RBI increases risk weights for banks and NBFCs. This is pretty big!

1) All consumer credit (other than housing, vehicle, gold, edu and MFI loans) see an increase in risk weight to 125% from 100%

What this means is:

1) All consumer credit (other than housing, vehicle, gold, edu and MFI loans) see an increase in risk weight to 125% from 100%

What this means is:

In effect, if a bank has 20% CAR for personal loans (unsecured) or loan against fd/stocks, then it's lent Rs. 100 for Rs. 20 in capital. Now that Rs. 100 will be counted as Rs. 125 (125% risk weight) so the CAR falls to 16%.

Banks and NBFCs will now see much lower CARs.

Banks and NBFCs will now see much lower CARs.

2) NBFC loans will also see an increase of risk weight to 125%. This affects most consumer lending NBFCs and nearly all fintech players.

3) Credit card receivables for banks RW up to 150% (from 125%) and for the two nbfcs that can issue credit cards it's up to 125% from 100%

3) Credit card receivables for banks RW up to 150% (from 125%) and for the two nbfcs that can issue credit cards it's up to 125% from 100%

See how it affects SBI cards:

- SBI Cards had CC receivables of 45,000 cr. with 23% CAR

- So 10,500 cr. in capital (23% of 45Kcr)

- Increase RW to 125% means 45K cr=56K cr risk weighted assets

- Capital is same, 10.5K cr. so CAR=Capital/RWA = 18%

- SBI Cards had CC receivables of 45,000 cr. with 23% CAR

- So 10,500 cr. in capital (23% of 45Kcr)

- Increase RW to 125% means 45K cr=56K cr risk weighted assets

- Capital is same, 10.5K cr. so CAR=Capital/RWA = 18%

This means that if SBI Cards wants to grow, and keep high CARs (min is 15% I think?) theyll need to raise capital and dilute.

Which means for the same profit = higher capital. Means, lower ROEs.

Which means for the same profit = higher capital. Means, lower ROEs.

Impacting this further is: bank loans to NBFCs which are currently only based on ratings (unrated is 100%), which is like

- AAA (20%)

- AA (30%)

- A (50%)

Everyone else is 100% or more

All this goes up by 25%, so AAA is 45%, AA 55%, A 75% for NBFCs. Whoa!

- AAA (20%)

- AA (30%)

- A (50%)

Everyone else is 100% or more

All this goes up by 25%, so AAA is 45%, AA 55%, A 75% for NBFCs. Whoa!

Housing Fin NBFCs and priority sector NBFCs are exempt from the higher risk weights.

If banks have to put down more capital to lend to NBFCs, they will charge higher interest rates (or not lend)

Means NBFCs will issue more bonds, and yields should increase.

If banks have to put down more capital to lend to NBFCs, they will charge higher interest rates (or not lend)

Means NBFCs will issue more bonds, and yields should increase.

Lastly, every bank and NBFC needs to set up a limit for unsecured consumer credit. Cannot be changed easily.

Top up loans for cars (and depreciating assets) to be considered unsecured. Those calls to top up your car loan? Will slow.

Top up loans for cars (and depreciating assets) to be considered unsecured. Those calls to top up your car loan? Will slow.

This will also increase the rate of interest charge by banks and NBFCs to consumers. Expect an increase in loan interest rates for personal loans, and higher rejection rates.

Expect NBFCs to try and raise capital as CARs will drop across the board, by 3 to 4%.

Hurt fintechs.

Expect NBFCs to try and raise capital as CARs will drop across the board, by 3 to 4%.

Hurt fintechs.

The stock prices should react tomorrow, but the banks and NBFCs with low CARs (compared to statutory requirements) will be hurt the most.

Except of course PSU banks who seem to be unfazed with anything :)

Except of course PSU banks who seem to be unfazed with anything :)

Credit cards have seen scorching credit growth on receivables - at 30%+ per year.

