There’s a $13 billion fund that you likely have never heard of that has tripled the returns of the average hedge fund over the last 20 years.

The most surprising thing is that their investment strategy involves buying and selling the same few hundred stocks.

Let’s dive in!

The most surprising thing is that their investment strategy involves buying and selling the same few hundred stocks.

Let’s dive in!

Greg Poole founded Echo Street Capital in 2002 at the age of 28 with less than $10 million in assets under management.

Echo Street manages $13 billion as of June 2023.

It’s a fascinating story of learning and continuously improving one’s investment process.

Echo Street manages $13 billion as of June 2023.

It’s a fascinating story of learning and continuously improving one’s investment process.

Greg Poole graduated first in his class from the University of Western Ontario.

He began his career at Goldman Sachs in 1996. By 2001, Greg had become the sole portfolio manager of the Goldman Sachs Waterside Opportunity Fund, a real estate focused long/short equity fund.

He began his career at Goldman Sachs in 1996. By 2001, Greg had become the sole portfolio manager of the Goldman Sachs Waterside Opportunity Fund, a real estate focused long/short equity fund.

He launched Echo Street Capital in 2002. The firm was also initially a long/short hedge fund with a focus on real estate strategies.

However, what’s remarkable is that Greg has reinvented the fund several times over the last 20 years.

However, what’s remarkable is that Greg has reinvented the fund several times over the last 20 years.

For example, during the 2008 crisis, Greg was willing to shift focus to credit opportunities.

The biggest reimagination of the fund came in 2010 when Greg introduced the term GoodCo to his investors. GoodCo has been the foundation of their strategy ever since.

The biggest reimagination of the fund came in 2010 when Greg introduced the term GoodCo to his investors. GoodCo has been the foundation of their strategy ever since.

The next big evolution came in 2013 when Greg hired a young quant, Andrew Yang.

The two created the System which was a quantamental approach that automated idea generation of GoodCos and allowed the fund to run equity market neutral.

The two created the System which was a quantamental approach that automated idea generation of GoodCos and allowed the fund to run equity market neutral.

With each reinvention, Echo Street Capital extended its success.

Echo Street tripled the returns of the average hedge fund over 20 years.

Even more impressively, they beat the S&P 500 net of fees while running with 20% net equity exposure and single digit volatility.

Echo Street tripled the returns of the average hedge fund over 20 years.

Even more impressively, they beat the S&P 500 net of fees while running with 20% net equity exposure and single digit volatility.

So what is GoodCo?

Echo Street describes GoodCos as “structurally superior to other companies. They occupy a privileged seat at the economic table and from that seat, enjoy higher organic growth & unusual reinvestment opportunities. These are the companies we partner with."

Echo Street describes GoodCos as “structurally superior to other companies. They occupy a privileged seat at the economic table and from that seat, enjoy higher organic growth & unusual reinvestment opportunities. These are the companies we partner with."

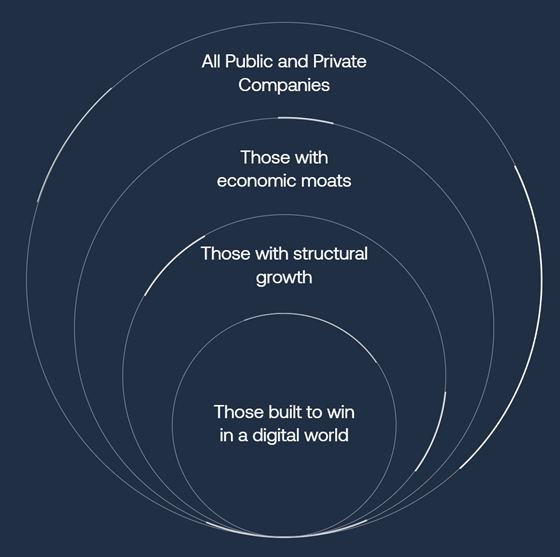

Echo Street invests in a universe of companies chosen for the consistency and durability of the earnings streams and their ability to compound value at higher-than-average rates.

Out of 60,000+ companies, only a few hundred are GoodCos.

Out of 60,000+ companies, only a few hundred are GoodCos.

