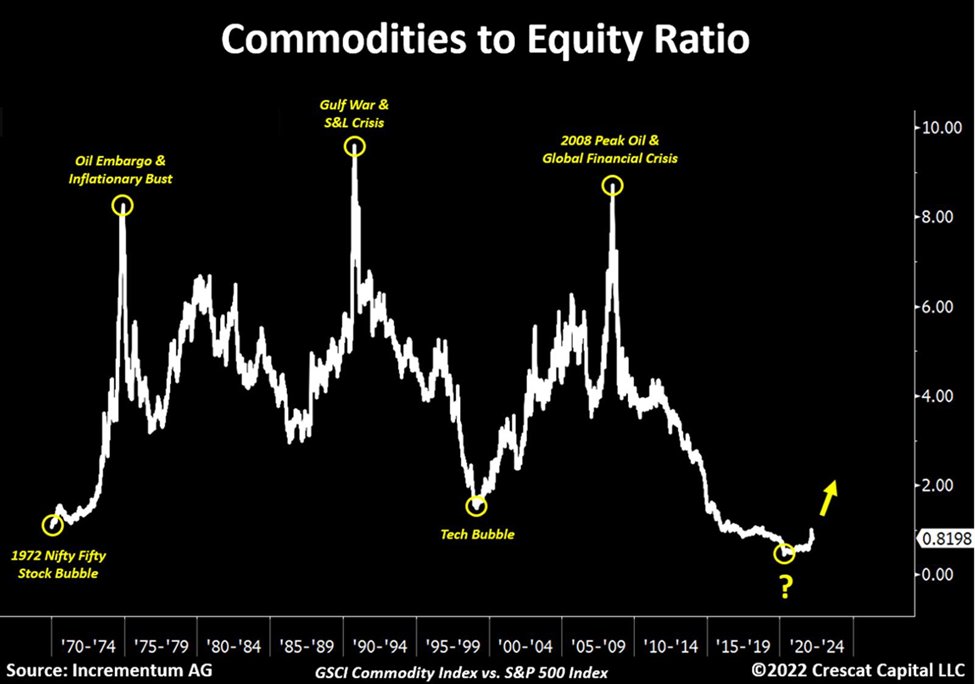

5) Commodities being historically undervalued compared to financial assets;

4) Inflation expectations exceeding the historical average for this decade, driving the need for tangible assets;

5) Commodities being historically undervalued compared to financial assets;

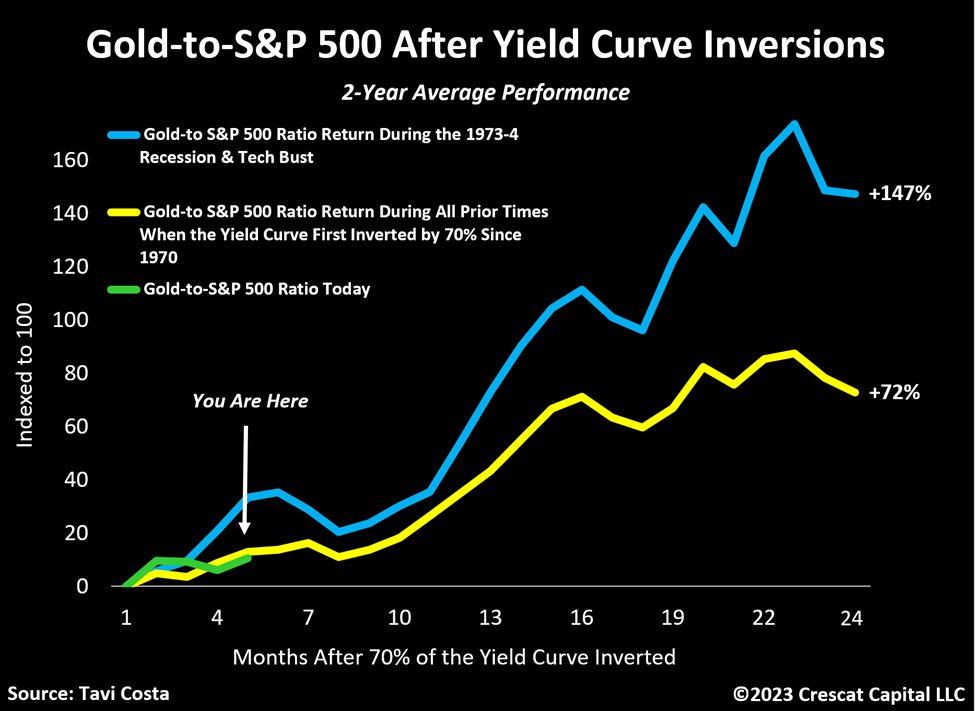

6) A significant number of yield-spread inversions in the US Treasury curve, surpassing the 70% threshold, making a compelling case for owning gold and reducing exposure to overvalued stocks;

