In this Detailed Thread 🧵 I'll look to Analyse 'HPL ELECTRIC & POWER'⚡⚡ Fundamentals, Financials, Technicals, Management, Order Book, Growth Potential💹, Industry Trigger, Valuation Metrics♎⚖️, Competitors, Risk Factor, Peers Comparison etc| Part 2

🏅Fundamental Analysis

✅Market Capitalisation:-Rs 683 Cr

✅Stock PE:- 22.6

✅Industry PE:- 33.7

✅ROCE:- 8.87%

✅ROE:- 3.83%

✅Book Value:- Rs 123

✅Intrinsic Value: Rs 101

✅Graham No:- Rs 114

✅Pledged Percentage:- 0

✅Piotroski Score:- 8

✅Debt to Equity:- 0.76

✅Market Capitalisation:-Rs 683 Cr

✅Stock PE:- 22.6

✅Industry PE:- 33.7

✅ROCE:- 8.87%

✅ROE:- 3.83%

✅Book Value:- Rs 123

✅Intrinsic Value: Rs 101

✅Graham No:- Rs 114

✅Pledged Percentage:- 0

✅Piotroski Score:- 8

✅Debt to Equity:- 0.76

✅Debt:- Rs 600 Cr

✅Reserves:- Rs 729 Cr

✅Fixed Assets:- Rs 451 Cr

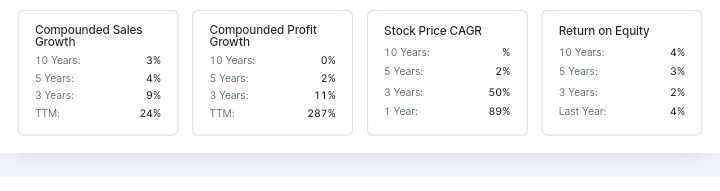

✅Sales Growth:- 24.5%

✅Profit Growth:- 287%

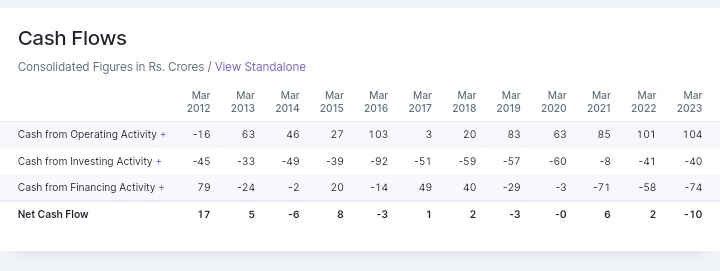

Last 3/5/10 Years Profit Growth, Sales Growth, ROCE, Accounting Ratios🧾,Cash Flow Statement♎⚖️ 👇

✅Reserves:- Rs 729 Cr

✅Fixed Assets:- Rs 451 Cr

✅Sales Growth:- 24.5%

✅Profit Growth:- 287%

Last 3/5/10 Years Profit Growth, Sales Growth, ROCE, Accounting Ratios🧾,Cash Flow Statement♎⚖️ 👇

🏅Financial Analysis, Chart Pattern analysis, Valuation Metrics⚖️♎, Comparison with Peers, Trigger, Concall Notes, Management

