Average True Range (ATR) is an essential technical indicator for volatility signals.

In 3 minutes, I'll teach you what took 3 months to learn.

Let's dive in. 🧵

#Quant #Trading #Algorithms #Python

In 3 minutes, I'll teach you what took 3 months to learn.

Let's dive in. 🧵

#Quant #Trading #Algorithms #Python

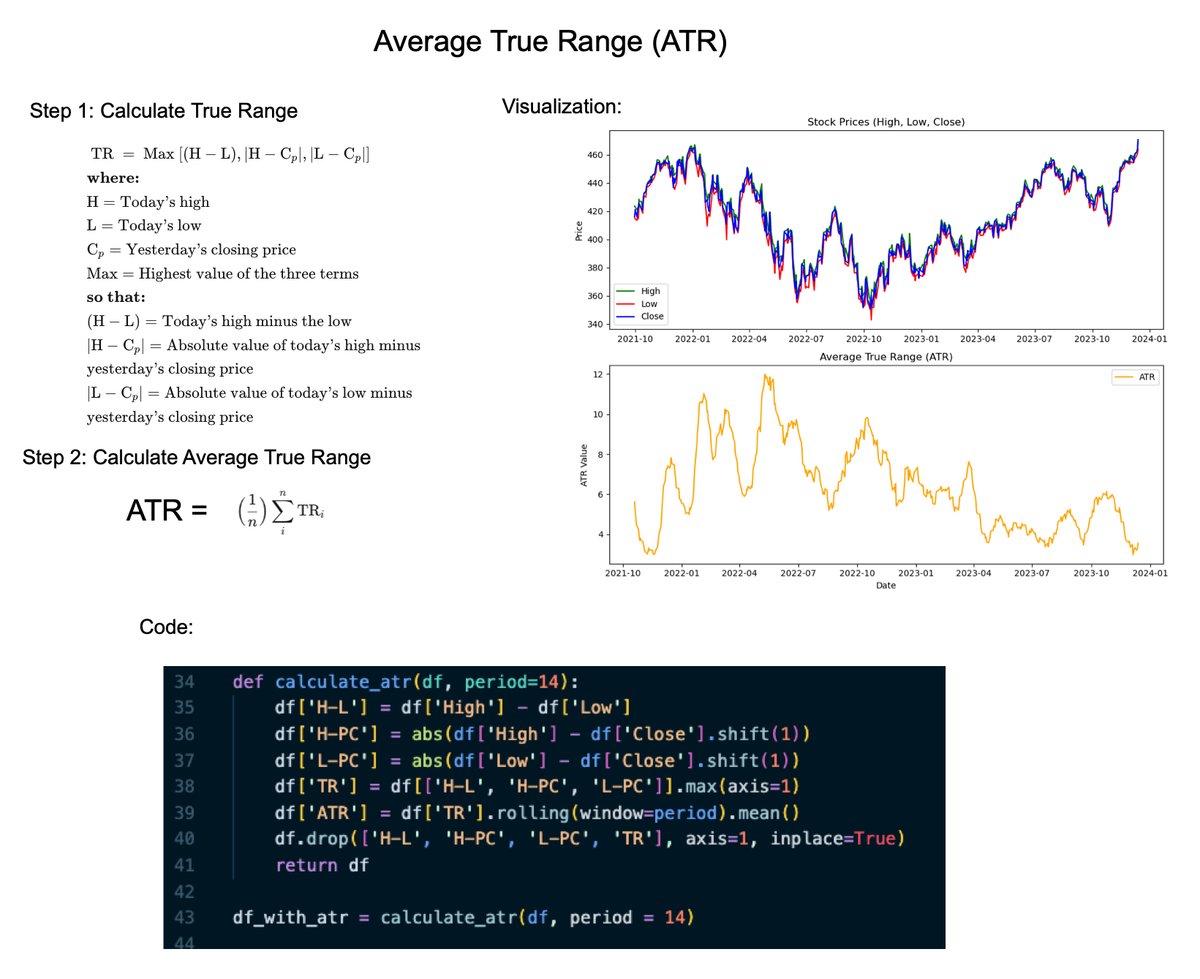

1. The Average True Range (ATR) is a technical analysis indicator used to measure market volatility.

It was introduced by J. Welles Wilder Jr. in his 1978 book "New Concepts in Technical Trading Systems."

