Mamaearth has filed a RHP and is planning for IPO on 31st October.

The IPO will be mainly subscribed by QIBs (mutual funds) due to SEBI guidelines, and will have a lock in of a year.

I had analysed their DRHP in Dec 22, here are my thoughts on their RHP and current business

The IPO will be mainly subscribed by QIBs (mutual funds) due to SEBI guidelines, and will have a lock in of a year.

I had analysed their DRHP in Dec 22, here are my thoughts on their RHP and current business

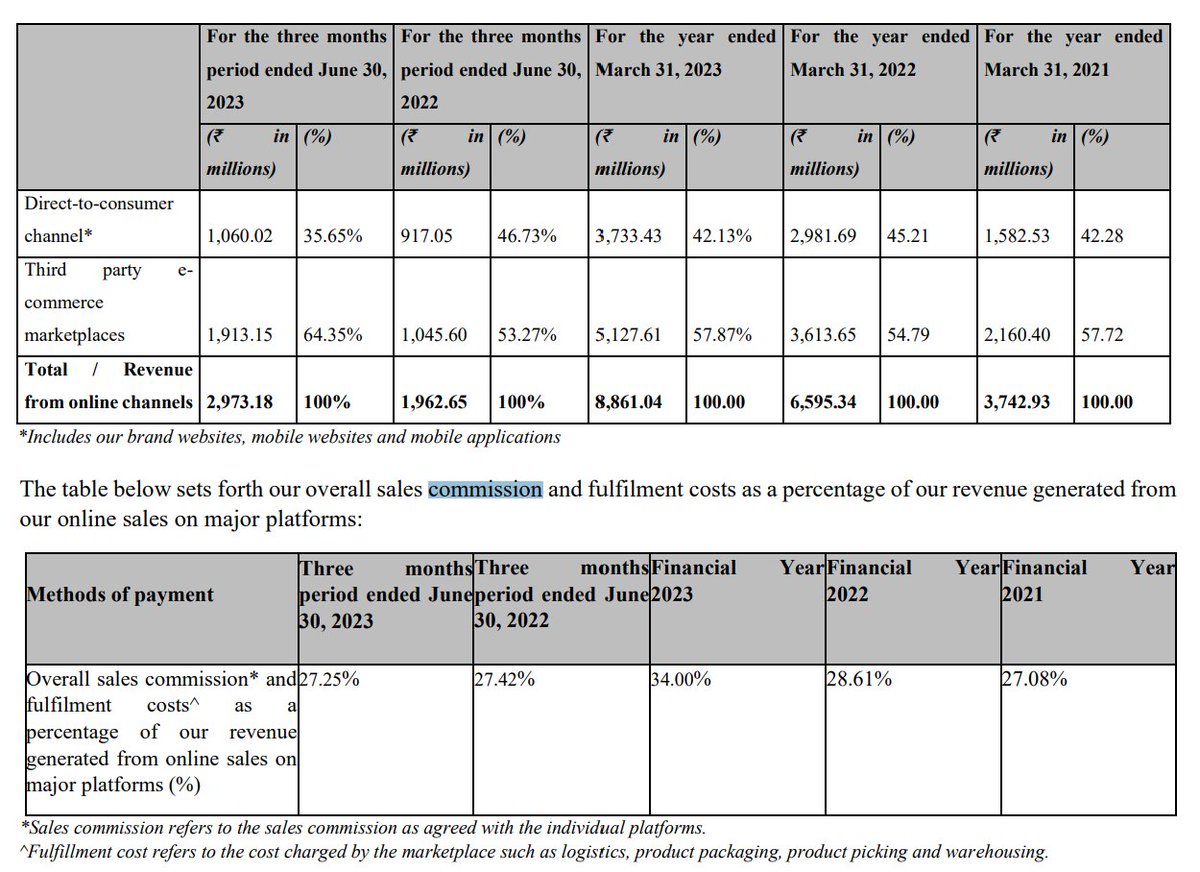

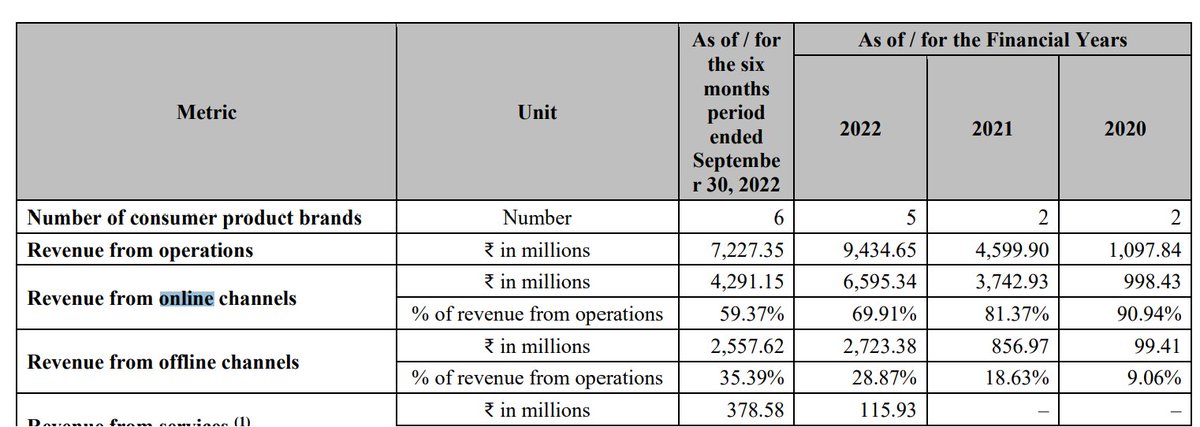

Mamaearth is still and online heavy brand, and further to that 65% of their online sales are on Flipkart/Amazon.

Share of their own website has been constantly reducing from a peak of ~47%

This is because platforms discount products to grab the market.

Share of their own website has been constantly reducing from a peak of ~47%

This is because platforms discount products to grab the market.

Comparing Q1 yoy growth figures, the platform sales grew 90% in Q1 FY24 versus a meagre 10% growth in D2C in same period.

On annualised numbers both the channels grew at CAGR of 54% from FY21 to FY23.

On annualised numbers both the channels grew at CAGR of 54% from FY21 to FY23.

