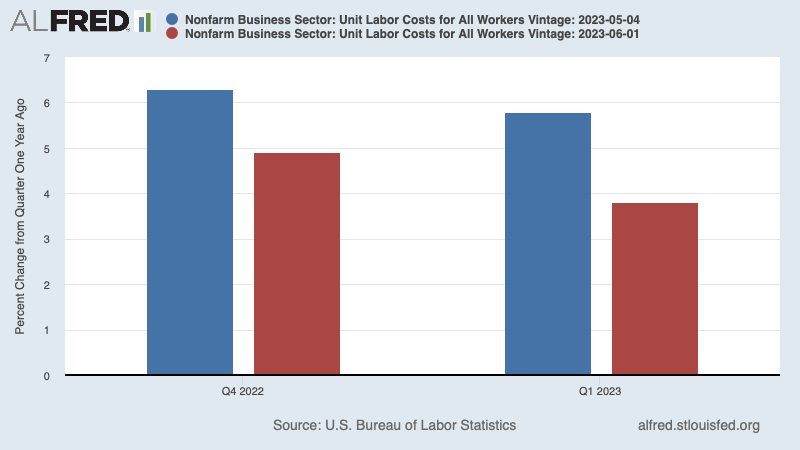

I've been saying for a while that the BLS is messing with our heads — or, actually, that in a time of big structural shifts different indicators give contrary indications, plus we get big revisions. So here's what the latest revisions have done to unit labor costs 1/

Some economists have been pointing to rapidly rising ULC as a reason for pessimism about inflation. But suddenly ULC is telling a much less dire story. In fact, it's suggesting major disinflation 2/

I've complained in the past that we talk a lot about "underlying" inflation without any clear model of what that means. But we do have a pretty clear model — Phelps/Taylor/Calvo — of "embedded" inflation, defined as ... 3/

inflation that would persist even if there's no major imbalance between aggregate supply and demand. In a world of staggered price and wage setting, this embedded inflation would reflect a combination of past cost increases and expected future increases 4/

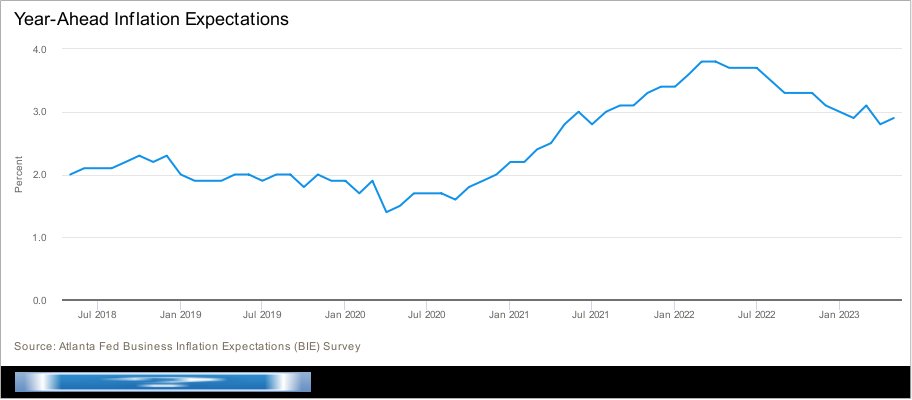

And we do have data on business expectations of future cost increases — more relevant and much more stable than consumer expectations, albeit only for Atlanta area. But still 5/

The Atlanta Fed also asks businesses how much their costs have risen over the past year. This number was much lower than pre-revision ULC; but now they're about the same 6/

So we have a declining rate of cost increases and declining expectations of future inflation. An average would still show embedded inflation slightly above 3 percent — but it's clearly down over the past year. Score one for immaculate disinflation hopes 7/

And maybe the Fed's job is done? 8/

Loading suggestions...