💫Financial Results Analysis

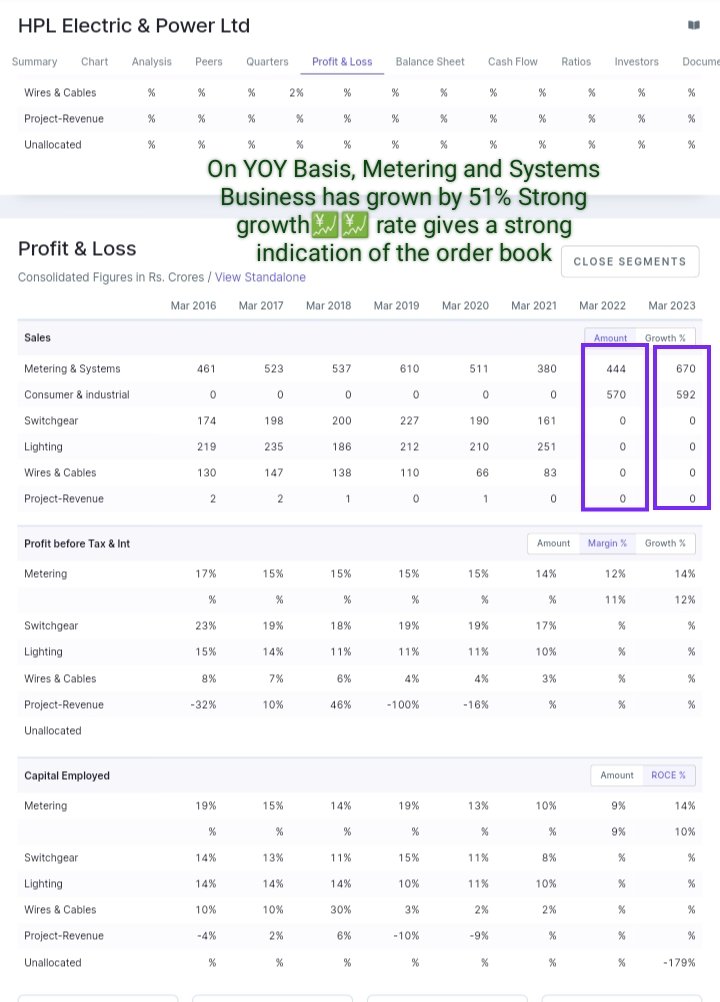

✅HPL ELECTRIC has witnessed a very good Quarter in Q4FY23

✅The company Sales has increased by about 24.48%,

💫Financial Results Analysis

✅HPL ELECTRIC has witnessed a very good Quarter in Q4FY23

✅The company Sales has increased by about 24.48%,

Operating Profits have increased by about 25.6% and Net Profits has increased by about 275% on YOY Basis💹💹

✅HPL ELECTRIC witnessed its highest ever Revenue and Operating Profits in its History in FY23

✅The company EPS has increased from 1.21 to 4.69 on YOY Basis

✅HPL ELECTRIC witnessed its highest ever Revenue and Operating Profits in its History in FY23

✅The company EPS has increased from 1.21 to 4.69 on YOY Basis

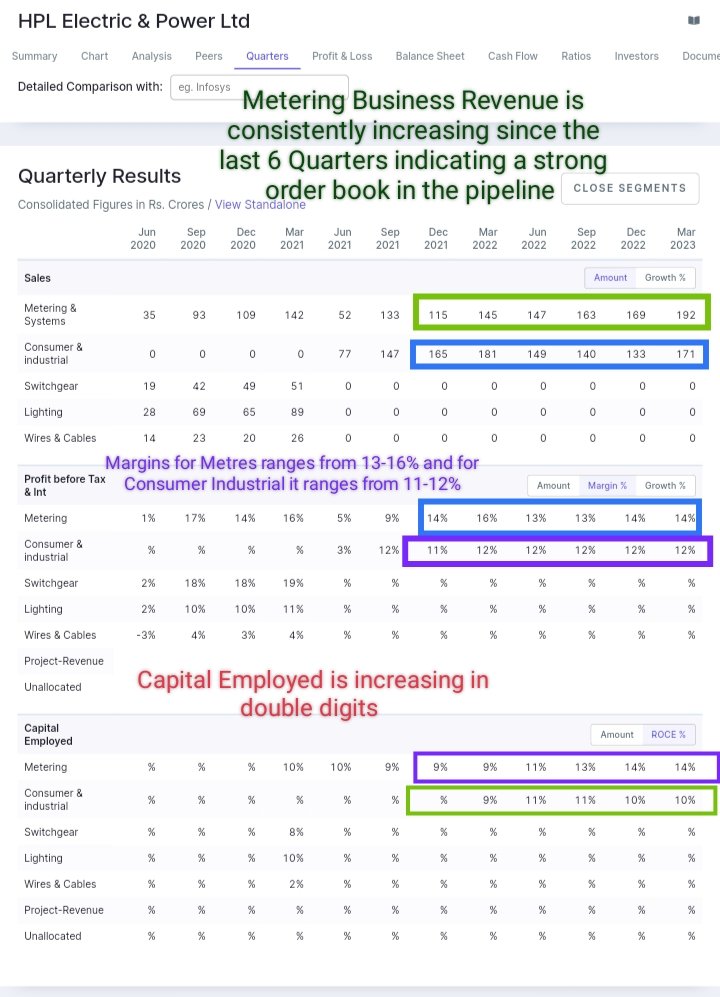

✅It is to be noted that HPL ELECTRIC has two Business Verticals:-

1.Metering & Systems:- It Contributes to 55% of Revenue and;

