The most anticipated liquidity drain from markets is here, with many headlines foreseeing turbulence ahead. Yet, its effects might not deliver the impact many believe. Hidden forces have emerged, acting against a liquidity squeeze. The “Transitory Pause” is here... 1/

After an epic rise in stock prices in the first half of 2023, investors are wondering if the second half will produce the opposite outcome. A liquidity-fueled rally has driven the S&P500 up 12% so far this year. But now, the next significant "liquidity drain" is about to begin...

The latest political drama has ended in a debt ceiling suspension till 2025, allowing monetary leaders to fire up the printing press once again. The U.S Treasury, over the rest of 2023, is now set to issue a net ~$1 trillion of bills into the most systemically important market...

If history repeats, officials will aim to fill the U.S. govt's bank account, the Treasury General Account (TGA) within the Fed's system, with around $600 billion by September. Holding the master key to every commercial bank’s Fed account, the TGA will slowly amass reserves...

The consensus is concerned over two effects of the "TGA refill": a large issuance of government debt prompting market instability, and the subsequent draining of bank deposits and reserves reducing liquidity. The outcomes of both, however, aren't as scary as they appear...

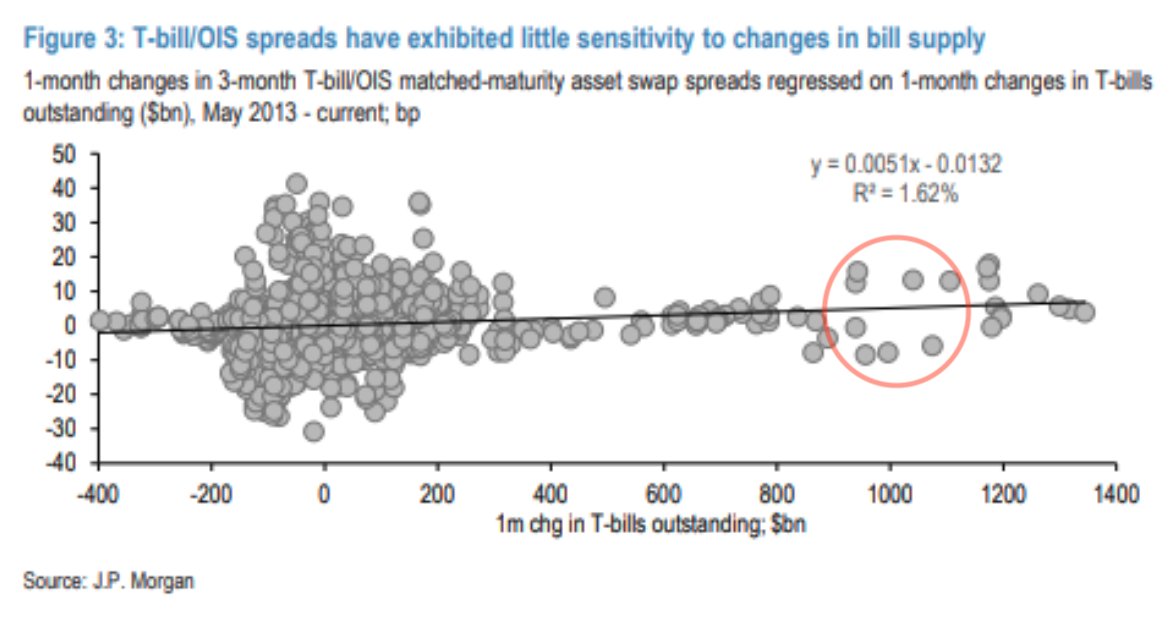

First, it's believed that issuing such a large quantity of t-bills in a short space of time will be difficult for markets to absorb, blowing out spreads and provoking turmoil. But as history shows, bond markets absorb huge issuances, even within a month, without much hassle...

As for demand, with yields offering the highest return in decades, plus the switch from an unsecured (LIBOR) to a “secured” (SOFR) monetary standard in full swing, the world is eager to chomp on America’s ever-increasing debt load. Financial behemoths are hungrier than ever...

