A risky, elaborate trade, one infamous for blowing up everytime, is growing in popularity in the world’s most systemic bond market. When turmoil inevitably emerges, only the Fed’s volatility suppressor can come to the rescue. The Treasury Market Unwind™ is looming... 1/

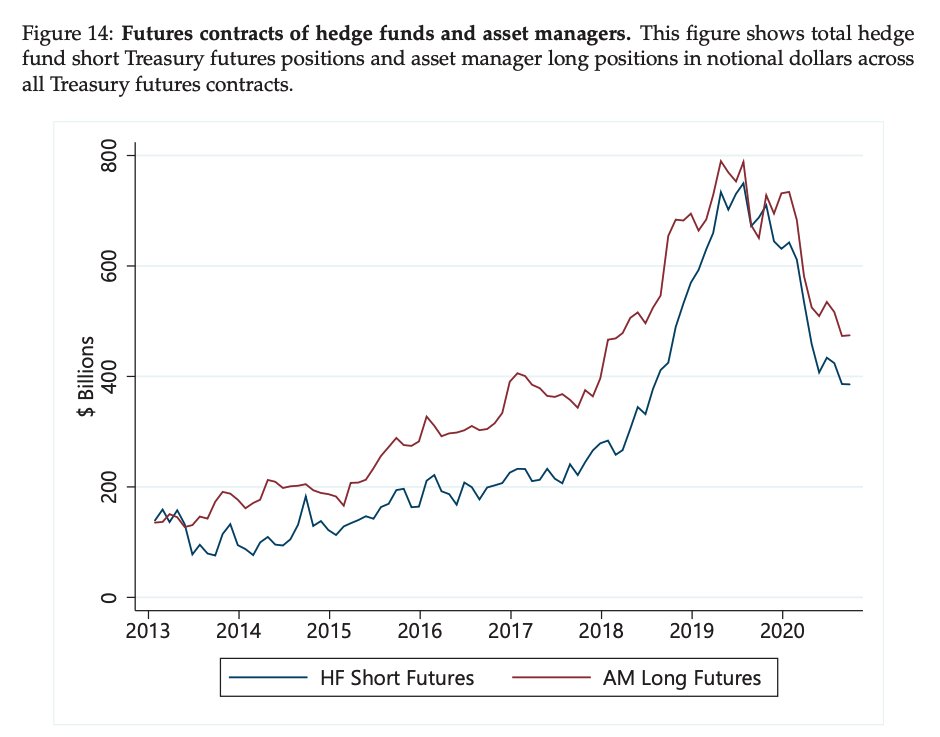

Early in 2018, a series of events formed an exploit in America’s sovereign debt market. After large U.S. Treasury issuance, a fall in foreign demand, and regulatory changes, asset managers began to shift out of Treasuries and into long positions of associated Treasury futures...

This shift was so intense that prices of Treasury futures and of those in the underlying cash market began to diverge. Noticing an arbitrage opportunity, hedge funds started to take the opposite side of asset managers’ positions. The cash-futures "basis trade" was re-emerging...

By going “long the basis,” which meant simultaneously shorting Treasury futures and buying the securities underlying these contracts in the cash market, hedge funds — primarily relative-value funds —had high odds of profiting from what was deemed a nearly risk-free arbitrage...

Futures prices kept rising above their associated Treasury securities, allowing traders to buy Treasuries at a discount to the price they’d receive upon delivering the security into a futures contract. The basis, the difference in price between cash and futures, was the profit...