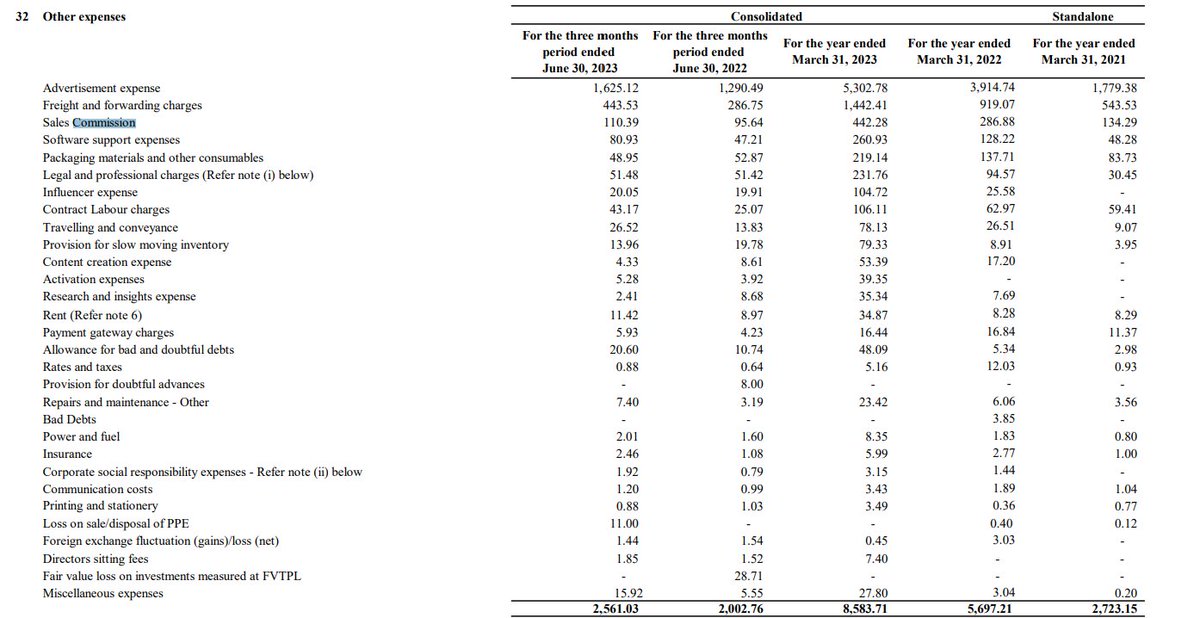

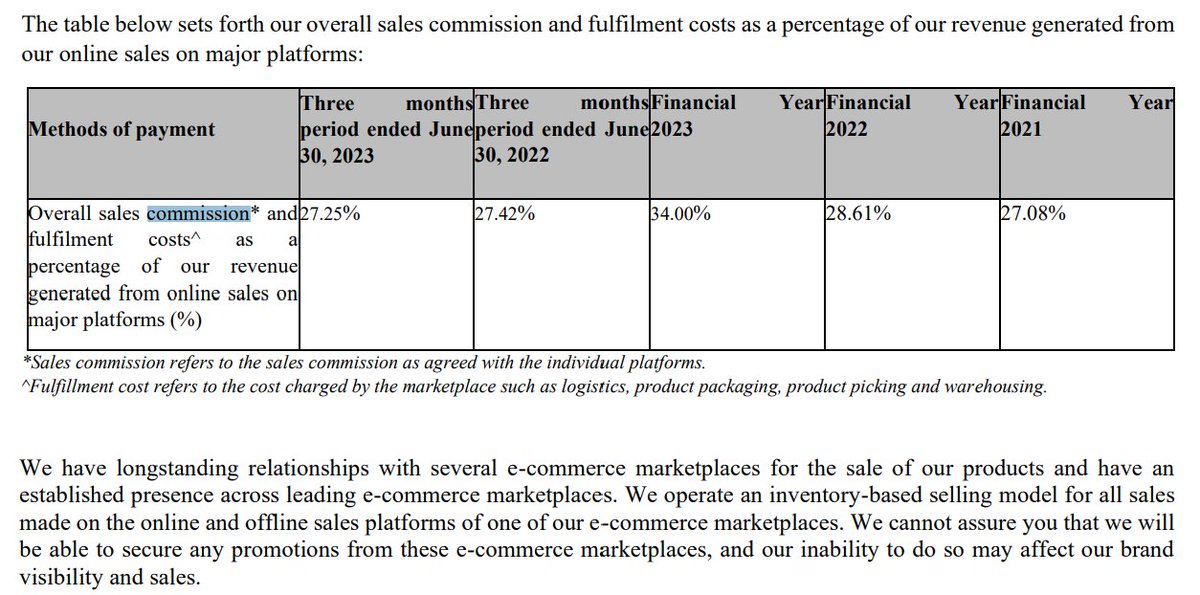

In Q1 FY24 The company has incurred a commission expense of 11 crores on a sale of 190 crores on online channels.

this is ~ 5.75% which is grossly discounted compared to arms length pricing of marketplaces.

In FY23 it is 44 crores on 512 crore, ~8.52%

How long will this last?

this is ~ 5.75% which is grossly discounted compared to arms length pricing of marketplaces.

In FY23 it is 44 crores on 512 crore, ~8.52%

How long will this last?

My entire premise during their Dec 22 DRHP was that Mamaearth is a Flipkart/Amazon discounted brand, where in they are boosting their sales by not charging them fees as per their published rates.

x.com

x.com

This is common, but it is also a risk, platforms can take away this benefit, reduce this or give it to a competitor, the sales can be affected in future.

Contraty to their DRHP, they have disclosed their cost of selling on online channels and also acknowledged the above risk

Contraty to their DRHP, they have disclosed their cost of selling on online channels and also acknowledged the above risk

Mamaearth is a company where the online platforms have promoted them, they are at a risk of decline in case platforms stop promoting them, and the platforms are going all in to capture the consumers.

This creates a huge problem for them to grow at same pace in D2C and offline

This creates a huge problem for them to grow at same pace in D2C and offline

Before going on other points, here are some points which I observe while comparing the DRHP and RHP.

In H1-23 their commission expense was 16 crores for online sales of 429 cr(~4%), however in H2-23 it has almost doubled to 28 crores generating additional sale of 457 crore (~6%)

In H1-23 their commission expense was 16 crores for online sales of 429 cr(~4%), however in H2-23 it has almost doubled to 28 crores generating additional sale of 457 crore (~6%)

While most businesses enjoy economies of scale and reduced expenses with scale, for Mamaearth the increase in revenue and disproportionate increase in commission expense, there is no certainty of the elasticity of this in future