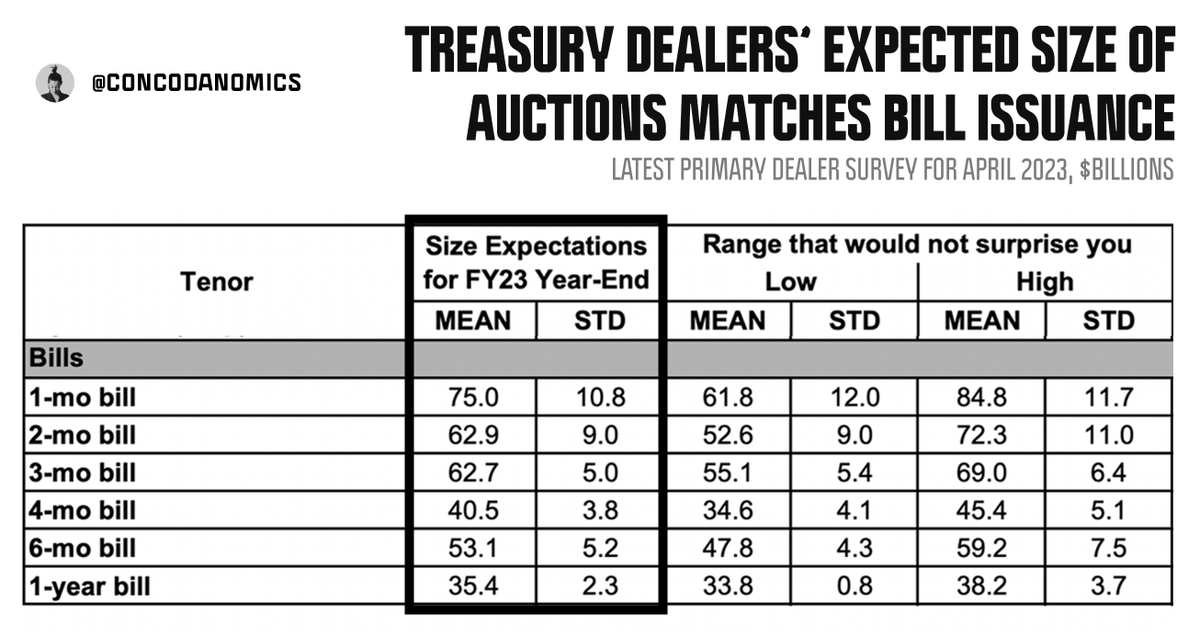

We also know in advance that major market players are willing to consume a large batch of sovereign debt by referring to the Fed's latest survey of its primary dealers, specific entities the Fed mandates to make markets in Treasuries. Expected supply is in line with demand...

Instead, it's not whether market participants will be able to absorb trillions in new issuance but who buys the majority of Treasuries issued that will influence liquidity. The real concern is the subsequent liquidity drain from the banking system. The coast isn't clear...

