Last week, some BIG changes were rolled out in 3 savings schemes:

- PPF

- Senior Citizen Savings Scheme (SCSS)

- Post Office Fixed Deposit

Some of these changes bring cheer

But a few are also unsettling, especially the one in FDs.

Let’s look at them in detail.

A 🧵

- PPF

- Senior Citizen Savings Scheme (SCSS)

- Post Office Fixed Deposit

Some of these changes bring cheer

But a few are also unsettling, especially the one in FDs.

Let’s look at them in detail.

A 🧵

1. PPF

Let’s discuss some basics first, which are relevant to the recent changes.

PPF matures after 15 years.

Post that, you can extend it in the block of 5 years.

So, you can stay invested in PPF for as many years as you want.

Let’s discuss some basics first, which are relevant to the recent changes.

PPF matures after 15 years.

Post that, you can extend it in the block of 5 years.

So, you can stay invested in PPF for as many years as you want.

Let’s say your PPF matured after 15 years.

You decide to extend it.

So, you’ll need to remain invested for another 5 years.

What’s your total investment period?

It’s 15 + 5 = 20 years

You decide to extend it.

So, you’ll need to remain invested for another 5 years.

What’s your total investment period?

It’s 15 + 5 = 20 years

Say you need the entire money in the PPF account before the completion of 20 years.

So, you decide to close it in the 17th year.

In this case, you’ll need to pay a penalty.

How much?

It’s 1%.

And it’s applicable on the interest that you have received for all 17 years.

So, you decide to close it in the 17th year.

In this case, you’ll need to pay a penalty.

How much?

It’s 1%.

And it’s applicable on the interest that you have received for all 17 years.

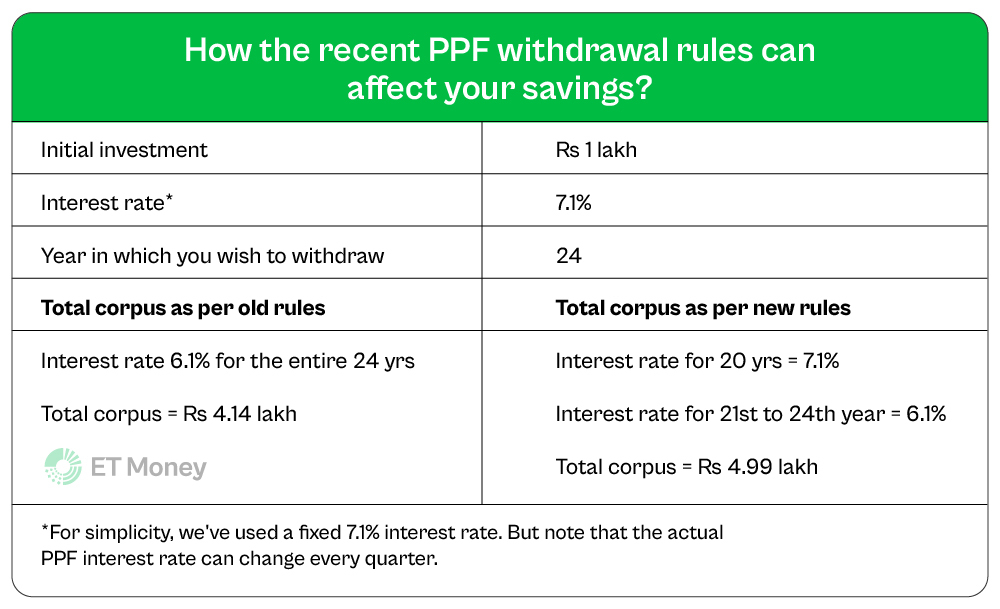

The penalty was quite high.

The government has rationalised it.

Now, you still need to pay the 1% penalty.

But it’s only on the interest you receive after PPF maturity.

In our example, the penalty will be on the interest received in the 16th and 17th years.

The government has rationalised it.

Now, you still need to pay the 1% penalty.

But it’s only on the interest you receive after PPF maturity.

In our example, the penalty will be on the interest received in the 16th and 17th years.

Simply put, now, the penalty applies only for the interest received during the extension.

It won't affect the interest earned in the first 15 years or any 5-year extension that you complete.

To understand this even better, look at the example in the table below.

It won't affect the interest earned in the first 15 years or any 5-year extension that you complete.

To understand this even better, look at the example in the table below.

2. SCSS

There were several changes in SCSS.

But 4 of them are notable.

UPDATE 1: Senior citizens can now invest in SCSS for as many years as they wish.

EARLIER RULE: They could invest for a maximum of 8 years (5 years and then extend it for 3 years only once).

There were several changes in SCSS.

But 4 of them are notable.

UPDATE 1: Senior citizens can now invest in SCSS for as many years as they wish.

EARLIER RULE: They could invest for a maximum of 8 years (5 years and then extend it for 3 years only once).

UPDATE 2: It’s about pre-mature withdrawals after you extend the SCSS for 3 years.

You can now withdraw at any time.

EARLIER RULE: During the 3-year extended period, you could withdraw only after the completion of one year without penalty.

But there’s a catch…

You can now withdraw at any time.

EARLIER RULE: During the 3-year extended period, you could withdraw only after the completion of one year without penalty.

But there’s a catch…

Earlier, there was no penalty for pre-mature withdrawal.

But now there will be a 1% penalty when you withdraw prematurely at any time through the 3-year tenure.

So, you can access the money in the 6th year, which wasn't there before.

But you need to pay a penalty.

But now there will be a 1% penalty when you withdraw prematurely at any time through the 3-year tenure.

So, you can access the money in the 6th year, which wasn't there before.

But you need to pay a penalty.

UPDATE 3: Allows more time for people to invest their retirement benefits in SCSS.

Retirees (between 55 and 60) can now invest their retirement benefits in SCSS within 3 months of receiving them.

EARLIER RULE: They had to do it within 1 month.

Retirees (between 55 and 60) can now invest their retirement benefits in SCSS within 3 months of receiving them.

EARLIER RULE: They had to do it within 1 month.

UPDATE 4: Widens the SCSS eligibility for spouses of govt employees, aged 50 or more, who die on duty.

Even if the spouse is not a senior, he or she can invest.

This applies to both central & state govt employees eligible for retirement benefits or death compensation.

Even if the spouse is not a senior, he or she can invest.

This applies to both central & state govt employees eligible for retirement benefits or death compensation.

3. 5-YEAR POST OFFICE DEPOSITS

EARLIER RULE: If you closed a 5-year deposit after 4 years, the interest rate of a 3-year deposit (7% at present) was used for interest calculation.

NEW RULE: Now, interest would be payable at the Savings Account rate (4% at present).

EARLIER RULE: If you closed a 5-year deposit after 4 years, the interest rate of a 3-year deposit (7% at present) was used for interest calculation.

NEW RULE: Now, interest would be payable at the Savings Account rate (4% at present).

We put a lot of effort into creating such informative threads.

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the first tweet. 👇

x.com

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the first tweet. 👇

x.com

Loading suggestions...