Disc : they havent disclosed platform sales in DRHP

Disc : they havent disclosed platform sales in DRHP

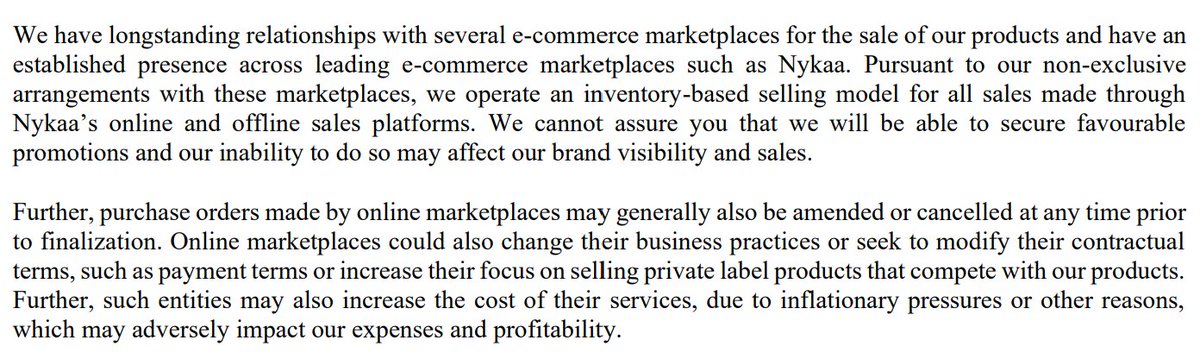

Another interesting thing is observed is the elimination of this paragraph regarding their relation with Nykaa. The excerpt is from their DRHP but is missin in the RHP

It seems Mamaearth and Nykaa have had a change in business terms in current year

It seems Mamaearth and Nykaa have had a change in business terms in current year

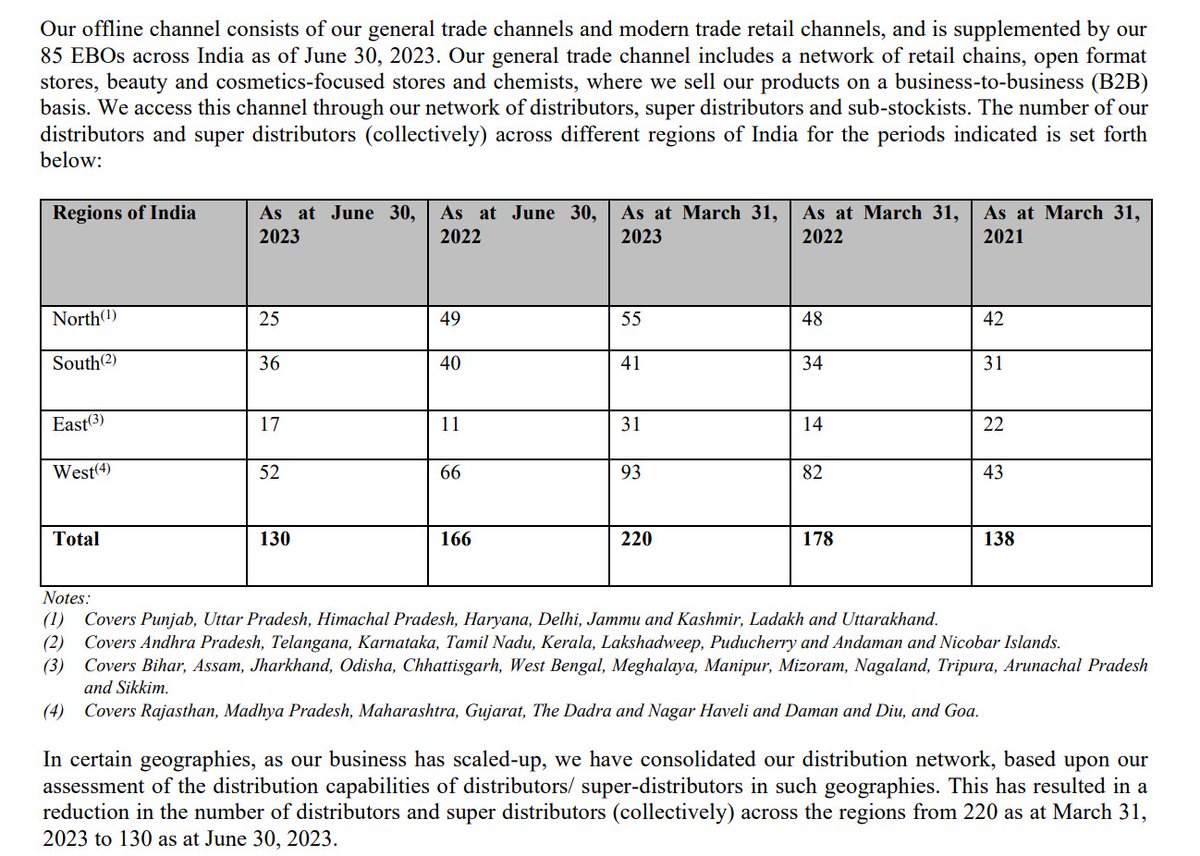

The comany has increased disclosures on their offline business in the RHP compared to DRHP.

Last year I had made observations that how they are unable to generate any cashflow from their offline business

x.com

Last year I had made observations that how they are unable to generate any cashflow from their offline business

x.com

As mamaearth aims to transition into an offline first brand, it has done a lot of corrections since their DRHP

The biggest is by almost halving the number of distributors and super distributors.

