Some useful options market info for people interested in market mechanics. 🧵

How large is the options market and how important is it? The options contracts open today are worth aggregate roughly $400B. The stock market is $45.5T. This makes the options market worth about 1% of the total US stock market. Seems unimportant, right?

Not so fast. Options contracts have leverage that the market makers have to hedge. The amount they have to hedge is the option delta. The gross market delta that all contracts represent is about $3T, or 6.5% of the stock market. Okay getting more important.

Contracts are also traded in very large numbers, especially on $SPX index options. Comparing all of the volume for the stocks in the S&P 500 to the delta traded on stock shows that 79% of daily volume can be attributed to delta hedging.

Volume on index options like $SPX are about 80% of the dollars traded on the underlying, and index futures volume traded accounts for 400% of the underlying volume. Obviously a lot of this delta is netted out so it's not all hedged, but it's clear to see that...

Volume on index and equity options, and futures trading *IS* the market. Underlying volume on stocks themselves, not associated with hedging activity, is estimated to be on the order of 1% of all trading activity. So understanding these derivatives is vital.

All told, daily volumes on these contracts total roughly $400B per day in trading activity. Given a leverage ratio on the order of 8 or so, that's $50B a day moving the market, mostly in derivatives trading.

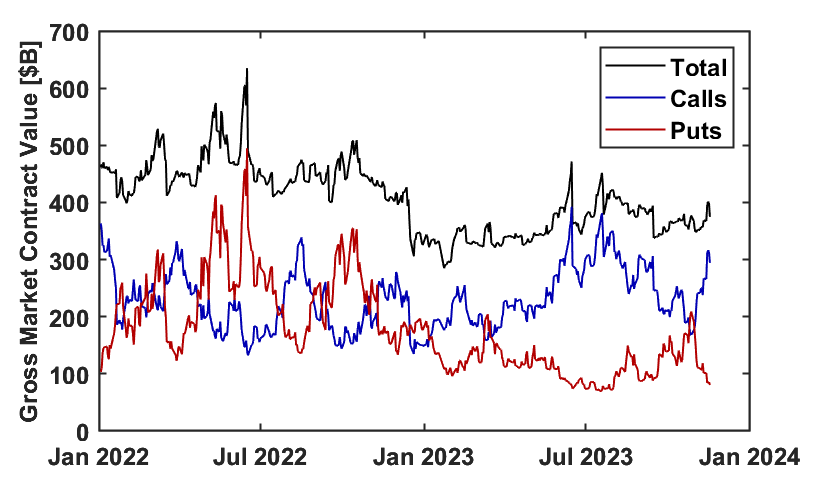

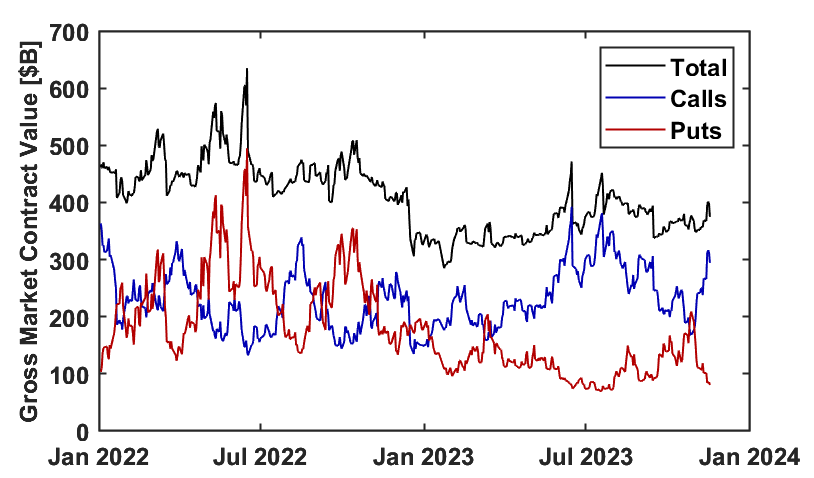

Alright now that we know the scope let's dig a little deeper into this information. First thing I will note is that the total value of options contracts on chain is actually down from last year, but it's mostly steady in the $300-500B range.