2.Consumer & Industrial (Switchgear+Lightings+Wires & Cables):- It contributes to 45% of Revenue

1.Metering & Systems:- It Contributes to 55% of Revenue and;

2.Consumer & Industrial (Switchgear+Lightings+Wires & Cables):- It contributes to 45% of Revenue

✅HPL ELECTRIC is performing exceptionally well in the Metering & Systems Business its Revenue is continuously increasing 6 Quarters in this segment since Dec-2021 reflecting a robust order book for the company(Since FY23 Q2 Metering Business is growing at more than 20% on QOQ

Basis)

✅Consumer Segment is little stagnant but the company expects good growth in FY24 by growing at double digits pace(As per Concall)

✅The Margins for Metering Segment is at 14% and for Consumer it is at 12%

✅The ROCE has improved considerably and are in double digits

✅Consumer Segment is little stagnant but the company expects good growth in FY24 by growing at double digits pace(As per Concall)

✅The Margins for Metering Segment is at 14% and for Consumer it is at 12%

✅The ROCE has improved considerably and are in double digits

💫Chart Pattern📉📈

✅CMP of the Stock is Rs 106

✅The Stock is trading above all the EMAs and DMAs

✅Daily RSI is at 68, Weekly RSI is at 68 and Monthly RSI is at 66(The Stock has yet not gone in Overbought Zone)

✅The stock will give a 6 Months old BO above Rs 115

✅CMP of the Stock is Rs 106

✅The Stock is trading above all the EMAs and DMAs

✅Daily RSI is at 68, Weekly RSI is at 68 and Monthly RSI is at 66(The Stock has yet not gone in Overbought Zone)

✅The stock will give a 6 Months old BO above Rs 115

✅In June 2022, the Stock made a bottom @50.80 and then it went till Rs 115 and then it again came to Retest Rs 75 in March-April 2023 Corrections

✅Now, after 6 Months it is very close to its Breakout Zone

✅HPL ELECTRIC ⚡⚡ will give a 7.5 Years old Breakout above Rs 116

✅Now, after 6 Months it is very close to its Breakout Zone

✅HPL ELECTRIC ⚡⚡ will give a 7.5 Years old Breakout above Rs 116

✅There's a good Margin of Safety

✅This Stock will become weak only below Rs 94 as there's a sign of Accumulation from the lower levels with big volumes

✅This Stock will become weak only below Rs 94 as there's a sign of Accumulation from the lower levels with big volumes