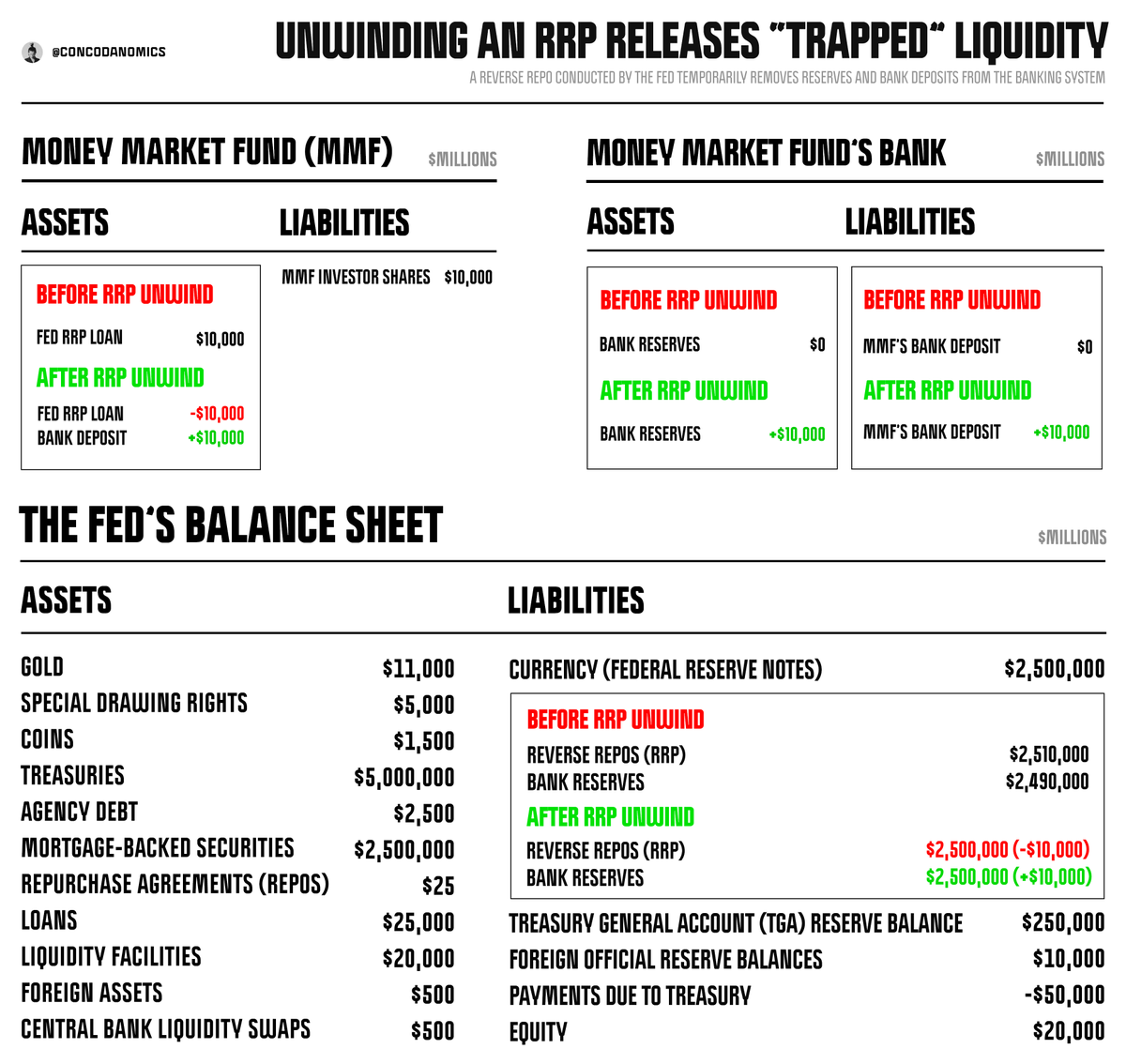

The most bullish scenario for liquidity is if most t-bills are bought with cash stored mostly by money market funds (MMFs) and some banks in the Fed's RRP (reverse repo) facility. This is where, after factoring in regulation and risk vs. reward, most excess cash ends up...

For the uninitiated, repo (short for repurchase agreements) is a market for borrowing securities, usually Treasuries, for a fee overnight or over another short period. An RRP (reverse repo) is the opposite perspective: cash is lent, secured by collateral, and earns interest...

RRPs conducted by the Fed are the most illiquid type of money market investment available. While t-bills and most other repo agreements can be liquidated intraday to raise cash, the RRP "traps" liquidity by only allowing access to cash after 3:30 pm...

The TGA refill could cause MMFs to unwind RRPs, transforming illiquid RRP liabilities on its balance sheet into highly liquid reserves. But this won't increase liquidity in the banking system. It will merely transform one form of trapped liquidity into another...

