China’s NBS released preliminary Q3 numbers last week. Some highlights:

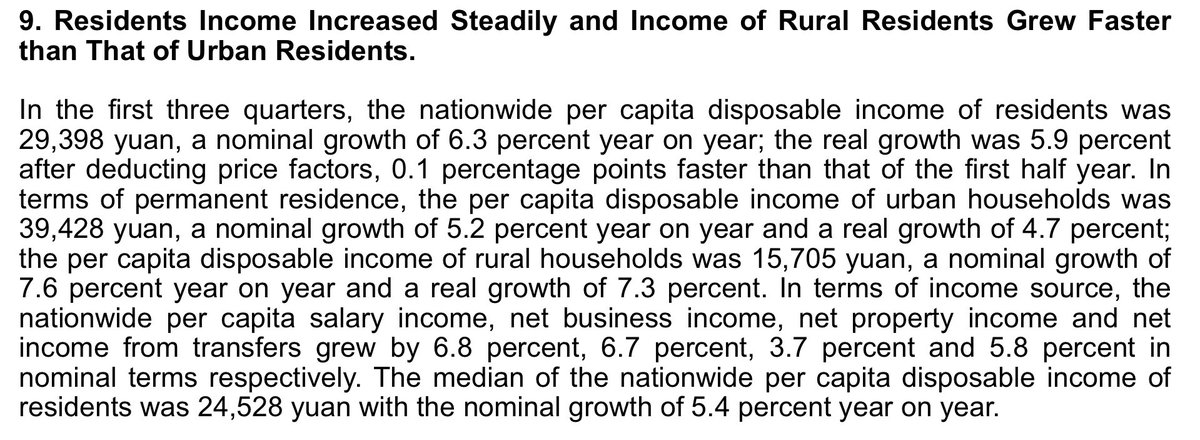

▪️ Q3 confirmed that disposable income growth continued to be strong at 5.9% real, outpacing GDP growth by 0.7%.

▪️ Rural incomes growing faster than urban incomes, lowering the gap between the two.

▪️ Q3 confirmed that disposable income growth continued to be strong at 5.9% real, outpacing GDP growth by 0.7%.

▪️ Rural incomes growing faster than urban incomes, lowering the gap between the two.

For context, there’s been a ton of discussion on this narrower disposable income number and the broader HH income numbers in recent weeks.

To be clear: Chinese HH incomes neither low compared to other countries, nor has its growth been weak in recent years.

To be clear: Chinese HH incomes neither low compared to other countries, nor has its growth been weak in recent years.

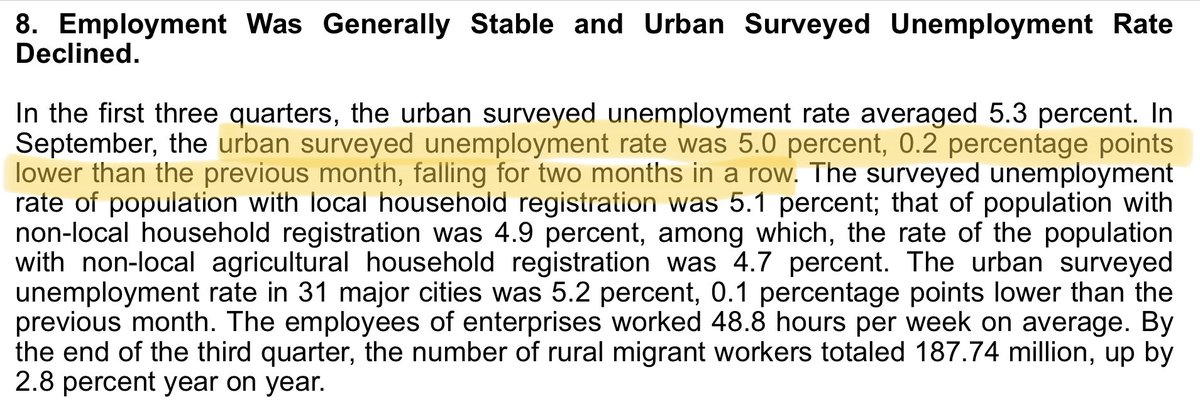

The main factor supporting HH incomes is employment.

Unemployment rates have remained low despite the ongoing property adjustment.

Unemployment rates have remained low despite the ongoing property adjustment.