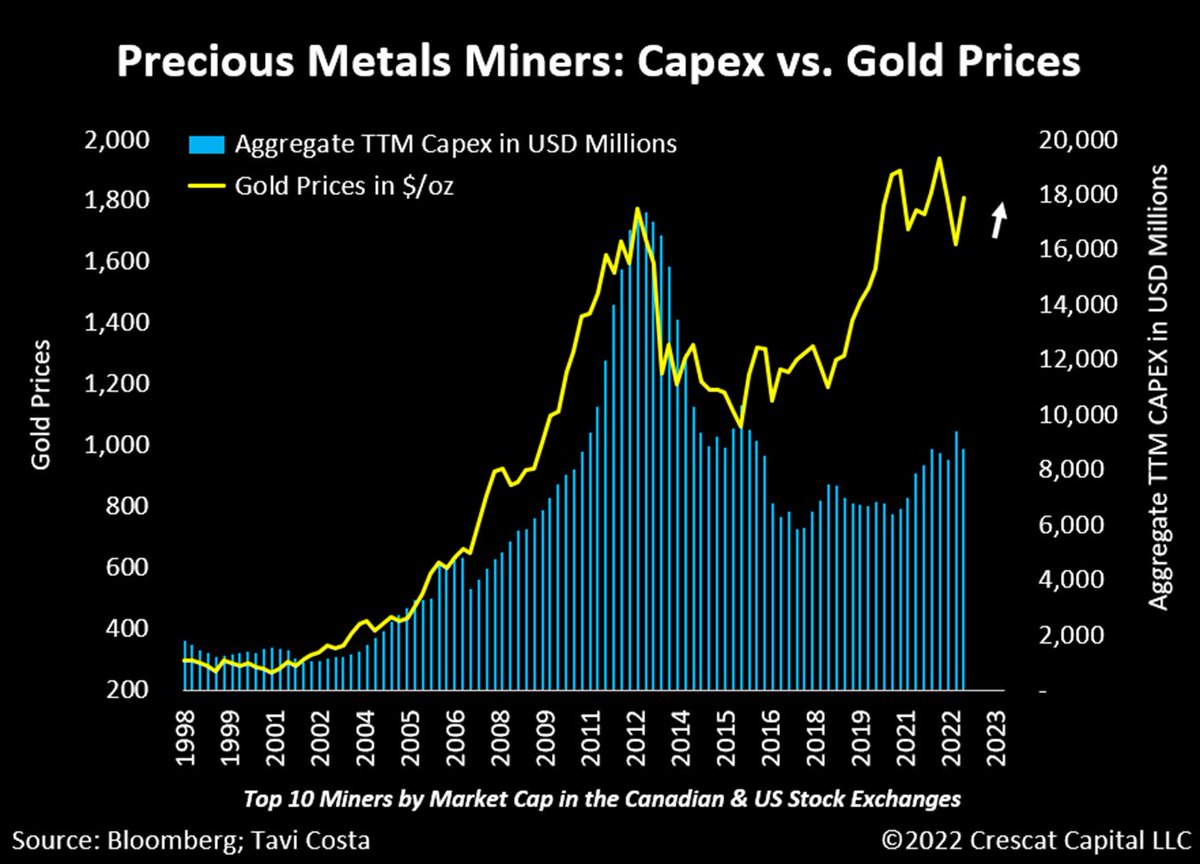

7) Major mining companies inclined to ultra-conservatism, prioritizing returning capital to shareholders over investing in the current and future production of precious metals;

8) Insufficient investments in exploration resulting in a lack of new gold and silver discoveries, compounded by the geological challenges of finding new mineral deposits;

9) ESG mandates and government pressure deterring the development of new resource projects;

10) Institutional investors pressuring traditional gold-focused companies to pivot to green metals;

10) Institutional investors pressuring traditional gold-focused companies to pivot to green metals;

10) The US and other developed economies are currently facing a trifecta of macro imbalances:

▪️ The debt problem reminiscent of the 1940s;

▪️ A speculative environment like the late 1920s and 1990s;

▪️ Inflationary concerns akin to the 1970s;

▪️ The debt problem reminiscent of the 1940s;

▪️ A speculative environment like the late 1920s and 1990s;

▪️ Inflationary concerns akin to the 1970s;

If you are interested in reading more, see below our latest research letter:

“Gold: A Far Superior Alternative”

crescat.net

“Gold: A Far Superior Alternative”

crescat.net

Loading suggestions...