Usha Martin - A business undergoing transformation

Highlights from #UshaMartin 2023 Annual Report and May 2023 concall.

Highlights from #UshaMartin 2023 Annual Report and May 2023 concall.

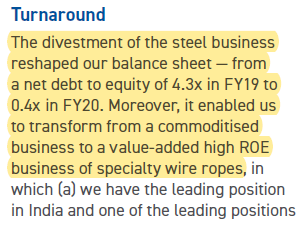

For those of you who remember, we had covered Usha Martin's turnaround story @

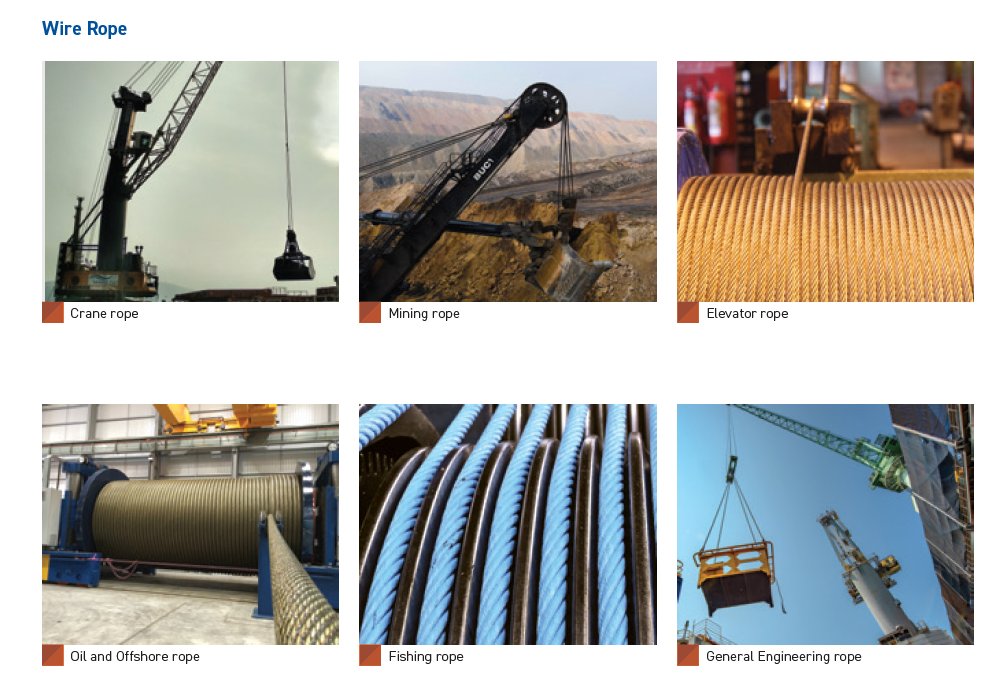

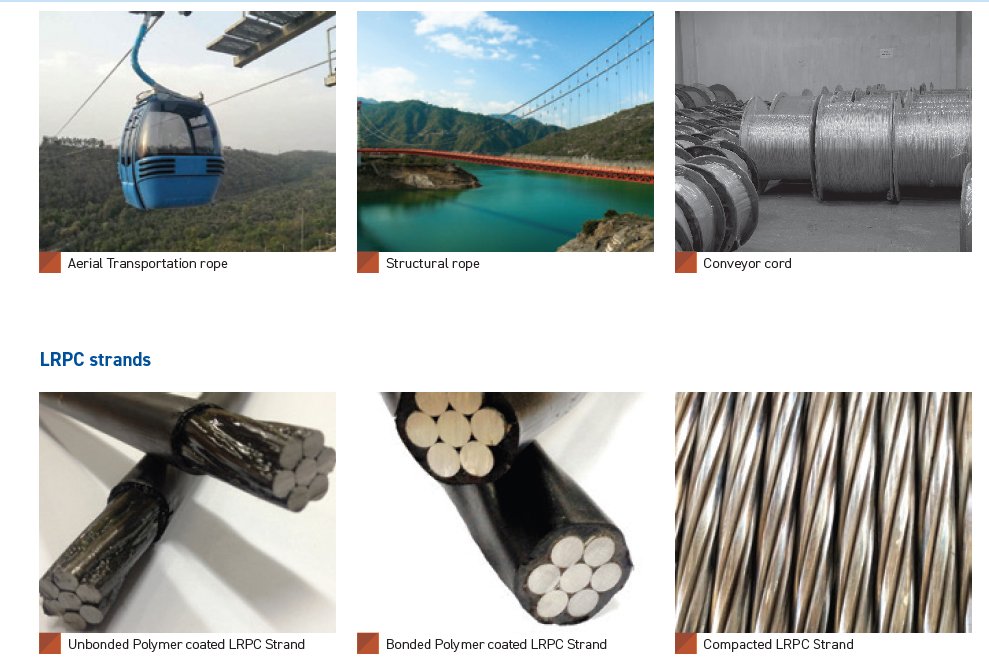

What does Usha Martin make?

Before we proceed please share this thread because we've invested many hours creating this content for you.