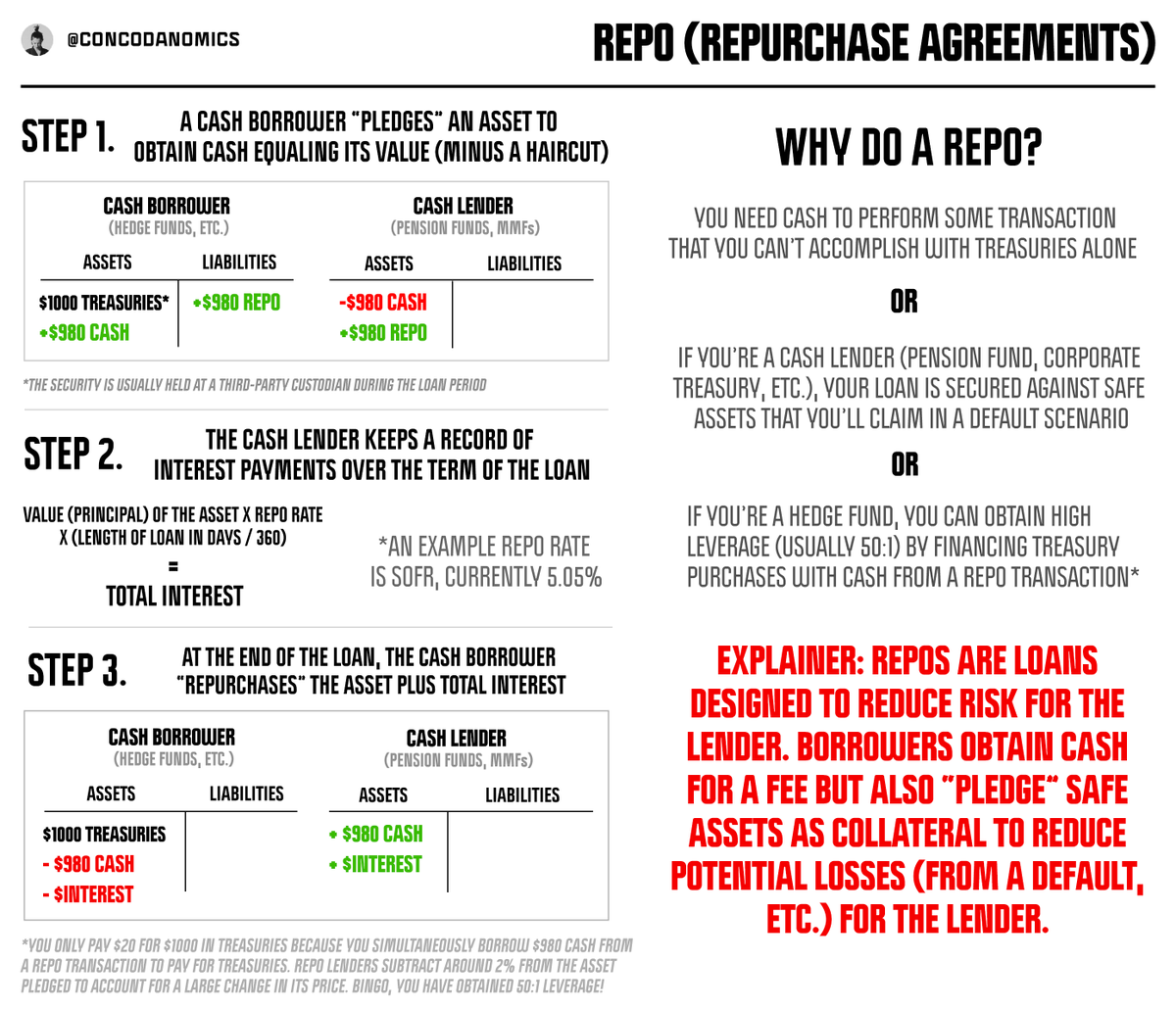

But although this trade offered nearly risk-free returns, the resulting profits were lackluster. For hedge funds to achieve significant enough returns, they had to employ immense amounts of leverage. To execute highly leveraged trades, hedge funds used bilateral repo markets...

Bilateral repos are cash loans secured against specific securities. By borrowing cash against the Treasuries they would use to deliver into futures contracts, hedge funds only needed to commit a fraction of capital to finance basis trade positions...