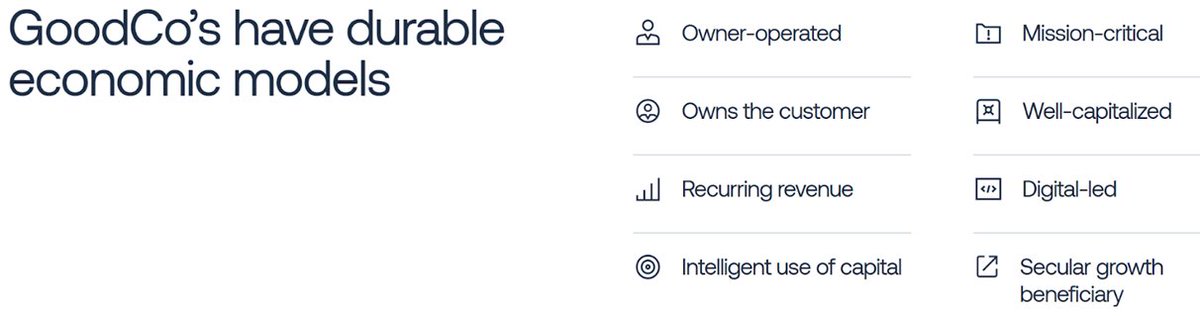

GoodCos have the following characteristics:

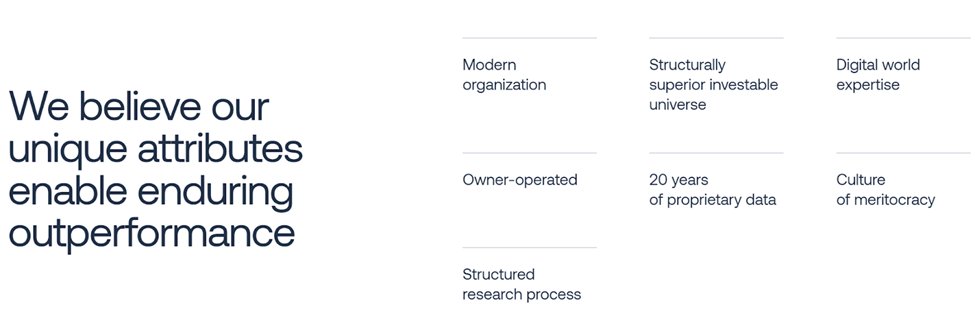

1. Owner-operated

2. Own the customer

3. Recurring revenue

4. Intelligent use of capital

5. Mission-critical

6. Well-capitalized

7. Digital-led

8. Secular growth beneficiary

1. Owner-operated

2. Own the customer

3. Recurring revenue

4. Intelligent use of capital

5. Mission-critical

6. Well-capitalized

7. Digital-led

8. Secular growth beneficiary

The 2 most critical criteria for GoodCos are:

Durable economic moats: entrenched within customers’ workflows and difficult to displace.

Structural Growth: enjoy competitive advantages and secular tailwinds that allow them to compound value faster than the broader market.

Durable economic moats: entrenched within customers’ workflows and difficult to displace.

Structural Growth: enjoy competitive advantages and secular tailwinds that allow them to compound value faster than the broader market.

What are examples of GoodCo’s that Echo Street tracks and invests in?