Your retweets inspire us to keep delivering value & help spread knowledge with our other investor friends.

Join the 68 amazing people who retweeted our HBL Power thread.

Your retweets inspire us to keep delivering value & help spread knowledge with our other investor friends.

Join the 68 amazing people who retweeted our HBL Power thread.

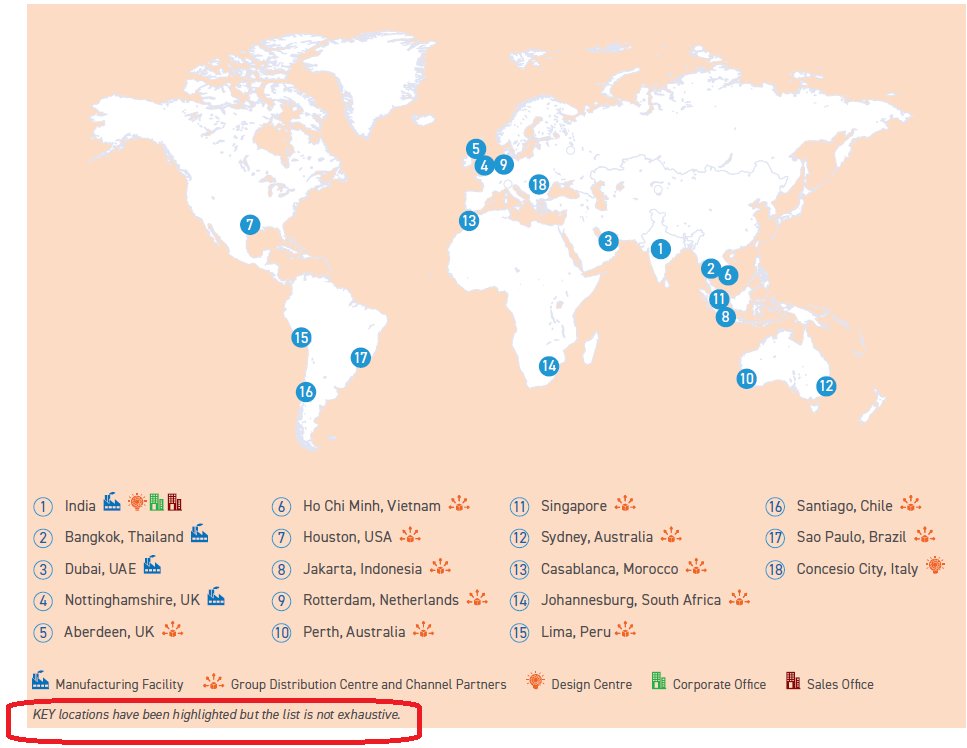

Usha Martin has key manufacturing facilities in India, Thailand, UAE & UK.

Design centres in India and Italy.

Design centres in India and Italy.

Distribution Centers and Channel partners in 17 countries.