It was introduced by J. Welles Wilder Jr. in his 1978 book "New Concepts in Technical Trading Systems."

2. Usage in Trading:

ATR does not provide an indication of price direction, instead it measures volatility.

High ATR values indicate high volatility and low ATR values indicate low volatility.

ATR does not provide an indication of price direction, instead it measures volatility.

High ATR values indicate high volatility and low ATR values indicate low volatility.

3. How to Develop Signals

Traders might use this information to:

- Adjust stop-loss orders

- Size Positions

- Entry/Exit Signals

Note- ATR is often used in combination with other Technical Signals (e.g. trend, price, and volume filters).

Traders might use this information to:

- Adjust stop-loss orders

- Size Positions

- Entry/Exit Signals

Note- ATR is often used in combination with other Technical Signals (e.g. trend, price, and volume filters).

4. Calculation

Calculating ATR involves 2 steps.

First calculate the True Range.

Second, calcualte the Average True Range which is just an average over the last N true range.

Calculating ATR involves 2 steps.

First calculate the True Range.

Second, calcualte the Average True Range which is just an average over the last N true range.

5. Code in Python

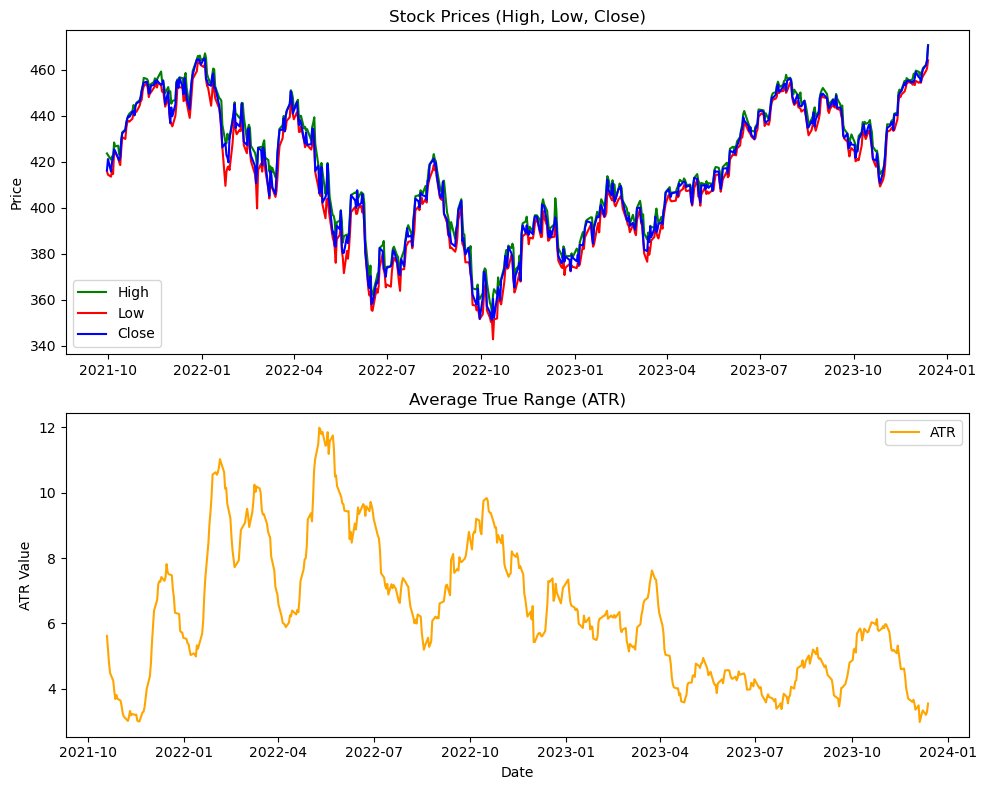

We can calculate the True Range (TR) in python.

Then simply use the pandas rolling mean, which yields the Average True Range (ATR).

We can calculate the True Range (TR) in python.

Then simply use the pandas rolling mean, which yields the Average True Range (ATR).

Want to see ATR in action (full Python code)?

Join 5100+ on our Quant Science Newsletter.

👉The next algorithmic trading tutorial uses ATR (drops Sunday): learn.quantscience.io

Join 5100+ on our Quant Science Newsletter.

👉The next algorithmic trading tutorial uses ATR (drops Sunday): learn.quantscience.io

Loading suggestions...