Shuvh Nivesh pick 📈📉

(1/n)

🔸Stock Name: Sagar Cements

🔸Target: Rs. 305

🔸Upside Potential: ~24%

🔸Timeframe: 12 months

(1/n)

🔸Stock Name: Sagar Cements

🔸Target: Rs. 305

🔸Upside Potential: ~24%

🔸Timeframe: 12 months

(2/n)

🟧 Investment Rationale

🔸On an expansion spree

🔹Sagar Cements has been one of the fastest growing cement companies wherein its capacity has nearly doubled from 5.8 MT in FY19 to 10 MT currently (~15% CAGR)

🟧 Investment Rationale

🔸On an expansion spree

🔹Sagar Cements has been one of the fastest growing cement companies wherein its capacity has nearly doubled from 5.8 MT in FY19 to 10 MT currently (~15% CAGR)

(3/n)

🔹In FY23, company recorded robust volume growth of 34% YoY to 4.8 MT mainly driven by commissioning of new capacities in Jeerabad, MP (Central: 1.0 MT) and Jajpur, Odhisa (East: 1.5 MT)

🔹In FY23, company recorded robust volume growth of 34% YoY to 4.8 MT mainly driven by commissioning of new capacities in Jeerabad, MP (Central: 1.0 MT) and Jajpur, Odhisa (East: 1.5 MT)

(4/n)

🔹The Jeerabad facility has witnessed swift ramp-up with utilisation rates already at 80%+ levels and generating Rs. 840+ EBITDA/T in Q1FY24E

🔹Recently, it acquired Andhra Cements (1.8 MT) to further consolidate its position in southern markets

🔹The Jeerabad facility has witnessed swift ramp-up with utilisation rates already at 80%+ levels and generating Rs. 840+ EBITDA/T in Q1FY24E

🔹Recently, it acquired Andhra Cements (1.8 MT) to further consolidate its position in southern markets

(5/n)

🔹Operations have commenced from Q1FY24E (sold ~30K Ton volumes) and the management expects the new facility to add ~ 0.75 MT volumes in FY24 (42% CU)

🔹Operations have commenced from Q1FY24E (sold ~30K Ton volumes) and the management expects the new facility to add ~ 0.75 MT volumes in FY24 (42% CU)

(6/n)

🔹While company’s performance in Q1FY24 was tepid (mainly owing to maintenance shutdown at its mother-plant in Mattampally), we expect the volumes & profitability trajectory to improve in the ensuing quarters

🔹While company’s performance in Q1FY24 was tepid (mainly owing to maintenance shutdown at its mother-plant in Mattampally), we expect the volumes & profitability trajectory to improve in the ensuing quarters

(7/n)

🔹We model in volume growth of 25% YoY to 6.0 MT in FY24E and 10% YoY to 6.7 MT by FY25E. Benefit of declining fuel costs expected to flow from Q2FY24 onwards (~ Rs. 100/t in Q2 and further reduction expected in H2FY24)

🔹We model in volume growth of 25% YoY to 6.0 MT in FY24E and 10% YoY to 6.7 MT by FY25E. Benefit of declining fuel costs expected to flow from Q2FY24 onwards (~ Rs. 100/t in Q2 and further reduction expected in H2FY24)

(8/n)

🔸B/S deleveraging to begin from FY25E

🔹Higher capex over 4 years (including acquisition of Andhra Cements) has resulted in gross debt bloating from ~ Rs. 400 crore in FY20 to Rs. 1470 crore as on FY23 (D/E: 0.9x)

🔸B/S deleveraging to begin from FY25E

🔹Higher capex over 4 years (including acquisition of Andhra Cements) has resulted in gross debt bloating from ~ Rs. 400 crore in FY20 to Rs. 1470 crore as on FY23 (D/E: 0.9x)

(9/n)

🔹Going forward, company is looking for mainly brownfield expansion (in Jeerabad, Gudipadu & Andhra Cements) which could entail lower capex requirements

🔹We build in capex of Rs. ~ 400 crore over FY24-25E (incurred capex of Rs. 1300+ crore in last 2 years)

🔹Going forward, company is looking for mainly brownfield expansion (in Jeerabad, Gudipadu & Andhra Cements) which could entail lower capex requirements

🔹We build in capex of Rs. ~ 400 crore over FY24-25E (incurred capex of Rs. 1300+ crore in last 2 years)

(10/n)

🔹We expect the company to generate steady free cash flow (FCF) & model in debt reduction of ~Rs 350 cr by FY25E (D/E: 0.6x)

Though not factored in our estimates, Vizag land sale (part of Andhra Cement acquisition) could further help deleverage the b/s (worth~ Rs 400 cr)

🔹We expect the company to generate steady free cash flow (FCF) & model in debt reduction of ~Rs 350 cr by FY25E (D/E: 0.6x)

Though not factored in our estimates, Vizag land sale (part of Andhra Cement acquisition) could further help deleverage the b/s (worth~ Rs 400 cr)

(11/n)

🟥 Rating and Target Price

♦️Sagar Cement is trading at attractive valuations (US$ 50/t vs replacement cost of US$ 110/t)

♦️Sagar Cement is an attractive regional play in the southern cement markets & has demonstrated the ability to be one of the lowest cost producers

🟥 Rating and Target Price

♦️Sagar Cement is trading at attractive valuations (US$ 50/t vs replacement cost of US$ 110/t)

♦️Sagar Cement is an attractive regional play in the southern cement markets & has demonstrated the ability to be one of the lowest cost producers

(12/n)

♦️Hence, we ascribe BUY rating on the stock. We value Sagar at Rs. 305 i.e. 10x FY25E EV/EBITDA

Disclaimer: Disclaimer: bit.ly

♦️Hence, we ascribe BUY rating on the stock. We value Sagar at Rs. 305 i.e. 10x FY25E EV/EBITDA

Disclaimer: Disclaimer: bit.ly

(13/n)

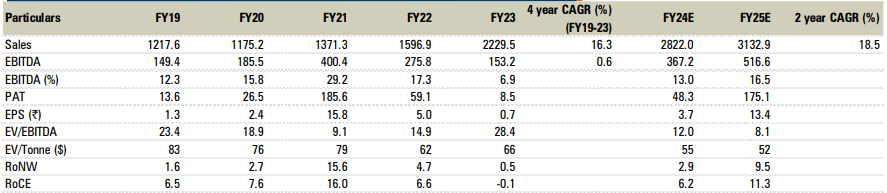

🟥 Key Financial Summary

🟥 Key Financial Summary

Loading suggestions...