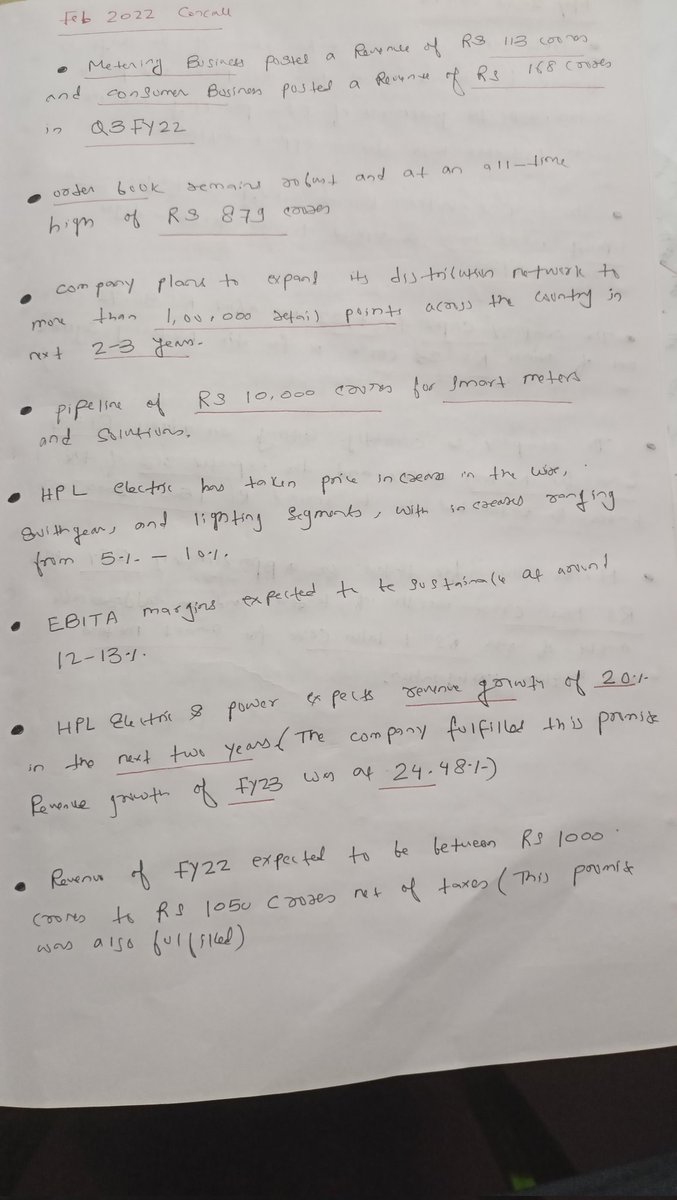

🏅Last 8 Concall Notes (From August 2021 to June 2023) Took me 10-12 Hours to study the Concall in details, I've highlighted the most important points by underline

Important Highlights:-

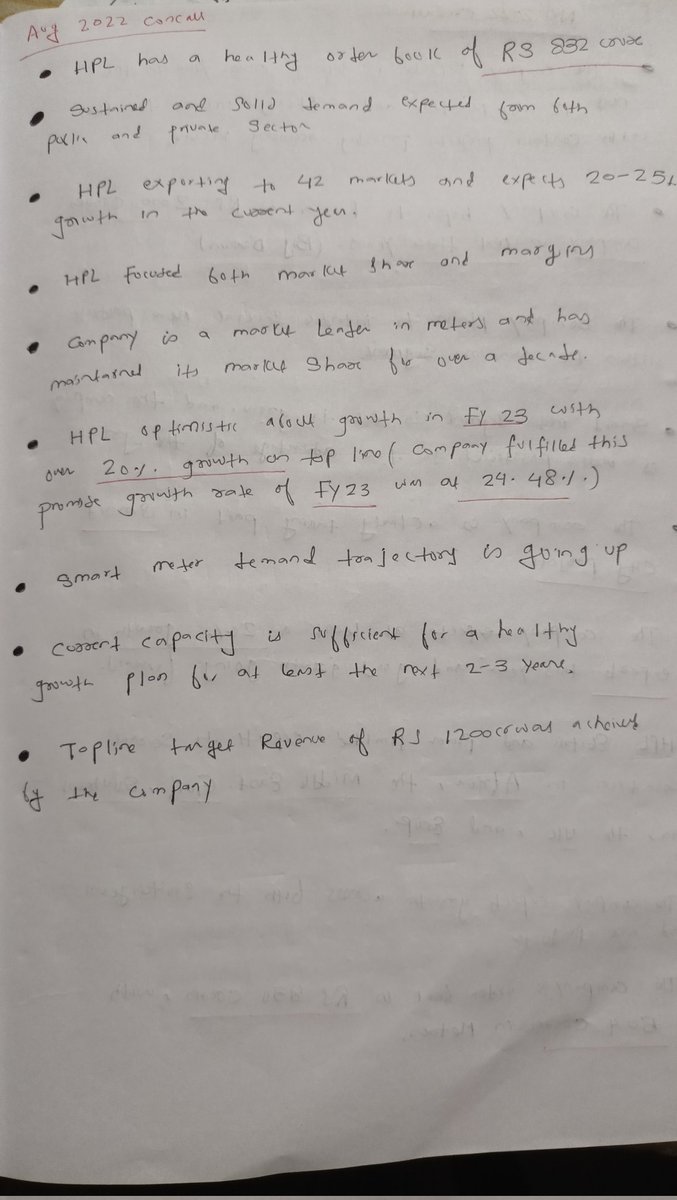

💫The company had a order book of only Rs 704 Cr in Q4 FY21 and in 2 years this Order Book