Foreign subsidiaries

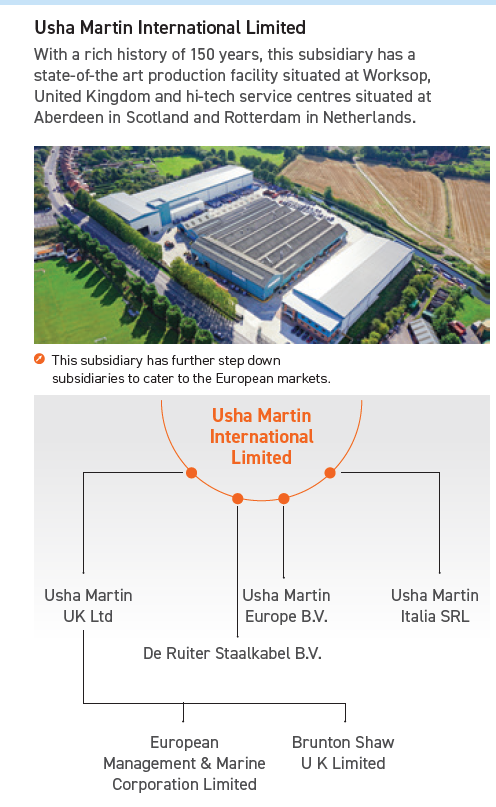

UK - Wire rope products, Shackles, Slings, Lifting and Rigging gear including Marine Mooring equipment and Anchoring systems

Netherlands - Specialty wire rope solutions

UK - Wire rope products, Shackles, Slings, Lifting and Rigging gear including Marine Mooring equipment and Anchoring systems

Netherlands - Specialty wire rope solutions

Singapore - Steel wire rope products including mooring rope, crane rope, slings and accessories required in marine, offshore, oil exploration, mining and industrial applications.

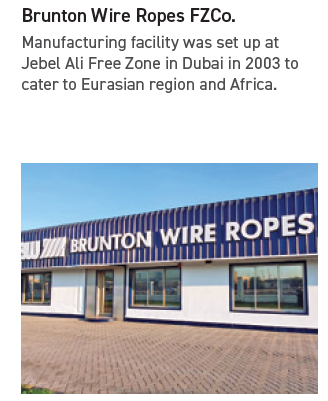

Brunton Wire Ropes - Dubai.

Steel wire ropes for oil & gas, crane, general engineering, fishing, dredging, mining, and elevator applications.

Customers - Major oil giants, mining groups, elevator OEMs, and big rigging companies.

Steel wire ropes for oil & gas, crane, general engineering, fishing, dredging, mining, and elevator applications.

Customers - Major oil giants, mining groups, elevator OEMs, and big rigging companies.

Being strategically located at Jebel Ali, Dubai (World's 9th largest port) has helped Brunton Wire's customers to get ropes faster in all parts of the world.

Usha Siam Steel Industries, Thailand - Caters to countries in the South East Asia-Pacific region.

Manufactures steel wire rope, automotive control cable, fine rope, strand and specialty wire.

Manufactures steel wire rope, automotive control cable, fine rope, strand and specialty wire.

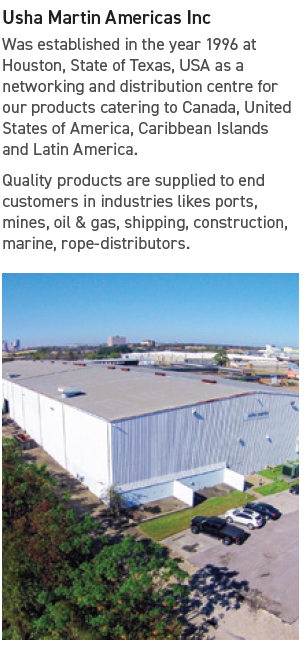

Usha Martin Americas - Networking and distribution centre for Canada, United States of America, Caribbean Islands and Latin America

Customers - Ports, mines, oil & gas, shipping, construction, marine, rope-distributors

Customers - Ports, mines, oil & gas, shipping, construction, marine, rope-distributors