Despite the total value remaining similar, the composition of value in puts or calls varies substantially. In 2022, both puts and calls were evenly weighted with heavy oscillations between them. These oscillations were the source of market volatility that year.

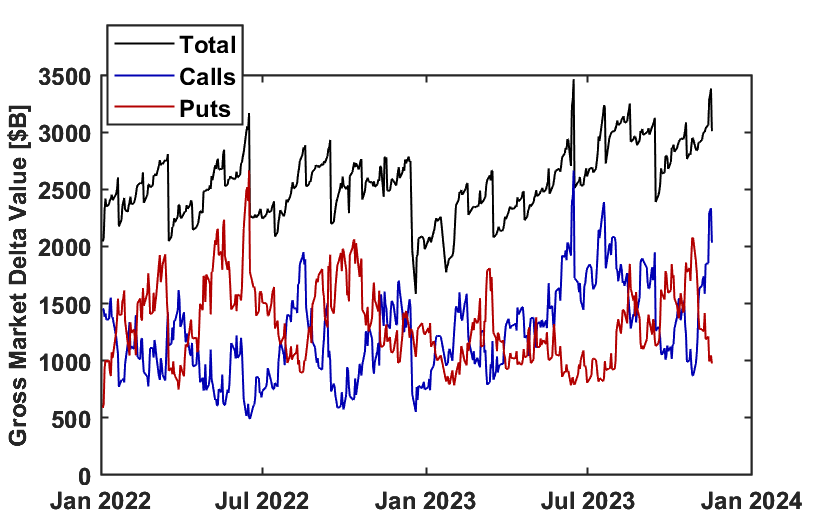

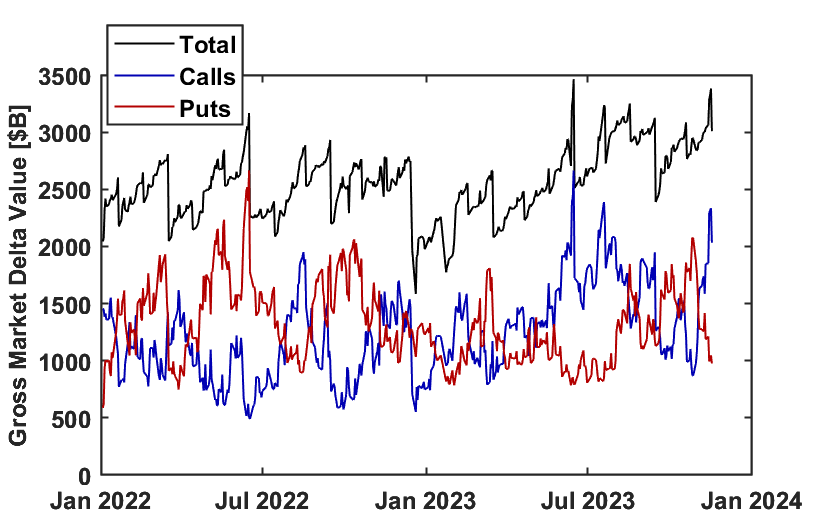

In 2023, things become much different. Throughout most of the year, call values have consistently held above puts. You may think that this means that calls are running the show...

But in gross delta value we see a similar behavior to 2022 where the value of puts and calls oscillate about a similar value. What's the discrepancy here? In short, leverage.