The biggest is by almost halving the number of distributors and super distributors.

The company had disclosed offline revenue of 255 crores for H1FY23 in DRHP and 539 crores for FY23 in RHP maintaining a marginal growth in H2FY23

It means that sales on online platforms is still the highest growth channel for them Validating that they are heavily dependent on F/A

It means that sales on online platforms is still the highest growth channel for them Validating that they are heavily dependent on F/A

The biggest difference being seen is in trade receivables, as mentioned during DRHP, in H1FY23 they have trade receivables of 140 crores which has now improved to 127 cr in FY23, 138 cr in Q1FY24

They dont give a break up of offline versus online channel

x.com

They dont give a break up of offline versus online channel

x.com

However it can be judged that there is no relationship between their highest growth channel i.e. platform sales and the trade receivables on various reporting dates.

Offline sales seems to be a very bumply channel which is impacted by the discounts by platforms

Offline sales seems to be a very bumply channel which is impacted by the discounts by platforms

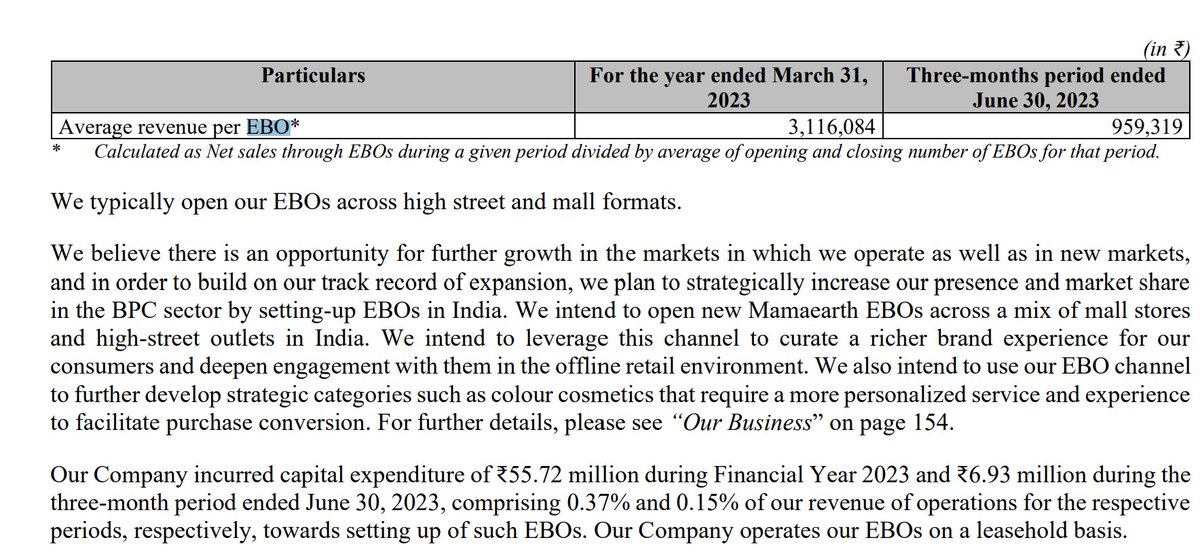

Another sales channel which differentiates Mamaearth from other D2C brands is their EBO network, they had 35 EBOs in Dec 22 which grew to 77 in March 23 and 85 as on today.

EBOs generated 26.5 crore revenue in FY23, ~1.75% of total sales and ~4.85% of offline sales

EBOs generated 26.5 crore revenue in FY23, ~1.75% of total sales and ~4.85% of offline sales

An interesting disclosure in RHP is the average sale per EBO which seems to have a good growth, however they are silent on offline KPIs like same store growth, ASP etc

Regardless of them trying to become aggressive on EBOs and offline, their share in sales and sales growth is the least, they are a new business segment and there is no certainity of these channels to become their highest grossing channels

Bottomline still remains that Mamaearth is a Flipkart/Amazon dependent brand.

Mutual funds will subscribe to the IPO and it will be successful, best of luck to the team and investors.

Most important if the 30x ROI that they are giving to early investors.

Mutual funds will subscribe to the IPO and it will be successful, best of luck to the team and investors.

Most important if the 30x ROI that they are giving to early investors.

An interesting revenue item is "sales from services" which was 67 crores ~5% of total revenue in FY23 and 11 crores ~2.5% in Q1 24

Not sure how stable this revenue is and the RHP and DRHP is silent on its future

Not sure how stable this revenue is and the RHP and DRHP is silent on its future

Loading suggestions...