India is the world’s second-largest producer here.

One of the oldest industries in the Indian economy which contributes:

📌2.3% to GDP

📌4% share of the global trade

📌13% to Industrial Production

📌12% to exports

📌4.5 crore employment

A thread on Textile & Apparel Sector

1/n

One of the oldest industries in the Indian economy which contributes:

📌2.3% to GDP

📌4% share of the global trade

📌13% to Industrial Production

📌12% to exports

📌4.5 crore employment

A thread on Textile & Apparel Sector

1/n

2/n

This thread covers -

1. Evolution of Indian Textile Sector

2. Textile & Apparel Value Chain

3. Opportunity Size

4. Market across value chain

5. Govt. Initiative

6. Export Opportunity: FTA with UK

7. Technical Textile: New arena of growth

8. Current buzz in this sector

This thread covers -

1. Evolution of Indian Textile Sector

2. Textile & Apparel Value Chain

3. Opportunity Size

4. Market across value chain

5. Govt. Initiative

6. Export Opportunity: FTA with UK

7. Technical Textile: New arena of growth

8. Current buzz in this sector

3/n

Evolution of Indian Textile Sector

Started in 1854, with first textile mill of Mumbai, India had 409 Textile mills post partition. 2016 onwards, India is now focussed on Make in India Mission as well as a focus on Technical textiles.

A brief history:

Evolution of Indian Textile Sector

Started in 1854, with first textile mill of Mumbai, India had 409 Textile mills post partition. 2016 onwards, India is now focussed on Make in India Mission as well as a focus on Technical textiles.

A brief history:

4/n

First let's understand the process of how raw cotton turns into beautiful clothing through a 5 stage process:

First let's understand the process of how raw cotton turns into beautiful clothing through a 5 stage process:

5/n

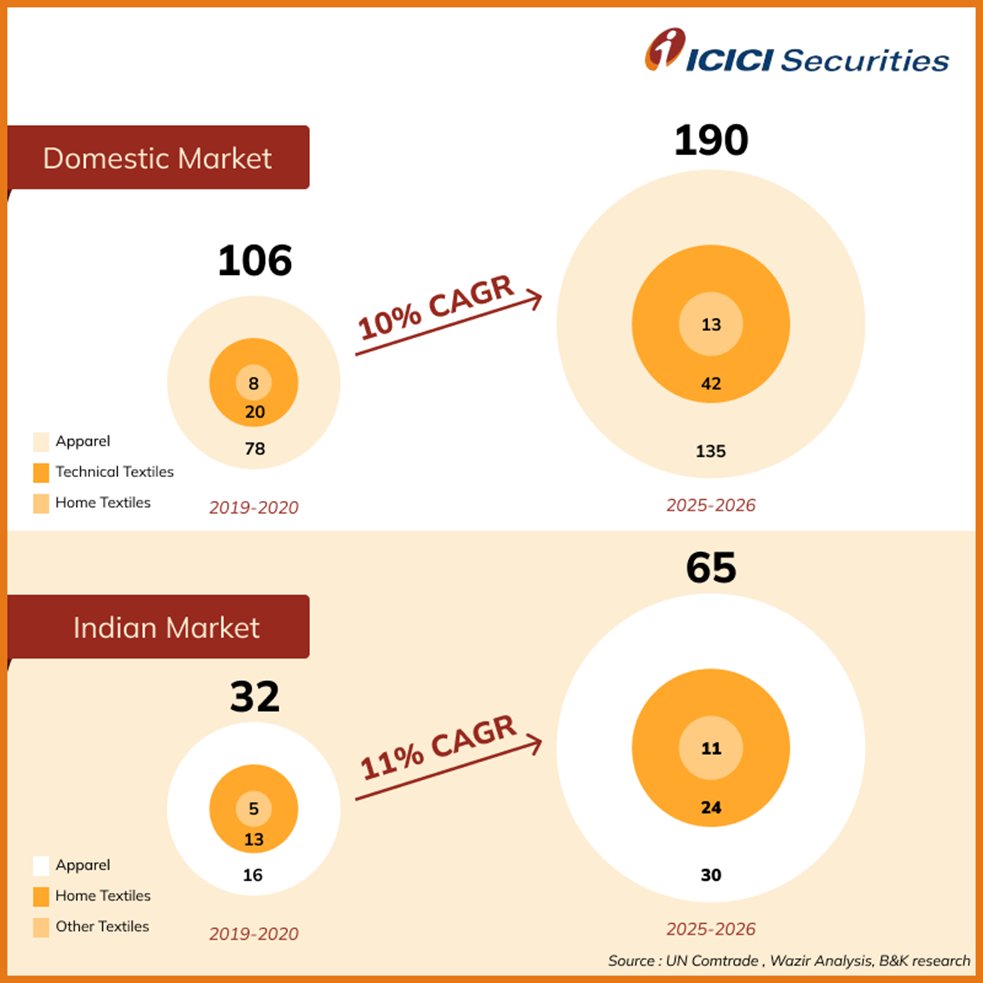

Textile is a $255 bn opportunity by FY25-26 broadly split in 3:1 ratio between domestic ($190 Bn, 10% CAGR) and export markets ($65 Bn, 11% CAGR).

India has strong presence across Yarn & Home Textile but lagging in end apparel which is the biggest opportunity for India.

Textile is a $255 bn opportunity by FY25-26 broadly split in 3:1 ratio between domestic ($190 Bn, 10% CAGR) and export markets ($65 Bn, 11% CAGR).

India has strong presence across Yarn & Home Textile but lagging in end apparel which is the biggest opportunity for India.

6/n

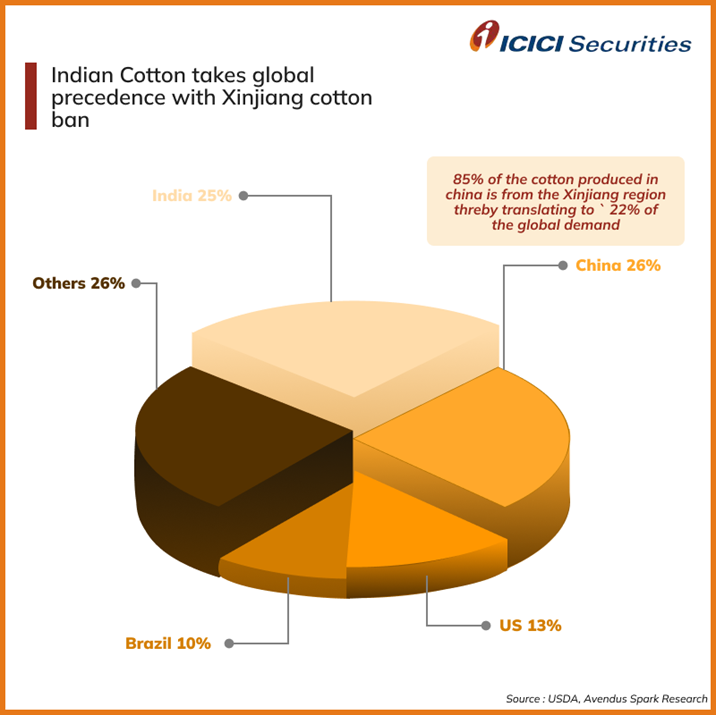

Step 1: Cotton - the raw material.

India is the largest producer of Cotton and 2nd largest in Man-made Fibre (MMF).

In mid 2022, US imposed a ban on cotton & cotton products originating from Xinjiang in China. India stands to gain and emerge as a key cotton exporter.

Step 1: Cotton - the raw material.

India is the largest producer of Cotton and 2nd largest in Man-made Fibre (MMF).

In mid 2022, US imposed a ban on cotton & cotton products originating from Xinjiang in China. India stands to gain and emerge as a key cotton exporter.

