How much pension will you get from NPS after you retire?

Well, it depends on 3 things.

1. Corpus

2. Annuity variant

3. Insurer

Say, a 60-year-old buys an annuity for Rs 1 cr today.

His monthly pension can range from Rs 44,750 to Rs 77,000.

What should you keep in mind?

A 🧵

Well, it depends on 3 things.

1. Corpus

2. Annuity variant

3. Insurer

Say, a 60-year-old buys an annuity for Rs 1 cr today.

His monthly pension can range from Rs 44,750 to Rs 77,000.

What should you keep in mind?

A 🧵

First, some basics.

NPS matures when you turn 60.

Of the total money accumulated, you can withdraw up to 60% tax-free.

With the remaining 40%, you must buy an annuity plan from an annuity service provider (insurance company).

In return, you can get a lifelong pension.

NPS matures when you turn 60.

Of the total money accumulated, you can withdraw up to 60% tax-free.

With the remaining 40%, you must buy an annuity plan from an annuity service provider (insurance company).

In return, you can get a lifelong pension.

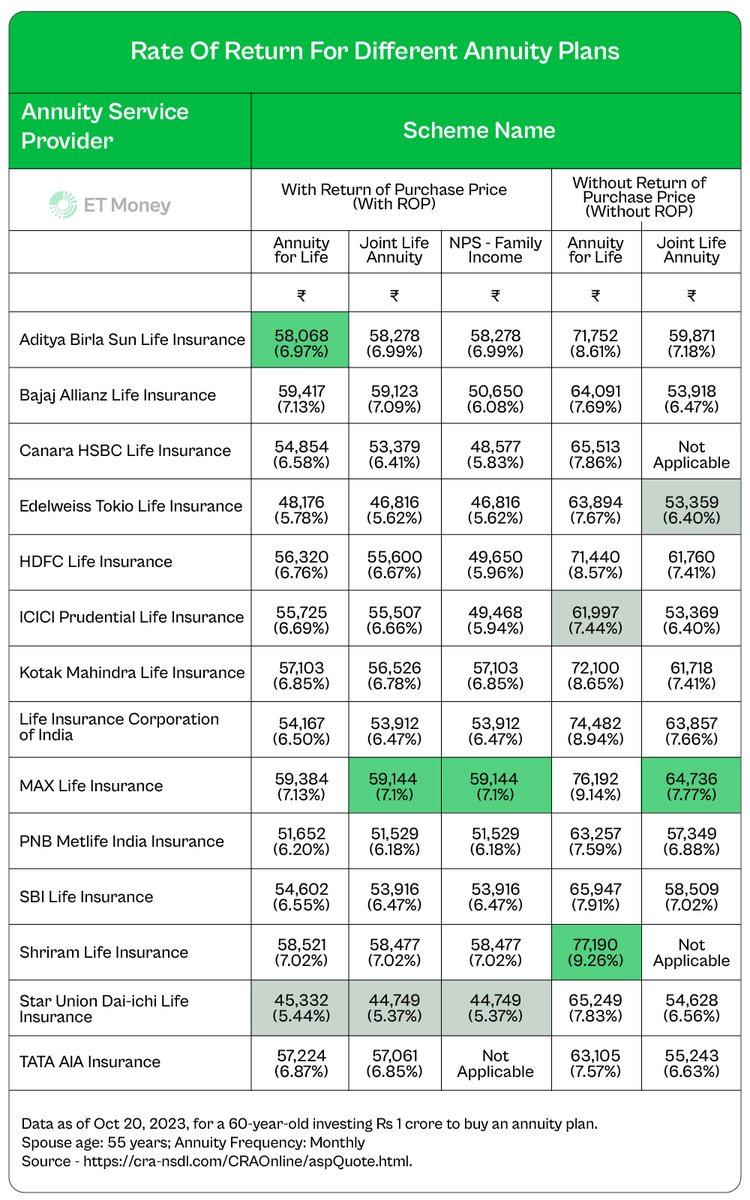

Currently, there are 14 authorized Annuity Service Providers (ASPs).