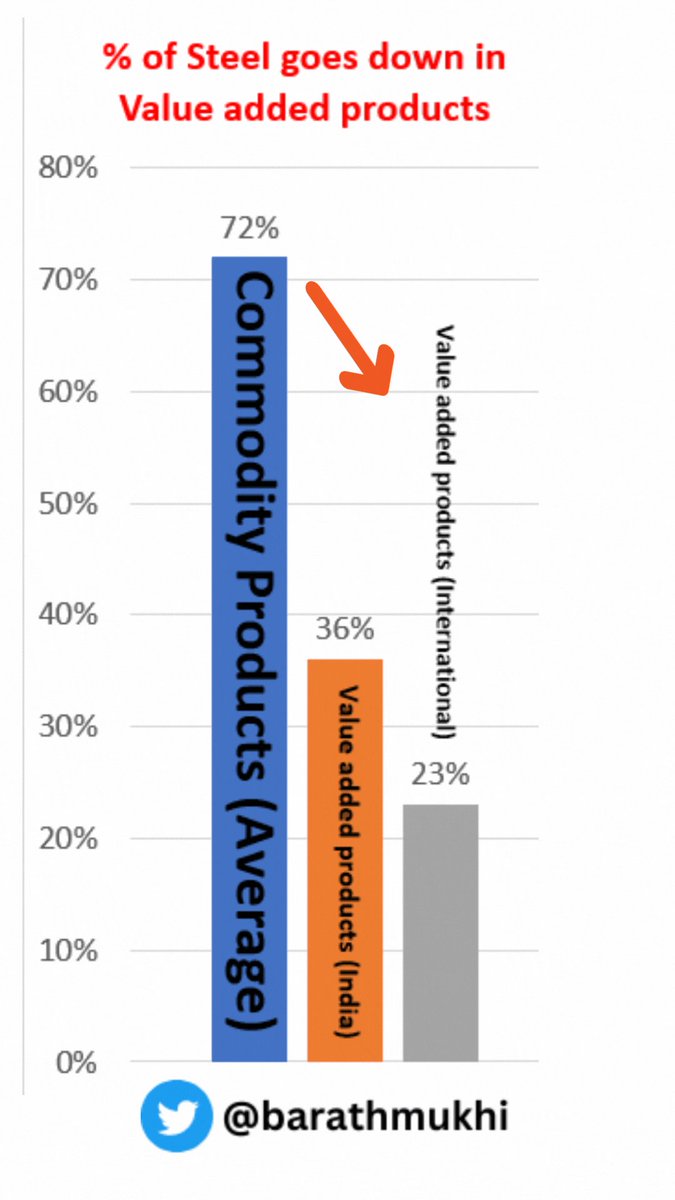

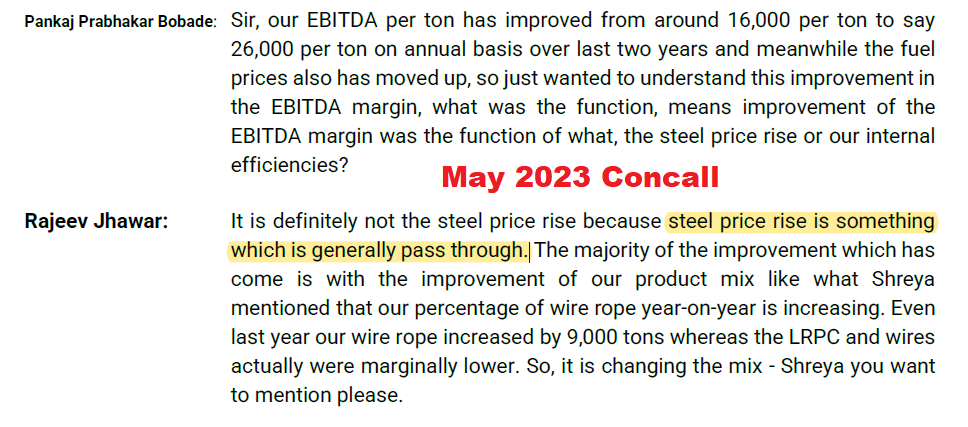

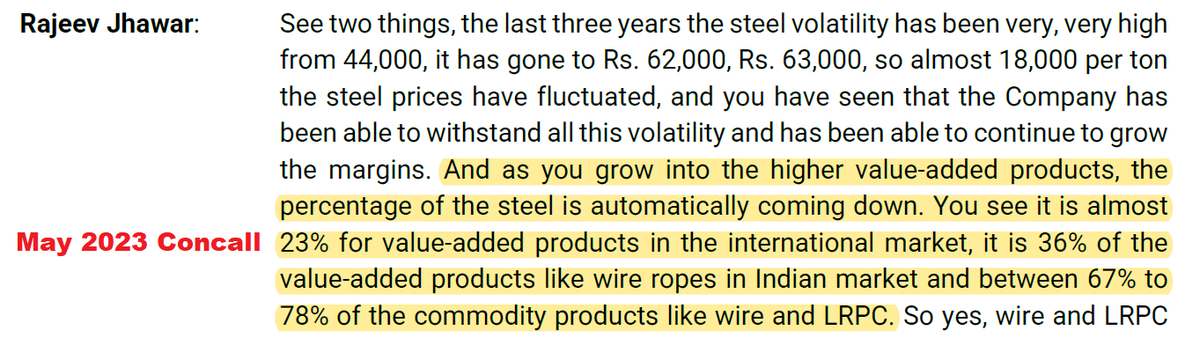

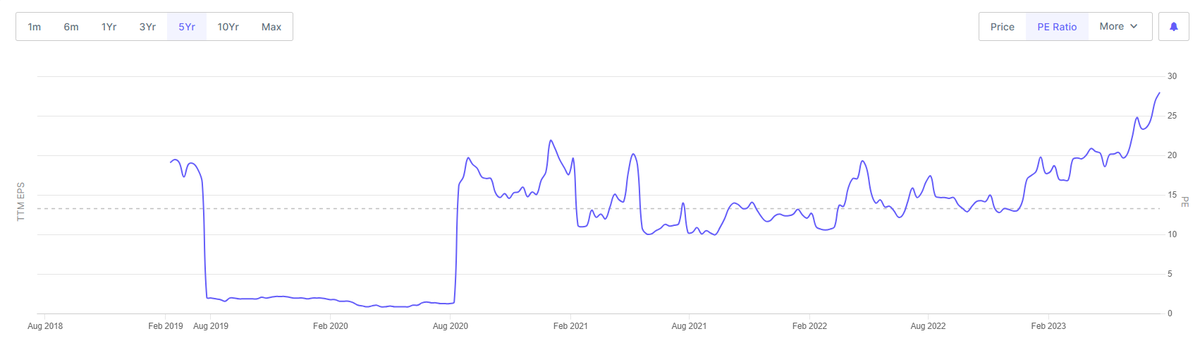

In their 2023 AR, mgmt is saying they are able to grow despite volatility in commodity prices.

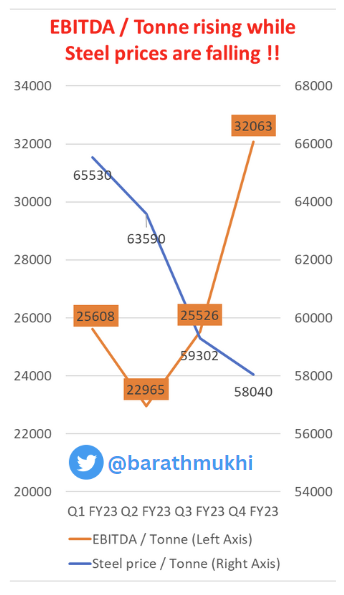

In the turnaround thread we had covered the fact that Usha Martin is indeed able to grow even in the face of falling steel prices.

In FY 2023, the steel industry was under pressure because of multiple issues such as supply chain disruptions, RM cost inflation, increase in freight costs, etc.

Yet, Usha Martin were able to grow their profits by 20%

And that happened because Usha Martin has been shifting towards value-added products, focusing on unique features to achieve better margins rather than relying solely on the quantity of raw materials like steel.

The above graph tallies with the management's claim that steel price is now a pass through.

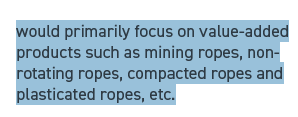

So which of their products are value added?

Some of them are mining ropes, non-rotating ropes, compacted ropes and plasticated ropes.

Some of them are mining ropes, non-rotating ropes, compacted ropes and plasticated ropes.

Production of value added products increased by 2.5%.

Also note the lesser component of steel in the pricing of exports because realizations are better in international markets.

2023 annual report also states they are focusing on high value products to improve margins.