The amount of leverage hedge fund traders achieved was determined by the repo market they used to finance Treasury purchases. Hedge funds borrowed in uncleared, cleared, or sponsored bilateral repo markets, each dominated by leveraged participants funding various exotic trades...

While cleared and sponsored repo offered greater transparency and lower counterparty risk, uncleared repo markets (also known as NCCBR) delivered superior leverage and flexibility...

Cash lenders in each repo market lent money equal to the value of the Treasury securities the cash borrower (i.e. hedge fund) pledged, minus a haircut: a percentage the lender subtracted from the security’s value to protect against adverse market movements...

In the shadowy depths of the uncleared repo market, haircuts fell to as low as 0%, allowing for much higher leverage than cleared and sponsored repo markets. Subsequently, uncleared repo swamped cleared repo in size and activity...

Soon enough by 2019, the uncleared repo market facilitated around ~$1.4 trillion in outstanding transactions. Meanwhile, hedge funds were regularly borrowing up to a hundred times the capital they committed to basis trades, achieving in most cases more than 99:1 leverage...

As 2020 approached, short positions in Treasury futures had soared by over 100%, with hedge funds making up ~73% of the volume. Billions upon billions of dollars had been allocated to highly leveraged basis trades, on what was perceived to be a low-risk, high-return wager...

The trade’s major vulnerabilities were only exposed to the fiercest of black swan events, but as it turned out, the COVID market panic was around the corner. Just as the basis trade was rippling into mainstream circles, the Treasury Market Unwind™ had commenced...

As the COVID financial meltdown arose in March 2020, the defects arising from enormous interventions and radical responses to the GFC (Great Financial Crisis) became apparent for all to witness...

Before regulators implemented an ocean of rules and regulations, from the Dodd-Frank Act to the Basel Framework, the structure of the system created a default flight to safety into the U.S. Treasury market during a crisis...

But after a decade of moving from an unsecured to a secured standard, markets had absorbed a large quantity of Treasuries as a safeguard. The financial system's monetary plumbers had already flipped from net short to net long safe assets before the crisis had unfolded...

Thus, as the COVID turmoil transpired, it became evident that the traditional flight of safety into Treasuries had already taken place. The new flight to safety in times of crisis had become a dash for cash .i.e cold, hard U.S. dollars...