Important Highlights:-

💫The company had a order book of only Rs 704 Cr in Q4 FY21 and in 2 years this Order Book

Has increased to Rs 1550 Cr

💫The company is maintaining a winning rate of 22-23% in Smart Meter tenders and it has about 20-25% Market Share

💫The Company could benifit from the government announcements Rs 3.03 lakh Crores of power distribution schemes including 25 Crores

💫The company is maintaining a winning rate of 22-23% in Smart Meter tenders and it has about 20-25% Market Share

💫The Company could benifit from the government announcements Rs 3.03 lakh Crores of power distribution schemes including 25 Crores

Smart Meters.

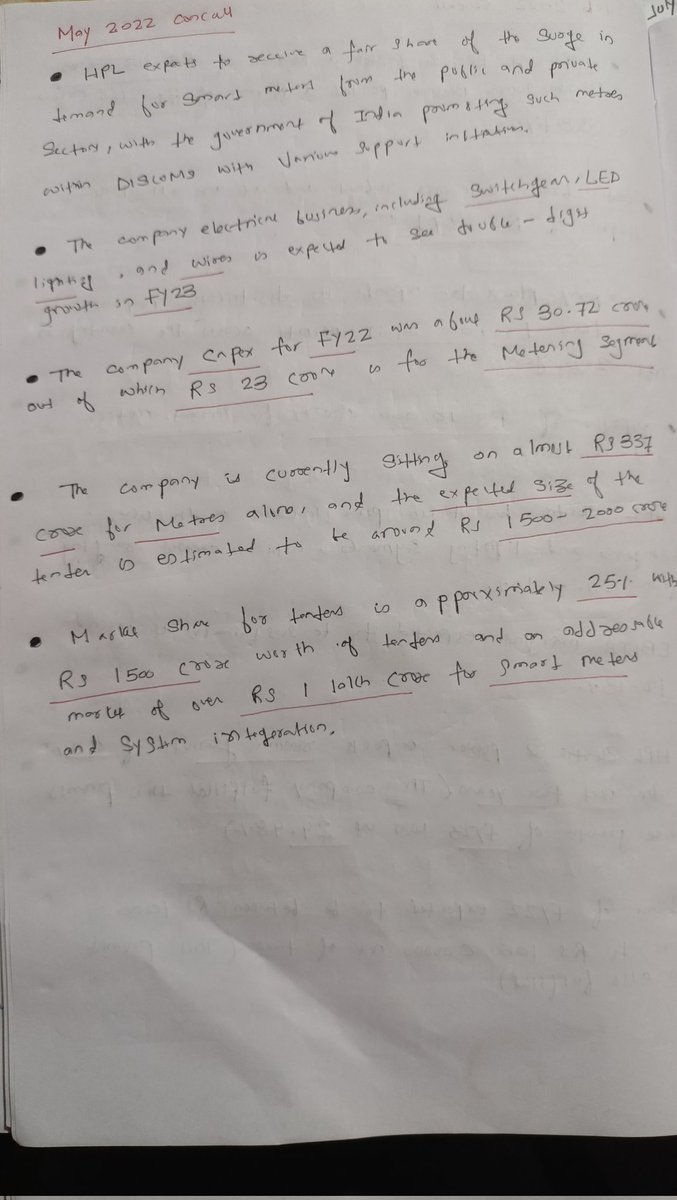

💫HPL has invested into new Products and it exports to 42 Markets

💫The company is working to become debt free in the consumer Business in next 3-4 years(As per Concall Notes of Aug-2021)

💫HPL is focused in Smart in Electric metres but it has the capability to

💫HPL has invested into new Products and it exports to 42 Markets

💫The company is working to become debt free in the consumer Business in next 3-4 years(As per Concall Notes of Aug-2021)

💫HPL is focused in Smart in Electric metres but it has the capability to

Add water & gas meters

💫Pipeline of Rs 10,000 Crores order book for Smart Meters

💫Company did a CAPEX of Rs 30.72 Cr in FY22 of which Rs 23 was for the Metering Systems