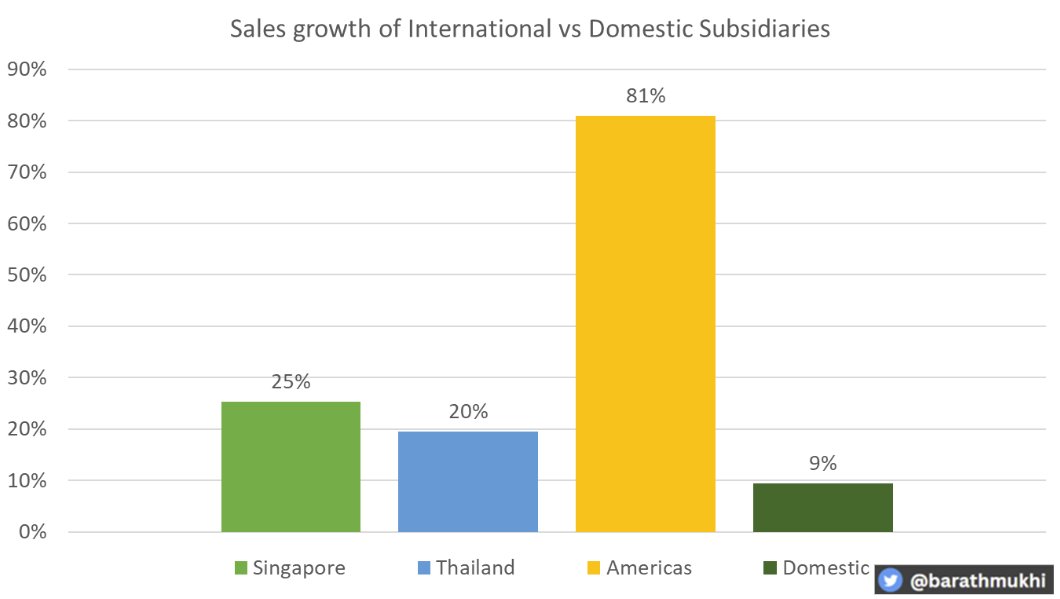

This explains why Usha Martin is trying to grow exports faster than their domestic business.

Click Show Replies to continue reading the thread.

Click Show Replies to continue reading the thread.

Exports growing faster than domestic business

And 55% of their overall sales comes from Exports.

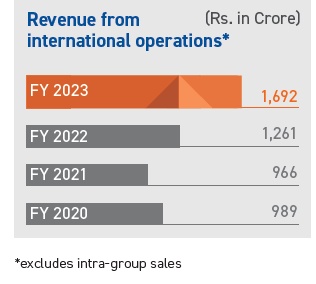

2023 exports revenue of 1692 Crs.

Plans to expand presence in countries where it has limited presence.

Focus is also on services business and value added products.

Improving organizational structure.