Broadly, these ASPs provide 5 annuity variants. (See image)

Your pension amount will vary based on the plan (or the variant) you choose.

Broadly, these ASPs provide 5 annuity variants. (See image)

Your pension amount will vary based on the plan (or the variant) you choose.

Let’s understand annuity calculation with an example.

Say you invested in NPS and accumulated Rs 2.5 cr by 60.

You can withdraw up to Rs 1.5 crore (60% of Rs 2.5 cr) tax-free.

But you must invest at least 40% (Rs 1 cr in our example) to buy an annuity plan.

Say you invested in NPS and accumulated Rs 2.5 cr by 60.

You can withdraw up to Rs 1.5 crore (60% of Rs 2.5 cr) tax-free.

But you must invest at least 40% (Rs 1 cr in our example) to buy an annuity plan.

Now, pension differs based on annuity plans.

The most preferred option is Annuity For Life With ROP (70% of users opt for this)

For a 60-year-old, the monthly pension can be:

Highest: Rs 59,417 (7.13%) with Bajaj Allianz

Lowest: Rs 45,332 (5.44%) with Star Union Dai-ichi

The most preferred option is Annuity For Life With ROP (70% of users opt for this)

For a 60-year-old, the monthly pension can be:

Highest: Rs 59,417 (7.13%) with Bajaj Allianz

Lowest: Rs 45,332 (5.44%) with Star Union Dai-ichi

Does ‘Annuity for Life WITH ROP’ (the most popular option) give the highest pension?

No. Usually, it’s the ‘Annuity For Life WITHOUT ROP’.

Why?

Two reasons:

A. Pension stops once the subscriber dies

B. The insurer keeps the amount invested. It’s not passed to the nominee

No. Usually, it’s the ‘Annuity For Life WITHOUT ROP’.

Why?

Two reasons:

A. Pension stops once the subscriber dies

B. The insurer keeps the amount invested. It’s not passed to the nominee

On the other hand, the ‘Family Income With ROP’ plan often offers the lowest pension.

For the various annuity types and their corresponding returns, check the table 👇

For the various annuity types and their corresponding returns, check the table 👇

One more thing.

If an NPS subscriber has more than Rs 10 lakh to buy annuity plans, he can split it 50-50 in two types of annuities.

For example, he can buy an ‘Annuity for life without ROP’ and a ‘Family Income with ROP’ at the same time.

But, there’s a condition…👇

If an NPS subscriber has more than Rs 10 lakh to buy annuity plans, he can split it 50-50 in two types of annuities.

For example, he can buy an ‘Annuity for life without ROP’ and a ‘Family Income with ROP’ at the same time.

But, there’s a condition…👇

An NPS subscriber must buy all his annuity plans from a single annuity provider.

For instance, you cannot buy one plan from HDFC Life Insurance and another from SBI Life Insurance.

This certainly limits your flexibility.

For instance, you cannot buy one plan from HDFC Life Insurance and another from SBI Life Insurance.

This certainly limits your flexibility.

WRAP UP

Annuity plans offer FD-like returns right now.

However, you need to keep these things in mind:

1. No withdrawals are allowed after you buy an annuity plan

2. The rate at which you buy the annuity plan is locked for life

3. Pension is taxable

Annuity plans offer FD-like returns right now.

However, you need to keep these things in mind:

1. No withdrawals are allowed after you buy an annuity plan

2. The rate at which you buy the annuity plan is locked for life

3. Pension is taxable

Now, there are also positives.

Retirees often make emotional choices, like giving money to their children for their well-being (think 'Baghban' movie).

Thus, the absence of liquidity in an annuity plan can actually be a blessing.

Retirees often make emotional choices, like giving money to their children for their well-being (think 'Baghban' movie).

Thus, the absence of liquidity in an annuity plan can actually be a blessing.

We put a lot of effort into creating such informative threads.

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the FIRST tweet.

x.com

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the FIRST tweet.

x.com

Loading suggestions...