💫Smart Meters trajectory is going up

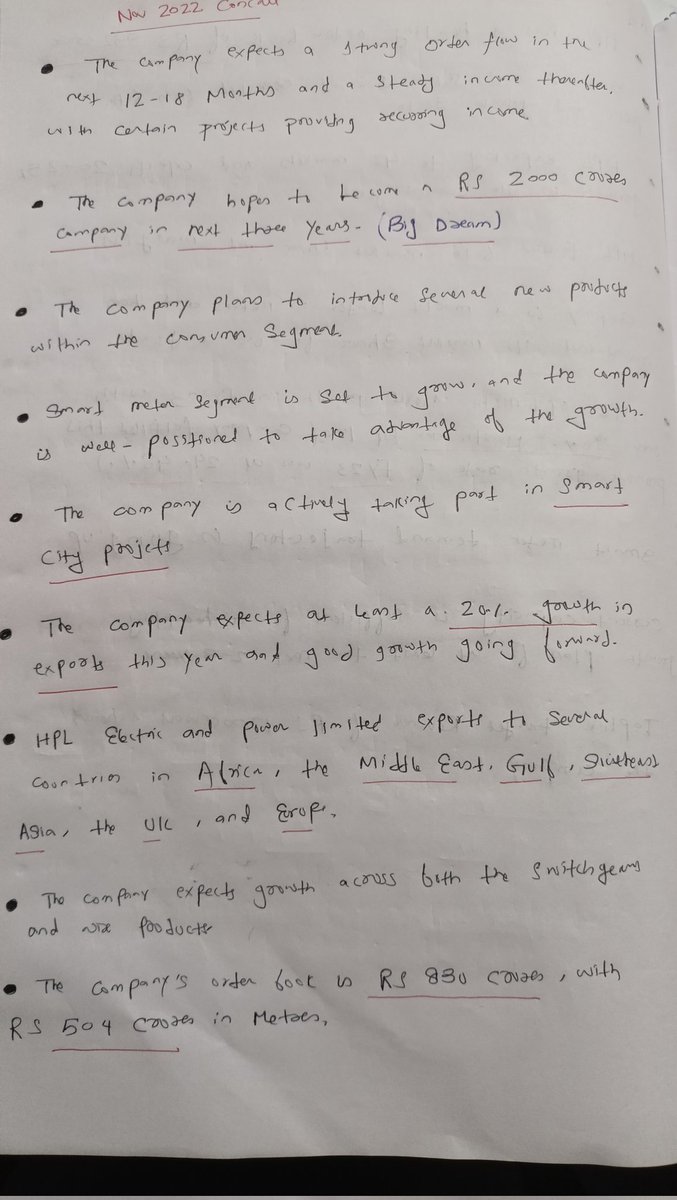

💫The company hopes to become a Rs 2000 Cr Company in next three

💫Pipeline of Rs 10,000 Crores order book for Smart Meters

💫Company did a CAPEX of Rs 30.72 Cr in FY22 of which Rs 23 was for the Metering Systems

💫Smart Meters trajectory is going up

💫The company hopes to become a Rs 2000 Cr Company in next three

Years(As per Nov-2022 Concall Big Dream)

💫The company exports to several markets like Africa, the Middle East, Gulzar Southeast, Asia, Uk and the Europe