7/n

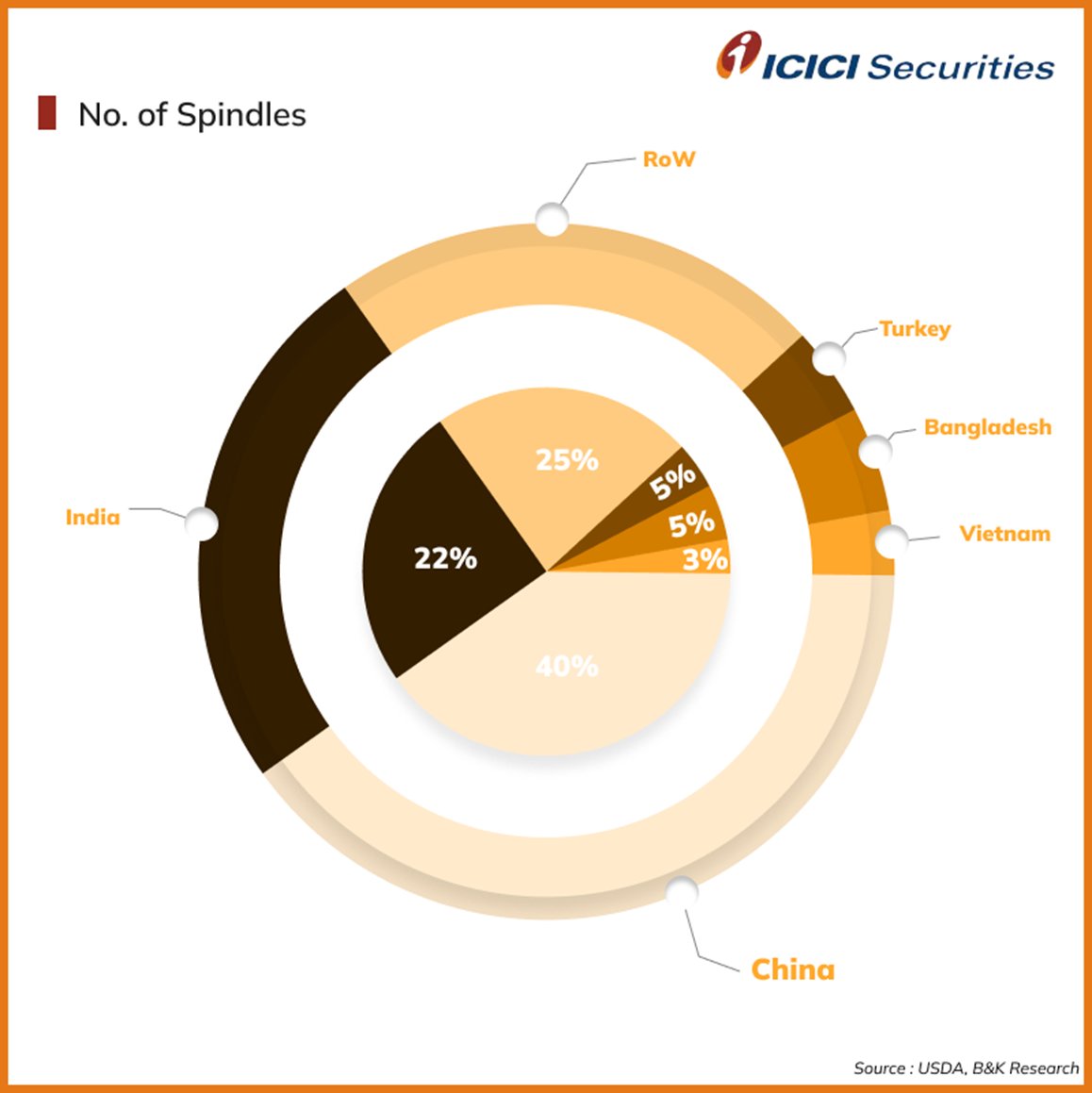

Step 2: Spinning of yarn from Cotton

India has 2nd largest spinning capacity in the world post China. The Spinning sector in India is largely organized and is globally competitive in terms of variety, process and production quality.

Step 2: Spinning of yarn from Cotton

India has 2nd largest spinning capacity in the world post China. The Spinning sector in India is largely organized and is globally competitive in terms of variety, process and production quality.

8/n

Step 3: Weaving/Knitting

Largely fragmented & 95% fabric is produced in small industries.

🚨 Weakest link in supply chain due to high tariffs and low investment in technology. India lags in cotton fabric exports with 9% share (China: 69%)

Reading

indiantextilemagazine.in

Step 3: Weaving/Knitting

Largely fragmented & 95% fabric is produced in small industries.