Now at over 2.17 lakh crores. This is probably causing part of the problem:

Now at over 2.17 lakh crores. This is probably causing part of the problem:

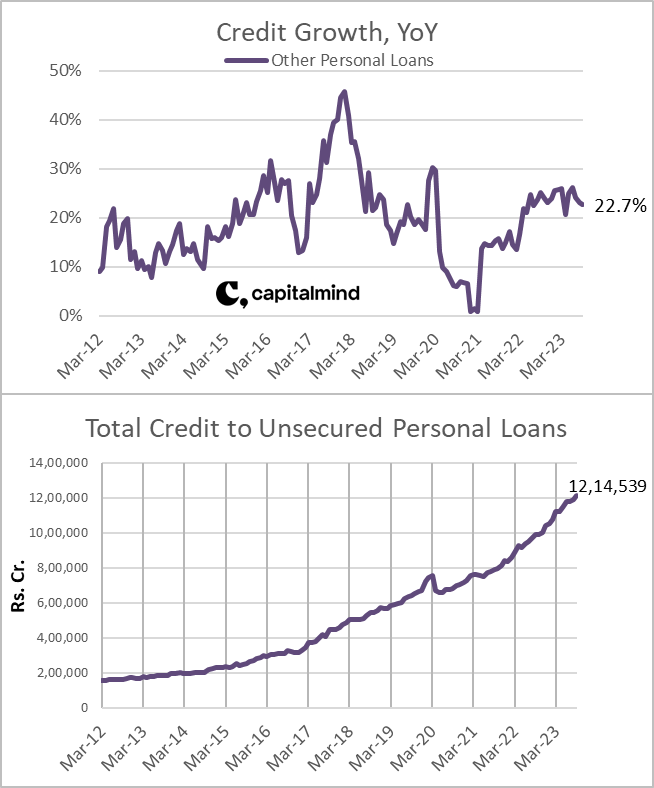

Unsecured personal loans have also been growing strongly, at 23%, and have crossed 12 lakh crores - second largest single sector of lending to individuals after housing.

Fintech lenders operate in this space, primarily.

Fintech lenders operate in this space, primarily.

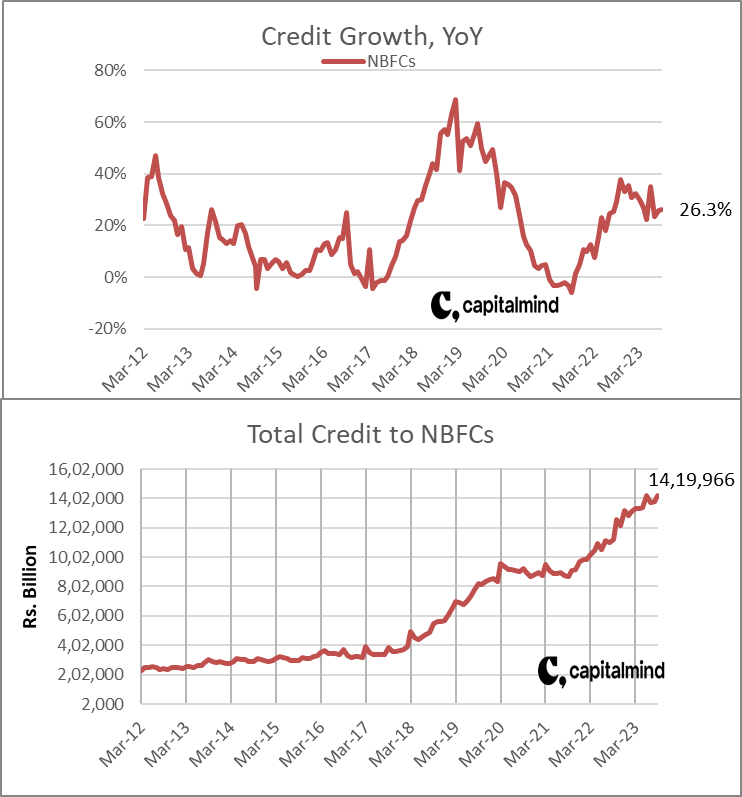

Bank lending to NBFCs also has seen similar growth. The higher risk weights is a double whammy - banks have to put higher capital of their own, and then NBFCs further need more capital to lend.

Will hurt all lenders including fintech that have large bank borrowings:

Will hurt all lenders including fintech that have large bank borrowings:

Twitter space on this? Long time no space.

Have to do this tomorrow morning. Cricket is important :)

I did one anyhow.

More: RBI has actually not excluded banks lending for microfinance or priority sector loans from this higher risk weight. Only edu/gold/housing/vehicle loans are exempt from the 125% risk weight.

Only NBFCs get a lower risk weight on microfinance loans. Which means if an NBFC sells a microfinance loan pool to a bank, the bank has to put 125% risk weight against it (but if it didn't sell, the NBFC would only need 100% risk weight)

Gonna be messy.

Only NBFCs get a lower risk weight on microfinance loans. Which means if an NBFC sells a microfinance loan pool to a bank, the bank has to put 125% risk weight against it (but if it didn't sell, the NBFC would only need 100% risk weight)

Gonna be messy.

Loading suggestions...