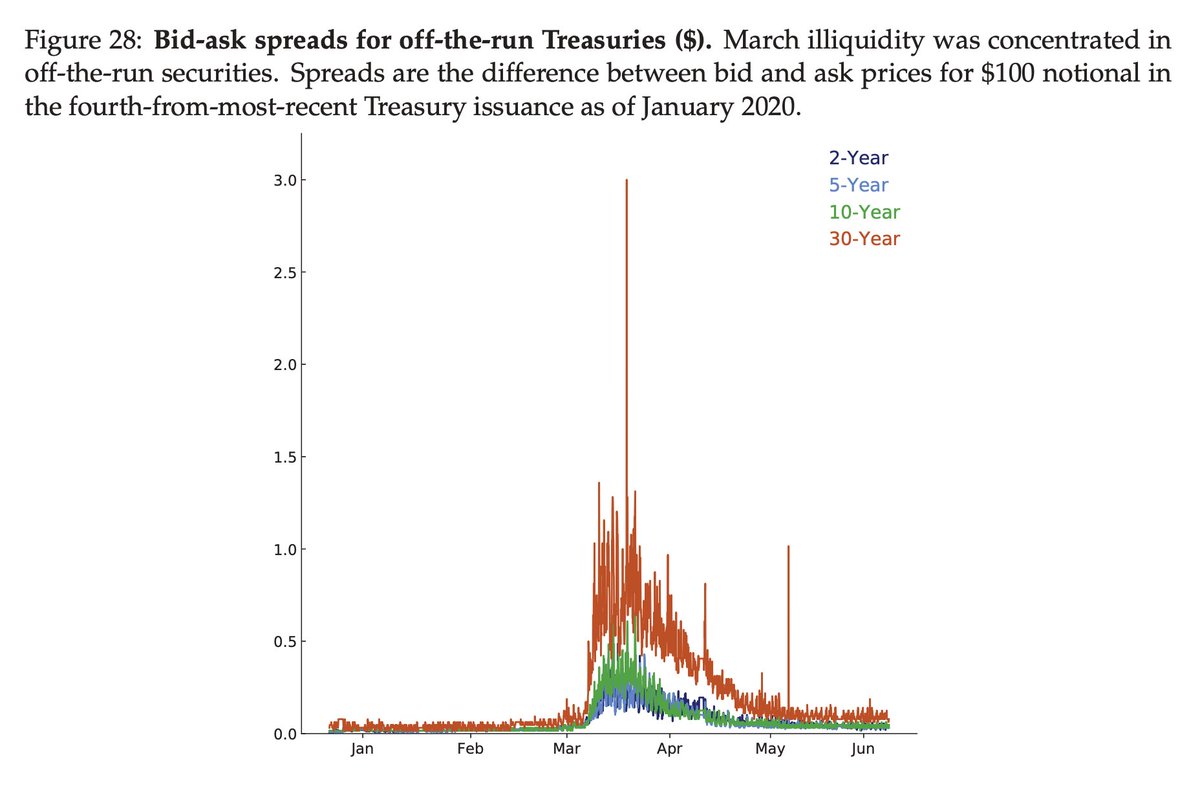

As pandemic fears spread, Treasury market volatility spiked and bid/ask spreads widened. Investors who never expected to have to liquidate Treasuries, mainly foreign central banks and U.S money funds, suddenly dumped their holdings en masse. An illiquidity spiral had arisen...

The illiquidity created via these firesales rippled through the financial system, enough to contest the cash-futures basis trade’s vulnerabilities: margin risk (sharp moves in futures and bond prices spurring margin calls) and rollover risk (the cost to rollover a repo rising)...

Traders financing their positions using repo loans rolled over on an overnight basis had to unwind a now unaffordable trade. Meanwhile, those hit by large increases in margin requirements were hit with margin calls. The "long basis" trade had grown unprofitable for many...

But before a mass unwind of basis trades could cause serious damage, exacerbating an illiquidity spiral, the Federal Reserve’s “volatility suppressor" came to the rescue. By simply announcing it would pledge to purchase an unlimited amount of bonds, calm re-emerged in markets...

Dealers and other monetary plumbers recommenced making markets in Treasuries, prompting basis trades to not only regain profitability but provide liquidity as markets recovered. All the Federal Reserve had to do to revive market sentiment was announce it was willing to step in...

Fast forward to today, and a recent Fed study has revealed convincing evidence that the Treasury cash-futures basis trade is not only back but growing in numbers...

Familiar futures positioning and borrowing patterns in the bilateral repo markets have started to gain momentum. Like before the COVID crash materialized, the basis trade is likely helping to bind the Treasury, cash, and repo markets firmly together...

So when disruption arises in the U.S. Treasury market once more, the Fed will be on higher alert than ever before, watching and waiting to fire up its volatility suppressor to prevent any Treasury market turmoil...

The only major disorder to arise from the next near-miss will be outrage over the Fed’s ever-growing power in markets, especially their eagerness to step in at the first sign of danger. Bailouts but also political backlash are now both guaranteed.

Thanks for reading! If you enjoyed this, feel free to retweet the top tweet of this thread and follow @concodanomics for more…

You can also subscribe below to receive more in-depth articles about finance, markets, and geopolitics in your inbox...

👉 concoda.substack.com 👈

You can also subscribe below to receive more in-depth articles about finance, markets, and geopolitics in your inbox...

👉 concoda.substack.com 👈

Loading suggestions...