Policymakers have not resorted to significant HH stimulus because employment has been solid.

Policies to support maximum employment are policymakers’ preferred approach to HH incomes support.

Policies to support maximum employment are policymakers’ preferred approach to HH incomes support.

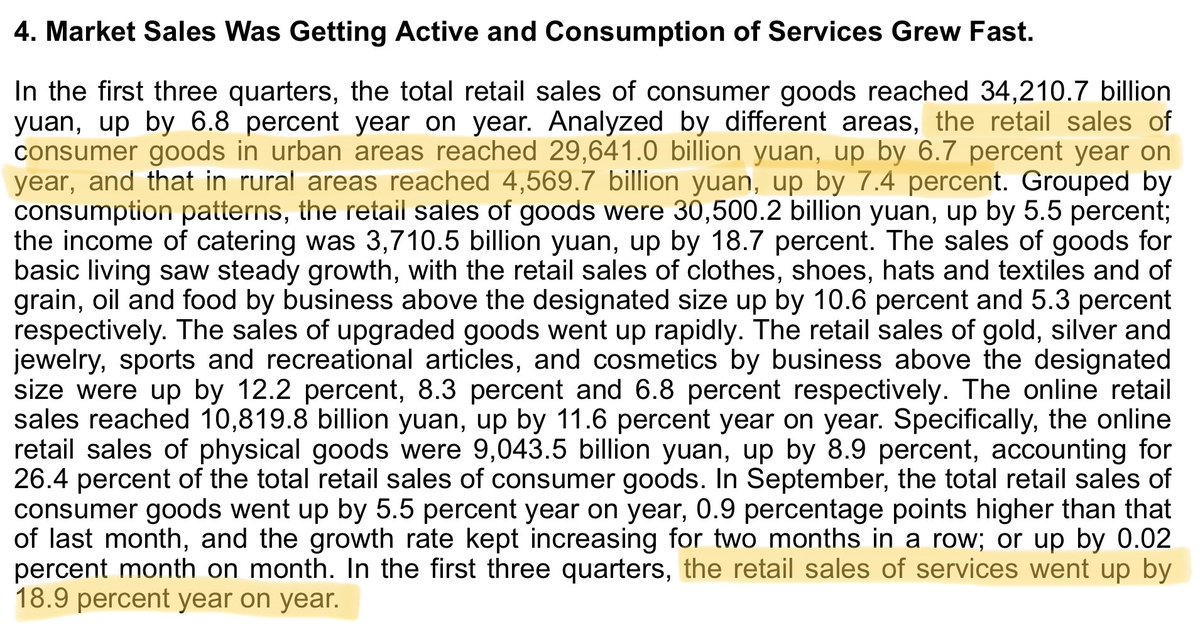

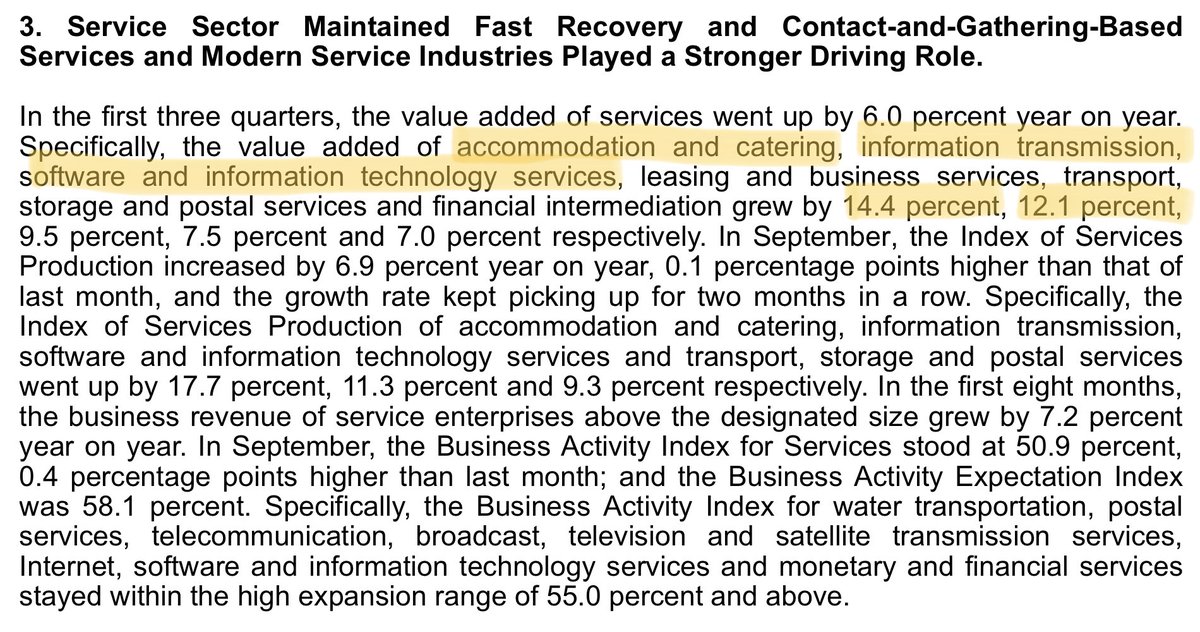

So despite lack of HH-focused stimulus, consumption has shown signs of recovery, led more by intangible services like travel and software than physical goods.

HHs are starting to spend some of its rising income on consumption activities, and saving less.