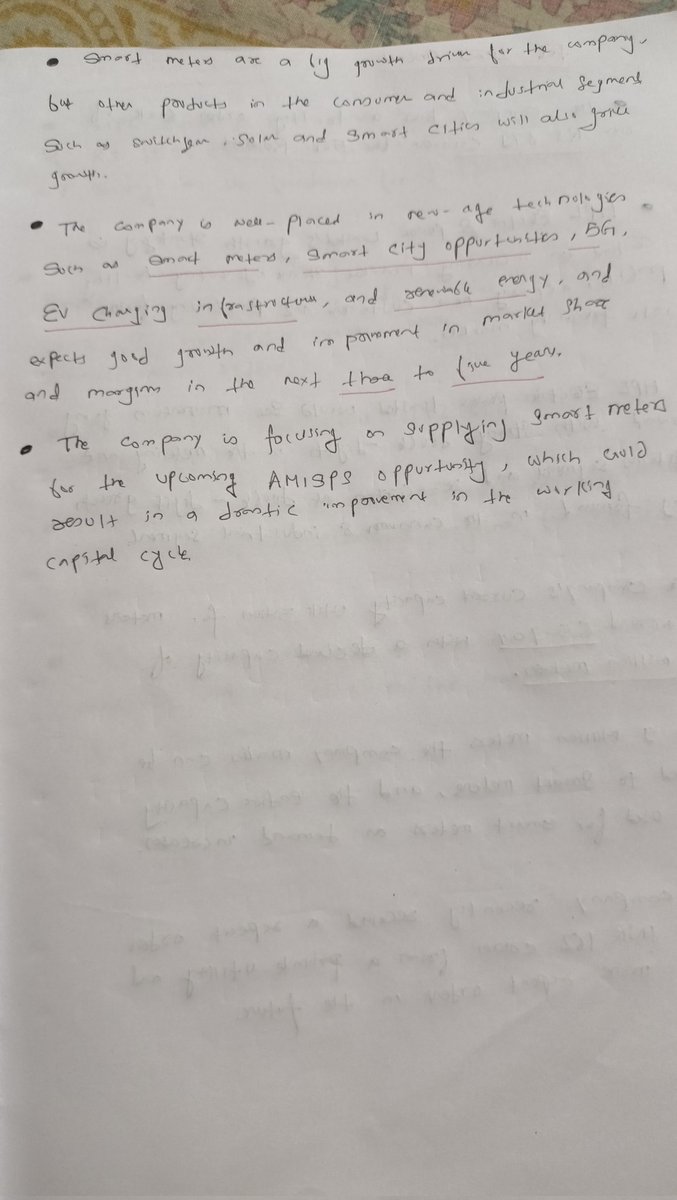

💫The company is well placed in new- age technologies such as Smart Meters, Smart City Opportunities, 5G, EV

💫The company exports to several markets like Africa, the Middle East, Gulzar Southeast, Asia, Uk and the Europe

💫The company is well placed in new- age technologies such as Smart Meters, Smart City Opportunities, 5G, EV

Charging, infrastructure and renewable energy and expects good growth and improvement in market share and margins in the next three to five years

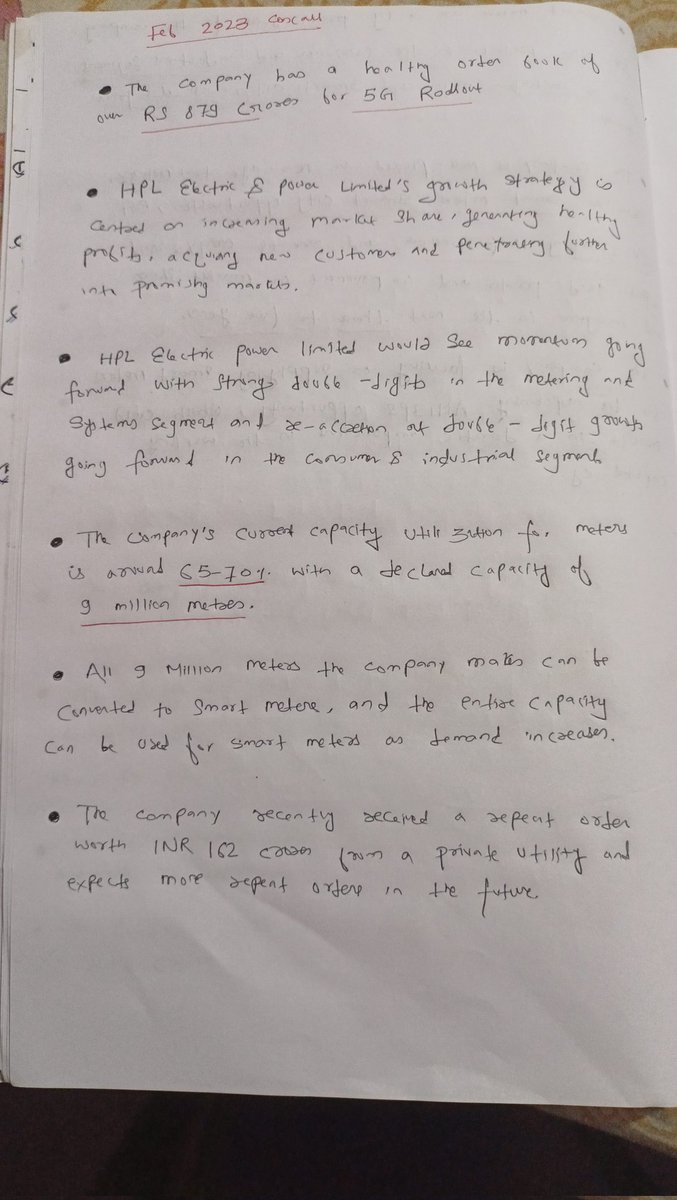

💫The company current capacity utilisation for meters is around 65-70% with a declared capacity of 9 Million Metres