Just like when it initially invested in an RRP, the MMF's t-bill payment removes deposits from the banking system and "neutralizes" reserves, which this time are sent to the U.S. government's bank account at the Fed (the TGA), withdrawing liquidity from the private sector...

Reserves are "neutralized" since the cash can't be deployed by private entities into the economy or assets. As for the t-bill the MMF bought, it's highly unlikely to be liquidated. Thus, after a "TGA refill bill" has been funded by RRP cash, "liquidity" remains neutral...

It's not as easy for MMFs, however, to simply pull money from the RRP to fund new t-bills. They have to be incentivized to do so. MMFs, after all, are investment vehicles looking to maximize their returns while under the watch of regulators. Specific conditions are required...

For a sizeable "RRP drain" to even have a chance of occurring, 1-month Treasury yields must rise not only above the RRP rate but also SOFR (the Secured Overnight Financing Rate), the rate for private repos conducted on the same platform the Fed uses for RRP trades...

Due to regulation, government-only MMFs, the most common type of MMF, prefer investing in overnight repos (SOFR and RRP) rather than 1-month bills. These funds must maintain a WAM (weighted average maturity) of 60 days or less, and overnight repos count as a zero-day maturity...

Overnight repos also provide ample day-to-day liquidity while juicing returns. Consequently, the spread between bill yields and repo (SOFR and RRP) must widen significantly for MMFs to find bills tempting. Thus the chance that they step up is lower than many envision...

If MMFs aren't tempted to absorb bills using RRP cash, failing to dampen the effects of a TGA refill, a sea of other willing buyers will step in, from onshore corporate treasurers to offshore banks to international organizations. If so, deposits and reserves will tumble...

But the decrease in reserves and deposits caused by these entities ingesting billions in bonds is not the only type of liquidity impacting financial markets. While the narrative of a "TGA refill" crushing risk assets has risen to prominence, opposing forces have emerged...