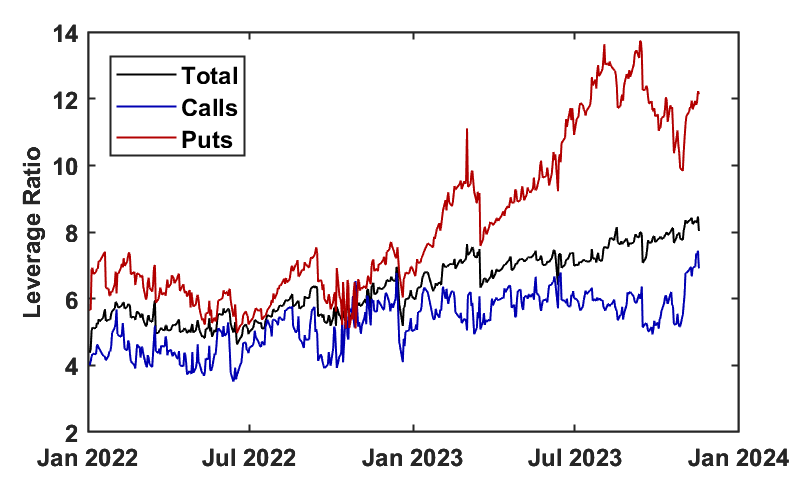

The ratio of delta to contract value shows you the leverage the instruments provide. As can be seen below, call leverage has primarily stayed contained between 4-6. Puts on the other hand, rocketed from 7 last year to 10-14x this year.

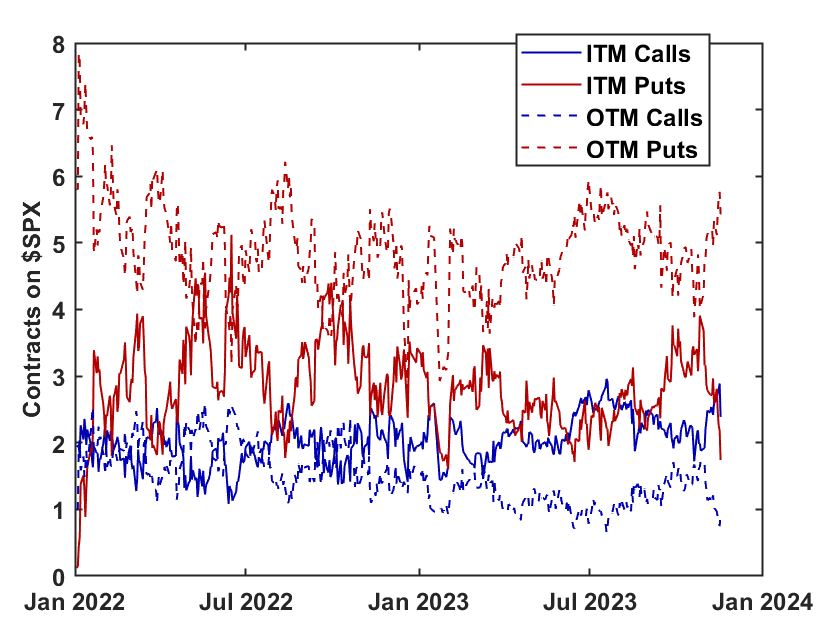

Looking at just the number of contracts, there are twice as many puts as there are calls. Further, 75% of these puts are OTM or out of the money, meaning they are plentiful, cheap, and highly levered. This is typically what happens when puts are heavily sold to the market maker

This is commonly done to earn steady income, particularly when markets aren't going up but otherwise not going down, like now. The problem is that these sold puts have very dangerous risk/reward if markets become too volatile, and become self defeating in large numbers.

As people create generous supply of puts by selling them, they drop the price on the market. Every subsequent sold put is riskier with less return.

We are in a highly leveraged environment, where one crazy swing can unwind this trade.

We are in a highly leveraged environment, where one crazy swing can unwind this trade.

What's interesting is that we just had a massive rally on the back primarily of bought calls over the last few weeks. The rally was so intense, that real volatility is larger than the volatility priced by the sold puts.

If this rally pulls back hard enough, it will squeeze the sold puts even harder than anything we saw in 2022. The biggest move was 20% in october 2022. Given leverage is 70% larger now on sold puts, a squeeze of similar magnitude would land $SPX at $3000.

Now obviously there is a low probability of this happening, and there are structural reasons on the chain for why it will be hard to go below $3600, we can get there just from options volatility.

Even if this imbalance doesn't unwind violently, there's not much upside beyond $4600 at the moment. Odds are we head down from here. We'll see!

Loading suggestions...