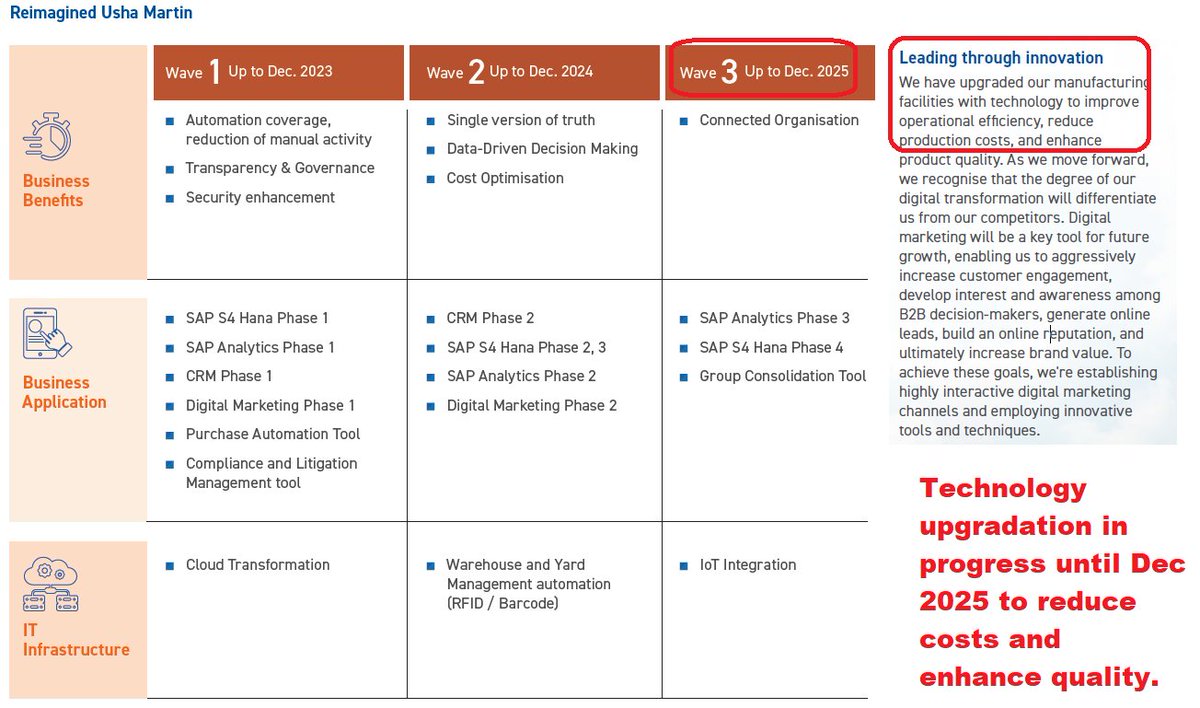

Technology upgradation to drive cost reduction and further improve operational efficiencies.

Key growth segments - Ports, mining, elevator, oil and offshore.

Capex expected to come online within FY 2024.

167 Crs of Capex planned in FY 2024.

Capex 75% from internal accruals.

20-25% from debt.

20-25% from debt.

With asset turns of 2-3x.

Peak revenue potential of 1431 Crs, in a bull case scenario.

(310+167 Capex * 3x Asset turns = 1431 Crs)

Peak revenue potential of 1431 Crs, in a bull case scenario.

(310+167 Capex * 3x Asset turns = 1431 Crs)

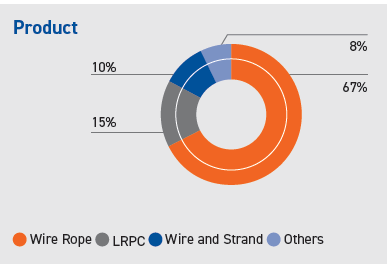

Revenue breakup.

67% from Wire Ropes. This is where most of the malaai is.

33% from others.

67% from Wire Ropes. This is where most of the malaai is.

33% from others.

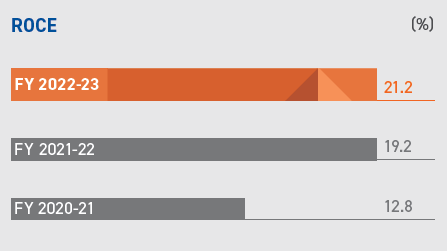

ROCE has been steadily improving.

Expected to go up further.

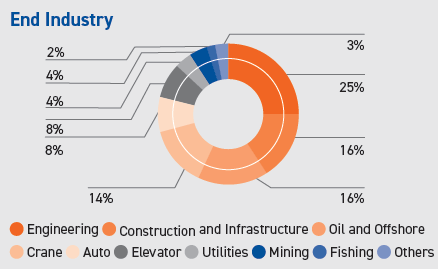

End industries - Mainly Engineering, Infra, Oil & Offshore and Crane contribute 71%.

Other industries contribute 29%

Other industries contribute 29%

Expect 15% CAGR growth in topline until 2025-2026.

Operating EBITDA target of 18%.

Operating EBITDA target of 18%.

Ending this thread with some anti-thesis pointers.

Usha Martin's business is heavily dependant on the macro environment.

Any disruptions at the macro level that can cause a slowdown in end user industries could lead to a slowdown in Usha Martin's business.

Usha Martin's business is heavily dependant on the macro environment.

Any disruptions at the macro level that can cause a slowdown in end user industries could lead to a slowdown in Usha Martin's business.