• Data Sciences

• Dominant Vertical Software

• Software Systems of Record

• Life Sciences

• Alternative Real Estate

• Highly Engineered Manufacturing

• Data Sciences

• Dominant Vertical Software

• Software Systems of Record

• Life Sciences

• Alternative Real Estate

• Highly Engineered Manufacturing

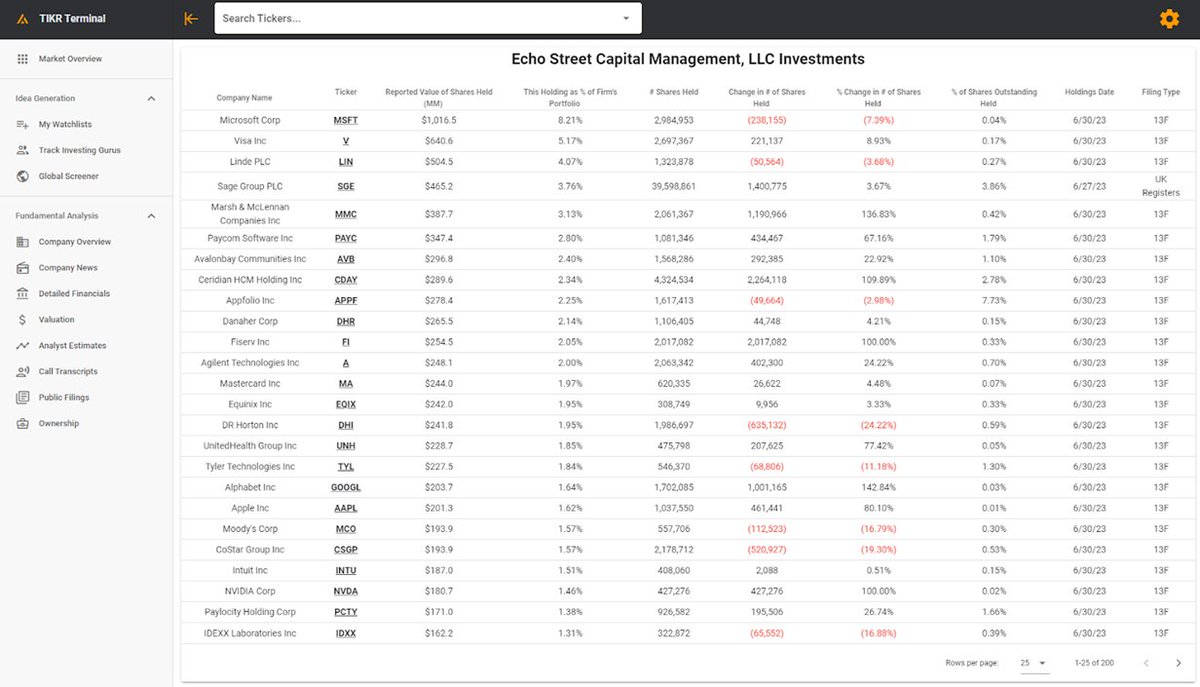

Echo Street’s top 10 stocks (@thetikr):

1. Microsoft ($MSFT)

2. Visa ($V)

3. Linde Plc ($LIN)

4. Sage Group ($SGE)

5. Marsh & McLennan ($MMC)

6. Paycom ($PAYC)

7. Avalonbay ($AVB)

8. Ceridian ($CDAY)

9. Appfolio ($APPF)

10. Danaher ($DHR). I wrote about Danaher in my pinned post

1. Microsoft ($MSFT)

2. Visa ($V)

3. Linde Plc ($LIN)

4. Sage Group ($SGE)

5. Marsh & McLennan ($MMC)

6. Paycom ($PAYC)

7. Avalonbay ($AVB)

8. Ceridian ($CDAY)

9. Appfolio ($APPF)

10. Danaher ($DHR). I wrote about Danaher in my pinned post

What also makes Echo Street’s strategy unique is its quantamental approach.

For example, they classify & score economic moats and secular growth trends.

Fundamental research is augmented with charting & cyclical analysis + quant tools.

For example, they classify & score economic moats and secular growth trends.

Fundamental research is augmented with charting & cyclical analysis + quant tools.

Echo Street shorted stocks with the following characteristics:

1. Business unfavorably positioned relative to ongoing secular changes

2. Management team that is unlikely adequate to respond to those changes

3. Over-leveraged balance sheets

4. extreme valuation

1. Business unfavorably positioned relative to ongoing secular changes

2. Management team that is unlikely adequate to respond to those changes

3. Over-leveraged balance sheets

4. extreme valuation

Beyond the specific strategy that Echo Street has executed on, what’s most impressive has been Greg’s willingness to keep an open mind and reinvent the fund.

He’s been able to help Echo Street navigate multiple market transitions and regime changes.

He’s been able to help Echo Street navigate multiple market transitions and regime changes.

Most recently he shut down the L/S hedge fund in late 2020 to focus on the long-only strategy.

“The workflow involved in finding investment ideas is joyful… the workflow involved in smoothing the ride is increasingly a soul-sapping one”

“The workflow involved in finding investment ideas is joyful… the workflow involved in smoothing the ride is increasingly a soul-sapping one”

From 2002 - 2020, the L/S hedge fund returned an annualized 9.4%. It beat the S&P 500 with half the volatility.

But the firm’s long-only fund returned ~21% annualized since 2015.

Mitigating short-term volatility is expensive, which is likely why they shut down the L/S fund.

But the firm’s long-only fund returned ~21% annualized since 2015.

Mitigating short-term volatility is expensive, which is likely why they shut down the L/S fund.

Echo Street believes they have the ability to continue to outperform.

Only time will tell if they can continue to adapt to changing market conditions!

Only time will tell if they can continue to adapt to changing market conditions!

Thanks for reading!

It would mean a lot if you could like and repost the first post to help others find it If you found this thread helpful.

I’ll also be putting out more threads on investing and entrepreneurship, so be sure to follow me @skhetpal

It would mean a lot if you could like and repost the first post to help others find it If you found this thread helpful.

I’ll also be putting out more threads on investing and entrepreneurship, so be sure to follow me @skhetpal

Loading suggestions...