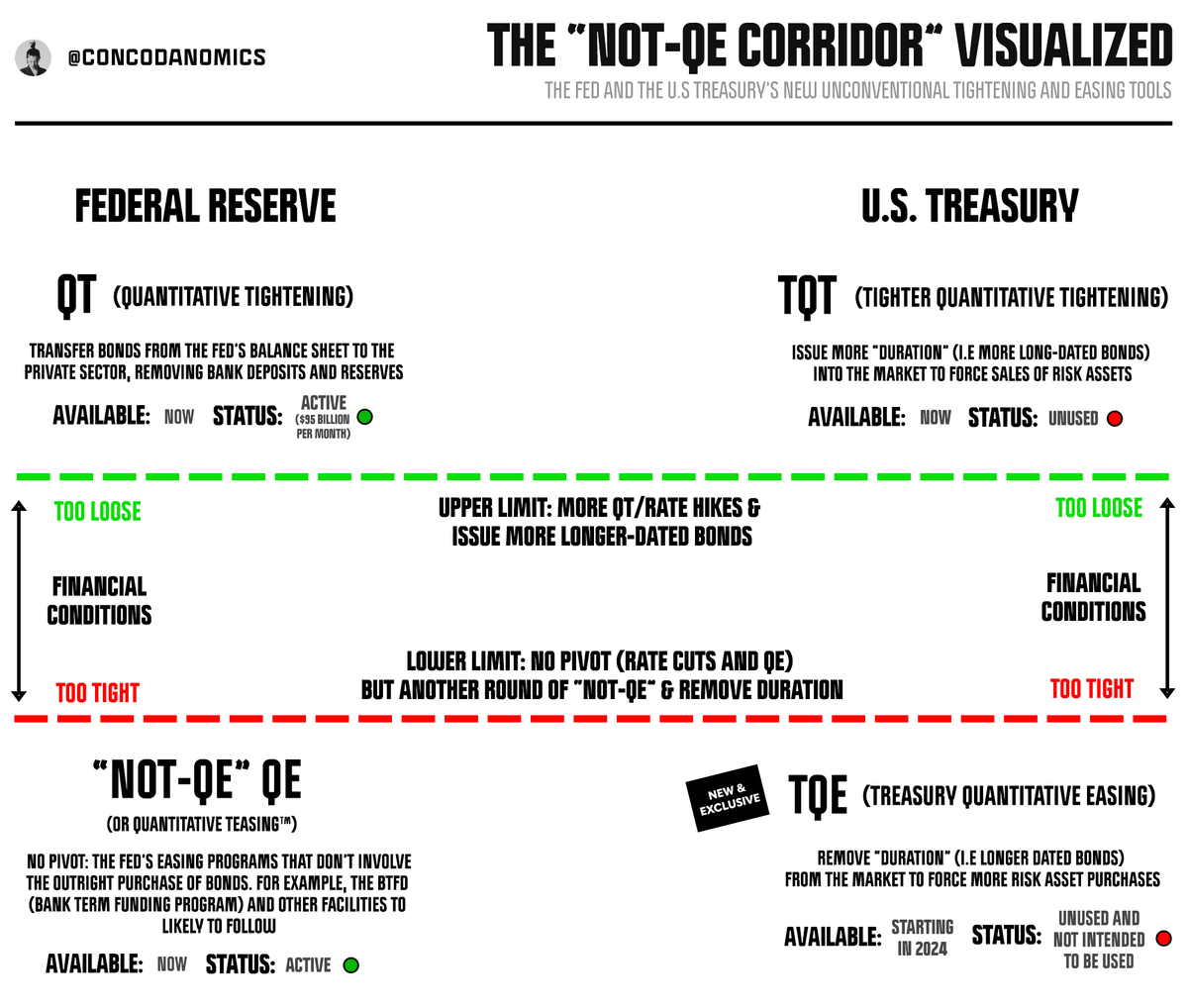

Not only have we moved toward the upper limit of, what Conks calls, the Not-QE Corridor, signifying a loosening of financial conditions. Silently, the Fed has temporarily withdrawn from signaling tightness. With the "Fed skip" in play, the Transitory Pause is now in session...

A Transitory Pause is a combination of the Fed’s inaction and silence around enforcing an adequate tightening of financial conditions. The market has been repressed by heightened volatility and uncertainty for so long, that when it sniffs out dovishness, risk assets respond...

Previous measures the Fed has implemented to quell financial conditions have proven ineffective, or even defunct, and fail to discourage animal spirits. QT (quantitative tightening), which on its own has failed to achieve actual tightening, is even offset by other forces...

Meanwhile, a sharp hiking regime has been replaced by the idea that the Fed could possibly pause for good, thereby enabling volatility to tumble and flows to resume into financial assets, uninhibited. With the Transitory Pause in play, the world's natural long bias has awoken...

Retirement funds, no longer weighing increased vol (volatility) and rate hike intensity, have stopped rebalancing out of stocks into bonds, while entities that load up on stocks solely on falling vol have been buying like crazy. Bond vol plunging has also spurred more activity...

The icing on the cake for the risk asset rally was the Fed’s recent silence. What’s more, the market has likely been frontrunning the “blackout period,” which currently limits FOMC staff's ability to speak publicly or be questioned. The Transitory Pause has reached max potency...

If the “Not-QE” era persists, front-running the Fed’s silence and inaction to tighten will become a regular window in which risk assets soar. The “Transitory Pause” will eventually become a defining theme in markets. But right now, we’re only within an early iteration...

The Fed will likely once again intervene and reiterate its tightening stance, which they’ve seemingly forsaken over the past few months. The latest Transitory Pause will end, not via a “TGA refill”, but by a more powerful trigger: the return of a hawkish Fed.

Thanks for reading! If you enjoyed this, feel free to retweet the top tweet of this thread and follow @concodanomics for more.

You can also subscribe below to receive more in-depth articles about finance, markets, and geopolitics in your inbox...

👉 concoda.substack.com 👈

You can also subscribe below to receive more in-depth articles about finance, markets, and geopolitics in your inbox...

👉 concoda.substack.com 👈

Loading suggestions...