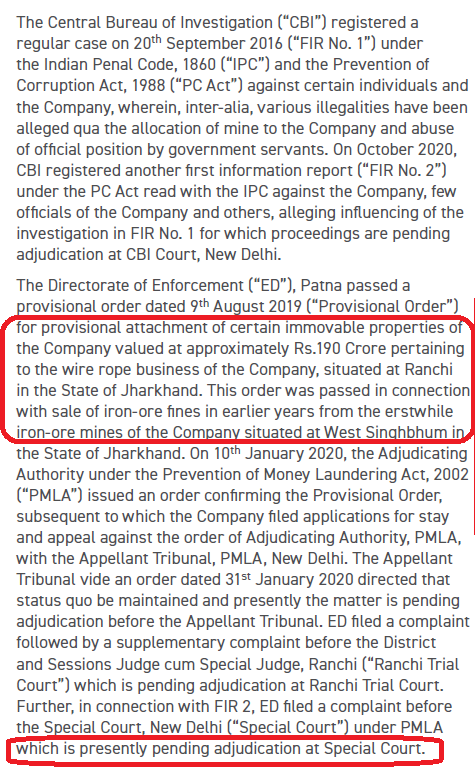

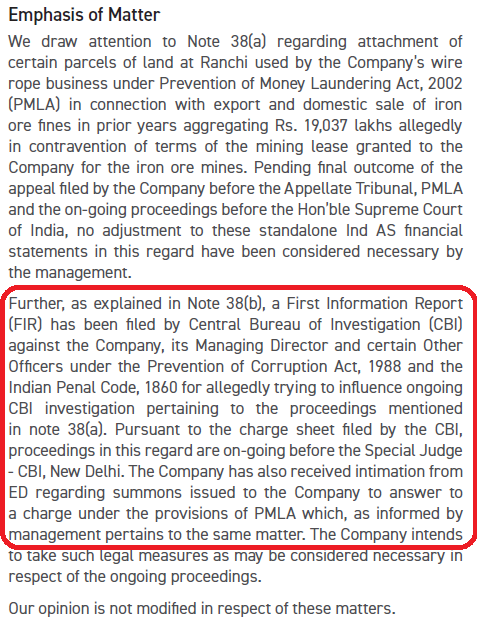

Pending contingent liabilities

Emphasis of matter by Usha Martin's auditors

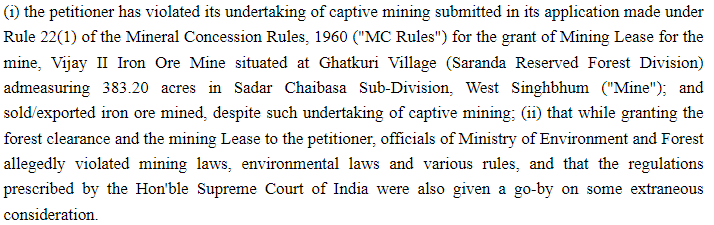

Here are some snippets related to the above liabilities from the chargesheet filed at the Jharkhand High Court.

Personally my stance as an investor is - These allegations are serious in nature.

However we need to understand that doing mining business in India is not easy and getting approvals can take years and be very frustrating for entrepreneurs.

However we need to understand that doing mining business in India is not easy and getting approvals can take years and be very frustrating for entrepreneurs.

Ties with Charlie Munger's Kantian Fairness Tendency.

My interpretation of that mental model was that one should tolerate some unfairness, provided it means a greater fairness for all (UM's employees and their families, vendors, customers)

My interpretation of that mental model was that one should tolerate some unfairness, provided it means a greater fairness for all (UM's employees and their families, vendors, customers)

And for shareholders =D

The good news is Usha Martin hived off their steel business in 2019 and it's very unlikely that they would repeat something like this in the future.

The above contingent liabilities are one of the reasons why Usha Martin's stock used to trade at a median P/E of 14 until last year.

Valuation - About how much of an upside is left from here (Currently trading at 28x earnings) is likely to depend upon how fast they can scale up their exports + value added products while improving margins.

If this thread made your investing life easier, please feel free to join our Telegram Channel, where we share a lot of content on small and mid caps with good future potential.

t.me

t.me

Loading suggestions...