🚨 Weakest link in supply chain due to high tariffs and low investment in technology. India lags in cotton fabric exports with 9% share (China: 69%)

Reading

indiantextilemagazine.in

9/n

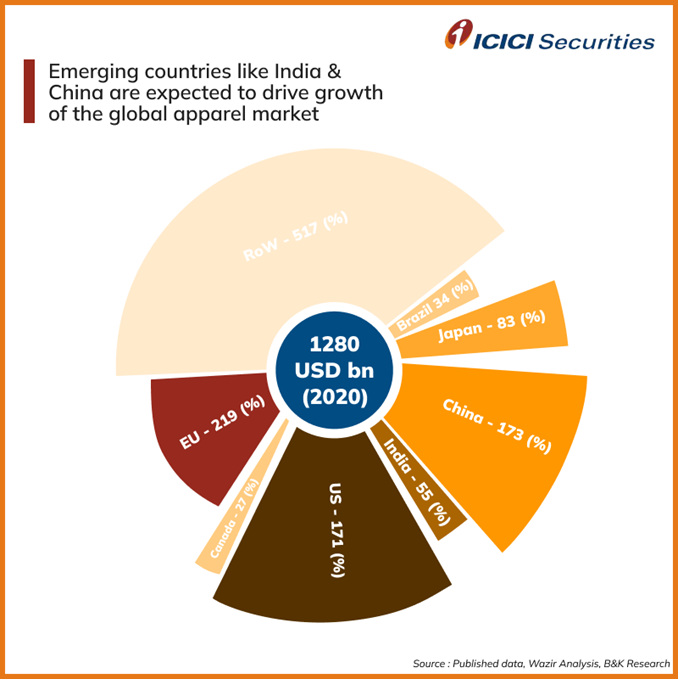

Step 4: Apparel

Apparel is the last and the biggest segment which is almost 57% of the value chain.

Global Apparel market is worth $1.3 Tn with demand led by US and EU (30% of global market)

Tip: Investors should look for export share in Apparel exporters.

Step 4: Apparel

Apparel is the last and the biggest segment which is almost 57% of the value chain.

Global Apparel market is worth $1.3 Tn with demand led by US and EU (30% of global market)

Tip: Investors should look for export share in Apparel exporters.

10/n

Indian Textile is spread across regional hubs.

Save this image and check companies operating in each region.

Indian Textile is spread across regional hubs.

Save this image and check companies operating in each region.

11/n

Initiatives:

1. Govt has launched 7 Mega Integrated Textile Region and Apparel (MITRA) with investment of Rs 4445 Cr by FY27-28.

2. Govt has also approved Rs. 10,683 crore for man-made fibre and technical textiles under PLI Scheme.

3. FTAs in progress with EU and Africa

Initiatives:

1. Govt has launched 7 Mega Integrated Textile Region and Apparel (MITRA) with investment of Rs 4445 Cr by FY27-28.

2. Govt has also approved Rs. 10,683 crore for man-made fibre and technical textiles under PLI Scheme.

3. FTAs in progress with EU and Africa

12/n

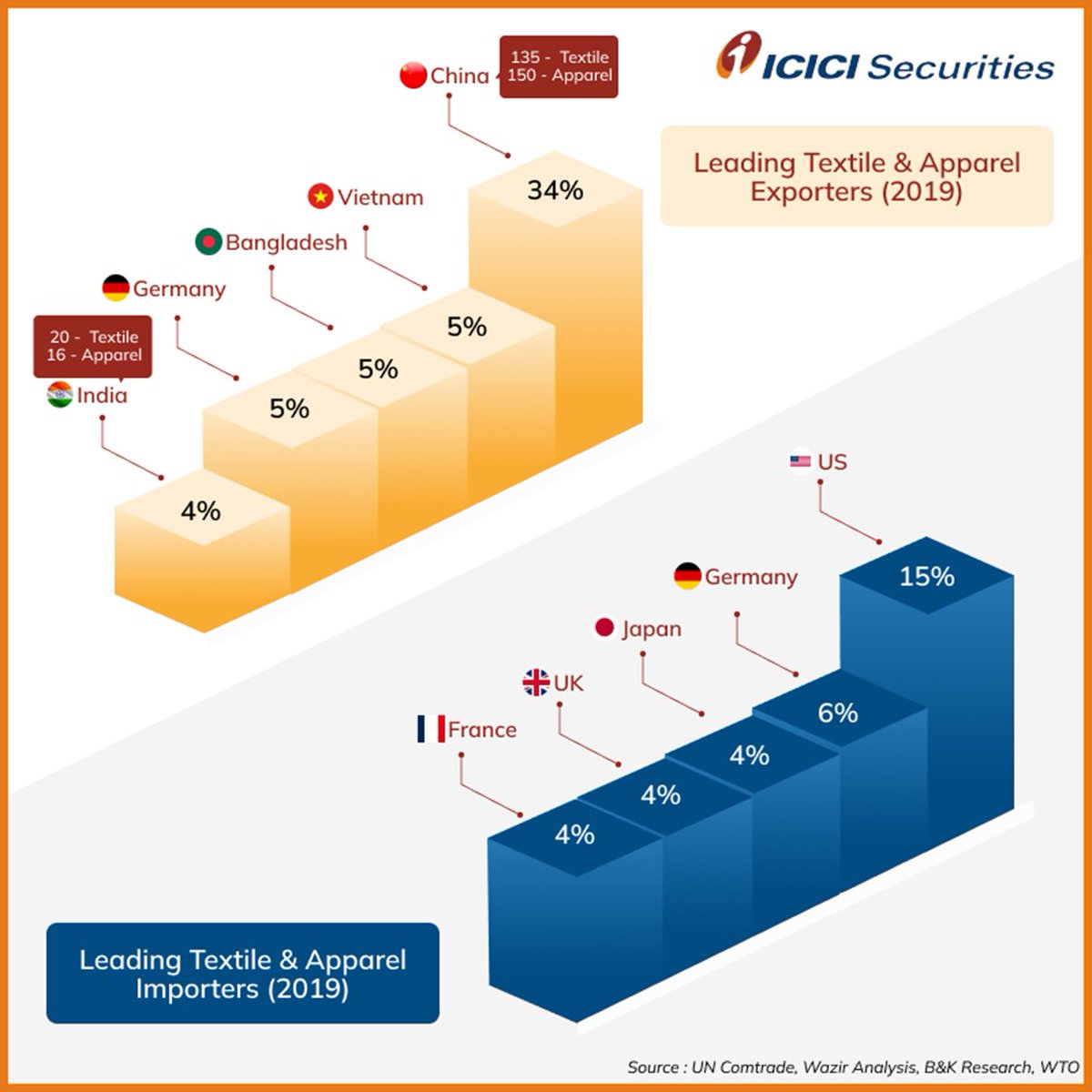

Export Opportunity: Big

Indian Textile (yarn) exports are ~1/7th of China's while our apparel exports are ~1/10th of China.

Further, India’s apparel exports are less than half of Vietnam’s & Bangladesh’s Apparel Exports.

Export Opportunity: Big

Indian Textile (yarn) exports are ~1/7th of China's while our apparel exports are ~1/10th of China.

Further, India’s apparel exports are less than half of Vietnam’s & Bangladesh’s Apparel Exports.

13/n

🎯 1% market share shift to India can create $8Bn export opportunity.

MNCs are looking for partners other than China post-Xinjiang human rights violation issue. India with cheap Cotton (30% cheaper than China), labour and Govt initiative has a strong competitive position.

🎯 1% market share shift to India can create $8Bn export opportunity.

MNCs are looking for partners other than China post-Xinjiang human rights violation issue. India with cheap Cotton (30% cheaper than China), labour and Govt initiative has a strong competitive position.

14/n

In last 3 years, China has lost US export share by 8%, which is largely gained by Vietnam (4%) & Bangladesh (2%).

Why?

Vietnam sources raw material from China at a very short lead time.

Bangladesh has Duty-free access to Europe

This is why FTAs are important for India.

In last 3 years, China has lost US export share by 8%, which is largely gained by Vietnam (4%) & Bangladesh (2%).

Why?

Vietnam sources raw material from China at a very short lead time.

Bangladesh has Duty-free access to Europe

This is why FTAs are important for India.

15/n

The 11th round of talk on UK FTA is already done in July, where discussion on 19 out of 26 chapters is closed.

India is pushing for a "zero tariff" for textile, leather industries. India views FTA with Britain as a crucial step to becoming a bigger exporter.

The 11th round of talk on UK FTA is already done in July, where discussion on 19 out of 26 chapters is closed.

India is pushing for a "zero tariff" for textile, leather industries. India views FTA with Britain as a crucial step to becoming a bigger exporter.

Thank you for reading Part 1.

In part 2, we will add details on our favorite textile companies and cover details on MMF, the emerging segment.

Follow us @ICICI_Direct and do reshare the thread if you liked it!

In part 2, we will add details on our favorite textile companies and cover details on MMF, the emerging segment.

Follow us @ICICI_Direct and do reshare the thread if you liked it!

Loading suggestions...