HHs are starting to spend some of its rising income on consumption activities, and saving less.

As long as HH incomes remained strong, this would eventually lead to rising consumption - which is what we are seeing now, even if it took a bit longer than expected.

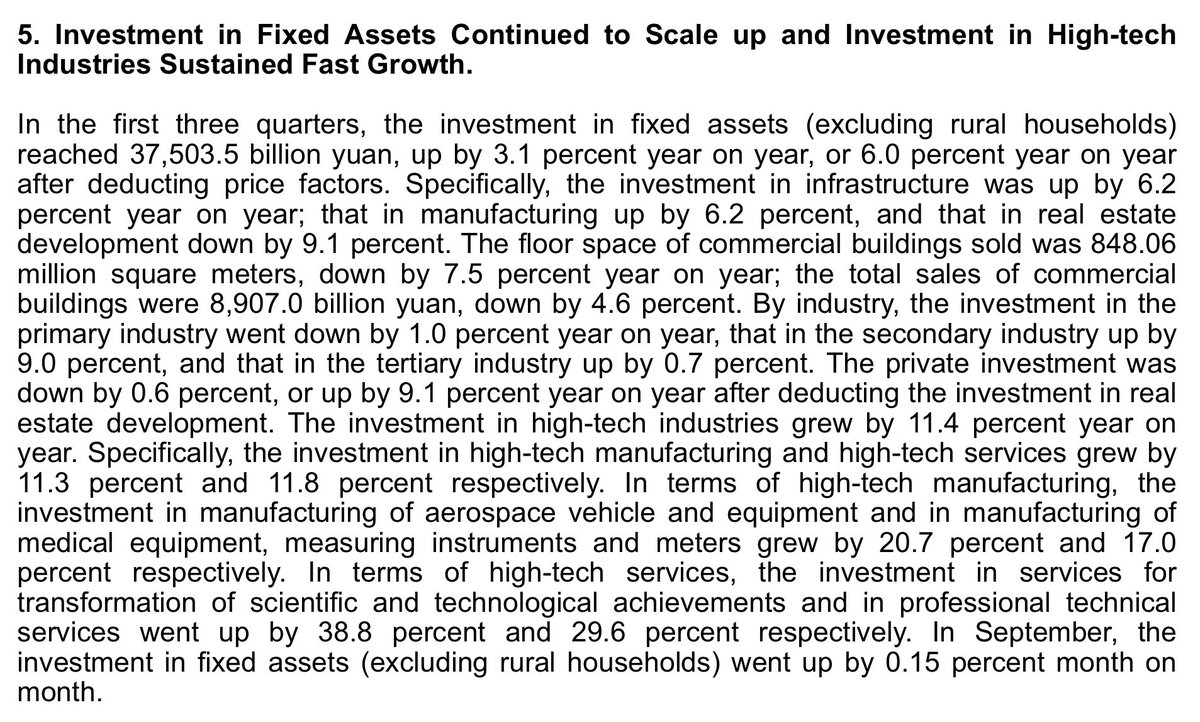

FAI data continues to support the notion of a controlled sectoral transition from the property sector to others, notably high-tech manufacturing and high-tech services.

Infrastructure is also solid and has a few more years of run left before following property.

Infrastructure is also solid and has a few more years of run left before following property.

Loading suggestions...