Who buys lavish apartments for Rs 10-20 CRORES?

You may be aware of their names through news reports.

But what you may not know is the trick they use to buy those houses.

So what is it?

Sell equities, use the gains to buy a property and pay ZERO tax.

A detailed 🧵

You may be aware of their names through news reports.

But what you may not know is the trick they use to buy those houses.

So what is it?

Sell equities, use the gains to buy a property and pay ZERO tax.

A detailed 🧵

Let us first show you how it works with an example.

You sell your equity investments. Profits = Rs 51 lakh. Of this, Rs 1 lakh will be tax-free.

You will pay 10% tax on Rs 50 lakh. That comes to Rs 5 lakh. But this can be ZERO.

Details in the next tweet. 👇

You sell your equity investments. Profits = Rs 51 lakh. Of this, Rs 1 lakh will be tax-free.

You will pay 10% tax on Rs 50 lakh. That comes to Rs 5 lakh. But this can be ZERO.

Details in the next tweet. 👇

Paying ZERO tax is possible thanks to the Section 54F of the IT Act.

Basically, the law allows you to save tax if you buy a house using profits earned by selling some investments.

These could be stocks, mutual funds, your stake in a company, and even gold.

Basically, the law allows you to save tax if you buy a house using profits earned by selling some investments.

These could be stocks, mutual funds, your stake in a company, and even gold.

So, that’s why many founders buy luxury houses when exit their businesses.

That’s also the reason why you see more people buying expensive flats when stock markets do well.

But, like all laws, there are some conditions.

Here are 7 important points that we think you must know.

That’s also the reason why you see more people buying expensive flats when stock markets do well.

But, like all laws, there are some conditions.

Here are 7 important points that we think you must know.

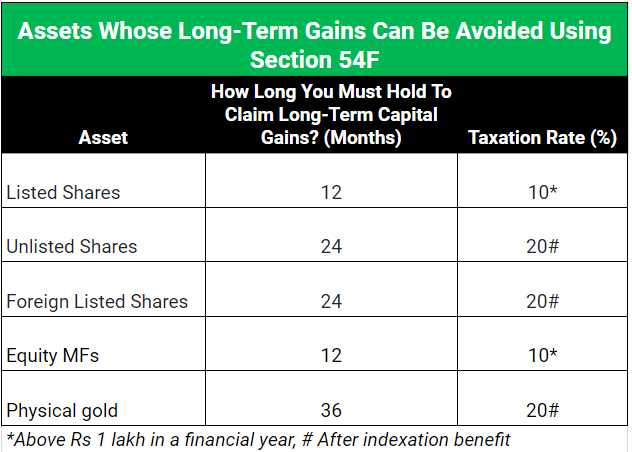

POINT 1: Tax benefits are available on select investment avenues only.

Some of them include listed & unlisted stocks, foreign shares, equity funds, and physical gold.

Also, the capital gains need to be ‘long-term’.

Details in image 👇

Some of them include listed & unlisted stocks, foreign shares, equity funds, and physical gold.

Also, the capital gains need to be ‘long-term’.

Details in image 👇

POINT 2: You have to utilize the entire corpus you receive, not just profits.

Suppose you had invested Rs 50 lakh in stocks.

And you made a gain of Rs 40 lakh after 5 years.

You need to use the entire Rs 90 lakh (principal + gains) to buy a residential property.

Suppose you had invested Rs 50 lakh in stocks.

And you made a gain of Rs 40 lakh after 5 years.

You need to use the entire Rs 90 lakh (principal + gains) to buy a residential property.

POINT 3: You need to utilize the corpus within a specific time:

A. Buy a house within 2 years of selling your assets

B. If building a house, construct within 3 years

C. You can also pay ZERO tax if you bought a residential property one year before the sale of the asset

A. Buy a house within 2 years of selling your assets

B. If building a house, construct within 3 years

C. You can also pay ZERO tax if you bought a residential property one year before the sale of the asset

POINT 4: On the day you sell your assets, you shouldn’t be owning more than one residential property.

POINT 5: The money must only be used for a house.

You cannot invest in land or commercial property.

You cannot invest in land or commercial property.

POINT 6: After purchase, you must remain invested in the house for at least 3 years.

You cannot just sell the house and moonwalk away.

If you sell the house before the 3 years, you will need to pay the tax, penalty, and interest on the LTCG from the date of the sale.

You cannot just sell the house and moonwalk away.

If you sell the house before the 3 years, you will need to pay the tax, penalty, and interest on the LTCG from the date of the sale.

POINT 7: One important point before we wrap up.

Many individuals took advantage of this tax hack extensively.

So, the government has put some restrictions.

There’s a cap of Rs 10 crore on the tax exemption.

An example should make this point clear. 👇

Many individuals took advantage of this tax hack extensively.

So, the government has put some restrictions.

There’s a cap of Rs 10 crore on the tax exemption.

An example should make this point clear. 👇

Say, you sold your investments for Rs 20 crores.

You buy a property for Rs 20 crores.

You will get tax exemption only on the first Rs 10 crores.

For the remaining Rs 10 crores, you have to pay tax.

You buy a property for Rs 20 crores.

You will get tax exemption only on the first Rs 10 crores.

For the remaining Rs 10 crores, you have to pay tax.

Wrap up

Sec 54F is a significant reason you often hear about rich people scooping up fancy homes.

Retail investors can also use it to their advantage, too.

You can save for the down payment using MFs & pay no tax on it.

But, keep the above-mentioned 7 points in mind.

Sec 54F is a significant reason you often hear about rich people scooping up fancy homes.

Retail investors can also use it to their advantage, too.

You can save for the down payment using MFs & pay no tax on it.

But, keep the above-mentioned 7 points in mind.

Investing in real estate (other than staying in it) has its own risks.

To save, say Rs 10 lakh in tax, you can end up buying Rs 1 crore of illiquid real estate with limited potential for returns & low rental yields.

Factor in everything before making a decision.

To save, say Rs 10 lakh in tax, you can end up buying Rs 1 crore of illiquid real estate with limited potential for returns & low rental yields.

Factor in everything before making a decision.

We put a lot of effort into creating such informative threads.

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the first tweet. 👇

x.com

So, if you find this useful, show some love. ❤️

Please like, share, and retweet the first tweet. 👇

x.com

Loading suggestions...