💫The company current capacity utilisation for meters is around 65-70% with a declared capacity of 9 Million Metres

💫All 9 Million Metres can be converted into Smart Meters, and the entire Capacity can be used for Smart Meters as demand increases

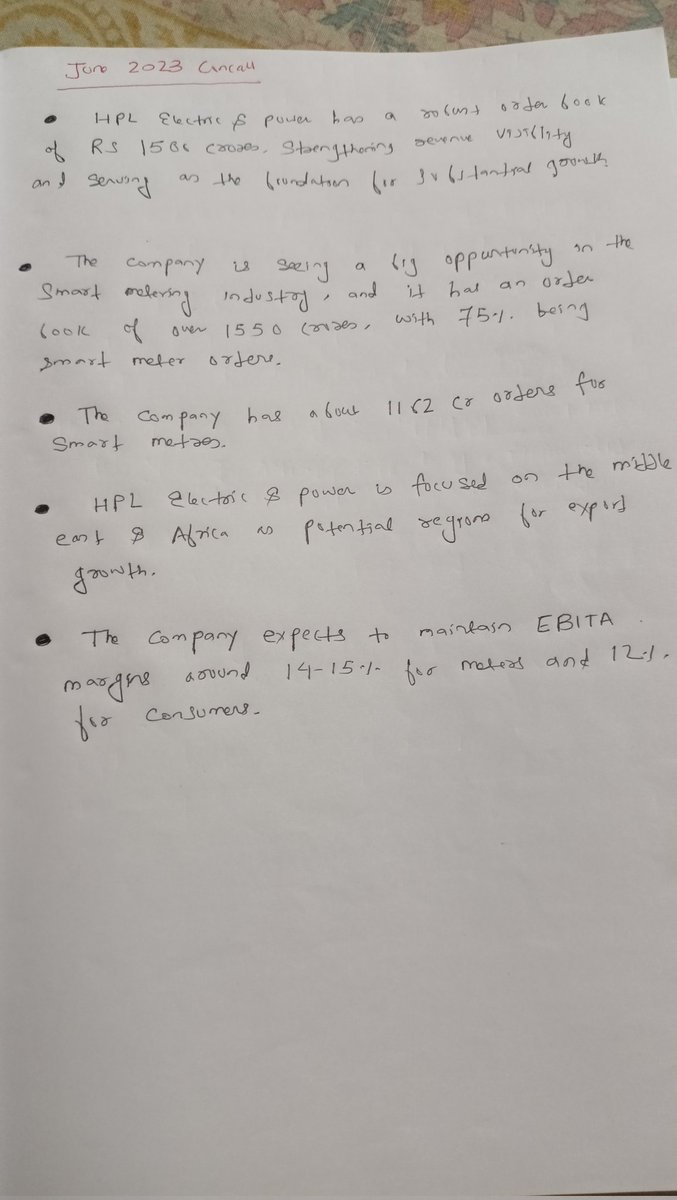

💫As per most recent June 2023 Concall, the Company has a robust order book of Rs 1550 Cr of which 75% is from Smart Meters of Rs 1160 Cr is from

💫As per most recent June 2023 Concall, the Company has a robust order book of Rs 1550 Cr of which 75% is from Smart Meters of Rs 1160 Cr is from

Smart Meters and rest 25% or Rs 390 Order is from Consumer & Industrial

💫The company expects a margin of 14-15% for the Metering Business and 12% for the Consumer Industrial Business

💫The company has focused for 20% Growth in FY24

💫The company expects a margin of 14-15% for the Metering Business and 12% for the Consumer Industrial Business

💫The company has focused for 20% Growth in FY24

Loading suggestions...